|

시장보고서

상품코드

1721497

정유압 변속기 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Hydrostatic Transmission Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

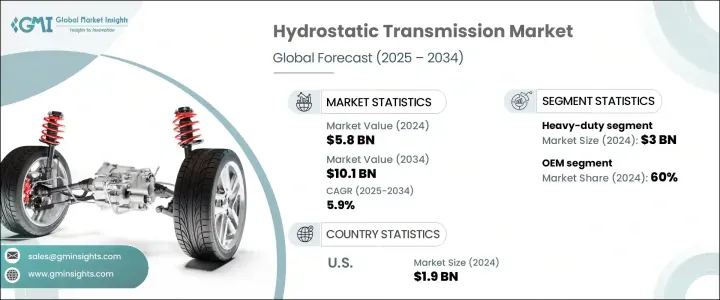

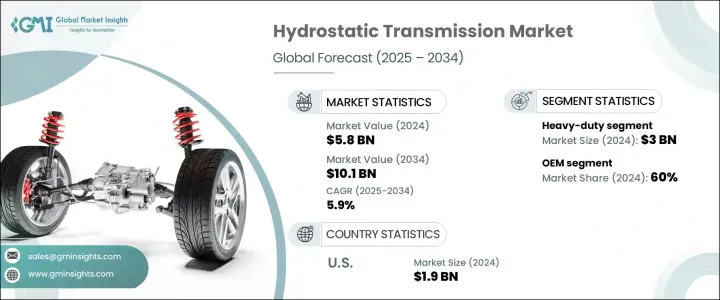

세계의 정유압 변속기 시장 규모는 2024년 58억 달러로 평가되었고, CAGR 5.9%를 나타내 2034년에는 101억 달러에 이를 것으로 예측되고 있습니다. 광업 등의 분야에서 수요가 높아지고 있어 부드럽고 응답성이 높고, 연료 효율이 높은 전력 공급에 대한 요구가 설계의 우선순위를 바꾸고 있습니다.

제조업체는 차세대 장비의 요구를 충족시키기 위해 완벽한 기계 작동과 지능형 제어를 지원하는 고급 기능의 통합에 주력하고 있습니다. 가능성을 의식하는 오늘날의 상황에서 매우 중요한 요소가 되고 있습니다. 또한, 인프라 투자의 확대, 노동력 부족, 스마트 농업과 자동 자재관리의 추진이, 특히 북미, 유럽, 아시아태평양, 중동 및 아프리카의 정유압 변속기 시장에 큰 기세를 주고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 58억 달러 |

| 예측 금액 | 101억 달러 |

| CAGR | 5.9% |

주요 산업 전체의 성장은 에너지 효율적인 변속기 시스템에 대한 선호도가 높아지고 원활한 전력 변조에 대한 수요가 큰 원동력이 되고 있습니다. 이러한 기술 혁신은 차량 아키텍처를 재정의하여 더욱 부드러운 운영과 시스템의 신뢰성 향상을 가능하게 하고 있습니다.

시장 세분화에서는 용량별로 라이트 듀티, 미디엄 듀티, 헤비 듀티의 각 시스템을 분류하고 있습니다. 2024년에 30억 달러의 압도적인 점유율을 차지했습니다. 연료 효율을 유지하면서 가혹한 조건 하에서도 안정된 성능을 발휘하기 때문에 특히 매력적입니다. 업계의 리더들은 정밀 제어 모듈, 전자 관리 유닛, 에너지 절약 기능 강화 등을 갖춘 차세대 시스템을 개발하고 높아지는 산업계의 요구에 부응하고 있습니다.

유통에 의하면, 시장은 OEM 채널과 애프터마켓 채널로 나뉘어져 있습니다. OEM은 ADAS 및 기타 지능형 운전 시스템과의 호환성에 최적화된 유닛을 제공함으로써 대응하고 있습니다.

미국의 정유압 변속기 시장은 2024년에 19억 달러를 창출했고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 6.2%를 나타낼 전망입니다. 성장의 주된 원동력은 유압 시스템 설계의 혁신, 인프라 투자, 농업과 건설에 있어서의 정밀도에 초점을 맞춘 기기의 급증입니다.

Parker Hannifin, Dana, Bosch Rexroth, John Deere, CNH Industrial, Eaton, Danfoss, Mahindra & Mahindra, Husqvarna, Kubota 등의 기업들은 R&D 투자, 전략적 파트너십, 혁신적인 제품 출시를 통해 우수성을 높이고 있습니다. IoT 대응 시스템과 진단 기술에 투자하고 있습니다. OEM과의 협업은 첨단 차량 플랫폼에의 통합을 간소화하는 한편, 합병이나 지역 확대에 의해 세계 기업은 신흥 시장의 급증하는 수요에 의해 잘 대응할 수 있게 되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체의 상황

- 원재료 공급업체

- 부품 공급업체

- 제조업체

- 기술 공급업체

- 유통 채널 분석

- 최종 용도

- 이익률 분석

- 공급업체의 상황

- 기술 및 혁신 전망

- 특허 분석

- 규제 상황

- 코스트 내역 분석

- 주요 뉴스와 대처

- 영향요인

- 성장 촉진요인

- 오프로드 차량이나 특수 차량에서의 사용 증가

- 스마트 유압 시스템의 진보

- 연비 향상을 위한 규제 강화

- 하이브리드 유압 전동 파워트레인 개발

- 업계의 잠재적 위험 및 과제

- 초기 높은 비용

- 복잡한 유지보수 요건

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계·예측 : 용량별(2021-2034년)

- 주요 동향

- 헤비 듀티

- 중형

- 경량

제6장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 유압 펌프

- 유압 모터

- 밸브 및 컨트롤

- 필터

- 기타

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 농업

- 공사

- 자재 취급

- 기타

제8장 시장 추계·예측 : 변속기별(2021-2034년)

- 주요 동향

- 폐쇄형 루프

- 개방형 루프

제9장 시장 추계·예측 : 판매 채널별(2021-2034년)

- 주요 동향

- 애프터마켓

- OEM

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 이탈리아

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- AGCO

- Ariens

- Bosch Rexroth

- CNH Industrial

- Daedong Industrial

- Dana

- Danfoss

- Eaton

- Husqvarna

- Iseki

- JCB

- John Deere

- Kubota

- Mahindra & Mahindra

- MTD

- Parker Hannifin

- Sauer-Danfoss

- Tuff Torq

- Yanmar

- ZF Friedrichshafen

The Global Hydrostatic Transmission Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 10.1 billion by 2034. As industries worldwide continue to evolve toward smarter, cleaner, and more energy-efficient technologies, hydrostatic transmission systems are gaining strong traction. The market is experiencing heightened demand from sectors such as automotive, agriculture, construction, and mining, where the need for smooth, responsive, and fuel-efficient power delivery is reshaping design priorities. The increasing adoption of automation and electrification across industrial and vehicular platforms is significantly influencing transmission technologies.

Manufacturers are focusing on integrating advanced features that support seamless machine operation and intelligent control to match the needs of next-generation equipment. End users are leaning toward systems that ensure precision handling, reduced emissions, and higher reliability-factors that are crucial in today's performance-driven and sustainability-conscious landscape. Moreover, growing infrastructure investments, labor shortages, and the push for smart farming and automated material handling are adding substantial momentum to the hydrostatic transmission market, especially across North America, Europe, Asia Pacific, and the Middle East & Africa.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 5.9% |

Growth across key industries is largely driven by the rising preference for energy-efficient transmission systems and the demand for seamless power modulation. Enhanced vehicle performance, precise control, and improved fuel economy are among the core benefits propelling adoption. As hydraulic technology continues to mature, manufacturers are incorporating intelligent features such as electronic controls and smart sensors into their systems. These innovations are redefining vehicle architecture, allowing smoother operation and greater system reliability. The movement toward automated, sustainable machinery is fueling robust demand in sectors such as heavy construction, agricultural equipment, and industrial vehicles.

Segmented by capacity, the market includes light-duty, medium-duty, and heavy-duty systems. Among these, heavy-duty hydrostatic transmissions held a commanding USD 3 billion in 2024. This dominance stems from their ability to deliver high torque, long operational life, and reliability in high-load, rugged applications. Heavy-duty systems are especially attractive for their consistent performance under extreme conditions while maintaining fuel efficiency. Industry leaders are developing next-gen systems equipped with precision control modules, electronic management units, and energy-saving enhancements to meet escalating industrial requirements. These upgrades are strengthening the foothold of heavy-duty solutions across mission-critical operations.

Based on distribution, the market is split between OEM and aftermarket channels. The OEM segment secured a 60% share in 2024, bolstered by rising integration of hydrostatic systems into new vehicle designs. Consumers are increasingly favoring factory-installed units that work in sync with built-in safety and automation features. OEMs are responding by delivering units optimized for compatibility with ADAS and other intelligent driving systems. The demand is especially high among premium models where smooth drive control and fuel savings are non-negotiable. Regulatory mandates pushing for enhanced safety and sustainability continue to drive OEM adoption.

United States Hydrostatic Transmission Market generated USD 1.9 billion in 2024 and is poised to grow at 6.2% CAGR between 2025-2034. Growth is primarily driven by innovation in hydraulic system designs, infrastructure investments, and the surge in precision-focused equipment in agriculture and construction. The adoption of hybrid transmissions and sensor-based control features is accelerating. With a national focus on automation and sustainable industrial practices, the US market is witnessing fast-paced deployment across varied applications.

Companies such as Parker Hannifin, Dana, Bosch Rexroth, John Deere, CNH Industrial, Eaton, Danfoss, Mahindra & Mahindra, Husqvarna, and Kubota are sharpening their edge with R&D investments, strategic partnerships, and innovative product launches. Many players are investing in IoT-enabled systems and diagnostic technologies to optimize lifecycle performance and operational efficiency. Collaborations with OEMs are simplifying integration into advanced vehicle platforms, while mergers and regional expansions are enabling global players to better serve the surging demand from emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increased use in off-highway and specialty vehicles

- 3.7.1.2 Advancements in smart hydraulic systems

- 3.7.1.3 Regulatory push for fuel efficiency

- 3.7.1.4 Development of hybrid hydrostatic-electric powertrains

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs

- 3.7.2.2 Complex maintenance requirements

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Heavy-duty

- 5.3 Medium-duty

- 5.4 Light-duty

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Hydraulic pumps

- 6.3 Hydraulic motors

- 6.4 Valves & controls

- 6.5 Filters

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Agriculture

- 7.3 Construction

- 7.4 Material handling

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Transmission, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Closed-loop

- 8.3 Open-loop

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Aftermarket

- 9.3 OEM

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AGCO

- 11.2 Ariens

- 11.3 Bosch Rexroth

- 11.4 CNH Industrial

- 11.5 Daedong Industrial

- 11.6 Dana

- 11.7 Danfoss

- 11.8 Eaton

- 11.9 Husqvarna

- 11.10 Iseki

- 11.11 JCB

- 11.12 John Deere

- 11.13 Kubota

- 11.14 Mahindra & Mahindra

- 11.15 MTD

- 11.16 Parker Hannifin

- 11.17 Sauer-Danfoss

- 11.18 Tuff Torq

- 11.19 Yanmar

- 11.20 ZF Friedrichshafen