|

시장보고서

상품코드

1934732

건축용 단열재 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Building Insulation Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

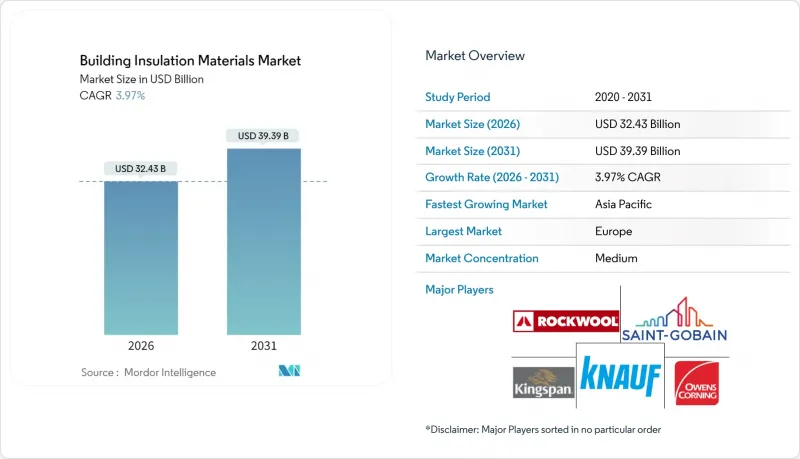

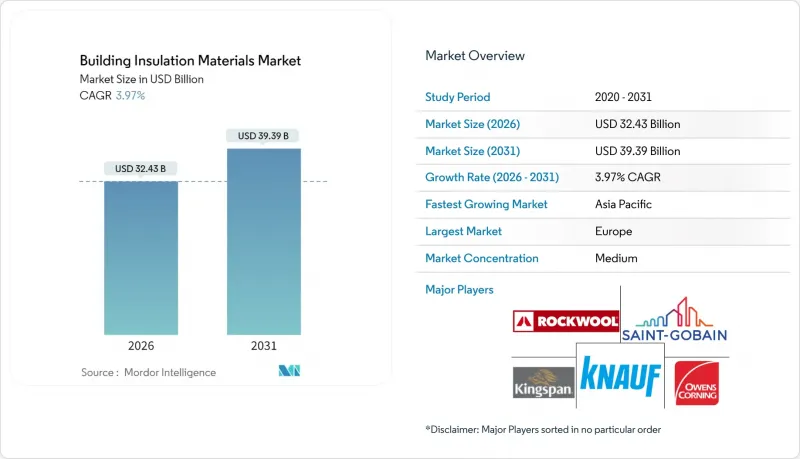

건축용 단열재 시장은 2025년 311억 9,000만 달러에서 2026년에는 324억 3,000만 달러로 성장하며, 2026-2031년에 CAGR 3.97%로 추이하며, 2031년까지 393억 9,000만 달러에 달할 것으로 예측되고 있습니다.

유럽과 북미의 규제 강화, 아시아태평양의 급속한 도시화, 주택 소유자들의 에너지 절약에 대한 인식이 높아짐에 따라 첨단 단열 및 방음 솔루션의 잠재 시장이 확대되고 있습니다. 각 제조업체들은 더 높은 단열성능(R값)을 얇은 프로파일로 실현하고, 제조과정에서의 탄소배출량을 줄이고, 우수한 내화성능을 갖춘 제품군을 개발하기 위해 경쟁하면서 소재 기술 혁신이 가속화되고 있습니다. 경쟁 전략은 지역적 범위와 제품 범위를 확대하는 인수를 중심으로 전개되고 있으며, 오웬스코닝이 39억 달러에 인수한 메이슨나이트 인터내셔널(Masonite International)의 인수가 그 좋은 예입니다. 이번 인수로 보완적인 건축 외장재 제품을 추가하는 동시에 1억 2,500만 달러의 비용 시너지를 기대할 수 있게 되었습니다.

세계 건축 단열재 시장 동향 및 인사이트

에너지 절약형 건축물에 대한 수요 증가

2024년 국제 에너지 절약 기준(IECC) 등 새로운 건축 기준에서는 미국 기후대 2-3에서는 다락방 단열재에 R49, 기후대 4-8에서는 R60을 요구하고 있으며, 단열 성능 기준이 강화됨에 따라 설계자는 더 높은 성능의 제품을 선택해야 하는 상황입니다. 대서양을 사이에 두고 유럽에서는 개정된 '건축물 에너지 성능 지침'에 따라 2030년까지 에너지 사용량을 16% 감축하는 법적 구속력 있는 목표가 설정되어 유럽 주택 재고의 리노베이션에 대한 추진력이 더욱 강화되고 있습니다. 상업시설 소유주들이 ANSI/ASHRAE/IES 90.1-2022 기준(2019년 대비 9.8%의 현장 에너지 절감 효과) 달성을 목표로 하는 가운데, 임대 가능 면적을 확보하기 위해 더 얇은 구조로 동등한 단열 성능(R값)을 구현하는 자재에 대한 수요가 증가하고 있습니다. 제조업체는 저열전도성 코어와 반사성 표면재를 결합한 하이브리드 솔루션을 제공하여 1mm당 단열 성능을 극대화하고 있습니다.

북미 그린 리노베이션 인센티브 확대

미국의 '에너지 효율 주택 개보수 세액공제'는 대상 단열재 비용의 최대 30%를 환급해줌으로써 주택 소유자의 투자 회수 기간을 실질적으로 단축시킵니다. 저소득층 주택에 대한 보완적 기준은 연간 가계 지출을 크게 줄이고 저소득층에 대한 채용을 촉진하고 있습니다. 이 프로그램들은 정해진 바닥 면적 기준을 초과하는 건물에 대한 에너지 개보수를 의무화하는 지방 자치 단체의 기후 계획과 연계되어 향후 10년간 자재 수요를 지원하는 프로젝트 파이프라인을 형성하고 있습니다. 블로우 및 스프레이 폼 단열 시스템을 개보수 공극에 최적화한 제조업체들은 이 증가분을 흡수할 준비가 되어 있습니다.

고가의 자재 및 시공비

가격에 민감한 많은 시장에서 에어로젤 블랭킷과 같은 첨단 시스템은 우수한 단열 성능에도 불구하고 특수한 취급이 필요하므로 총 설치 비용이 높아져 여전히 너무 비싸다고 인식되고 있습니다. 대규모 사회주택 프로그램의 재정적 제약은 프리미엄 제품의 추진력을 더욱 둔화시키고, 수명주기 비용 절감 효과가 높은 지출을 정당화하더라도 설계자가 중저가 유리섬유와 폴리스티렌으로 돌아갈 수밖에 없는 상황을 만들어내고 있습니다. 생산 규모 확대에 따른 단가 하락과 인센티브에 따른 가격 차이가 해소되기 전까지는 프리미엄 소재는 성능이 사양을 결정하는 틈새 프로젝트에 국한될 것입니다.

부문 분석

2025년 기준, 유리섬유는 건축용 단열재 시장의 34.62%를 차지할 것으로 예측됩니다. 이는 오랜 기간 구축된 공급망과 경쟁력 있는 가격 설정에 힘입은 바 큽니다. 유리섬유 코어는 신뢰할 수 있는 내열성과 불연성을 제공하며, 모든 기후대에서 표준 소재가 되었습니다. 폴리스티렌은 BASF의 루트비히스하펜 공장의 비드 균일성 및 단열 성능 향상을 위한 설비 증설 등 생산능력 확대에 힘입어 CAGR 4.16%로 가장 빠르게 성장하고 있습니다. 내화성능과 차음성이 최우선인 분야에서는 미네랄울이 지지를 유지하고 있으며, 셀룰로오스계는 지속가능성에 대한 평가와 재생재료를 중시하는 지역 프로그램을 배경으로 성장세를 이어가고 있습니다. PUR(폴리우레탄) 및 PIR(폴리이소시아뉼레이트) 폼은 고단열 성능이 요구되는 고급 용도에 대응하지만, 비용과 가연성에 대한 우려로 인해 시장 점유율 확대가 억제되고 있습니다. 에어로젤은 여전히 틈새 시장이지만, 초임계 건조 사이클을 단축하는 공정 개선을 통한 비용 절감이 실현된다면 시장을 혁신할 수 있는 잠재력을 가지고 있습니다.

비용, 탄소발자국 감축 목표, 강화되는 방화규제가 R값뿐만 아니라 사양 결정에 영향을 미치게 되었습니다. 이러한 변화로 인해 내습성과 구조적 강성 등 서로 다른 특성을 결합한 복합 코어 패널에 대한 수요가 생겨나고 있습니다. 각 제조업체들은 보다 엄격한 실내 공기질 기준에 맞추어 포름알데히드 및 페놀류 배출을 줄이는 바인더 화학 기술에 대한 투자를 진행하고 있습니다. 그 결과, 건축 단열재 시장에는 두 가지 흐름이 병행하고 있습니다. 성숙한 범용 제품은 수량 기준으로 안정화되는 반면, 고성능 제품군은 저변은 작지만 더 빠른 성장세를 보이고 있습니다.

지붕 조립은 2025년 매출의 29.12%를 차지했습니다. 이는 외피 상부를 통과하는 열유속이 집중되므로 에너지 효율화 개보수의 1차 대상이기 때문입니다. 시공이 비교적 용이하고, 태양광발전 지원 지붕에 대한 보조금에 단열 패키지가 포함되는 경우가 많아 수요를 지원하고 있습니다. 건축 단열재 시장에서 방음 칸막이 및 공조 덕트용 제품 시장 규모는 소음 공해가 공중 보건 문제로 인식되면서 2031년까지 연평균 복합 성장률(CAGR) 4.85%로 확대될 것으로 예측됩니다. 벽체 내부 공간 및 외부 단열 마감 시스템도 마찬가지입니다. 리노베이션 프로그램에서는 외관과 단열 성능을 모두 향상시키는 외관 리노베이션이 우선적으로 고려되기 때문입니다. 바닥 및 지하실용 솔루션은 슬래브 단부의 열 손실이 건물 전체의 단열 성능을 저하시키는 추운 지역에서 성장이 예상됩니다.

통합 설계가 확산되고 있습니다. 건축가는 단열, 방음, 방습의 목적을 동시에 달성하는 시스템을 지정하여 상세 설계를 간소화하고 공사 기간을 단축하고 있습니다. 이러한 종합적인 사고방식은 천공 위험이 높은 방습층이 필요 없거나 방음 매트를 내장한 다기능 보드에 대한 수요를 견인하고 있습니다. 그 결과, 제품 메시지에서 단독 단열 성능 값보다 시스템 호환성을 강조하는 경향이 강해졌고, 주요 공급업체들 사이에서 컨설팅형 판매 접근법이 강화되고 있습니다.

지역별 분석

유럽은 2025년 37.88%의 점유율을 유지했습니다. 이는 2030년까지 건축물 배출량 60% 감축, 2050년까지 기존 건축물의 배출량 제로화를 목표로 하는 구속력 있는 기후 변화 대응법이 촉진요인으로 작용하고 있습니다. 지침의 국내 법제화로 인해 외단열 마감 시스템, 미네랄울, 고성능 경질보드에 대한 수요가 가속화되고 있습니다. 생산자들은 지역 생산 능력을 확장하고 있으며, 그 예로 2026년 가동 예정인 영국 쿤호프사의 1억 7,200만 파운드 규모의 암면 공장을 들 수 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 4.88%로 가장 빠르게 성장하는 지역입니다. 중국, 인도, 동남아시아 시장이 현지 규제를 국제 베스트 프랙티스와 일치시키고 있기 때문입니다. 효율적인 가전제품과 친환경 건물에 대한 정부 부양책은 급속한 도시화에 따른 기초적인 인구통계학적 수요를 강화시키고 있습니다. 록울의 타밀 나두 공장과 같은 생산 능력의 증설은 리드 타임을 단축하고 가격 책정을 현지화하여 비용에 민감한 부문에서 채택을 촉진할 것입니다.

북미에서는 연방 세액 공제 및 유틸리티 리베이트에 힘입은 견고한 리노베이션 활동과 안정적인 신규 건설 프로젝트가 맞물려 시장이 활성화되고 있습니다. 시장의 관심은 저 VOC 제품으로 옮겨가고 있으며, 공조 덕트 및 주거 공간의 재료 교체를 촉진하고 있습니다. 기업의 ESG 공시 규정은 환경 투명성을 높이고 있으며, 검증된 환경 제품 선언(EPD)을 통해 저탄소화를 증명할 수 있는 공급업체가 우위를 점할 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

The Building Insulation Materials Market is expected to grow from USD 31.19 billion in 2025 to USD 32.43 billion in 2026 and is forecast to reach USD 39.39 billion by 2031 at 3.97% CAGR over 2026-2031.

Heightened regulatory stringency in Europe and North America, rapid urbanization in Asia-Pacific, and growing homeowner awareness of utility savings are together expanding the addressable base for advanced thermal and acoustic solutions. Material innovation intensifies as manufacturers race to deliver higher R-values in slimmer profiles, lower embodied carbon, and superior fire performance-often within a single product family. Competitive strategies revolve around acquisitions that broaden geographic reach and product scope, illustrated by Owens Corning's USD 3.9 billion purchase of Masonite International that added complementary building envelope products while promising USD 125 million in cost synergies.

Global Building Insulation Materials Market Trends and Insights

Growing demand for energy-efficient buildings

New codes, such as the 2024 International Energy Conservation Code, require R49 attic insulation in US Climate Zones 2-3 and R60 in Zones 4-8, tightening thermal envelope thresholds that push specifiers toward higher-performance products. Across the Atlantic, the revised Energy Performance of Buildings Directive sets a binding 16% reduction in energy use by 2030, reinforcing momentum for upgrades in European housing stock. As commercial owners strive to meet ANSI/ASHRAE/IES 90.1-2022, which yields 9.8% site energy savings versus the 2019 edition, demand is shifting toward materials that deliver equivalent R-values in thinner assemblies to preserve rentable area. Manufacturers are responding with hybrid solutions that pair low-conductivity cores with reflective facers to maximize thermal performance per millimeter.

Increasing green retrofitting incentives in North America

The US Energy Efficient Home Improvement Credit reimburses up to 30% of qualifying insulation expenses, effectively narrowing payback periods for homeowners. Complementary standards for affordable housing are driving significant annual household savings, encouraging adoption among lower-income brackets. These programs coincide with municipal climate plans that mandate energy retrofits for buildings above defined floor-area thresholds, creating a pipeline of projects that sustain material demand through the decade. Manufacturers with blown-in and spray foam systems tailored to retrofit cavities are positioned to capture this incremental volume.

High materials and installation cost

Many price-sensitive markets still perceive advanced systems such as aerogel blankets as cost-prohibitive despite superior thermal resistance, because specialized handling elevates total installed cost. Capital constraints in large-scale social housing programs further dampen momentum for premium products, forcing specifiers to revert to mid-range fiberglass or polystyrene even when lifecycle savings justify higher outlays. Until manufacturing scale lowers unit price or incentives bridge the gap, premium materials will remain confined to niche projects where performance drives specification.

Other drivers and restraints analyzed in the detailed report include:

- Increasing government support for eco-friendly and sustainable materials

- Growing preference for low-VOC bio-based foams

- Availability of affordable alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiberglass held 34.62% of the building insulation materials market in 2025, anchored by long-established supply chains and competitive pricing. Its glass-fiber core delivers reliable thermal resistance and non-combustibility, making it a staple across climate zones. Polystyrene is the fastest climber at 4.16% CAGR thanks to capacity expansions such as BASF's upgrade in Ludwigshafen that improves bead consistency and thermal performance. Mineral wool retains traction where fire rating and sound attenuation are paramount, while cellulose growth rides sustainability credentials and regional programs that value recycled content. PUR and PIR foams address premium applications requiring high R-value per inch, yet their share is checked by cost and flammability perceptions. Aerogels remain niche but could disrupt as costs fall due to process improvements that shorten supercritical drying cycles.

Cost, embodied-carbon targets and tightening fire regulations now shape specification more than R-value alone. This shift is creating space for hybrid panels that laminate different cores to combine strengths such as moisture tolerance and structural rigidity. Manufacturers are investing in binder chemistries that lower formaldehyde and phenol emissions, anticipating stricter indoor-air-quality standards. As a result, the building insulation materials market sees parallel tracks: mature commodities stabilize on volume, while high-performance classes grow faster albeit from a smaller base.

Roof assemblies captured 29.12% of 2025 revenue because heat-flux concentration through the top of the envelope makes them the first target for energy upgrades. Installation is comparatively straightforward, and subsidies for solar-ready roofs often bundle thermal packages, which sustains volume. The building insulation materials market size for acoustic partition and HVAC ducts is forecast to expand at a 4.85% CAGR to 2031 as health authorities recognize noise pollution as a public health issue. Wall cavities and external insulation finish systems follow closely because renovation programs prioritize facade upgrades that boost both aesthetics and thermal performance. Floor and basement solutions grow in colder climates where slab-edge losses weaken overall envelope performance.

Integrated design is gaining ground: architects specify systems that address thermal, acoustic and moisture objectives simultaneously to simplify detailing and shorten construction schedules. This holistic mindset drives demand for multi-functional boards that eliminate puncture-prone vapor barriers or incorporate acoustic mats. Consequently, product messaging increasingly highlights system compatibility rather than stand-alone thermal metrics, reinforcing a consultative selling approach among leading suppliers.

The Building Insulation Materials Market Report is Segmented by Material Type (Fiberglass, Mineral Wool, Cellulose, and More), Application (Roof, Wall, Floor and Basement, and More), End-User (Residential and Non-Residential), Installation (New Construction and Renovation), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe maintained 37.88% share in 2025, driven by binding climate legislation that targets a 60% emission cut in buildings by 2030 and a zero-emission stock by 2050. National transposition of the directive accelerates demand for exterior insulation and finish systems, mineral wool, and high-performance rigid boards. Producers are scaling regional capacity, evidenced by Knauf's GBP 172 million rock mineral wool factory in the United Kingdom that will start operations in 2026.

Asia-Pacific is the fastest-growing region with a 4.88% CAGR to 2031 as China, India, and Southeast Asian markets align local codes with international best practice. Government stimulus for efficient appliances and green buildings reinforces underlying demographic demand from rapid urbanization. Capacity additions such as Rockwool's Tamil Nadu plant shorten lead times and localize pricing, which improves adoption in cost-sensitive segments.

North America combines a steady new-build pipeline with robust retrofit activity catalyzed by federal tax credits and utility rebates. Market interest is shifting to lower-VOC products, spurring material substitution in HVAC ducts and occupied spaces. Corporate ESG disclosure rules are advancing environmental transparency, favoring suppliers that can prove low embodied carbon through verified EPDs.

- Armacell

- Aspen Aerogels Inc.

- Atlas Roofing Corporation

- BASF SE

- Beijing New Building Materials Public Limited Company

- Cellofoam North America Inc.

- Covestro AG

- Dow

- DuPont

- GAF Materials LLC

- Holcim

- Huntsman International LLC

- Johns Manville

- Kingspan Group

- Knauf Group

- Owens Corning

- Recticel NV/SA

- ROCKWOOL A/S

- Saint-Gobain

- Synthos

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Energy Efficient Buildings

- 4.2.2 Increasing Green Retrofitting Incentives in North America

- 4.2.3 Increasing Governemnt Support for the Usage of Eco-Friendly and Sustainable Materials

- 4.2.4 Growing Preference for Low-VOC Bio-based Foams

- 4.2.5 Rising Infrastructure and Industrialization in Asia-Pacific

- 4.3 Market Restraints

- 4.3.1 High Materials and Installation Cost

- 4.3.2 Availability of Affordable Alternatives

- 4.3.3 Regulatory Scrutiny on Global Warming Potential of Blowing Agents

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Fiberglass

- 5.1.2 Mineral Wool

- 5.1.3 Cellulose

- 5.1.4 Polyurethane/Polyisocyanurate Foams (PUR/PIR)

- 5.1.5 Polystyrene

- 5.1.6 Other Materials (Cork, Aerogel and Vacuum Insulation Panels, Spray Foams, Hemp, Calcium-Silicate, etc.)

- 5.2 By Application

- 5.2.1 Roof

- 5.2.2 Wall (External and Cavity)

- 5.2.3 Floor and Basement

- 5.2.4 Ceiling and Attic

- 5.2.5 Acoustic Partition and HVAC Duct

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Non-Residential

- 5.3.2.1 Commercial

- 5.3.2.2 Infrastructure

- 5.3.2.3 Other Non-Residential Industries (Education, Healthcare, Civic and Religious,etc.)

- 5.4 By Installation

- 5.4.1 New Construction

- 5.4.2 Renovation

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics Countries

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Armacell

- 6.4.2 Aspen Aerogels Inc.

- 6.4.3 Atlas Roofing Corporation

- 6.4.4 BASF SE

- 6.4.5 Beijing New Building Materials Public Limited Company

- 6.4.6 Cellofoam North America Inc.

- 6.4.7 Covestro AG

- 6.4.8 Dow

- 6.4.9 DuPont

- 6.4.10 GAF Materials LLC

- 6.4.11 Holcim

- 6.4.12 Huntsman International LLC

- 6.4.13 Johns Manville

- 6.4.14 Kingspan Group

- 6.4.15 Knauf Group

- 6.4.16 Owens Corning

- 6.4.17 Recticel NV/SA

- 6.4.18 ROCKWOOL A/S

- 6.4.19 Saint-Gobain

- 6.4.20 Synthos

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technological Advancements in Green Insulation Materials