|

시장보고서

상품코드

1851571

헬스케어 포장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Healthcare Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

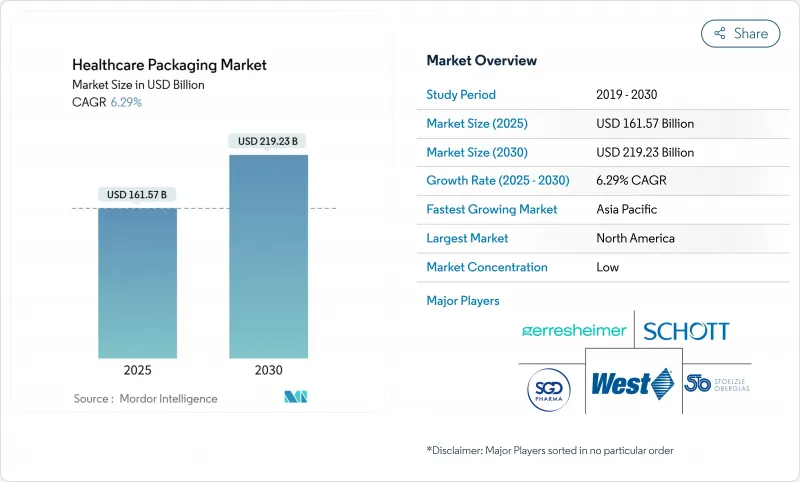

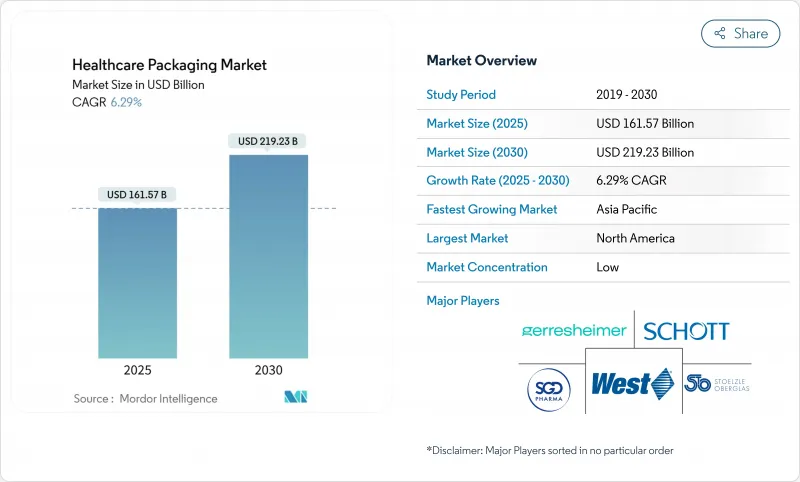

헬스케어 포장 시장 규모는 2025년 1,615억 7,000만 달러에 이르고, 2030년 CAGR 6.29%를 나타내 2,192억 3,000만 달러로 성장할 것으로 예측됩니다.

생물학적 제형에 대한 수요 가속화, 재택 치료 모델의 급속한 확대, 직렬화 규제 강화가 이러한 상승 궤도를 지원합니다. 인구동태의 기세는 유럽에서는 65세 이상의 인구가 젊은이를 웃도고, 사용하기 쉽고 고령자에게도 안전한 팩의 요구가 높아지고 있는 것으로부터도 분명합니다. 이와 병행하여, 의약품 브랜드의 소유자는 위조를 방지하기 위해 트레이서블에서 변조가 확인할 수 있는 디자인을 우선해, 1차 팩에 내장된 스마트 센서가 치료의 어드히어런스를 높이고 있습니다. 유럽 연합(EU)과 미국의 일부 주에서 지속가능성 규제는 장벽 보호를 손상시키지 않고 재활용 가능한 단일 소재 구조를 브랜드 소유자에게 밀어붙이고 있습니다. 불안정한 폴리머 원료 가격과 의료용 유리 생산 능력의 제약이 비용면에서 역풍이 되고 있지만, 지역 생산 거점에의 지속적인 투자가 공급 리스크를 완화하고 있습니다.

세계의 헬스케어 포장 시장 동향과 인사이트

셀프 케어·재택 진단 기기 수요 급증

당뇨병 치료 장비에 대한 연간 의료 기술 자본 지출은 2024년 70억 9,000만 달러에 달했고, 그중 27억 달러는 소매 대응 무균 포장이 필요한 지속 포도당 모니터에 충당됩니다. BD의 PIVO Pro와 MiniDraw 출시는 각 브랜드가 병원 수준의 무균성을 보장하면서 통신 판매에 적합한 크기의 개봉 방지 파우치를 어떻게 지정하고 있는지를 보여줍니다. 메드트로닉의 FDA가 승인한 InPen-Simplera Smart MDI 시스템은 포장이 의약품뿐만 아니라 통합된 전자 및 컴패니언 앱도 보호해야 한다는 점을 강조합니다. 따라서 헬스케어 포장 시장은 소아용이면서도 노인에게도 친화적인 클로저, 센서용 다층 캐비티, 원격 의료 워크플로우에 적합한 QR 대응 설명서 등에 축발을 두고 있습니다. 재택 간호의 보급이 진행됨에 따라 헬스케어 포장 시장은 강력한 성장 호를 묘사합니다.

직렬화 및 위조 방지 의무화

미국에서는 2024년 11월에 DSCSA가 완전히 시행되었고 데이터 교환 오류율은 최대 30%에 달하며, 코드가 일치하지 않으면 하루에 11만 팩을 격리할 위험이 있습니다. BD의 iDFill RFID 주사기는 1차 레벨에 식별자를 내장함으로써 기업이 2차 라벨을 생략하고 라인 속도를 가속화할 수 있음을 보여줍니다. 유럽의 FMD 규칙은 인간과 기계가 읽을 수 있는 이중 코드를 요구하고 있으며, 헬스케어 포장 시장을 디지털 인프라 투자로 더욱 밀어 올리고 있습니다. 직렬화가 복잡해짐에 따라 하드웨어, 소프트웨어 및 유효한 클라우드 서비스를 번들로 제공할 수 있는 공급업체가 점유율을 확대합니다.

석유계 수지의 가격 변동

LyondellBasell의 휴스턴 정유소 운영 중단과 Formosa의 새로운 폴리프로필렌 플랜트의 가동으로 프로파일렌 공급이 급박하고 Argus는 2025년 2자리 가격 상승을 예상하고 있습니다. 엔지니어링 수지 비용은 2025년 3월 다시 상승하여 컨버터 마진을 침식했습니다. FDA 인증 재료 코드에 묶여 있는 건강 관리 브랜드는 수지를 즉시 전환할 수 없기 때문에 소규모 컨버터는 유동성 부족에 직면하고 있습니다. 헬스케어 포장 시장에서는 대기업이 장기 헤지와 멀티소싱을 이용하여 변동성을 둔화시키는 한편, 배리어 불량의 위험을 초래하지 않고 다운가우징을 가능하게 하는 보다 배리어성이 높은 모노PP 라미네이트를 평가했습니다.

부문 분석

2024년 헬스케어 포장 시장 점유율은 계속 플라스틱이 70.12%를 차지하며, 비교할 수 없는 비용 효율성과 유연한 가공창을 반영했습니다. 반대로 유리는 제로 이온 용출 용기를 필요로 하는 생물 제제에 밀려 10.42%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 쇼트파마의 3억 7,100만 달러를 던진 노스캐롤라이나 공장은 401명의 고용을 창출해 GLP-1 주사제용의 붕규산염 주사기 생산 능력을 확대할 예정이며, 프리미엄 바이알에 대한 장기적인 신뢰를 증명하는 것입니다. 고가치 유리 바이알, 카트리지 및 주사기의 헬스케어 포장 시장 규모는 mRNA, 유전자 편집 및 세포 치료가 임상에서 철수함에 따라 확대될 것으로 보입니다.

흡입기, 유연한 정맥 주사 백, 점안기에서는 첨단 플라스틱이 우위를 유지하고 있지만, 특정한 불소 수지 코팅에 대한 PFAS 규제에 의해 수지 배합 업자는 새로운 배리어 화학물질의 개발을 강요하고 있습니다. TekniPlex의 재활용 가능한 투명 블리스터 라미네이트와 같은 하이브리드 솔루션은 PET와 EVOH를 결합하여 이전에는 호일에만 사용된 수증기 투과성 목표를 달성합니다. 판지는 EU의 재활용 의무화로 인해 2차 포장에서 전진하고 있지만, 1차 의약품 접촉층으로의 침투는 여전히 제한적입니다. 가압식 약물전달용 에어로졸에서는 금속이 계속 사용되고 있지만, 유럽 시장에서는 추진제의 단계적 폐지가 진행되어, 현재 초기 시험이 행해지고 있는 조류 베이스의 바이오 머티리얼에 백화의 화살이 서 있습니다. 원재료의 다양화로 인해 시장 상황은 치료 클래스가 용기 선택을 좌우하는 미묘한 상황이 되었습니다.

병 및 용기는 2024년 헬스케어 포장 시장에서 40.21%의 점유율을 유지했지만 블리스터 팩은 CAGR 8.67%를 나타낼 전망입니다. Amcor사의 재활용 대응 AmSky 시스템은 PVC에서 HDPE로 대체하여 온실가스 배출량을 70% 줄이면서도 습기에 민감한 강압제에 요구되는 배리어 사양을 유지하고 있습니다. NFC 태그가 장착된 컴플라이언스 블리스터 카드는 섭취 이벤트를 기록하고 임상의에게 복용 어드히어런스 대시보드를 제공합니다. 바이알과 앰풀은 여전히 동결건조제에 의무화되어 있지만, Stevanato의 EZ-fill 플랫폼을 통해 Nipro는 교환 시간을 80% 단축하는 D2F의 Ready-to-fill 유리 바이알을 상품화했습니다.

웨어러블 인젝터와 결합된 카트리지는 8mm 얇은 캐뉼라로 축 발을 옮겨 고점도의 생물학적 제제를 취급합니다. 파우치는 얇은 레터 박스 출하 형식을 가능하게 해, 소비자 직접 판매의 진단 킷에는 빠뜨릴 수 없는 것이 되고 있습니다. 기타 '카테고리'는 RFID 센서가 장착된 건조제 파우치가 스마트 팩에 내장되어 습도 이상이 발생하면 약사에게 경고를 하게 되어 팽창하고 있습니다. 결국, 헬스케어 포장 시장은 분자 감수성, 사용법 용량 및 전자상거래의 새로운 규범에 따라 각 형식의 역할이 결정되는 폼 팩터 계층을 포함합니다.

지역 분석

북미는 2024년에 헬스케어 포장 시장 점유율의 36.35%를 차지하고 이익률이 높은 코딩 장비를 강제하는 FDA의 직렬화 규칙이 이를 지원했습니다. 공급망의 혼란은 계속되고 있으며, 공급자의 80%는 공급 부족의 심각화를 예상하고 있으며, 중규모 시스템에서는 연간 350만 달러의 비용 증가를 전망하고 있습니다. BD의 25억 달러의 국내 생산 능력 증대는 무역 혼란으로부터 헬스케어 포장 시장을 보호하는 리쇼어링의 논리를 강조합니다. 그러나 의료기기에 대한 관세는 현재 25%에 달하고 있으며, 컨버터는 멕시코와 캐나다에서 금형을 이중 조달하는 동기부여가 되고 있습니다.

아시아태평양은 인도, 중국, ASEAN의 제네릭 의약품 확대와 공적 의료 자금을 배경으로 CAGR 9.32%를 기록하여 가장 급성장하고 있는 지역입니다. Amcor의 Phoenix Flexibles 인수는 인도의 클린룸 라미네이션 생산 능력을 두 배로 늘리고 현지 공급에 대한 헌신을 보여주었습니다. 일본의 건강 2025 박람회에서는 크라이오바리데이션된 바이알이 필요한 재생 헬스케어 포장에 스포트라이트가 적용되었습니다. TOPPAN과 DNP는 섬유 기반 멸균 팩을 전시했고, 이 지역이 원형 소재로 기울어져 있음을 보여주었습니다.

유럽은 규제의 변화에도 불구하고 강력한 처리 능력을 유지하고 있습니다. 향후 예정된 재활용 의무화는 기존의 다층 포일에 과제를 맞추고 있지만, 바이오의 배리어층의 연구 개발 자금을 뒷받침하고 있습니다. 독일은 유리 주사기 생산에서 불균형한 점유율을 차지하고 있지만, 생산 능력의 제약이 스페인과 체코 공화국에 대한 투자에 박차를 가하고 있습니다. 중동 및 아프리카에서는 사우디아라비아와 이집트에서 기초적 제네릭 의약품 공장의 확장이 이어져 GMP 등급 필름의 그린필드 수요가 확대됩니다. 남미는 한자릿수 중반의 성장으로, 브라질의 ANVISA는 카톤 사이즈를 작게 하는 e리플릿을 도입해 물류 비용을 삭감했습니다. 이러한 움직임을 종합하면 헬스케어 포장 시장 역학이 각 대륙에서 확대되고 다국적 컨버터의 위험 포트폴리오를 다양화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 셀프 케어 및 재택 진단 기기 수요 급증

- 직렬화와 위조 방지의 의무화

- 고령화와 만성질환의 만연

- 지속가능성 주도 소재 대체

- 세포 및 유전자 치료용 저온 포장

- 어드히어런스 추적용 RFID/NFC 부착 스마트 팩

- 시장 성장 억제요인

- 석유계 수지 가격의 변동

- 복수의 관할 구역에 걸친 복잡한 폐기물 처리 규칙

- 의료용 유리의 생산 능력 병목

- 커넥티드 포장에서 사이버 보안 위험

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 업계 간 경쟁

제5장 시장 규모와 성장 예측

- 재료별

- 유리

- 플라스틱

- 종이 및 판지

- 금속 및 호일

- 제품 유형별

- 병 및 용기

- 바이알 및 앰풀

- 카트리지 및 사전 충전 주사기

- 블리스터 팩

- 파우치 및 백

- 기타 제품 유형

- 포장 단계별

- 1차 포장

- 2차 포장

- 3차 포장

- 최종 사용자별

- 제약 제조

- 의료기기 OEM

- 영양보조식품 및 OTC

- 재택 건강 관리 제공업체

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주, 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Gerresheimer AG

- SCHOTT AG

- Corning Incorporated

- West Pharmaceutical Services

- AptarGroup Inc.

- Becton Dickinson & Co.

- SGD Pharma

- Nipro Corporation

- Piramal Glass

- Oliver Healthcare Packaging

- Smurfit WestRock

- Sealed Air Corp.

- Sonoco Products Co.

- Catalent Inc.

- Beatson Clark PLC

- Shandong Medicinal Glass

- Sisecam Group

- Arab Pharmaceutical Glass Co.

- Stolzle-Oberglas GmbH

제7장 시장 기회와 향후 전망

KTH 25.11.24The healthcare packaging market size reached USD 161.57 billion in 2025 and is projected to grow to USD 219.23 billion by 2030, registering a 6.29% CAGR.

Accelerated demand for biologics, rapid expansion of home-care treatment models, and tightening serialization rules anchor this upward trajectory. Demographic momentum is evident as the over-65 cohort now outnumbers youth in Europe, intensifying needs for user-friendly, senior-safe packs. In parallel, pharmaceutical brand owners prioritize traceable, tamper-evident designs to curb counterfeits, while smart sensors embedded in primary packs enhance therapy adherence. Sustainability regulations in the European Union and select U.S. states are pushing brand owners toward recyclable mono-material structures without compromising barrier protection. Volatile polymer feedstock pricing and constrained medical-grade glass capacity remain cost headwinds, but ongoing investment in regional production hubs is cushioning supply risk.

Global Healthcare Packaging Market Trends and Insights

Demand Surge in Self-Care and Home-Diagnostic Devices

Annual med-tech capital spending on diabetes care devices hit USD 7.09 billion in 2024, with USD 2.7 billion earmarked for continuous glucose monitors that require retail-ready sterile packaging. BD's PIVO Pro and MiniDraw launches show how brands now spec tamper-proof pouches sized for mail-order fulfillment while ensuring hospital-grade sterility. Medtronic's FDA-cleared InPen-Simplera Smart MDI system underscores that packaging must protect not only the drug but also the embedded electronics and companion apps. The healthcare packaging market, therefore, pivots toward child-resistant yet senior-friendly closures, multi-layer cavities for sensors, and QR-enabled instructions that match telehealth workflows. Intensified home-care adoption keeps the healthcare packaging market on a robust growth arc.

Serialization and Anti-Counterfeit Mandates

Full enforcement of the U.S. DSCSA in November 2024 triggered up to 30% error rates in data exchanges, risking daily quarantines of 110,000 packs when codes mis-match.Cardinal Health's turnkey serialization service pipeline grew as drug makers outsourced coding, aggregation, and validation steps. BD's iDFill RFID syringe shows that embedding identifiers at the primary level lets companies dispense with secondary labels and accelerate line speeds. European FMD rules requiring dual human- and machine-readable codes further push the healthcare packaging market toward digital infrastructure investment. Suppliers able to bundle hardware, software, and validated cloud services gain share as serialization complexity mounts.

Petro-based Resin Price Volatility

The shutdown of LyondellBasell's Houston refinery and the commissioning of Formosa's new polypropylene plant tightened propylene supply, with Argus expecting double-digit price hikes in 2025. Engineering-resin costs climbed again in March 2025, eroding converter margins. Healthcare brands tied to FDA-validated material codes cannot switch resins quickly, so smaller converters face liquidity crunches. The healthcare packaging market sees larger players using long-term hedging and multi-sourcing to blunt volatility, while they evaluate higher-barrier mono-PP laminates that permit down-gauging without risking barrier failure.

Other drivers and restraints analyzed in the detailed report include:

- Aging Population and Chronic-Disease Prevalence

- Sustainability-Driven Material Substitution

- Complex Multi-Jurisdictional Waste-Disposal Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics continued to account for 70.12% of healthcare packaging market share in 2024, reflecting unmatched cost efficiency and flexible processing windows. Conversely, glass is advancing at a 10.42% CAGR, buoyed by biologics that require zero-ion-leach containers. SCHOTT Pharma's USD 371 million North Carolina plant will add 401 jobs and expand borosilicate syringe capacity for GLP-1 injectables, evidencing long-term confidence in premium vials. The healthcare packaging market size for high-value glass formats-vials, cartridges, syringes-will expand as mRNA, gene-editing, and cell therapies exit the clinic.

Advanced plastics retain dominance in inhalers, flexible IV bags, and ophthalmic droppers, but PFAS restrictions on certain fluoropolymer coatings force resin formulators to develop new barrier chemistries. Hybrid solutions, such as TekniPlex's clear recyclable blister laminate, combine PET with EVOH to reach moisture-vapour-transmission targets traditionally reserved for foil. Paperboard is making headway in secondary wraps thanks to EU recyclability mandates, yet its penetration into primary drug contact layers remains limited. Metals continue to serve pressurized drug delivery aerosols, but propellant phase-out in European markets is opening white-space for algae-based biomaterials now in early testing. Collectively, raw-material diversification positions the healthcare packaging market for a nuanced landscape where therapeutic class determines container of choice.

Bottles and containers retained a 40.21% slice of the healthcare packaging market in 2024, but blister packs are sprinting ahead with an 8.67% CAGR. Amcor's recycle-ready AmSky system substitutes PVC with HDPE, reducing greenhouse-gas emissions by 70% yet keeping the barrier specs demanded for moisture-sensitive antihypertensive tablets. Compliance blister cards featuring NFC tags now capture ingestion events, feeding adherence dashboards for clinicians. Vials and ampoules remain compulsory for lyophilized APIs, although Stevanato's EZ-fill platform allowed Nipro to commercialize D2F ready-to-fill glass vials that cut change-over time by 80%.

Cartridges paired with wearable injectors are pivoting toward 8-mm thin-wall cannulas to handle high-viscosity biologics. Pouches have become the go-to for direct-to-consumer diagnostics kits, enabling low-profile letter-box shipping formats. The "other" category is swelling as smart packs embed desiccant pouches with RFID sensors that alert pharmacists when humidity excursions occur. Ultimately, the healthcare packaging market embraces a form-factor hierarchy where each format's role is dictated by molecule sensitivity, dosage regimen, and emerging e-commerce fulfilment norms.

The Healthcare Packaging Market Report is Segmented by Material (Glass, Plastics, and More), Product Type (Bottles and Containers, Vials and Ampoules, Cartridges and Pre-Filled Syringes, and More), Packaging Level (Primary, Secondary, Tertiary), End-User (Pharmaceutical Manufacturing, Medical-Device OEMs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 36.35% of healthcare packaging market share in 2024, supported by FDA serialization rules that compel high-margin coding equipment. Supply-chain turbulence persists; 80% of providers expect shortages to intensify, adding up to USD 3.5 million in annual costs for medium-sized systems. BD's USD 2.5 billion domestic capacity build underscores a reshoring logic that protects the healthcare packaging market from trade disruptions. However, tariffs on medical devices now reaching 25% incentivize converters to dual-source tooling from Mexico and Canada.

Asia-Pacific is the fastest-growing region, charting a 9.32% CAGR on the back of generics expansion and public-health funding in India, China, and ASEAN. Amcor's acquisition of Phoenix Flexibles doubled its cleanroom lamination capacity in India, demonstrating commitment to localize supply. Japan's Health 2025 expo spotlighted regenerative-medicine packaging that demands cryo-validated vials. TOPPAN and DNP showcased fiber-based sterile packs, signaling a regional tilt toward circular materials.

Europe maintains strong throughput despite regulatory churn. The upcoming recyclability mandate challenges legacy multilayer foils, yet drives R&D funding for bio-based barrier layers. Germany captures disproportionate share of glass syringe output, but capacity constraints spur investments in Spain and the Czech Republic. Middle East & Africa continue to expand basic generic drug plants in Saudi Arabia and Egypt, opening greenfield demand for GMP-grade films. South America posts mid-single-digit growth; Brazil's ANVISA introduced e-leaflets that lower carton size, trimming logistics costs. Collectively these dynamics widen the healthcare packaging market size across every continent while diversifying the risk portfolio for multinational converters.

- Amcor plc

- Gerresheimer AG

- SCHOTT AG

- Corning Incorporated

- West Pharmaceutical Services

- AptarGroup Inc.

- Becton Dickinson & Co.

- SGD Pharma

- Nipro Corporation

- Piramal Glass

- Oliver Healthcare Packaging

- Smurfit WestRock

- Sealed Air Corp.

- Sonoco Products Co.

- Catalent Inc.

- Beatson Clark PLC

- Shandong Medicinal Glass

- Sisecam Group

- Arab Pharmaceutical Glass Co.

- Stolzle-Oberglas GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand surge in self-care and home-diagnostic devices

- 4.2.2 Serialization and anti-counterfeit mandates

- 4.2.3 Aging population and chronic-disease prevalence

- 4.2.4 Sustainability-driven material substitution

- 4.2.5 Cryogenic packaging for cell and gene therapies

- 4.2.6 Smart packs with RFID / NFC for adherence tracking

- 4.3 Market Restraints

- 4.3.1 Petro-based resin price volatility

- 4.3.2 Complex multi-jurisdictional waste-disposal rules

- 4.3.3 Medical-grade glass capacity bottlenecks

- 4.3.4 Cyber-security risks in connected packaging

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Glass

- 5.1.2 Plastics

- 5.1.3 Paper and Paperboard

- 5.1.4 Metals and Foils

- 5.2 By Product Type

- 5.2.1 Bottles and Containers

- 5.2.2 Vials and Ampoules

- 5.2.3 Cartridges and Pre-filled Syringes

- 5.2.4 Blister Packs

- 5.2.5 Pouches and Bags

- 5.2.6 Other ProductType

- 5.3 By Packaging Level

- 5.3.1 Primary Packaging

- 5.3.2 Secondary Packaging

- 5.3.3 Tertiary Packaging

- 5.4 By End-user

- 5.4.1 Pharmaceutical Manufacturing

- 5.4.2 Medical-Device OEMs

- 5.4.3 Nutraceuticals and OTC

- 5.4.4 Home-Healthcare Providers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Gerresheimer AG

- 6.4.3 SCHOTT AG

- 6.4.4 Corning Incorporated

- 6.4.5 West Pharmaceutical Services

- 6.4.6 AptarGroup Inc.

- 6.4.7 Becton Dickinson & Co.

- 6.4.8 SGD Pharma

- 6.4.9 Nipro Corporation

- 6.4.10 Piramal Glass

- 6.4.11 Oliver Healthcare Packaging

- 6.4.12 Smurfit WestRock

- 6.4.13 Sealed Air Corp.

- 6.4.14 Sonoco Products Co.

- 6.4.15 Catalent Inc.

- 6.4.16 Beatson Clark PLC

- 6.4.17 Shandong Medicinal Glass

- 6.4.18 Sisecam Group

- 6.4.19 Arab Pharmaceutical Glass Co.

- 6.4.20 Stolzle-Oberglas GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment