|

시장보고서

상품코드

1766269

유아용 주스 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Baby Juice Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

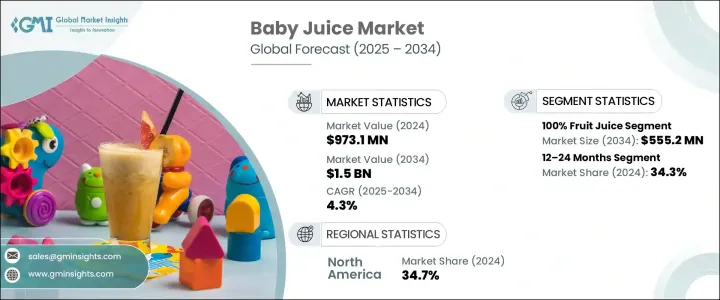

세계의 유아용 주스 시장은 2024년에는 9억 7,310만 달러로 평가되었고, 2034년에는 15억 달러에 이를 것으로 추정되며CAGR 4.3%로 성장할 전망입니다. 이러한 꾸준한 성장은 유아 영양에 대한 부모들의 인식이 높아지고 있음을 반영합니다. 부모들은 영유아에게 균형 잡힌 영양이 풍부한 식단을 제공하기 위해 점점 더 많은 관심을 기울이고 있으며, 필수 비타민과 미네랄이 풍부한 유아용 주스가 인기 있는 선택지가 되고 있습니다. 전 세계적으로 건강에 대한 의식이 높아짐에 따라 편리하고 영양이 강화된 제품에 대한 수요가 증가하고 있습니다. 또한, 직장 여성의 증가와 이중 소득 가구 등 생활 방식의 변화는 즉석 섭취 가능한 유아 식품 및 음료에 대한 의존도를 높이고 있습니다. 이러한 주스는 바쁜 일정으로 인해 자주 이동하는 부모들에게 빠르고 실용적인 해결책을 제공합니다.

라틴 아메리카, 아시아태평양, 아프리카 등 여러 지역의 신흥 시장 성장도 중요한 역할을 하고 있습니다. 출산율 증가, 가처분 소득 증가, 전자상거래 채널 강화 등 소매 인프라의 개선이 유아 영양 제품의 보급을 뒷받침하고 있습니다. 중산층 인구가 계속 증가함에 따라 포장된 유아용 주스의 접근성이 높아지고 있으며, 이는 서비스가 부족한 지역의 시장 침투를 촉진하고 이 부문의 전 세계적 확장을 공고히 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 9억 7,310만 달러 |

| 예측 금액 | 15억 달러 |

| CAGR | 4.3% |

100% 과일 주스 부문은 2034년까지 5억 5,520만 달러에 달할 것으로 예상되며, 2034년까지 연평균 4.5%의 성장률을 보일 것으로 전망됩니다. 건강에 민감한 구매 행동이 주류로 자리잡고 있으며, 어린이 식단에서 과도한 설탕 섭취에 대한 우려로 소비자들이 천연 대체품으로 눈을 돌리고 있습니다. 부모들은 첨가물이 없고 실제 과일 함량이 높은 주스를 선호하고 있습니다. 이러한 주스를 활력 있고 자연스럽고 생기가 넘치는 제품으로 포지셔닝하는 지속적인 홍보 및 인식 제고 캠페인은 영양에 민감한 오늘날의 육아 부모들의 공감을 얻고 있습니다. 이러한 선호도는 아이들의 균형 잡힌 성장을 지원하는 건강에 좋은 식품으로의 전환과 일치합니다.

연령대별로는 12-24개월 부문이 2024년에 34.3%의 점유율을 차지했으며, 2034년까지 연평균 6.8%의 성장률을 보일 것으로 예상됩니다. 이 단계는 아이들이 모유나 분유에서 주스 등 다양한 고형 및 반고형 식품으로 식단을 전환하기 시작하는 중요한 식습관 변화의 시기입니다. 이 부문의 부모들은 맛이 좋을 뿐 아니라 면역력, 소화 및 전반적인 발달을 지원하는 제품을 특히 신중하게 선택합니다. 이 연령대에 맞는 유아용 주스에는 일반적으로 비타민 C, 철분 및 기타 중요한 영양소가 함유되어 있으며, 천연 성분에 중점을 두고 있습니다. 포장도 중요한 역할을 합니다. 흘리지 않는 인체 공학적인 병은 혼자서 마시는 법을 배우는 유아를 위해 설계되어 부모와 어린 아이들 모두에게 매력적입니다.

2024년 북미의 유아용 주스 시장은 34.7%의 점유율을 차지했습니다. 이 지역의 리더십은 발전된 유통 시스템, 높은 가처분 소득, 클린 라벨, 강화형, 유기농 제품으로의 전환 추세에 힘입고 있습니다. 미국과 캐나다의 부모들은 유아기의 영양을 우선으로 하는 정보에 기반한 구매 결정을 점점 더 많이 촉진하고 있습니다. 제품 라벨링 및 안전에 관한 규제가 특히 엄격하여, 판매되는 제품에 대한 신뢰가 구축되어 있습니다. 정부의 감독과 영양에 중점을 둔 라벨링은 견고하고 투명한 유아용 주스 생태계를 조성하여 품질의 일관성과 소비자 안전을 보장합니다.

전 세계 유아용 주스 시장에서 활동하는 주요 기업으로는 Beech-Nut Nutrition Company, The Kraft Heinz Company, Sprout Foods, Inc., Campbell Soup Company 및 Nestle S.A.가 있습니다. 주요 브랜드들은 유기농, 비유전자변형, 알레르기 유발 성분이 없는 제품으로 제품 포트폴리오를 다양화하여 시장 지위를 강화하고 있습니다. 많은 기업들이 영양에 민감한 부모들을 공략하기 위해 비타민, 미네랄, 프로바이오틱스가 강화된 기능성 음료로 사업을 확장하고 있습니다. 재밀봉 가능하고 흘러나오지 않는 용기 등 매력적이고 편리한 포장재에 대한 전략적 투자는 부모와 영유아 모두의 사용 편의성을 높이고 있습니다. 브랜드들은 밀레니얼과 제너레이션 Z 부모층과 소통하기 위해 디지털 마케팅과 소셜 미디어 플랫폼을 활용하며, 전자상거래를 통해 유통망을 확대해 접근성을 높이고 있습니다. 소아 영양 전문가와의 협업과 안전 인증 준수 역시 건강에 민감한 소비자들의 브랜드 신뢰도와 신뢰도를 높이는 데 기여하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 편리한 유아 식품에 대한 수요 증가

- 개발도상국의 가처분 소득 증가

- 여성 근로자 인구 증가

- 제품 혁신 및 강화

- 산업의 잠재적 리스크 및 과제

- 유아기 조기 주스 섭취에 대한 소아과 전문가의 권고

- 설탕 함량 관련 건강 문제

- 전체 과일 및 집에서 만든 제품에 대한 선호도

- 엄격한 규제 프레임워크

- 시장 기회

- 유기농 및 천연 제품 개발

- 신흥 시장 확장

- 전자상거래 성장

- 기능성 및 강화 유아용 주스 제품

- 성장 가능성 분석

- 규제 상황

- 전 세계의 유아식 및 음료에 대한 규제

- FDA 규제 및 가이드라인

- 유럽 연합의 규제 프레임워크

- 주스의 HACCP 요건

- 라벨 표시와 건강 강조 표시 규제

- 규제가 시장 성장에 미치는 영향

- Porter's Five Forces 분석

- PESTEL 분석

- 현재의 기술 동향

- 신흥기술

- 성장 촉진요인

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속 가능한 사례

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 친환경 활동

- 소비자 행동 분석

- 부모의 취향과 결정 요인

- 구입 패턴

- 소아과의 권장 사항의 영향

- 건강과 영양에 관한 의식

- 브랜드 로얄티와 환승 행동

- 소아 영양의 동향

- 유아영양에 관한 가이드라인의 진화

- 연령에 따른 음료의 추천

- 유아기의 설탕 섭취에 관한 우려

- 아이의 개발에 있어서의 주스의 역할

- 영유아용 대체 음료

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 100% 과일 주스

- 과일 주스 블렌드

- 야채 주스

- 유기농 유아용 주스

- 강화 유아용 주스

- 기타

제6장 시장 추정 및 예측 : 연령층별(2021-2034년)

- 주요 동향

- 6-12개월

- 12-24개월

- 24-36개월

- 36개월 이상

제7장 시장 추정 및 예측 : 포장 형태별(2021-2034년)

- 주요 동향

- 병

- 파우치

- 판지

- 기타

제8장 시장 추정 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 슈퍼마켓 및 대형 슈퍼마켓

- 전문점

- 편의점

- 온라인 소매

- 약국과 약국

- 기타

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Nestle SA(Gerber Products Company)

- The Kraft Heinz Company

- Danone SA

- Beech-Nut Nutrition Company

- Hain Celestial Group

- Campbell Soup Company(Plum Organics)

- Nurture Inc.(Happy Family Organics)

- Sprout Foods, Inc.

- Ella's Kitchen

- Once Upon a Farm

- Apple & Eve, LLC

- Welch Foods Inc.

- Bellamy's Organic

- Organix Brands Ltd.

- The Coca-Cola Company

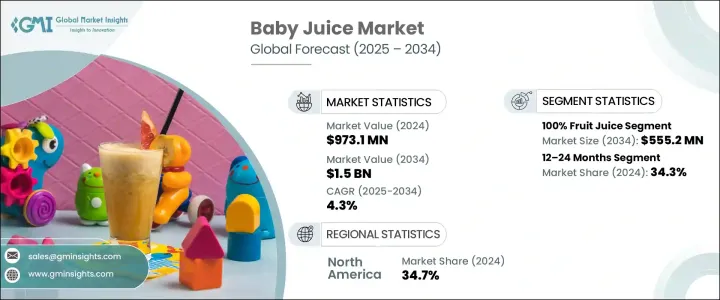

The Global Baby Juice Market was valued at USD 973.1 million in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 1.5 billion by 2034. This steady growth reflects rising parental awareness about early childhood nutrition. Parents are increasingly focused on providing well-rounded, nutrient-rich diets for their infants and toddlers, and baby juices-often enriched with essential vitamins and minerals-are becoming a favored option. As health consciousness grows globally, demand for convenient, fortified products is increasing. Additionally, lifestyle changes, including a growing population of working mothers and dual-income households, have boosted reliance on ready-to-consume baby foods and beverages. These juices offer a quick and practical solution for parents with busy schedules, especially those frequently on the go.

Growth in emerging markets across regions such as Latin America, Asia-Pacific, and Africa is also playing a key role. Rising birth rates, higher disposable incomes, and improved retail infrastructure-including stronger e-commerce channels-are supporting the spread of baby nutrition products. As middle-class populations continue to expand, accessibility to packaged baby juices is becoming easier, pushing forward market penetration in underserved regions and cementing the global reach of the category.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $973.1 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 4.3% |

The 100% fruit juice segment is forecast to reach USD 555.2 million by 2034, growing at a CAGR of 4.5% during 2034. Health-conscious buying behaviors are becoming more mainstream, and concerns around excess sugar in children's diets have driven consumers toward natural alternatives. Parents are gravitating toward juices with no added sugar and a focus on real fruit content. Ongoing promotions and awareness campaigns that position these juices as energizing and naturally vibrant are resonating with today's nutrition-minded caregivers. These preferences align with the shift away from indulgent feeding practices and a move toward healthier options that support balanced childhood development.

In terms of age demographics, the 12-24 months segment held 34.3% share in 2024 and is expected to grow at a CAGR of 6.8% through 2034. This stage marks a critical shift in dietary habits as children begin to transition from breast milk or formula to a broader range of solid and semi-solid foods, including juices. Parents in this segment are particularly selective, seeking products that not only taste good but also support immunity, digestion, and overall development. Baby juices tailored to this age group typically contain vitamin C, iron, and other important nutrients, with a strong focus on natural ingredients. Packaging also plays a major role-non-spill, ergonomic bottles are designed for toddlers learning to drink independently, helping boost appeal for both parents and young children.

North America Baby Juice Market held 34.7% share in 2024. The region's leadership is backed by advanced distribution systems, higher disposable incomes, and a shift toward clean-label, fortified, and organic options. Parents in both the U.S. and Canada are increasingly driven by informed purchasing decisions that prioritize early-life nutrition. Regulations around product labeling and safety are particularly stringent, which builds trust in the products available on the shelves. Government oversight and nutrition-focused labeling contribute to a robust and transparent baby juice ecosystem, ensuring consistency in quality and consumer safety.

Key players active in the Global Baby Juice Market include Beech-Nut Nutrition Company, The Kraft Heinz Company, Sprout Foods, Inc., Campbell Soup Company, and Nestle S.A. Leading brands are strengthening their market position by diversifying product portfolios with organic, non-GMO, and allergen-free offerings. Many have expanded into functional beverages fortified with vitamins, minerals, and probiotics to appeal to nutrition-savvy parents. Strategic investments in attractive, convenient packaging-such as resealable, spill-proof containers-are enhancing usability for parents and toddlers alike. Brands are also leveraging digital marketing and social media platforms to connect with millennial and Gen Z parents, while broadening distribution via e-commerce to boost accessibility. Collaborations with pediatric nutritionists and compliance with safety certifications further elevate brand credibility and trust among health-conscious consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Age group

- 2.2.3 Packaging type

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for convenient baby food options

- 3.2.1.2 Rising disposable income in developing economies

- 3.2.1.3 Increasing working women population

- 3.2.1.4 Product innovations and fortification

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Pediatric recommendations against early juice consumption

- 3.2.2.2 Health concerns related to sugar content

- 3.2.2.3 Preference for whole fruits and homemade options

- 3.2.2.4 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Development of organic and natural variants

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 E-commerce growth

- 3.2.3.4 Functional and fortified baby juice products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global regulations for baby food and beverages

- 3.4.2 FDA regulations and guidelines

- 3.4.3 European Union regulatory framework

- 3.4.4 Juice HACCP requirements

- 3.4.5 Labeling and health claim regulations

- 3.4.6 Impact of regulations on market growth

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.1.1 Juice processing technologies

- 3.6.1.2 Preservation methods

- 3.6.1.3 Packaging innovations

- 3.6.1.4 Quality testing advancements

- 3.6.1.5 Digital technologies in supply chain

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.6.1 Technology and Innovation landscape

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Consumer Behavior Analysis

- 3.13.1 Parental preferences and decision factors

- 3.13.2 Purchase patterns

- 3.13.3 Influence of pediatric recommendations

- 3.13.4 Health and nutrition awareness

- 3.13.5 Brand loyalty and switching behavior

- 3.14 Pediatric nutrition trends

- 3.14.1 Evolving guidelines for infant nutrition

- 3.14.2 Age-appropriate beverage recommendations

- 3.14.3 Sugar intake concerns in early childhood

- 3.14.4 Role of juices in child development

- 3.14.5 Alternative beverage options for infants and toddlers

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Liters)

- 5.1 Key trends

- 5.2 100% fruit juice

- 5.3 Fruit juice blends

- 5.4 Vegetable juice

- 5.5 Organic baby juice

- 5.6 Fortified baby juice

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Age Group, 2021-2034 (USD Million) (Kilo Liters)

- 6.1 Key trends

- 6.2 6–12 months

- 6.3 12–24 months

- 6.4 24–36 months

- 6.5 Above 36 months

Chapter 7 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Million) (Kilo Liters)

- 7.1 Key trends

- 7.2 Bottles

- 7.3 Pouches

- 7.4 Cartons

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Kilo Liters)

- 8.1 Key trends

- 8.2 Supermarkets and hypermarkets

- 8.3 Specialty stores

- 8.4 Convenience stores

- 8.5 Online retail

- 8.6 Pharmacies and drug stores

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Liters)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Nestle S.A. (Gerber Products Company)

- 10.2 The Kraft Heinz Company

- 10.3 Danone S.A.

- 10.4 Beech-Nut Nutrition Company

- 10.5 Hain Celestial Group

- 10.6 Campbell Soup Company (Plum Organics)

- 10.7 Nurture Inc. (Happy Family Organics)

- 10.8 Sprout Foods, Inc.

- 10.9 Ella’s Kitchen

- 10.10 Once Upon a Farm

- 10.11 Apple & Eve, LLC

- 10.12 Welch Foods Inc.

- 10.13 Bellamy's Organic

- 10.14 Organix Brands Ltd.

- 10.15 The Coca-Cola Company