|

시장보고서

상품코드

1797749

배터리 바인더 재료 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Battery Binder Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

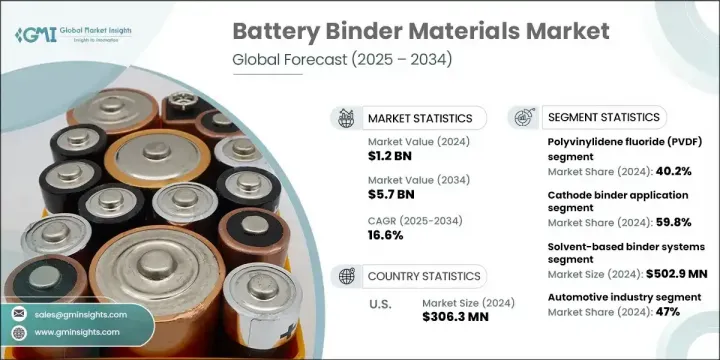

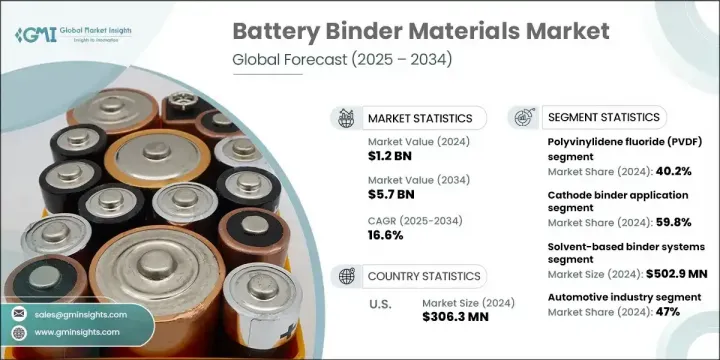

세계의 배터리 바인더 재료 시장은 2024년에 12억 달러로 평가되었으며 CAGR 16.6%를 나타내 2034년에는 57억 달러에 이를 것으로 추정됩니다.

이러한 증가 동향은 전기자동차, 모바일 일렉트로닉스, 신재생에너지 저장 시스템 등 다양한 고성장 부문에서 리튬 이온 배터리 수요 증가로 인한 영향이 큽니다. 배터리 바인더는 활성 입자를 전극 집전체에 고정하는 데 사용되는 특수 폴리머로, 고효율, 고용량, 수명이 긴 배터리를 설계하는 데 점점 더 중요해지고 있습니다. 구조적인 "접착제" 역할은 응집 결합과 내구성을 보장하고 배터리의 기계적 무결성과 사이클 성능에 직접 영향을 미칩니다.

웨어러블 및 스마트폰과 같은 최신 소비자 장비를 위한 에너지 밀도가 높은 컴팩트한 배터리 설계의 확대는 바인더 재료의 배합에서 혁신을 가속화하고 있습니다. 재생에너지 인프라에 대규모 배터리 저장 시스템이 통합되어 긴 수명의 열 안정성 바인더의 필요성이 급격히 증가하고 있습니다. 제조업체는 전극의 응집력을 높이고 기계적 강도를 높이고 유연성을 향상시키는 차세대 아크릴계 바인더의 제조에 주력하고 있습니다. 경량 부품과 환경적 적합성을 중시하는 개발 증가가 제품 개발의 조타를 계속하고 있으며, 지속 가능한 재료의 채용이 진행됨에 따라 첨단 제조 부문에서 수요가 더욱 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 12억 달러 |

| 예측 금액 | 57억 달러 |

| CAGR | 16.6% |

음극 바인더 부문은 2024년에 59.8%의 점유율을 차지했고, 2034년의 CAGR은 16.5%를 나타낼 것으로 예측됩니다. 이러한 바인더는 엄격한 충방전 사이클 하에서 음극의 내구성과 성능을 유지하는 데 필수적입니다. 그 중에서도 PVDF(폴리불화비닐리덴)는 견고한 내약품성과 내열성, 신뢰성이 높은 접착성, 폭넓은 음극 재료와의 적합성으로 알려져 있습니다. 음극 바인더는 활물질이 집전체 표면에 효과적으로 연결된 상태를 유지하고 배터리의 안정성과 출력 효율에 기여하는데 중요한 역할을 합니다.

2024년 용제계 바인더 시스템 부문 시장 규모는 5억 290만 달러로 평가되었고, 2034년의 CAGR은 16.8%를 나타낼 것으로 예측되고 있습니다. 역사적으로 NMP를 사용한 PVDF 기반 용매 바인더는 우수한 접착성, 화학적 내성 및 성능을 제공할 수 있기 때문에 배터리 제조에 선호되고 사용되어 왔습니다. 그러나 이러한 재료는 현재 유럽이나 북미 등 주요 지역에서 환경 안전 규제가 강화되어 규제 강화에 직면하고 있습니다. 솔벤트 시스템이 여전히 주류이면서 수성 및 친환경 바인더 기술로의 전환이 상황을 바꾸고 있으며, 제조업체는 성능을 희생하지 않고보다 깨끗하고 컴플라이언스에 적합한 대체품으로 전환하고 있습니다.

2024년 미국의 배터리 바인더 재료 시장 규모는 3억 630만 달러로 평가되었고, 2034년 CAGR은 13.7%를 나타낼 것으로 전망됩니다. 미국은 견조한 전기자동차의 전개, 에너지저장에 대한 엄청난 투자, 뿌리 깊은 제조 에코시스템에 힘입어 배터리 바인더 기술 혁신의 중심거점으로 번영을 계속하고 있습니다. 국내 배터리 공급망에 대한 연방 정부의 광범위한 지원은 첨단 접착제 생산에 대한 재정적인센티브와 함께 급속히 발전하는 시장에서 미국 골격을 강화하고 있습니다. 또한 전략적 자본주입으로 SBR, PVDF 등 차세대 바인더 재료의 생산능력도 향상하고 있으며 지역개발을 더욱 촉진하고 있습니다.

세계의 배터리 바인더 재료 시장을 선도하는 주요 기업으로는 Zeon Corporation, Solvay SA, Chemours Company, Sinochem Lantian, Dongyue Group, Arkema SA, Kureha Corporation, Shanghai 3F New Materials, JSR Corporation, Shandong Huaxia Shenzhou New Material 등이 있습니다. 이러한 기업들은 세계의 지속가능성 목표를 충족하는 친환경 고성능 바인더 배합을 개발하기 위해 연구개발에 많은 투자를 하고 있습니다. 배터리 셀 제조업체와 OEM과의 제휴로 차세대 배터리 시스템에 신재료를 신속하게 통합할 수 있습니다. 각 회사는 또한 생산 능력을 확대하고 합작 투자에 진입하여 지역 도달범위를 강화하고 있습니다. 규제 상황의 변화에 대응하기 위해, 시장 상황을 선도하는 각사는 제조시의 확대성과 에너지 효율에 중점을 두면서 기존 용제계 시스템에서 수성 대체 시스템으로의 이행을 진행하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 전기자동차 시장 확대

- 에너지 저장 시스템 도입

- 소비자용 전자기기 제품 수요 증가

- 배터리 성능 향상 요건

- 산업의 잠재적 리스크 및 과제

- 높은 재료비와 가격 변동

- 환경과 안전 규제

- 기술적 성능 제한

- 공급망의 집중 위험

- 시장 기회

- 차세대 배터리 기술

- 지속 가능한 바이오 바인더 개발

- 실리콘 양극 기술의 채용

- 신흥 시장에의 침투

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)

- (참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속 가능한 사례

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 활동

- 탄소발자국의 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정·예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 폴리비닐리덴 플루오라이드(PVDF)

- 카르복시메틸 셀룰로오스(CMC)

- 스티렌-부타디엔 고무(SBR)

- 폴리아크릴산(PAA)

- 기타 특수 바인더

제6장 시장 추정·예측 : 용도별(2021-2034년)

- 주요 동향

- 음극 바인더의 용도

- NCM 음극 시스템

- NCA 음극 시스템

- LFP 음극 시스템

- 고전압 음극 재료

- 양극 바인더의 용도

- 흑연 양극 시스템

- 실리콘 기반 음극 시스템

- 리튬 티타네이트 산화물(LTO) 시스템

- 차세대 음극 재료

제7장 시장 추정·예측 : 기술별(2021-2034년)

- 주요 동향

- 용제계 바인더 시스템

- 기존 PVDF 시스템

- 수성 바인더 시스템

- CMC/SBR 조합

- 하이브리드 바인더 시스템

- 다중 성분 배합

- 차세대 기술

- 고체 배터리 바인더

- 전도성 바인더 네트워크

- 자기 복구 재료

제8장 시장 추정·예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 자동차 산업

- 전기승용차

- 전기상용차

- 하이브리드 전기자동차

- 소비자용 전자 기기

- 스마트폰 및 태블릿

- 노트북 및 휴대용 장치

- 웨어러블 전자 기기

- 게임 및 엔터테인먼트 장비

- 에너지 저장 시스템

- 그리드 스케일의 에너지 저장

- 주택 에너지 저장

- 상업 및 산업용 저장

- 신재생에너지 통합

- 산업용도

- 자재관리 기기

- 백업 전원 시스템

- 통신 인프라

- 의료 및 헬스케어 기기

제9장 시장 추정·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Arkema SA

- Chemours Company

- Dongyue Group

- JSR Corporation

- Kureha Corporation

- Shandong Huaxia Shenzhou New Material

- Shanghai 3F New Materials

- Sinochem Lantian

- Solvay SA

- Zeon Corporation

The Global Battery Binder Materials Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 16.6% to reach USD 5.7 billion by 2034. This upward trend is largely influenced by the escalating demand for lithium-ion batteries across a variety of high-growth sectors such as electric vehicles, mobile electronics, and renewable energy storage systems. Battery binders-specialized polymers used to secure active particles to electrode current collectors-are becoming increasingly vital in designing batteries with greater efficiency, higher capacity, and extended lifespans. Their role as structural "adhesives" ensures cohesive binding and durability, directly impacting the battery's mechanical integrity and cycle performance.

The expansion of energy-dense, compact battery designs for modern consumer devices like wearables and smartphones is accelerating innovation in binder material formulations. With the integration of large-scale battery storage systems into renewable energy infrastructure, the need for long-lasting and thermally stable binders has grown sharply. Manufacturers are focusing on producing next-generation acrylic-based binders to boost electrode cohesion, enhance mechanical strength, and improve flexibility. Rising emphasis on lightweight components and environmental compatibility continues to steer product development, while growing adoption of sustainable materials further elevates demand in advanced manufacturing sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 16.6% |

The cathode binders segment held 59.8% share in 2024, with projected growth at a CAGR of 16.5% through 2034. These binders are essential in maintaining cathode durability and performance under rigorous charge-discharge cycles. Among the most used materials is PVDF (polyvinylidene fluoride), known for its robust chemical and thermal resistance, reliable adhesion, and compatibility with a wide range of cathode materials. Cathode binders play a critical role in ensuring that the active materials remain effectively connected to the collector surface, thereby contributing to battery stability and output efficiency.

In 2024, the solvent-based binder systems segment was valued at USD 502.9 million and is projected to grow at a CAGR of 16.8% through 2034. Historically, PVDF-based solvent binders using NMP were favored in battery manufacturing due to their ability to offer superior adhesion, chemical resilience, and performance. However, these materials are now facing tighter restrictions due to increasing environmental and safety regulations in key regions like Europe and North America. While solvent-based systems still dominate, the shift toward water-based and more eco-friendly binder technologies is reshaping the landscape, pushing manufacturers toward cleaner and more compliant alternatives without compromising performance.

United States Battery Binder Materials Market generated USD 306.3 million in 2024, with expected growth at a CAGR of 13.7% through 2034. The nation continues to thrive as a central hub for battery binder innovation, propelled by its robust electric vehicle rollout, significant investments in energy storage, and deep-rooted manufacturing ecosystem. Extensive federal support for domestic battery supply chains, combined with financial incentives for advanced adhesive production, has strengthened the U.S. foothold in this fast-evolving market. Strategic capital infusion is also advancing production capabilities for next-gen binder materials like SBR and PVDF, further driving local development.

Key companies leading the Global Battery Binder Materials Market include Zeon Corporation, Solvay S.A., Chemours Company, Sinochem Lantian, Dongyue Group, Arkema S.A., Kureha Corporation, Shanghai 3F New Materials, JSR Corporation, and Shandong Huaxia Shenzhou New Material. They are investing significantly in R&D to develop environmentally friendly and high-performance binder formulations that meet global sustainability goals. Collaborations with battery cell manufacturers and OEMs are enabling faster integration of new materials into next-generation battery systems. Companies are also expanding production capacity and entering joint ventures to strengthen their regional reach. To comply with shifting regulatory landscapes, market leaders are transitioning from traditional solvent-based systems to water-based alternatives while focusing on scalability and energy efficiency during manufacturing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Technology

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electric vehicle market expansion

- 3.2.1.2 Energy storage system deployment

- 3.2.1.3 Consumer electronics demand growth

- 3.2.1.4 Battery performance enhancement requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High material costs and price volatility

- 3.2.2.2 Environmental and safety regulations

- 3.2.2.3 Technical performance limitations

- 3.2.2.4 Supply chain concentration risks

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation battery technologies

- 3.2.3.2 Sustainable and bio-based binder development

- 3.2.3.3 Silicon anode technology adoption

- 3.2.3.4 Emerging market penetration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyvinylidene Fluoride (PVDF)

- 5.3 Carboxymethyl Cellulose (CMC)

- 5.4 Styrene-Butadiene Rubber (SBR)

- 5.5 Polyacrylic Acid (PAA)

- 5.6 Other Specialty Binders

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cathode binder applications

- 6.2.1 NCM cathode systems

- 6.2.2 NCA cathode systems

- 6.2.3 LFP cathode systems

- 6.2.4 High-voltage Cathode Materials

- 6.3 Anode binder applications

- 6.3.1 Graphite anode systems

- 6.3.2 Silicon-based anode systems

- 6.3.3 Lithium titanate oxide (LTO) systems

- 6.3.4 Next-generation anode materials

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Solvent-based binder systems

- 7.2.1 Traditional PVDF systems

- 7.3 Water-based binder systems

- 7.3.1 CMC/SBR combinations

- 7.4 Hybrid binder systems

- 7.4.1 Multi-component formulations

- 7.5 Next-generation technologies

- 7.5.1 Solid-state battery binders

- 7.5.2 Conductive binder networks

- 7.5.3 Self-healing materials

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive industry

- 8.2.1 Electric passenger vehicles

- 8.2.2 Electric commercial vehicles

- 8.2.3 Hybrid electric vehicles

- 8.3 Consumer electronics

- 8.3.1 Smartphones and tablets

- 8.3.2 Laptops and portable devices

- 8.3.3 Wearable electronics

- 8.3.4 Gaming and entertainment devices

- 8.4 Energy storage systems

- 8.4.1 Grid-scale energy storage

- 8.4.2 Residential energy storage

- 8.4.3 Commercial and industrial storage

- 8.4.4 Renewable energy integration

- 8.5 Industrial applications

- 8.5.1 Material handling equipment

- 8.5.2 Backup power systems

- 8.5.3 Telecommunications infrastructure

- 8.5.4 Medical and healthcare devices

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arkema S.A.

- 10.2 Chemours Company

- 10.3 Dongyue Group

- 10.4 JSR Corporation

- 10.5 Kureha Corporation

- 10.6 Shandong Huaxia Shenzhou New Material

- 10.7 Shanghai 3F New Materials

- 10.8 Sinochem Lantian

- 10.9 Solvay S.A.

- 10.10 Zeon Corporation