|

시장보고서

상품코드

1836614

오프 하이웨이 차량용 엔진 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Off Highway Vehicle Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

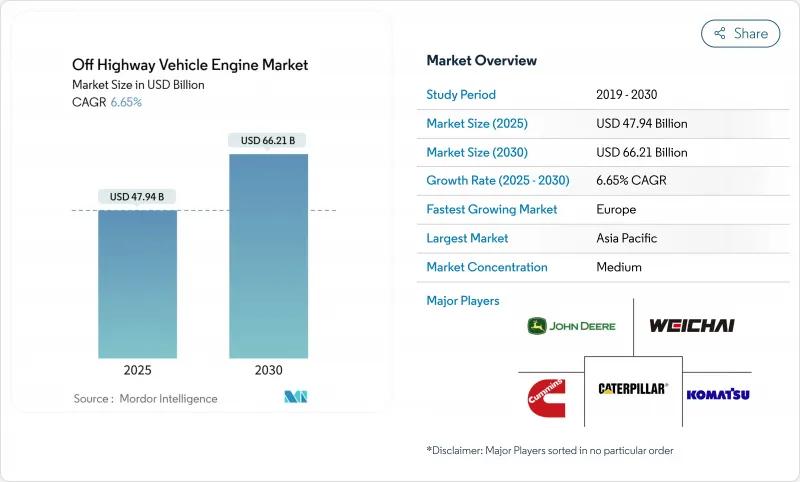

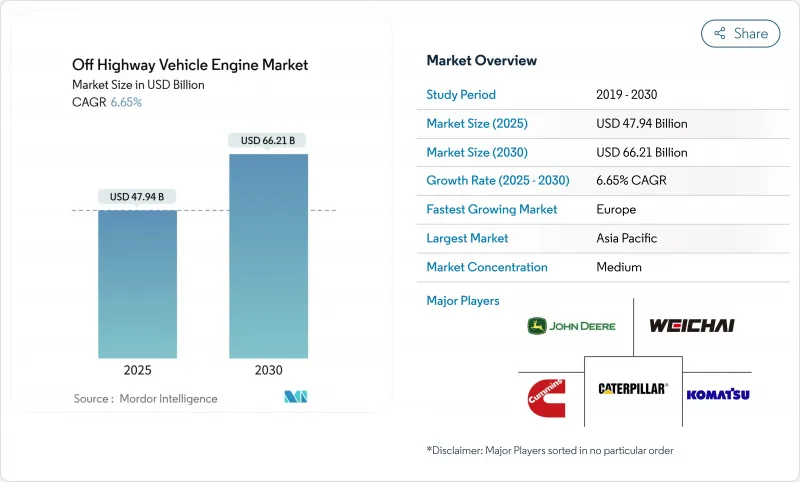

오프 하이웨이 차량용 엔진 시장 규모는 2025년에 479억 4,000만 달러, 예측 기간 중(2025-2030년) CAGR은 6.65%를 나타내고, 2030년에는 662억 1,000만 달러에 달할 것으로 예측됩니다.

인프라 지출 증가, 배기 가스 규제 강화, 농업, 광업, 자재관리 분야에서 기계화의 진전이 엔진 수요를 재구성하고 있습니다. 성장은 여전히 디젤 기술에 두고 있지만, 텔레매틱스, 예지 보전, 수소화 식물성 기름 및 재생 가능 디젤 연료와의 호환성의 급속한 진전에 도움이 되고, 하이브리드 전기 및 연료에 얽매이지 않는 플랫폼이 그 발자취를 넓히고 있습니다.

세계 오프 하이웨이 차량용 엔진 시장 동향과 통찰

대규모 세계 인프라 파이프라인(G7 및 BRI)

1조 2,000억 달러의 인프라 투자 및 고용 촉진법(Infrastructure Investment and Jobs Act)은 미국 중서부 각주에서 건설기계의 연간 매출을 10% 증가시키는 원동력이 되고 있습니다. 중국의 '일대일로(Belt and Road) 구상' 하에서의 병행투자는 아프리카, 동남아시아, 동유럽 전역에서 대형 굴삭기와 불도저 수요를 자극하고 있습니다. 중국의 수출업체는 2023년 처음으로 건설기계의 해외 출하량이 국내 판매량을 웃돌아 세계 공급 체인의 균형을 재구축하고 오프 하이웨이 자동차 엔진 시장의 수를 강화합니다. 다년간의 자금 테두리로 제조업체는 안심하고 생산 능력을 확대하고 하이브리드 대응 설계를 개량할 수 있습니다.

아시아태평양과 아프리카에서 진행되는 농업의 기계화

트랙터의 보급률은 2024년 남아시아 농장의 74%에 달했고, 물 펌프와 탈곡기의 보급률은 65%를 넘었습니다. 인도와 중국의 농촌 임금 상승이 농장을 자본 집약적인 관행으로 향하게 하여 30-120마력의 범위에서 꾸준한 교체 수요를 창출하고 있습니다. 사하라 이남의 아프리카는 기계화에서 남미를 여전히 벗어나 가혹한 현장 조건 하에서도 신뢰성 높은 성능을 발휘하는 소형 연비 효율 엔진의 상당한 잠재 수요가 있음을 보여줍니다. 서비스 지향 비즈니스 모델은 소규모 소유자가 소유권 없이 기계에 접근할 수 있게 하고, 엔진 공급업체를 위한 시장 범위를 넓히고, 오프 하이웨이 차량용 엔진 시장을 추가로 지원합니다.

소형 기계의 전동화 가속

2024년에는 전동 휠 로더가 중국 판매의 10%를 차지하고 세계 6,000-7,000대의 전동 건설 기계가 판매됩니다. 여러 중국 OEM이 100마력 미만의 레거시 엔진 공급업체에 압력을 가하여 비용 패리티를 달성. 유럽 도시에서는 디젤이 제한되어 있어 실내 해체 작업이나 폐기물 처리 작업에 배터리 채택이 가속화되고 있습니다. 그러나 장거리 채광, 임업 및 24시간 가동 채석 작업은 에너지 밀도와 신속한 연료 보급의 필요성으로 인해 여전히 디젤에 의존하고 있으며, 오프 하이웨이 자동차 엔진 시장의 핵심 수요를 유지하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- Stage V/Tier 5 규범의 엄격화가 구입전 및 개조 사이클을 유발

- OEM의 하이브리드 대응 모듈형 엔진 플랫폼으로의 전환

- 급등 후처리 비용 대 가격에 민감한 구매자

부문 분석

건설 기계는 2024년 오프 하이웨이 자동차 엔진 시장 매출의 58.36%를 차지했으며, 도로, 교량 및 교통 시스템에서 정부의 자극 조치로 그 지위가 견고해졌습니다. 아시아태평양의 거대 프로젝트와 미국의 자금 급증이 121-400마력의 블록에 의존하는 굴삭기, 도저, 로더 수요를 지지하고 있습니다. 구리, 리튬, 니켈 프로젝트는 배터리 공급망을 수용하기 위해 확대되어 광산기계가 다시 기세를 보이고 있습니다. 임업 및 자재관리의 틈새 분야에서는 급격한 지형에서 최대 330마력을 발휘하는 John Deere PowerTech(TM) PSS 9.0L과 같은 엔진이 선호됩니다. 전동 컴팩트 로더의 CAGR은 6.27%를, 듀티 사이클과 충전 액세스가 예측 가능한 장소에서의 조기 전동화의 성공을 나타내고 있습니다. 그럼에도 불구하고, 24시간 가동된 채굴 굴삭기와 갱내 운반에는 여전히 고마력의 디젤이 불가결하며, 오프 하이웨이 차량용 엔진 시장의 대수를 유지하고 있습니다.

유럽의 소형 건설 차량은 공회전 시간을 줄이기 위해 텔레매틱스를 채택하여 연료 소비량을 12% 줄이고 오버홀 간격을 연장합니다. 아시아 렌탈 사업자는 서비스 접근이 용이한 모듈형 엔진을 선호하며, 바쁜 도시 지역의 현장에서의 다운타임을 낮게 억제하고 있습니다. 아프리카의 '벨트 앤 로드' 프로젝트에서는 연비 효율과 터프니스를 밸런싱시킨 90-200kW의 미드레인지 엔진에 대한 수요가 높아지고 있습니다. 라틴아메리카의 광업 대기업은 현지 규제 강화에 대비하여 EU 스테이지 V에 준거한 파워트레인을 요구하고 있습니다. 이러한 역학이 결합되어 건설 기계는 극 위치를 유지하고 광산기계는 오프 하이웨이 차량 엔진 시장에서 점진적으로 점유율을 확대하고 있습니다.

31-70마력의 카테고리는 2024년 오프 하이웨이 차량용 엔진 시장 점유율의 64.51%를 차지하고, 2030년까지의 CAGR은 7.02%를 기록할 전망입니다. 도시의 고밀도화에 의해 좁은 도로에 적합해, 마무리면에의 감싸 피해를 경감하는 조종성이 높은 기계가 요구되고 있습니다. OEM은 스타트 스톱 기능과 고급 연료 맵을 통합하여 함대 매니저에 호소하는 2자리 소비 절감을 촉구하고 있습니다. 텔레매틱스 플랫폼은 아이들링 시간을 시각화하고 딜러를 방문하지 않고 지역의 소음과 배기가스 규제를 충족시키기 위한 파라미터 미세 조정을 무선으로 실시할 수 있습니다.

캐터필러의 3512B-EUI(1,450마력)가 벤치마크인 계속되는 부문인 채굴 트럭이나 대형 유압 굴삭기에서는 400마력 이상의 높은 브래킷이 사용되고 있습니다. 수가 적음에도 불구하고 이러한 엔진은 프리미엄 가격과 애프터마켓 부품 수입을 요구합니다. 반대로 30마력 이하의 플랫폼은 배터리 팩이 잔디 관리, 골프 코스, 소규모 지자체 작업으로 풀 시프트의 성능을 발휘하게 되었기 때문에 전동화의 침식에 가장 시달리고 있습니다. 그 결과, 연구개발비는 오프 하이웨이 차량용 엔진 시장을 지원하는 미드레인지 제품으로 향하는 한편, 고마력의 프레스티지 라인은 유지되게 됩니다.

지역별 분석

아시아태평양은 대규모 인프라 계획과 농업 기계화의 가속으로 2024년 38.17%의 매출을 유지했습니다. 중국은 2023년 국내 판매량을 초과하는 건설기계를 수출하고 국내 연조를 완화하고 창사와 서주에서 생산되는 엔진의 세계 채널을 창출했습니다. 인도에서는 정부 보조금으로 트랙터 구매가 용이해지고 몬순 변동에도 불구하고 2025년 소매량이 증가합니다. 수요는 혼잡한 도시의 작업 현장이나 소규모 농지에서의 작업에 적합한 31-120마력의 유닛으로 치우칩니다. 현지 OEM은 리엔지니어링 없이 아프리카와 유럽에 출하할 수 있도록 Tier 3과 스테이지 V 모두에서 인증된 모듈형 엔진을 선호하며 오프 하이웨이 자동차 엔진 시장의 확장성을 강화하고 있습니다.

CAGR 7.19%로 성장하는 유럽은 Stage V의 컴플라이언스 투자와 철도, 재생에너지, 순환형 경제 시설에 중점을 둔 Green Deal의 혜택을 받고 있습니다. 고객은 패시브 재생 기능이 있는 미립자 필터와 탄소 회계 대시보드를 통합한 텔레매틱스를 선호합니다. 고마츠의 스테이지 V 포트폴리오는 보다 오랜 기간 유지보수가 필요 없습니다는 것을 입증했으며, 엄격한 가동률 목표에 직면한 임대 회사들에게 설득력 있는 제안이 되었습니다. 유럽의 지자체도 수소 ICE 쓰레기 수거 차량을 시험적으로 도입하고 있으며, 공급업체는 대체 연료의 연구 개발을 지원하고 있습니다.

북미는 인프라 투자 및 고용촉진법을 활용하여 주간 고속도로 개수, 다리 교체, 항만 준설을 위한 지속적인 엔진 수요를 뒷받침하고 있습니다. 캘리포니아에서 곧 시행되는 Tier 5 규제는 세계적으로 가장 엄격한 기준을 설정하는 것으로, OEM 각사는 시행 몇년앞을 내다보고 차세대 SCR과 암모니아 센서의 테스트에 임할 것입니다. 남미, 중동, 아프리카는 고성장이지만 비용에 민감한 지역입니다. 통화의 역풍과 자금 조달의 격차에 의해 당면의 보급은 한정적이지만, 코모디티 사이클이 개선해, 다국간 금융기관이 아시아로부터 수입된 신뢰성이 높은 중마력 엔진이나 브라질에서 재생산된 엔진에 의존하는 도로, 발전소, 관개 계획을 후원하게 되면 상승 여력을 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 방대한 세계 인프라 파이프라인(G7과 BRI)

- 아시아태평양과 아프리카에서의 농업의 기계화의 진전

- Stage V/Tier 5 기준의 엄격화에 의해 사전 구입과 레트로 피트 사이클이 활성화

- OEM의 모듈식 하이브리드 대응 엔진 플랫폼으로의 시프트

- 텔레매틱스 주도의 예지 보전이 교환 사이클을 단축

- HVO/재생 가능 디젤의 호환성이 ICE의 관련성을 확대

- 시장 성장 억제요인

- 소형 기기의 전동화의 가속

- 후처리 비용의 급등과 가격에 민감한 바이어와의 경쟁

- 상품 가격의 변동이 엔진의 이폭을 압박

- 정비 간격을 연장하는 임대 차량

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌 의식의 강도

제5장 시장 규모 및 성장 예측 : 금액(USD)

- 차량 유형별

- 농업기계

- 건설기계

- 광산기계

- 임업 및 자재관리 기기

- 출력(HP)별

- 30 HP 이하

- 31-70 HP

- 71-120 HP

- 121-400 HP

- 400HP 이상

- 연료 유형별

- 디젤

- 가솔린

- 천연가스/바이오가스

- 하이브리드 전기연료 전지

- 엔진 배기량(L)별

- 2L 이하

- 2.1-3.5 L

- 3.6-7 L

- 7L 이상

- 추진기술별

- 기존 ICE

- 하이브리드

- 배터리 전기

- 연료전지 전기

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이집트

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AGCO Corporation

- Caterpillar Inc.

- Cummins Inc.

- Deere & Company

- Deutz AG

- Komatsu Ltd

- Mahindra Powertrain

- Scania AB

- Volvo Penta

- Yanmar Co.

- Weichai Power

- Kubota Corporation

- Perkins Engines

- MAN Engines

- Rolls-Royce Power Systems(MTU)

- Doosan Infracore

- FPT Industrial

- Kohler Engines

- Hatz Diesel

제7장 시장 기회와 전망

SHW 25.10.28The Off Highway Vehicle Engine Market size is estimated at USD 47.94 billion in 2025, and is expected to reach USD 66.21 billion by 2030, at a CAGR of 6.65% during the forecast period (2025-2030).

Increasing infrastructure spending, tighter emission rules, and rising mechanization across agriculture, mining, and material-handling applications are reshaping engine demand. Growth remains anchored in diesel technology but hybrid-electric and fuel-agnostic platforms are widening their footprint, helped by rapid progress in telematics, predictive maintenance, and compatibility with hydrotreated vegetable oil and renewable diesel fuels.

Global Off Highway Vehicle Engine Market Trends and Insights

Massive Global Infrastructure Pipeline (G7 & BRI)

The USD 1.2 trillion Infrastructure Investment and Jobs Act is driving annual construction equipment sales growth of 10% across the US Midwest states. Parallel investments under China's Belt and Road Initiative stimulate demand for heavy excavators and bulldozers across Africa, Southeast Asia, and Eastern Europe. Chinese exporters shipped more construction machines abroad than they sold domestically for the first time in 2023, rebalancing global supply chains and reinforcing volume in the off-highway vehicle engine market. Multi-year funding windows enable manufacturers to scale capacity and refine hybrid-ready designs with confidence.

Growing Mechanization of Agriculture in Asia-Pacific and Africa

Tractor penetration reached 74% of South Asian farms in 2024, while water pumps and threshers exceeded 65% adoption. Rising rural wages across India and China push farms toward capital-intensive practices, creating steady replacement demand in the 30-120 HP range. Sub-Saharan Africa still trails South America in mechanization, signaling a sizeable addressable pool for compact, fuel-efficient engines that perform reliably in harsh field conditions. Service-oriented business models allow smallholders to access machinery without ownership, broadening market reach for engine suppliers and further supporting the off-highway vehicle engine market.

Accelerating Electrification of Compact Equipment

Electric wheel loaders captured 10% of Chinese sales in 2024, with 6,000-7,000 electric construction machines sold worldwide. Cost parity achieved by several Chinese OEMs pressures legacy engine providers in the sub-100 HP class. European urban zones restrict diesel, accelerating battery adoption for indoor demolition and waste-handling tasks. However, long-haul mining, forestry, and 24-hour quarry operations still rely on diesel due to energy density and quick refueling needs, preserving core demand inside the off highway vehicle engine market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Stage V / Tier 5 Norms Triggering Pre-buy & Retrofit Cycles

- OEM Shift to Modular Hybrid-Ready Engine Platforms

- Escalating After-treatment Cost vs. Price-Sensitive Buyers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Construction equipment generated 58.36% of 2024 off-highway vehicle engine market revenue, a position fortified by government stimulus in roads, bridges, and transit systems. Asia Pacific megaprojects, together with the US funding surge, sustain demand for excavators, dozers, and loaders that rely on 121-400 HP blocks. Mining equipment shows renewed momentum because copper, lithium, and nickel projects expand to meet battery supply chains. Forestry and materials-handling niches favor engines like the John Deere PowerTech(TM) PSS 9.0 L delivering up to 330 hp in steep terrain. Electric compact loaders post a 6.27% CAGR, illustrating early electrification success where duty cycles and charging access are predictable. Nevertheless, high-horsepower diesel remains essential for round-the-clock mining shovels and underground haulage, upholding volume in the off highway vehicle engine market.

Compact construction fleets in Europe adopt telematics to trim idle hours, cutting fuel burn by 12% and extending overhaul intervals. Asian rental operators prefer modular engines with easy service access, keeping downtime low on busy urban sites. Belt and Road projects in Africa pull demand for mid-range 90-200 kW engines that balance fuel efficiency and toughness. Mining majors in Latin America request EU Stage V compliant powertrains to future-proof assets against tightening local rules. Together, these dynamics keep construction equipment in pole position while mining gradually widens its share of the off highway vehicle engine market.

The 31-70 HP category held 64.51% of off-highway vehicle engine market share in 2024 and records a 7.02% CAGR to 2030, fueled by compact excavators, skid-steers, and mid-size tractors used in rice paddies and horticulture. Urban densification calls for maneuverable machinery that fits narrow streets and reduces collateral damage on finished surfaces. OEMs integrate start-stop functions and advanced fuel maps, claiming double-digit consumption cuts that appeal to fleet managers. Telematics platforms visualize idle time and enable over-the-air parameter tweaks to meet local noise or emission constraints without dealership visits.

Higher brackets above 400 HP serve mining trucks and large hydraulic shovels, segments where Caterpillar's 3512B-EUI at 1,450 hp remains a benchmark. Despite lower unit volumes, these engines command premium pricing and aftermarket parts revenue. Conversely, sub-30 HP platforms suffer most from electrification encroachment because battery packs now deliver full-shift performance for lawn care, golf course, and small municipal tasks. The resulting polarization directs R&D spending toward mid-range products that anchor the off highway vehicle engine market while preserving high-horsepower prestige lines.

The Off Highway Vehicle Engine Market Report is Segmented by Vehicle Type (Agricultural Machinery and More), Power Output (Less Than or Equal To 30 HP, 31-70 HP, and More), Fuel Type (Diesel, Gasoline, and More), Engine Displacement (Less Than or Equal 2 L, 2. 1 To 3. 5 L, and More), Propulsion Technology (Conventional ICE and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained 38.17% revenue in 2024 due to large-scale infrastructure programs and accelerating farm mechanization. China exported more construction equipment than it sold at home during 2023, cushioning domestic softness and creating a global channel for engines produced in Changsha and Xuzhou. India's government subsidies improve tractor affordability, lifting 2025 retail volumes despite monsoon variability. Demand skews toward 31-120 HP units maneuvering in congested urban job sites or small farm plots. Regional OEMs favor modular engines certified for both Tier 3 and Stage V so they can ship to Africa or Europe without re-engineering, reinforcing the scalability of the off-highway vehicle engine market.

Europe, growing at 7.19% CAGR, benefits from Stage V compliance investments and the Green Deal's focus on rail, renewable energy, and circular economy facilities. Customers prioritize particulate filters with passive regeneration and telematics, integrating carbon accounting dashboards. Komatsu's Stage V portfolio demonstrates maintenance-free operation for a longer duration, a compelling proposition for rental firms facing tight utilization targets. European municipalities also pilot hydrogen ICE refuse trucks, supporting supplier R&D in alternative fuels.

North America capitalizes on the Infrastructure Investment and Jobs Act, which underwrites sustained engine demand for interstate highway revamps, bridge replacements, and port dredging. California's forthcoming Tier 5 rules set the strictest global bar, pushing OEMs to test next-generation SCR and ammonia sensors several years ahead of enforcement. South America, the Middle East, and Africa represent high-growth but cost-sensitive regions. Currency headwinds and financing gaps limit immediate penetration yet offer upside as commodity cycles improve and multilateral lenders sponsor roads, power plants, and irrigation schemes that rely on reliable medium-horsepower engines imported from Asia or remanufactured in Brazil.

- AGCO Corporation

- Caterpillar Inc.

- Cummins Inc.

- Deere & Company

- Deutz AG

- Komatsu Ltd

- Mahindra Powertrain

- Scania AB

- Volvo Penta

- Yanmar Co.

- Weichai Power

- Kubota Corporation

- Perkins Engines

- MAN Engines

- Rolls-Royce Power Systems (MTU)

- Doosan Infracore

- FPT Industrial

- Kohler Engines

- Hatz Diesel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Massive global infrastructure pipeline (G7 & BRI)

- 4.2.2 Growing mechanization of agriculture in Asia-Pacific and Africa

- 4.2.3 Stricter Stage V / Tier 5 norms triggering pre-buy & retrofit cycles

- 4.2.4 OEM shift to modular hybrid-ready engine platforms

- 4.2.5 Telematics-driven predictive maintenance shortening replacement cycles

- 4.2.6 HVO/renewable-diesel compatibility extending ICE relevance

- 4.3 Market Restraints

- 4.3.1 Accelerating electrification of compact equipment

- 4.3.2 Escalating after-treatment cost vs. price-sensitive buyers

- 4.3.3 Commodity-price volatility squeezing engine margins

- 4.3.4 Rental fleets extending overhaul intervals

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Agricultural Machinery

- 5.1.2 Construction Equipment

- 5.1.3 Mining Equipment

- 5.1.4 Forestry & Material-Handling Equipment

- 5.2 By Power Output (HP)

- 5.2.1 Less than or equal to 30 HP

- 5.2.2 31-70 HP

- 5.2.3 71-120 HP

- 5.2.4 121-400 HP

- 5.2.5 More than 400 HP

- 5.3 By Fuel Type

- 5.3.1 Diesel

- 5.3.2 Gasoline

- 5.3.3 Natural-/Bio-Gas

- 5.3.4 Hybrid-Electric & Fuel-Cell

- 5.4 By Engine Displacement (L)

- 5.4.1 Less than or equal 2 L

- 5.4.2 2.1 to 3.5 L

- 5.4.3 3.6 to 7 L

- 5.4.4 More than 7 L

- 5.5 By Propulsion Technology

- 5.5.1 Conventional ICE

- 5.5.2 Hybrid

- 5.5.3 Battery-Electric

- 5.5.4 Fuel-Cell Electric

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Egypt

- 5.6.5.4 Turkey

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.3.1 AGCO Corporation

- 6.3.2 Caterpillar Inc.

- 6.3.3 Cummins Inc.

- 6.3.4 Deere & Company

- 6.3.5 Deutz AG

- 6.3.6 Komatsu Ltd

- 6.3.7 Mahindra Powertrain

- 6.3.8 Scania AB

- 6.3.9 Volvo Penta

- 6.3.10 Yanmar Co.

- 6.3.11 Weichai Power

- 6.3.12 Kubota Corporation

- 6.3.13 Perkins Engines

- 6.3.14 MAN Engines

- 6.3.15 Rolls-Royce Power Systems (MTU)

- 6.3.16 Doosan Infracore

- 6.3.17 FPT Industrial

- 6.3.18 Kohler Engines

- 6.3.19 Hatz Diesel

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment