|

시장보고서

상품코드

1750474

전기자동차 음향 발생기 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Electric Vehicle Sound Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

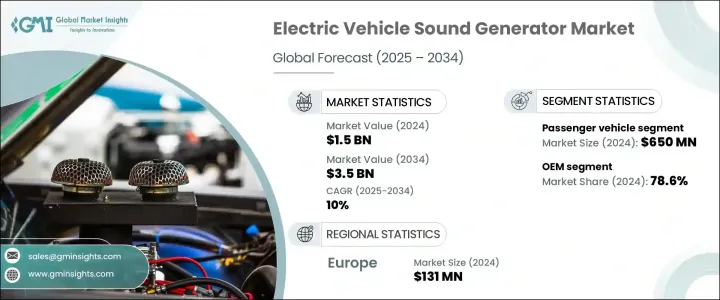

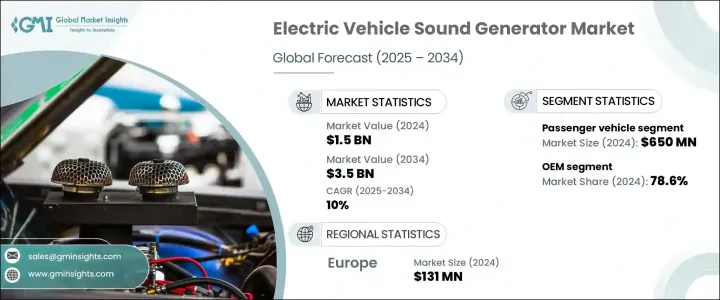

세계의 전기자동차 음향 발생기 시장은 2024년에 15억 달러로 평가되었고, 2034년에는 35억 달러에 이를 것으로 추정되며, CAGR 10%로 성장할 전망입니다.

전기자동차는 저속 주행 시 거의 소리를 내지 않아 도시 지역과 보행자 밀집 지역에서 안전 위험을 초래합니다. 전 세계 규제 기관들은 시각 장애인을 포함한 보행자를 경고하기 위해 전기자동차이 합성 소리를 발생하도록 요구하고 있습니다. 이 규제 압력은 자동차 제조사들이 EVSG를 표준 기능으로 채택하도록 촉진하고 있습니다. 전기자동차 생산 증가와 안전 우려의 결합은 특히 인구 밀도가 높은 도시에서 이 수요를 촉진하고 있습니다.

전기 이동 수단이 개인용 승용차에서 상업용 차량 및 대중 교통에 이르기까지 여러 부문으로 계속 확대됨에 따라 전기자동차 음향 발생기(EVSG)는 옵션 기능에서 필수 안전 부품으로 진화하고 있습니다. 도시의 교통 체증이 심해지고 보행자 구역이 증가함에 따라 저속으로 주행하는 전기자동차의 거의 소음이 없는 운행은 공공 안전에 실질적인 위험을 초래합니다. 소리 발생기는 보행자, 자전거 이용자 및 다른 도로 사용자에게 접근하는 차량을 알리는 청각적 신호를 생성하여 이 간극을 메우는 역할을 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 15억 달러 |

| 예측 금액 | 35억 달러 |

| CAGR | 10% |

전기자동차 음향 발생기 시장에서 승용차 부문은 40%의 점유율을 차지하며 2024년에는 6억 5천만 달러의 가치를 달성할 것으로 예상됩니다. 이는 승용차가 보행자와의 상호 작용이 빈번한 도시 지역에서 가장 많이 사용되기 때문입니다. 운전자가 장거리 여행을 하는 경우가 늘면서, 규제 준수를 보장하고 안전을 강화해야 할 필요성이 대두되어 자동차 제조업체들은 이러한 차량에 음향 발생기를 통합하고 있습니다. 제조업체들은 또한 법적 요건을 충족할 뿐 아니라 독특한 브랜드 아이덴티티를 구축하기 위해 맞춤형 EV 음향에 눈을 돌리고 있습니다. 안전과 브랜드 마케팅의 융합으로 승용 전기자동차에 첨단 EVSG 시스템의 채택이 가속화되고 있습니다.

OEM은 2024년 시장 점유율의 78.6%를 차지했습니다. 차량 생산 과정에서 EV 음향 시스템을 설치하면 파워트레인과 인포테인먼트 시스템 등 차량 내 전자 장치와 원활하게 통합될 수 있습니다. 이 접근 방식은 초기 단계에서 법규 준수를 보장해 보증 유지와 인증 절차 간소화에 기여합니다. OEM은 대규모 구매 및 조립을 통해 비용을 절감하고, 제조 효율성을 유지하면서 소비자에게 내장형 규제 준수 음향 솔루션을 제공할 수 있는 이점을 누릴 수 있습니다. 규제 기관은 차량이 도로에 출시되기 전에 규정 준수를 보장할 수 있기 때문에 OEM 설치를 선호합니다.

독일 전기자동차 음향 발생기 시장은 2024년에 1억 3,100만 달러를 기록했습니다. 이 나라의 우위는 강력한 자동차 제조 기반과 전기화 추진에 대한 적극적인 노력에 기인합니다. 독일 제조업체들은 EVSG 시스템을 가장 먼저 채택한 업체들 중 하나로, 규제 요건과 혁신을 활용하여 경쟁이 치열한 미래 시장에서 선두를 유지하고 있습니다. 이들의 접근 방식은 EU 소음 규제를 엄격하게 준수하는 동시에 음향 브랜딩에 중점을 두어 자동차 제조업체들이 브랜드 아이덴티티에 부합하는 시그니처 음향 프로파일을 만들 수 있도록 합니다. 대규모 생산 시설과 첨단 R&D 역량을 바탕으로 높은 출력을 자랑하는 전기자동차는 원활하게 통합된 EVSG 솔루션에 대한 수요를 더욱 부추기고 있습니다.

EVSG 시장의 주요 기업으로는 현대, ECCO, STMicroelectronics, Continental, Harman International, Aptiv, Denso, Forvia Hella, Brigade Electronics, Ansys 등이 있습니다. 경쟁력을 유지하기 위해 이들 기업은 디지털 음향 아키텍처 발전, OEM과의 파트너십 확대, AI 기반 음향 생성 기술 투자 등 핵심 전략을 채택하고 있습니다. 많은 기업은 다양한 전기자동차 유형에 적용 가능한 확장성 있는 솔루션을 개발하는 동시에 차량 내 통합과 사용자 경험을 개선하는 데 집중하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 부품 제조업체

- 소프트웨어 개발자와 음향 엔지니어

- 시스템 통합자

- 최종 용도

- 이익률 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 기술과 혁신의 상황

- 특허 분석

- 가격 동향

- 지역

- 제품

- 코스트 내역 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 보행자의 안전에 관한 규제 의무

- 전기자동차(EV)의 확산

- 음향 설계 및 기술의 발전

- OEM 통합 및 브랜드 차별화

- 업계의 잠재적 위험 및 과제

- 첨단 시스템의 높은 비용

- 기기술 및 표준화 장벽

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품별(2024-2034년)

- 주요 동향

- 외부 음향 발생기

- 내부 음향 발생기

- 맞춤형 음향 시스템

제6장 시장 추계 및 예측 : 추진력별(2024-2034년)

- 주요 동향

- 배터리 전기자동차(BEV)

- 하이브리드 전기자동차(HEV)

- 플러그인 하이브리드 전기자동차(PHEV)

- 연료전지 전기자동차(FCEV)

제7장 시장 추계 및 예측 : 차량별(2024-2034년)

- 주요 동향

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- 소형 상용차

- MCV

- HCV

- 이륜차와 삼륜차

- 오프로드 차량

제8장 시장 추계 및 예측 : 판매 채널별(2024-2034년)

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 컴포넌트별(2024-2034년)

- 주요 동향

- 하드웨어

- 스피커

- 증폭기

- 컨트롤러

- 액추에이터

- 배선 하네스

- 소프트웨어

- 음향 디자인 용도

- 제어 시스템

- 사용자 인터페이스 시스템

제10장 시장 추계 및 예측 : 속도역별(2024-2034년)

- 주요 동향

- 저속 음향 발생기(0-30 km/h)

- 전속도 음향 발생 장치(시속 30km 이상)

제11장 시장 추계 및 예측 : 지역별(2024-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제12장 기업 프로파일

- Ansys

- Aptiv

- Brigade Electronics

- Continental

- Denso

- ECCO

- ESI Group(Keysights)

- Forvia Hella

- General Motors

- Harman International

- 현대

- Mercedes-Benz

- Softeq

- Soundracer

- STMicroelectronics

- Thor

- TVS

- Volkswagen

- Volvo

The Global Electric Vehicle Sound Generator Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 3.5 billion by 2034, as electric vehicles (EVs) become more widespread, the demand for sound generators continues to rise. EVs are almost silent at low speeds, which poses safety risks in urban and pedestrian-heavy areas. Regulatory bodies worldwide have responded by requiring EVs to produce synthetic sounds to alert pedestrians, especially those who are visually impaired. This growing regulatory pressure pushes automakers to adopt EVSGs as a standard feature. The convergence of rising EV production and increasing safety concerns fuels this demand, particularly in densely populated cities.

As electric mobility continues to expand across multiple segments-from individual passenger cars to commercial fleets and public transit-electric vehicle sound generators (EVSGs) are evolving from optional features to mandatory safety components. With cities growing more congested and pedestrian zones increasing, the near-silent operation of EVs at low speeds poses a real risk to public safety. Sound generators help bridge this gap by producing audible cues that alert pedestrians, cyclists, and other road users to an approaching vehicle.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.5 Billion |

| CAGR | 10% |

The passenger vehicles segment in the electric vehicle sound generator market held a 40% share, reaching a valuation of USD 650 million in 2024, as these vehicles are most often used in urban areas where pedestrian interaction is frequent. As drivers travel longer distances, the need to ensure regulatory compliance and enhance safety prompts automakers to integrate sound generators in these vehicles. Manufacturers are also turning to custom-designed EV sounds not only to meet legal mandates but also to build distinctive brand identities. The fusion of safety and brand marketing is accelerating the adoption of advanced EVSG systems in passenger electric vehicles.

Original equipment manufacturers (OEMs) held the largest market share of 78.6% in 2024. Installing EV sound systems during vehicle production allows for seamless integration with onboard electronics and systems, including powertrains and infotainment units. This approach ensures legal compliance from the outset, which helps preserve warranties and streamline certification processes. OEMs benefit by reducing costs through large-scale purchasing and assembly, offering consumers built-in, regulation-ready sound solutions while maintaining manufacturing efficiency. Regulatory bodies favor OEM installation since it guarantees adherence before the vehicle hits the road.

Germany Electric Vehicle Sound Generator Market generated USD 131 million in 2024. The country's dominance is attributed to its strong automotive manufacturing base and aggressive push toward electrification. German manufacturers are among the earliest adopters of EVSG systems, leveraging regulatory requirements and innovation to stay ahead in the competitive landscape. Their approach blends strict adherence to EU sound regulations with a focus on acoustic branding, allowing automakers to create signature sound profiles that align with brand identity. The high output of electric vehicles, supported by large-scale production facilities and advanced R&D capabilities, further fuels demand for seamlessly integrated EVSG solutions.

Leading players in the EVSG market include Hyundai, ECCO, STMicroelectronics, Continental, Harman International, Aptiv, Denso, Forvia Hella, Brigade Electronics, and Ansys. To stay competitive, these companies are adopting key strategies such as advancing digital sound architecture, expanding partnerships with OEMs, and investing in AI-based sound generation. Many focus on scalable solutions for different EV types while enhancing in-vehicle integration and user experience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component manufacturers

- 3.2.3 Software developers and acoustic engineers

- 3.2.4 System integrators

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Price trend

- 3.7.1 Region

- 3.7.2 Product

- 3.8 Cost breakdown analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Regulatory mandates for pedestrian safety

- 3.11.1.2 Increasing adoption of EVs

- 3.11.1.3 Advancements in sound design and technology

- 3.11.1.4 OEM integration and brand differentiation

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High cost of advanced systems

- 3.11.2.2 Technical and standardization barriers

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 External sound generators

- 5.3 Internal sound generators

- 5.4 Customizable sound systems

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Battery electric vehicles (BEV)

- 6.3 Hybrid electric vehicles (HEV)

- 6.4 Plug-in hybrid electric vehicles (PHEV)

- 6.5 Fuel cell electric vehicles (FCEV)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicle

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Two and three wheelers

- 7.5 Off-highway vehicles

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Hardware

- 9.2.1 Speakers

- 9.2.2 Amplifiers

- 9.2.3 Controllers

- 9.2.4 Actuators

- 9.2.5 Wiring harnesses

- 9.3 Software

- 9.3.1 Sound design applications

- 9.3.2 Control systems

- 9.3.3 User interface systems

Chapter 10 Market Estimates & Forecast, By Speed Range, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Low-speed sound generators (0-30 km/h)

- 10.3 Full-speed range sound generators (more than 30 km/h)

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Ansys

- 12.2 Aptiv

- 12.3 Brigade Electronics

- 12.4 Continental

- 12.5 Denso

- 12.6 ECCO

- 12.7 ESI Group (Keysights)

- 12.8 Forvia Hella

- 12.9 General Motors

- 12.10 Harman International

- 12.11 Hyundai

- 12.12 Mercedes-Benz

- 12.13 Softeq

- 12.14 Soundracer

- 12.15 STMicroelectronics

- 12.16 Thor

- 12.17 TVS

- 12.18 Volkswagen

- 12.19 Volvo