|

시장보고서

상품코드

1684586

헬스케어 포장 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Healthcare Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

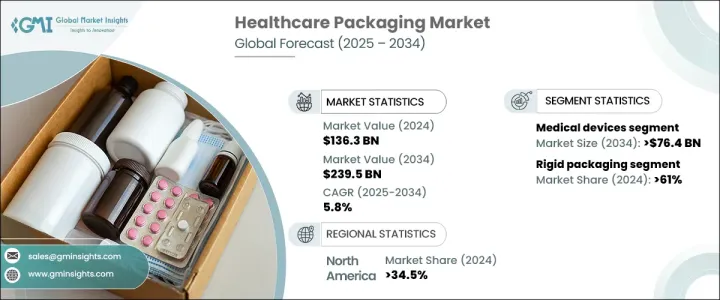

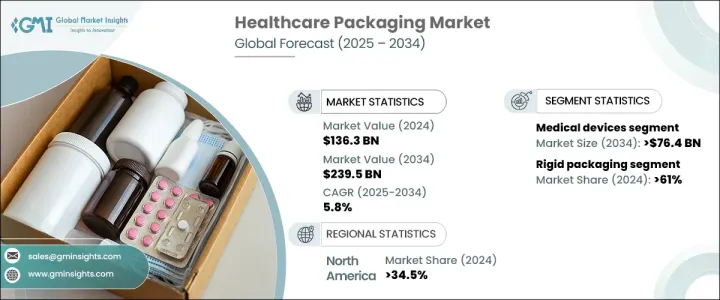

세계의 헬스케어 포장 시장은 2024년에 1,363억 달러였고, 2025년부터 2034년까지 CAGR 5.8%로 안정된 성장이 예측되고 있습니다.

이 시장의 주요 성장 요인은 혁신적이고 안전하며 지속 가능한 포장 솔루션에 대한 요구가 커지고 있는 것입니다. 최근 의료 산업은 생물 제제 및 특수 의약품의 특수한 요구에 대응하기 위해 고급 포장 기술을 채택하고 있습니다. 이와 병행하여 개발도상지역에서 건강관리에 대한 접근성이 개선되고 있으며, 효과적이고 효율적인 포장에 대한 수요가 높아지고 있습니다.

또한 의약품 전자상거래의 상승은 안전한 운송 및 보관을 지원하는 포장 솔루션에 새로운 기회를 제공합니다. 스마트 포장 통합은 정확한 투여와 실시간 정보 제공으로 환자의 컴플라이언스를 더욱 강화합니다. 이 추세는 공급망 효율을 최적화하고 비용을 절감하며 제품 추적성을 향상시킵니다. 헬스케어 분야가 진화를 계속하고 있는 가운데, 포장 시장은 의약품 및 의료 제품의 안전성과 품질을 확보하는데 있어서 중요한 역할을 한다고 생각됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1,363억 달러 |

| 예측 금액 | 2,395억 달러 |

| CAGR | 5.8% |

헬스케어 포장 시장은 단단한 포장과 연질 포장의 두 가지 주요 부문으로 나뉩니다. 경질 포장이 최대 시장 점유율을 차지했으며 2024년에는 61%를 차지했습니다. 이 부문의 이점은 제품을 보호하고 섬세한 건강 관리 제품의 무결성을 유지하는 능력 때문입니다. 경질 포장에는 폴리프로필렌이나 폴리카보네이트와 같은 고성능 재료가 사용되는 경우가 많으며, 엄격한 의료 컴플라이언스 규정을 충족하는 데 필수적입니다. 성형 기술의 지속적인 발전으로 제조업체는 가볍고 내구성있는 용기를 제조 할 수 있으며 필요한 강도와 보호를 유지하면서 운송 비용을 줄이는 데 기여합니다. 이러한 재료와 디자인의 지속적인 진화로 인해 경질 포장은 많은 건강 관리 응용 분야에서 선호되는 옵션입니다.

최종 사용자 용도를 살펴보면 헬스케어 포장 시장은 의약품과 의료기기로 분류됩니다. 의료기기 분야는 가장 높은 성장률이 예상되고 CAGR은 6.5%로 예측되고 있습니다. 이 부문은 의료기기 기술의 혁신과 무균, 내구성, 사용자 친화적인 포장 솔루션에 대한 수요 증가로 인해 2034년까지 764억 달러에 이를 것으로 예상됩니다. 의료 장비 포장은 진단 및 수술 도구에서 임플란트에 이르기까지 광범위한 제품의 무균성, 내구성 및 사용 용이성과 같은 엄격한 요구 사항을 충족해야 합니다. 보다 선진적인 의료기기가 시장에 등장함에 따라 포장 솔루션도 그에 따라 진화하여 최대한의 안전성과 기능성을 확보해야 합니다.

북미에서는 헬스케어 포장 시장이 우위를 유지하고 2024년에는 시장 점유율의 34.5%를 차지할 것으로 예상됩니다. 미국에서는 의료 제품의 기술 진보와 환자 안전의 중요성이 증가함에 따라 건강 관리 분야에서 첨단 포장 솔루션에 대한 수요가 크게 증가하고 있습니다. 변조 방지 포장이나 어린이가 열기 어려운 포장과 같은 기술 혁신은 의약품과 일반용 의약품 모두에서 높은 수요를 보고 있습니다. 재택 헬스케어의 대두도, 프리필드 시린지나 블리스터 팩 등, 보다 편리하고 사용하기 쉬운 포장 형태에 대한 요구에 박차를 가하고 있습니다. 이러한 개발은 의료 산업 전반에 걸쳐 보다 효율적이고 효과적인 포장 솔루션을 요구하는 광범위한 동향을 반영합니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료소스

- 공적소스

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 밸류체인에 영향을 주는 요인

- 변혁

- 미래의 전망

- 제조업체

- 유통업체

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 재활용 가능하고 지속 가능한 의료용 포장의 혁신

- 재택 헬스케어와 자기 투여의 동향의 확대

- 환자의 안전과 컴플라이언스 포장에 대한 의식의 향상

- 첨단 포장 솔루션을 필요로 하는 생물제제와 바이오시밀러의 성장

- 만성질환 증가에 따른 특수포장 솔루션 수요 증가

- 업계의 잠재적 리스크 및 과제

- 새로운 생물학적 제제의 포장 개발에서의 과제

- 헬스케어 포장 규제의 지역 격차

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 재료별, 2021-2034년

- 주요 동향

- 플라스틱

- 종이 및 판지

- 금속

- 유리

제6장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 경질 포장

- 병

- 상자 및 판지

- 트레이

- 프리필러블 흡입기

- 프리필러블 주사기

- 바이알 앰풀

- 병 및 캐니스터

- 기타

- 연질 포장

- 가방 및 파우치

- 튜브

- 필름 및 라미네이트

- 기타

제7장 시장 추계 및 예측 : 포장 유형별, 2021-2034년

- 주요 동향

- 1차 포장

- 2차 포장

- 3차 포장

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 의약품

- 경구제

- 주사제

- 외용약

- 점비약

- 기타

- 의료기기

- 일회용 소모품

- 치료기기

- 모니터링 진단 기기

- 기타

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 3M

- Adelphi Group

- Amcor

- Aptar CSP Technologies

- Berry Global

- CCL Industries

- Constantia Flexibles

- DS Smith

- DuPont

- Eastman Chemical

- Gerresheimer

- Graphic Packaging

- Huhtamaki

- Mayr-Melnhof Karton

- Nelipak

- Oliver Healthcare

- Printpack

- ProAmpac

- Schott Pharma

- Sealed Air

- SGD Pharma

- Solventum

- Sonoco Products

- West Pharmaceutical

- WestRock

The Global Healthcare Packaging Market was valued at USD 136.3 billion in 2024, with projections indicating a steady growth rate of 5.8% CAGR from 2025 to 2034. This market is primarily fueled by the growing need for innovative, secure, and sustainable packaging solutions. In recent years, the healthcare industry has been embracing advanced packaging technologies to meet the specific needs of biologics and specialty drugs. Alongside this, access to healthcare in developing regions is improving, driving an increase in demand for effective and efficient packaging.

Additionally, the rise of pharmaceutical e-commerce is providing new opportunities for packaging solutions that support safe transportation and storage. The integration of smart packaging is further enhancing patient compliance by ensuring accurate dosing and providing real-time information. This trend is also optimizing supply chain efficiency, reducing costs, and improving product traceability. As the healthcare sector continues to evolve, the packaging market will play a critical role in ensuring the safety and quality of pharmaceutical and medical products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $136.3 Billion |

| Forecast Value | $239.5 Billion |

| CAGR | 5.8% |

The healthcare packaging market is divided into two main segments: rigid and flexible packaging. Rigid packaging accounts for the largest market share, holding 61% in 2024. The dominance of this segment is largely due to its ability to protect products and maintain the integrity of sensitive healthcare products. Rigid packaging often employs high-performance materials like polypropylene and polycarbonate, essential for meeting stringent healthcare compliance regulations. With ongoing advancements in molding technologies, manufacturers are able to produce lightweight yet durable containers, helping reduce transportation costs while maintaining the necessary strength and protection. This continued evolution in materials and design is helping rigid packaging remain the preferred choice for many healthcare applications.

When examining end-user applications, the healthcare packaging market is categorized into pharmaceuticals and medical devices. The medical devices segment is expected to experience the highest growth rate, with a projected CAGR of 6.5%. This segment is expected to reach USD 76.4 billion by 2034, driven by innovations in medical device technology and the increasing demand for sterile, durable, and user-friendly packaging solutions. Medical device packaging must meet the demanding requirements of sterility, durability, and usability for a wide array of products, from diagnostic tools and surgical instruments to implants. As more advanced medical devices enter the market, the packaging solutions will need to evolve accordingly to ensure maximum safety and functionality.

In North America, the healthcare packaging market is expected to maintain its dominance, accounting for 34.5% of the market share in 2024. The U.S. is experiencing a significant increase in the demand for advanced packaging solutions within the healthcare sector, driven by technological advancements in medical products and a growing emphasis on patient safety. Innovations like tamper-evident and child-resistant packaging are seeing high demand for both pharmaceutical and over-the-counter products. The rise of home healthcare is also fueling the need for more convenient, user-friendly packaging formats, such as prefilled syringes and blister packs. These developments reflect a broader trend toward more efficient and effective packaging solutions across the healthcare industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Innovation in recyclable and sustainable medical packaging

- 3.5.1.2 Expanding home healthcare and self-administration trends

- 3.5.1.3 Rising awareness about patient safety and compliance packaging

- 3.5.1.4 Growth in biologics and biosimilars requiring advanced packaging solutions

- 3.5.1.5 Rising prevalence of chronic diseases boosting demand for specialized packaging solutions

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Challenges in developing packaging for emerging biologic therapies

- 3.5.2.2 Regional disparities in healthcare packaging regulations

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Paper & paperboard

- 5.4 Metal

- 5.5 Glass

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.2.1 Bottles

- 6.2.2 Boxes & cartons

- 6.2.3 Trays

- 6.2.4 Pre-fillable inhalers

- 6.2.5 Pre-fillable syringes

- 6.2.6 Vials & ampoules

- 6.2.7 Jars & canisters

- 6.2.8 Others

- 6.3 Flexible packaging

- 6.3.1 Bags & pouches

- 6.3.2 Tubes

- 6.3.3 Films & laminates

- 6.3.4 Others

Chapter 7 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Primary packaging

- 7.3 Secondary packaging

- 7.4 Tertiary packaging

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Pharmaceuticals

- 8.2.1 Oral drug

- 8.2.2 Injectables

- 8.2.3 Topical drug

- 8.2.4 Nasal drug

- 8.2.5 Others

- 8.3 Medical devices

- 8.3.1 Disposable consumables

- 8.3.2 Therapeutic equipment

- 8.3.3 Monitoring & diagnostic equipment

- 8.3.4 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3M

- 10.2 Adelphi Group

- 10.3 Amcor

- 10.4 Aptar CSP Technologies

- 10.5 Berry Global

- 10.6 CCL Industries

- 10.7 Constantia Flexibles

- 10.8 DS Smith

- 10.9 DuPont

- 10.10 Eastman Chemical

- 10.11 Gerresheimer

- 10.12 Graphic Packaging

- 10.13 Huhtamaki

- 10.14 Mayr-Melnhof Karton

- 10.15 Nelipak

- 10.16 Oliver Healthcare

- 10.17 Printpack

- 10.18 ProAmpac

- 10.19 Schott Pharma

- 10.20 Sealed Air

- 10.21 SGD Pharma

- 10.22 Solventum

- 10.23 Sonoco Products

- 10.24 West Pharmaceutical

- 10.25 WestRock