|

시장보고서

상품코드

1766215

열성형 FFS 기계 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Thermoform Form-Fill-Seal Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

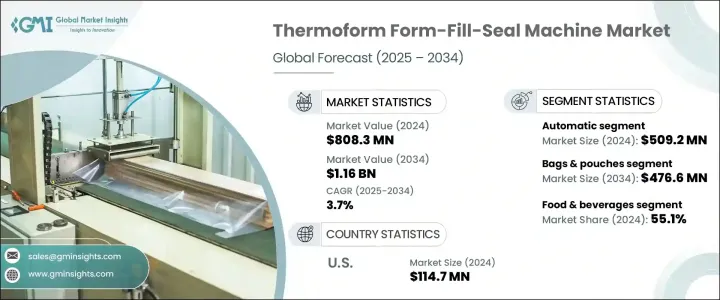

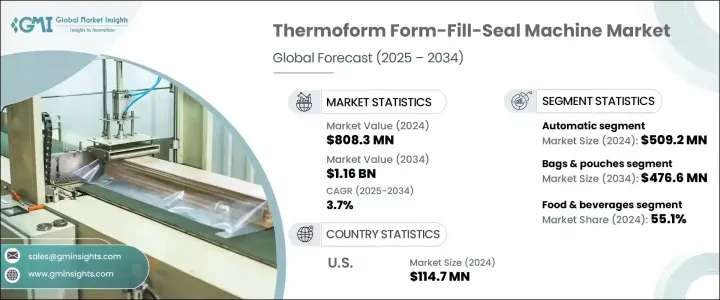

세계의 열성형 FFS 기계 시장은 2024년에는 8억 830만 달러에 달했고, CAGR 3.7%를 나타내며 2034년에는 11억 6,000만 달러에 이를 것으로 예측되고 있습니다.

이 성장은 세계 소비 증가와 지속가능성과 환경 친화적인 제조로의 급무 변화로 촉진됩니다. 플라스틱 폐기물 규제가 진화함에 따라 이러한 기계는 현재 재활용 가능한 머티리얼과 생분해성 머티리얼을 다루도록 설계되었습니다. 기업은 환경정책을 준수할 뿐만 아니라 지속가능한 패키징에 대한 소비자의 선호도를 높이기 위해 차세대 장비에 투자하고 있습니다. 서큘러 이코노미의 실천과 스마트 팩토리의 노력은 혁신적인 자동 포장 기술의 채용을 뒷받침하고 있습니다.

의약품, 식품, 소비재 등의 업계에서는 안전성의 향상, 내 탬퍼성, 유통 기한의 연장 등의 요구를 충족시키기 위해서, 열성형 FFS 기계의 사용이 증가하고 있습니다. 예측 유지 보수 및 공정 최적화를 위한 센서와 IoT 지원 시스템의 통합은 인더스트리 4.0 표준 하에서 기세를 늘리고 있습니다. 이 진화는 포장 라인을 세계적으로 재구성하고 기계를 보다 효율적으로 만들고 다양한 소재와 제품 유형에 적응하면서 비용 효율적이고 환경 친화적인 운영을 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 8억830만 달러 |

| 예측 금액 | 11억 6,000만 달러 |

| CAGR | 3.7% |

2024년 자동 열성형 FFS 기계 분야는 5억 920만 달러를 기록했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.5%를 나타낼 것으로 예측됩니다. 자동 모델은 빠르고 안정적이며 지속 가능한 패키징에 대한 수요가 증가함에 따라 널리 채택되었습니다. 수작업을 생략하면 인건비를 줄이고 일관성을 높이고 생산 라인의 처리량을 향상시킬 수 있습니다. 이 기계는 실시간 추적, 프로그래머블 로직 컨트롤러(PLC), 직관적인 터치스크린 컨트롤 등의 고급 인터페이스를 갖추고 있어 사용자 경험을 향상시키고 운영 효율성을 높입니다. 여러 포맷 및 기판에 대한 적응성은 섹터를 넘어서는 다양한 용도에 적합합니다.

가방과 파우치 포장 형식은 2024년에 세계 시장을 선도했고, 39.1%의 점유율을 확보했으며, 2034년에는 4억 7,660만 달러에 이를 것으로 예측되고 있습니다. 현재 관리된 분위기에서의 밀봉 기능을 제공하고 신선도를 확보하고 유통 기한을 연장하고 있습니다.또, 퇴비화 가능하고 환경에 안전한 소재의 사용을 서포트하도록 진화하고 있습니다.

2024년 미국의 열성형 FFS 기계 시장 규모는 1억 1,470만 달러로 평가되었고, 2034년까지의 CAGR은 3.9%를 나타낼 것으로 예상됩니다. 의류 솔루션의 채택 확대와 지속 가능한 실천과 밀접하게 관련되어 있습니다.

열성형 FFS 기계 시장 주요 기업은 DS Smith, Anchor Packaging, Inc. Huhtamaki Oyj, ProMach, Amcor PLC, Winpak Ltd. Bosch Packaging Technology, Placon Corporation, Barry-Wehmiller Group, Packcor Packaging Corporation, Sealed Air Corporation, Sealed Air Corporation, Company, Coesia Group 등이 있습니다. 세계의 열성형 FFS 기계 시장에서의 지위를 강화하기 위해 각 회사는 기계의 신뢰성을 높이고 가동 정지 시간을 단축하는 스마트 오토메이션 기능과 디지털 감시 툴의 통합에 주력하고 있습니다.

많은 기업들은 진화하는 환경 규제를 준수하고 재활용 가능한 재료와 생분해성 재료의 처리를 지원하기 위한 연구개발에 투자하고 있습니다. 전략적 파트너십은 공급망 능력과 제품 혁신을 강화하기 위해 형성되어 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 기회

- 성장 가능성 분석

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 기계 유형별

- 규제 상황

- 표준 및 규정 준수 요건

- 지역 규제 틀

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 수동

- 반자동

- 전자동

제6장 시장 추계·예측 : 포장 형태별(2021-2034년)

- 주요 동향

- 가방 및 파우치

- 컵 및 트레이

- 병

- 봉지

- 판지

- 기타

제7장 시장 추계·예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 식품 및 음료

- 의약품

- 화장품 및 퍼스널케어

- 화학약품

- 기타

제8장 시장 추계·예측 : 재료별(2021-2034년)

- 주요 동향

- 플라스틱

- 종이

- 알루미늄 호일

- 다층 필름

- 생분해성 재료

- 기타

제9장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 간접 판매

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제11장 기업 프로파일

- Amcor PLC

- Anchor Packaging, Inc.

- Barry-Wehmiller Group

- Bosch Packaging Technology

- Coesia Group

- DS Smith

- Huhtamaki Oyj

- Mondi Group

- Paccor Packaging Corporation

- Placon Corporation

- ProMach

- Sealed Air Corporation

- Sonoco Products Company

- Syntegon

- Winpak Ltd.

The Global Thermoform Form-Fill-Seal Machine Market was valued at USD 808.3 million in 2024 and is estimated to grow at a CAGR of 3.7% to reach USD 1.16 billion by 2034. This growth is fueled by rising global consumption and the urgent shift toward sustainability and eco-conscious manufacturing. With evolving plastic waste regulations, these machines are now designed to handle recyclable and biodegradable materials. Businesses are investing in next-generation equipment not only to stay compliant with environmental policies but also to align with growing consumer preferences for sustainable packaging. The push toward circular economy practices and smart factory initiatives is encouraging the adoption of innovative, automated packaging technologies.

In industries such as pharmaceuticals, food, and consumer goods, thermoform form-fill-seal machines are increasingly used to meet demands for improved safety, tamper resistance, and longer shelf life. The integration of sensors and IoT-enabled systems for predictive maintenance and process optimization is gaining momentum under Industry 4.0 standards. This evolution is reshaping packaging lines globally, making machines more efficient and adaptive to a wide variety of materials and product types while supporting cost-effective and environmentally friendly operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $808.3 million |

| Forecast Value | $1.16 billion |

| CAGR | 3.7% |

In 2024, the automatic thermoform form-fill-seal machine segment recorded USD 509.2 million and is expected to grow at a CAGR of 4.5% between 2025 and 2034. Automatic models are being widely adopted due to their ability to meet rising demands for fast, reliable, and sustainable packaging. The elimination of manual tasks reduces labor costs, enhances consistency, and increases throughput across manufacturing lines. These machines are equipped with advanced interfaces like real-time tracking, programmable logic controllers (PLCs), and intuitive touchscreen controls, which improve user experience and boost operational efficiency. Their adaptability to multiple formats and substrates makes them suitable for an expanding range of applications across sectors.

The bags and pouches packaging format led the global market in 2024, securing a 39.1% share and is forecasted to reach USD 476.6 million by 2034. The growing popularity of convenience foods and health-focused packaged goods is increasing demand for secure and hygienic packaging solutions. Form-fill-seal systems now offer controlled atmosphere sealing capabilities, ensuring freshness and extending shelf life. They are also evolving to support the use of compostable and environmentally safe materials. Regulations that prioritize food safety and packaging integrity continue to drive innovation in this category, as manufacturers seek tamper-proof and contamination-resistant solutions.

United States Thermoform Form-Fill-Seal Machine Market generated USD 114.7 million in 2024, with an anticipated CAGR of 3.9% through 2034. Growth in the U.S. is closely linked to expanding adoption of flexible packaging solutions and sustainable practices across the consumer goods, healthcare, and food and beverage sectors. Increasing demand for eco-friendly alternatives is also pushing companies to upgrade packaging lines with newer, more energy-efficient technologies.

Leading players in the Thermoform Form-Fill-Seal Machine Market include DS Smith, Anchor Packaging, Inc., Huhtamaki Oyj, ProMach, Amcor PLC, Winpak Ltd., Bosch Packaging Technology, Placon Corporation, Barry-Wehmiller Group, Paccor Packaging Corporation, Sealed Air Corporation, Syntegon, Mondi Group, Sonoco Products Company, and Coesia Group. To strengthen their position in the global thermoform form-fill-seal machine market, companies are focusing on integrating smart automation features and digital monitoring tools that enhance machine reliability and reduce operational downtime.

Many are investing in research and development to support the processing of recyclable and biodegradable materials in compliance with evolving environmental regulations. By incorporating flexible design features, these manufacturers are making machines compatible with various packaging formats and substrates. Strategic partnerships with raw material suppliers and OEMs are being formed to enhance supply chain capabilities and product innovation. Some are expanding their geographic presence by setting up regional service centers and technical support hubs to better serve localized markets and reduce lead times.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Machine type

- 2.2.3 End use industry

- 2.2.4 Packaging type

- 2.2.5 Material type

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By machine type

- 3.7 Regulatory landscape

- 3.7.1 standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034, (USD Million)(Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Semi-automatic

- 5.4 Fully automatic

Chapter 6 Market Estimates & Forecast, By Packaging Type, 2021 - 2034, (USD Million)(Thousand Units)

- 6.1 Key trends

- 6.2 Bags & pouches

- 6.3 Cups & trays

- 6.4 Bottles

- 6.5 Sachets

- 6.6 Cartons

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021 - 2034, (USD Million)(Thousand Units)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Pharmaceuticals

- 7.4 Cosmetics & personal care

- 7.5 Chemicals

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Material Type, 2021 - 2034, (USD Million)(Thousand Units)

- 8.1 Key trends

- 8.2 Plastic

- 8.3 Paper

- 8.4 Aluminum foil

- 8.5 Multi-layer films

- 8.6 Biodegradable materials

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Million)(Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Million)(Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Amcor PLC

- 11.2 Anchor Packaging, Inc.

- 11.3 Barry-Wehmiller Group

- 11.4 Bosch Packaging Technology

- 11.5 Coesia Group

- 11.6 DS Smith

- 11.7 Huhtamaki Oyj

- 11.8 Mondi Group

- 11.9 Paccor Packaging Corporation

- 11.10 Placon Corporation

- 11.11 ProMach

- 11.12 Sealed Air Corporation

- 11.13 Sonoco Products Company

- 11.14 Syntegon

- 11.15 Winpak Ltd.