|

시장보고서

상품코드

1822614

건축용 단열재 시장 : 기회, 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Building Thermal Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

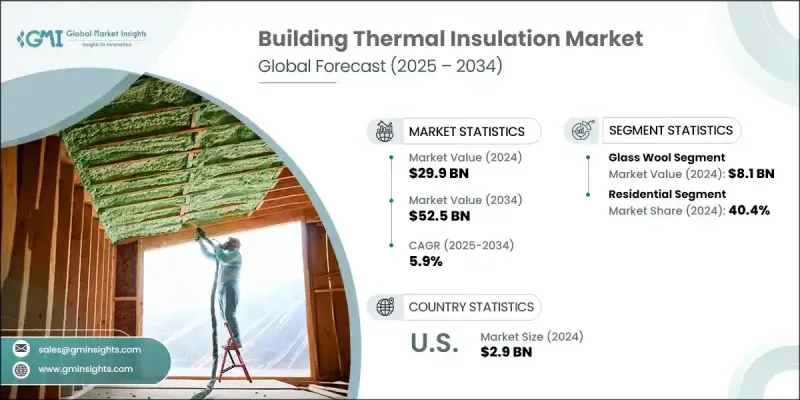

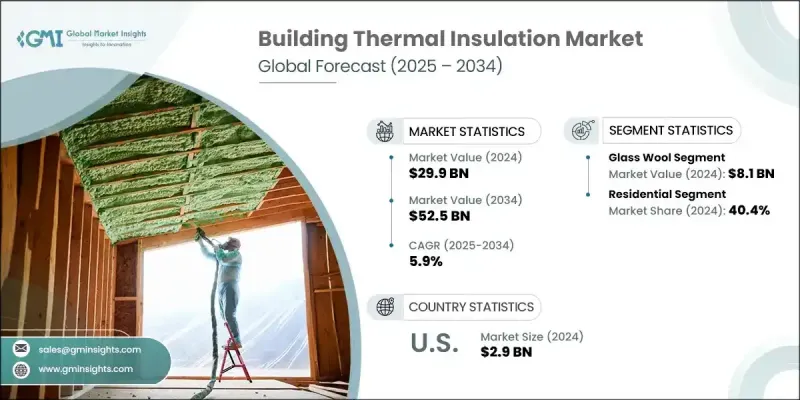

세계의 건축용 단열재 시장 규모는 2024년에 299억 달러로 평가되었고, CAGR은 5.9%를 나타낼 것으로 예측되며 2034년에 525억 달러에 이를 전망입니다. 환경 의식 고조와 기후 변화에 대한 우려가 건설 분야에서 에너지 효율적 솔루션 수요를 촉진하고 있습니다. 건물은 상당한 에너지 소비를 차지하며, 단열은 난방 및 냉방 수요를 줄여 온실가스 배출을 효과적으로 감소시킵니다. 이는 글로벌 지속가능성 이니셔티브와 부합하며 친환경 단열재 채택을 촉진합니다.

소비자, 개발사, 시공사들은 점점 더 지속가능하고 에너지 효율적인 옵션을 선호하여 천연 또는 재활용 소재로 제작된 제품에 대한 수요를 촉진하고 있습니다. LEED 및 BREEAM과 같은 규제 프레임워크와 그린빌딩 인증은 에너지 효율적인 단열재를 더욱 장려하는 한편, 세금 환급과 같은 재정적 인센티브는 채택을 촉진합니다. 결과적으로 에너지 효율적인 주거 및 상업 시설에 대한 투자가 지속적으로 증가하며, 단열재는 에너지 비용 절감과 환경 영향 최소화를 위한 핵심 요소로 자리매김하고 있습니다. 시장 성장은 보다 지속 가능한 구조물 건설에 대한 공동의 관심을 반영합니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 299억 달러 |

| 예측 금액 | 525억 달러 |

| CAGR | 5.9% |

시장은 재료별로 개방형 셀과 폐쇄형 셀 유형으로 구분됩니다. 개방형 셀 재료는 상당한 주목을 받아 2024년 129억 6,000만 달러를 기록했으며, 2034년까지 238억 4,000만 달러에 달할 것으로 예상됩니다. 이 소재들은 비용 효율성이 뛰어나 주거용 및 상업용 응용 분야, 특히 예산이 제한된 프로젝트에서 널리 채택되고 있습니다. 또한 방음 성능을 향상시키고 재활용 소재로 제작된 친환경 옵션으로 녹색 건축을 지원합니다. 개방형 셀 소재는 설치 용이성과 우수한 열 성능으로 선호되며, 에너지 효율 개선을 위한 기존 건물 개조 시 선호되는 선택지입니다.

유통 채널별로는 시장이 직접 판매와 간접 판매로 구분됩니다. 간접 채널은 2024년 45.01%의 점유율로 시장을 주도했으며, 2034년까지 196억 9,000만 달러에 달할 것으로 예상됩니다. 제조업체는 유통업체, 도매업체, 소매업체의 광범위한 네트워크를 통해 제품 공급과 고객 접근성을 효율화하는 혜택을 누립니다. 이러한 중간 유통망은 물류 문제를 줄이고 시장 침투력을 높여 제조사가 제품 개발과 브랜딩에 집중할 수 있도록 지원합니다. 간접 유통 채널은 온라인 플랫폼을 통해 증가하는 수요에도 대응하며 구매자의 접근성과 편의성을 향상시킵니다.

2024년 미국은 글로벌 시장 매출의 53.5%로 평가되었고, 2034년까지 연평균 성장률(CAGR) 6.3%로 성장할 전망입니다. 미국의 다양한 건설 산업과 엄격한 에너지 효율 규제는 첨단 단열 솔루션 수요를 촉진합니다. 세액 공제 및 친환경 인증을 포함한 정부 정책은 단열재 사용을 추가로 지원합니다. 단열 기술 혁신에 대한 국가적 강조와 다양한 기후대에서의 에너지 절약 솔루션 필요성은 시장 성장을 지속적으로 견인하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 에너지 효율 규제 강화

- 건설과 도시화의 진전

- 환경 문제와 지속가능성에 대한 노력

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자 비용

- 대체 기술의 가용성

- 기회

- 친환경 재활용 소재 개발

- 개조 및 리모델링 시장 성장

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신 상황

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 소재별

- 규제 상황

- 표준 및 규제 준수 요건

- 지역 규제 프레임워크

- 인증 기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 글라스울

- 석면

- 발포 폴리스티렌

- 압출 폴리스티렌

- 폴리우레탄

- 기타

제6장 시장 추계 및 예측 : 형태별(2021-2034년)

- 주요 동향

- 담요

- 패널

- 폼

- 기타

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 벽 단열

- 내벽

- 외벽

- 공동벽

- 커튼월

- 지붕 단열재

- 평지붕

- 경사 지붕

- 바닥/슬래브

- 기타

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 주거용

- 상업용

- 산업용

제9장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접

- 간접

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Armacell

- Burnett &Co

- Firestone Building Products

- GLT Products

- Johns Manville

- Kingspan Group

- Knauf Insulation

- Mapei

- NICHIAS Corporation

- Owens Corning

- Recticel Insulation

- Rockwool International

- Saint-Gobain Isover

- Siltherm

- URSA

The global building thermal insulation market was valued at USD 29.9 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 52.5 billion by 2034. Growing environmental awareness and concerns about climate change are driving the demand for energy-efficient solutions in construction. Buildings account for substantial energy consumption, and insulation reduces the need for heating and cooling, effectively lowering greenhouse gas emissions. This aligns with global sustainability initiatives and fuels the adoption of eco-friendly insulation materials.

Consumers, developers, and contractors increasingly prefer sustainable and energy-efficient options, spurring demand for products made from natural or recycled materials. Regulatory frameworks and green building certifications, such as LEED and BREEAM, further promote energy-efficient insulation, while financial incentives like tax rebates encourage adoption. As a result, investment in energy-efficient homes and commercial structures continues to rise, making insulation a critical component in reducing energy costs and minimizing environmental impact. The market's growth reflects a collective focus on building more sustainable structures.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.9 Billion |

| Forecast Value | $52.5 Billion |

| CAGR | 5.9% |

The market is segmented by material into open-cell and closed-cell types. Open-cell materials have gained substantial traction, contributing USD 12.96 billion in 2024 and projected to reach USD 23.84 billion by 2034. These materials are cost-effective and widely adopted in residential and commercial applications, especially in budget-conscious projects. They also enhance soundproofing and support green construction with eco-friendly options made from recycled materials. Open-cell materials are favored for their ease of installation and strong thermal performance, making them a preferred choice for retrofitting older buildings to improve energy efficiency.

By distribution channel, the market is divided into direct and indirect sales. Indirect channels led the market with a 45.01% share in 2024 and are expected to reach USD 19.69 billion by 2034. Manufacturers benefit from the extensive networks of distributors, wholesalers, and retailers, who streamline product availability and customer reach. These intermediaries reduce logistical challenges and improve market penetration, helping manufacturers focus on product development and branding. Indirect channels also cater to the growing demand through online platforms, enhancing accessibility and convenience for buyers.

The United States accounted for 53.5% of the global market's revenue in 2024 and is projected to grow at a CAGR of 6.3% through 2034. The nation's diverse construction industry and stringent energy-efficiency regulations drive demand for advanced insulation solutions. Government initiatives, including tax credits and green certifications, further support the use of thermal insulation. The country's emphasis on innovation in insulation technologies and the need for energy-saving solutions across varying climate zones continue to bolster market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising energy efficiency regulations

- 3.2.1.2 Growing construction and urbanization

- 3.2.1.3 Environmental concerns and sustainability initiatives

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Availability of alternative technologies

- 3.2.3 Opportunities

- 3.2.3.1 Development of eco-friendly and recycled materials

- 3.2.3.2 Retrofitting and renovation market growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By material

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Billion) (Thousand Square Meters)

- 5.1 Key trends

- 5.2 Glass wool

- 5.3 Stone wool

- 5.4 Expanded polystyrene

- 5.5 Extruded polystyrene

- 5.6 Polyurethanes

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Billion) (Thousand Square Meters)

- 6.1 Key trends

- 6.2 Blankets

- 6.3 Panels

- 6.4 Foam

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Square Meters)

- 7.1 Key trends

- 7.2 Wall insulation

- 7.2.1 Internal wall

- 7.2.2 External wall

- 7.2.3 Cavity wall

- 7.2.4 Curtain wall

- 7.3 Roof insulation

- 7.3.1 Flat roof

- 7.3.2 Pitch roof

- 7.4 Floor/Slab

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Thousand Square Meters)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Square Meters)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Square Meters)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Armacell

- 11.2 Burnett & Co

- 11.3 Firestone Building Products

- 11.4 GLT Products

- 11.5 Johns Manville

- 11.6 Kingspan Group

- 11.7 Knauf Insulation

- 11.8 Mapei

- 11.9 NICHIAS Corporation

- 11.10 Owens Corning

- 11.11 Recticel Insulation

- 11.12 Rockwool International

- 11.13 Saint-Gobain Isover

- 11.14 Siltherm

- 11.15 URSA