|

시장보고서

상품코드

1755196

오프 하이웨이 차량용 엔진 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Off Highway Vehicle Engines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

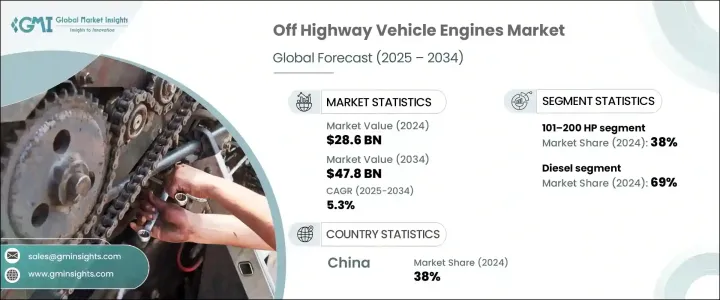

세계의 오프 하이웨이 차량용 엔진 시장은 2024년에 286억 달러로 평가되었으며 CAGR 5.3%를 나타내 2034년에는 478억 달러에 이를 것으로 추정됩니다.

시장 확대의 주요 요인은 현재 진행 중인 인프라의 진보, 농업의 기계화의 진전, 채굴 작업에 있어서의 장비 수요 증가입니다. 업계는 그 중요성을 지속적으로 높이고 있습니다. 정부가 대규모 공공 개발 프로젝트에 투자하고 농업 및 산업 생산량이 세계적으로 상승하는 동안 이러한 오프 하이웨이 분야에서 강력하고 효율적인 엔진의 필요성이 점점 커지고 있습니다.

이 성장의 주요 원동력 중 하나는 에너지 효율이 높고 저배출 가스 기술을 중시하는 경향이 강해지고 있다는 점입니다. 용량을 줄일 수 있는 차세대 엔진 시스템의 통합에 점점 더 힘을 쏟고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 286억 달러 |

| 예측 금액 | 478억 달러 |

| CAGR | 5.3% |

고출력의 저연비 엔진에 대한 수요는 특히 가혹한 조건 하에서 대형 기기가 가동하는 분야에서 높아지고 있습니다. 연비 향상, 배출 가스 저감, 성능 향상을 실현한 기존 시스템의 혁신과 업그레이드에 종사하고 있습니다.

2024년에는 출력 101-200마력의 엔진이 세계 시장을 선도해 전체의 약 38%의 점유율을 확보했습니다. 이 부문은 예측 기간 동안 5.8% 이상의 연평균 성장률(CAGR)을 나타낼 것으로 예상됩니다. 이 카테고리의 엔진의 인기는 강도와 효율의 균형에 기인하고 있으며, 여러 산업에 걸친 광범위한 중형 장비에 적합합니다.

연료의 관점에서 디젤 엔진은 2024년에도 최고 자리를 유지해 세계 시장의 약 69%를 차지했습니다. 이 부문은 2025년부터 2034년까지 6.5% 이상의 연평균 성장률(CAGR)을 나타낼 것으로 예상됩니다. 특히 원격지와 개발도상지역에서는 널리 이용 가능합니다. 그 결과, 디젤엔진은 오프 하이웨이 용도의 기간이 계속되고, 제조업체는 신뢰성이나 출력을 희생하지 않고 새로운 환경 기준에 적합하는 선진 디젤 기술의 연구를 우선하고 있습니다.

용도별로는 인프라 개발과 세계 도시화의 진전에 견인되어 건설기계 카테고리가 2024년의 주요 부문으로 부상했습니다. 탑재한 중장비에 대한 수요가 높아지고 있습니다. 이 기계는 가혹한 조건하에서 효율적으로 가동할 필요가 있어, 신뢰성이 높은 엔진 성능이 요구되기 때문에 이 분야는 시장 성장에 일관적으로 공헌하고 있습니다.

엔진 유형의 경우 2024년에도 내연 엔진(ICE)이 우위를 유지했습니다. 이 엔진은 중단없는 운전을 제공하며, 이것은 대규모의 지속적인 사용 환경에서 큰 이점이 될 것입니다.

2024년에는 중국이 아시아태평양의 오프 하이웨이 차량용 엔진 시장을 선도하여 지역 점유율의 약 38%를 차지하고 약 44억 달러의 매출을 계상했습니다. 중국의 광대한 농업 기반은 여러 업종에 걸친 생산 수요 증가에 대응할 수 있는 효율적이고 내구성 있는 엔진의 필요성을 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 부품 제조업체

- 엔진 제조업체(OEM)

- 자동차 제조업체(오프 하이웨이 OEM)

- 유통업체 및 애프터마켓 서비스 제공업체

- 이익률 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 타국에 의한 보복조치

- 업계에 미치는 영향

- 주요 원재료의 가격 변동

- 공급망 재구성

- 전력 출력과 비용에 미치는 영향

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정과 전력 출력 전략

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 기술과 혁신의 상황

- 가격 동향

- 코스트 내역 분석

- 특허 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 인프라 개발 증가

- 엔진 설계에 있어서의 기술적 진보

- 전기자동차와 하이브리드 오프 하이웨이 자동차 수요 증가

- 광업 부문의 성장

- 스마트 농업에 대한 투자 증가

- 업계의 잠재적 위험 및 과제

- 설비의 높은 초기 비용

- 유지보수 및 내구성 문제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계·예측 : 출력별(2021-2034년)

- 주요 동향

- 50HP 이하

- 50-100HP

- 101-200HP

- 201-400HP

- 400HP 이상

제6장 시장추계·예측 : 연료별(2021-2034년)

- 주요 동향

- 디젤

- 가솔린

- 기타

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 건설 장비

- 광산 장비

- 농업 장비

- 임업 장비

제8장 시장추계·예측 : 엔진별(2021-2034년)

- 주요 동향

- 내연기관(ICE)

- 하이브리드 엔진

- 전기 엔진

제9장 시장추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- Caterpillar

- CNH Industrial

- Cummins

- Deere &Company

- Doosan Infracore

- FPT Industrial

- Hatz Diesel

- Honda Motor

- Isuzu Motors

- Kohler

- Komatsu

- Kubota

- MAN

- Mitsubishi Heavy Industries

- Perkins Engines

- Scania

- Shaanxi Fast Gear

- Tata Motors

- Volvo

- Yanmar

The Global Off-Highway Vehicle Engines Market was valued at USD 28.6 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 47.8 billion by 2034. Market expansion is largely attributed to ongoing infrastructure advancements, increased mechanization in farming, and the rising demand for equipment in mining operations. These engines are essential for heavy-duty applications, and their importance continues to grow as industries seek high-performance solutions that can deliver both durability and operational efficiency. As governments invest in major public development projects and as agricultural and industrial output continue to rise globally, the need for powerful, efficient engines across these off-highway segments is becoming more critical.

One of the key drivers behind this growth is the increased emphasis on energy-efficient and low-emission technologies. The market is witnessing a notable shift as manufacturers invest in cleaner, hybrid, and electric powertrain alternatives. OEMs are increasingly focusing on the integration of next-generation engine systems that can reduce fuel usage while meeting stringent emissions regulations. This shift is motivated not only by environmental concerns but also by the rising cost of fuel and the global push toward sustainable practices. As a result, advanced engine platforms are gaining popularity in core industries where power and reliability remain non-negotiable.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $28.6 Billion |

| Forecast Value | $47.8 Billion |

| CAGR | 5.3% |

Demand for high-output, fuel-efficient engines is on the rise, especially in sectors where heavy-duty equipment operates under extreme conditions. Equipment used across various industries must deliver high torque and strong performance without compromising fuel economy. These functional requirements are pushing engine manufacturers to innovate and upgrade existing systems with enhanced fuel efficiency, lower emissions, and improved performance capabilities. OEMs are taking an active role in adopting cutting-edge technologies and are forming partnerships to design engines that meet the evolving demands of off-highway operations.

In 2024, engines with a power output ranging between 101 and 200 horsepower led the global market, securing approximately 38% of the total share. This segment is projected to grow at a CAGR of over 5.8% throughout the forecast timeline. The popularity of engines in this category stems from their balance between strength and efficiency, making them suitable for a wide range of mid-sized equipment across multiple industries. Their adaptability ensures reliable performance in diverse work environments, which keeps this segment at the forefront of demand.

From a fuel perspective, diesel-powered engines retained the top position in 2024, making up about 69% of the global market. This segment is forecasted to grow at a CAGR exceeding 6.5% between 2025 and 2034. Diesel remains the preferred choice due to its unmatched torque and energy output, especially in environments where consistent, high-power operation is vital. The global infrastructure for diesel supply is mature and widely accessible, particularly in remote or developing regions. As a result, diesel engines continue to be the backbone of off-highway applications, and manufacturers are prioritizing research into advanced diesel technologies that align with emerging environmental standards without sacrificing reliability or power.

On the application front, the construction equipment category emerged as the leading segment in 2024, driven by increased activity in infrastructure development and global urbanization. Rising investments in housing, transportation networks, and commercial infrastructure are translating into heightened demand for heavy machinery powered by robust engine systems. These machines need to operate efficiently under tough conditions, and the requirement for dependable engine performance makes this segment a consistent contributor to market growth.

Regarding engine type, internal combustion engines (ICEs) maintained their dominance in 2024. Their widespread use can be attributed to their long-standing reliability and established infrastructure. ICEs remain a popular choice, especially in regions where electrical charging facilities are sparse or inconsistent. These engines provide uninterrupted operation, which is a significant advantage in large-scale, continuous-use settings. Their ability to perform in harsh and remote environments ensures that demand remains strong, particularly in regions with growing industrialization and development.

In 2024, China led the Asia-Pacific off-highway vehicle engines market, capturing around 38% of the regional share and generating approximately USD 4.4 billion in revenue. The country's rapid industrial growth and extensive infrastructure rollout are key contributors to this leadership position. High demand for heavy machinery within the nation's development and mining sectors continues to drive engine sales. Moreover, China's expansive agricultural base adds to the requirement for efficient, durable engines capable of meeting rising output demands across multiple verticals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Engine manufacturers (OEMs)

- 3.2.4 Vehicle manufacturers (Off-Highway OEMs)

- 3.2.5 Distributors & aftermarket service providers

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Power output and cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and Power output strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising infrastructure development

- 3.11.1.2 Technological advancements in engine design

- 3.11.1.3 Growing demand for electric and hybrid off-highway vehicles

- 3.11.1.4 Growth in the mining sector

- 3.11.1.5 Increased investment in smart agricultures

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial cost of equipment

- 3.11.2.2 Maintenance and durability issues

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Power output, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Below 50 HP

- 5.3 50–100 HP

- 5.4 101–200 HP

- 5.5 201–400 HP

- 5.6 Above 400 HP

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gasoline

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Construction equipment

- 7.3 Mining equipment

- 7.4 Agricultural equipment

- 7.5 Forestry equipment

Chapter 8 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Internal combustion engines (ICE)

- 8.3 Hybrid engines

- 8.4 Electric engines

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Caterpillar

- 10.2 CNH Industrial

- 10.3 Cummins

- 10.4 Deere & Company

- 10.5 Doosan Infracore

- 10.6 FPT Industrial

- 10.7 Hatz Diesel

- 10.8 Honda Motor

- 10.9 Isuzu Motors

- 10.10 Kohler

- 10.11 Komatsu

- 10.12 Kubota

- 10.13 MAN

- 10.14 Mitsubishi Heavy Industries

- 10.15 Perkins Engines

- 10.16 Scania

- 10.17 Shaanxi Fast Gear

- 10.18 Tata Motors

- 10.19 Volvo

- 10.20 Yanmar