|

시장보고서

상품코드

1858844

RNA 간섭 치료제 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)RNA Interference Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

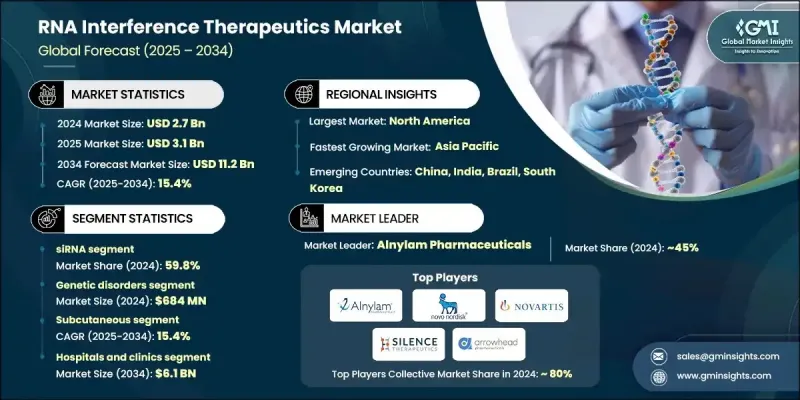

세계의 RNA 간섭 치료제 시장은 2024년에는 27억 달러로 평가되었고, CAGR 15.4%로 성장할 전망이며, 2034년에는 112억 달러에 이를 것으로 추정됩니다.

RNAi 기반 치료의 중요성이 증가하는 배경으로는 유전자 연구의 급증, 만성 질환의 부담 증가, 희귀 유전자 질환의 진단 증가 등이 있습니다. 이러한 치료법은 질병 관련 유전자를 침묵시키는 기능을 하며, 치료에 대한 정확하고 적극적인 접근법을 제공합니다. 기술 혁신, 특히 지질 나노입자 및 컨쥬게이트 시스템과 같은 전달 방법에서 RNAi 요법의 안전성과 효능이 현저히 향상되었습니다. 이에 따라 임상 용도의 폭이 넓어져 바이오 의약품 업계 내 협력 관계도 촉진되고 있습니다. RNAi가, 특히 간 이외의, 이전에는 도달하기 어려웠던 치료 영역으로 확대된 것은 그 임상적 유용성에 있어서 매우 중요한 변화를 나타내고 있습니다. 맞춤형 의료, 유전자 편집의 진보, 유전자 치료에 대한 국제적인 기운 증가는 시장의 기세에 크게 기여하고 있습니다. 유리한 규제 조건, 특히 희귀의약품의 개발을 위한 규제 조건은 촉진된 패스웨이와 더 긴 독점권을 제공하여 RNAi 영역을 제약 투자에 보다 매력적으로 만들고 있습니다. RNAi 시장은 틈새 과학에서 주류 치료로의 전환을 지원하는 민간 부문의 강력한 백업으로 진화를 계속하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 27억 달러 |

| 예측 금액 | 112억 달러 |

| CAGR | 15.4% |

소분자 간섭 RNA(siRNA) 분야는 2024년에 59.8%의 점유율을 차지하였고, CAGR 15.5%로 2034년에는 68억 달러에 달할 것으로 예측됩니다. siRNA 치료는 유전자 침묵의 정확성 및 오프 타겟 위험이 낮기 때문에 RNAi의 진보의 최전선에 있습니다. 보다 정교한 전달 기술의 개발과 유전자 발현 패턴의 깊은 이해는 간 이외의 새로운 치료 표적으로의 확장을 가능하게 했습니다. 심혈관 질환, 대사 질환 및 희귀 유전성 질환에서 유전자 발현을 조절하는 siRNA의 능력은 급속한 성장에 크게 기여합니다. 이 분야는 광범위한 RNAi 시장에서 가장 임상적으로 성숙하고 과학적으로 검증되었습니다.

유전성 질환 부문은 2024년에 6억 8,400만 달러를 창출했습니다. 이 이점은 다양한 유전성 질환의 원인 유전자를 표적으로 하는 siRNA 요법의 정확도가 높기 때문입니다. 이러한 치료법은 이전에는 효과적인 치료 옵션이 없었던 질병을 치료할 수 있는 강력한 잠재력을 가지고 있습니다. 희귀하고 유전적으로 뿌리 내린 질병의 치료에서 siRNA 기반 솔루션의 입증된 효능은 이 용도 분야에서 지속적인 임상 확장 및 상업적 관심을 지원합니다.

북미의 RNA 간섭 치료제 시장은 2024년에 45.7%의 점유율을 차지했습니다. 이 리더십은 주로 고급 헬스케어 인프라, 고도로 발달된 연구 생태계, 혁신적인 치료의 조기 도입의 조합으로 이어졌습니다. 미국 국립위생연구소(National Institutes of Health)와 같은 주요 기관으로부터의 대량의 자금 제공, 대기업 제약 기업 및 CDMO의 적극적인 참여로 이 지역의 의약품 개발이 가속화되고 있습니다. 정밀 기반 치료제에 대한 수요 증가와 유전성 질환 증가율은 이 분야의 지역 우위를 더욱 지원합니다.

세계의 RNA 간섭 치료제 시장에 기여하고 있는 주요 기업으로는 Silence Therapeutics, Sirnaomics, Arrowhead Pharmaceuticals, Alnylam Pharmaceuticals, Novartis, Creative Biogene, Arbutus Biopharma, Olix Pharmaceuticals, Benitec Biopharma, Sanofi, Novo Nordisk, Atalanta Therapeutics 치료제 시장에서 더 강한 존재를 확립하기 위해 대기업은 전략적 제휴, 기술 공유, 연구개발 투자에 주력하고 있습니다. 바이오테크놀러지 이노베이터와 주요 제약 회사와의 제휴를 통해 신속한 의약품 개척, 첨단 약물전달 시스템 접근, 보다 광범위한 시장 진출이 가능합니다. 또한 기업은 파이프라인의 다양화를 선호하고 일반적인 질병 및 희귀질환 모두를 대상으로 하는 치료제를 포함하도록 되어 있습니다. 오펀 드러그(희귀의약품)로 지정되어 규제 당국으로부터 신속한 승인을 얻을 수 있어 기업은 독점권 확대나 시장 투입 기간 단축 등 경쟁 우위를 얻을 수 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 유전성 질환의 유병률 증가

- RNA 전달 기술의 진보

- RNAi 기반 연구 투자 증가

- 만성 및 희귀질환에 대한 RNAi 치료제의 승인

- 업계의 잠재적 위험 및 과제

- RNAi 분자의 효과적인 전달에서의 과제

- RNAi 치료제의 높은 개발 비용

- 시장 기회

- 신경학 및 신경 퇴행성 질환에서 RNAi 용도

- 유전성 질환의 개별화 RNAi 요법

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 북미

- 기술 및 정세

- 현재의 기술 동향

- 신흥 기술

- 파이프라인 분석

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력

- 신제품 발표

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 소분자 간섭 RNA(siRNA)

- 마이크로 RNA(miRNA)

- 짧은 헤어핀 RNA(shRNA)

- 기타 제품 유형

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 암

- 유전자 질환

- 심혈관 질환

- 바이러스 감염증

- 신경퇴행성 질환

- 안과 질환

- 호흡기 질환

- 기타 용도

제7장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 정맥내 투여

- 피하(SC)

- 기타 투여 경로

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원 및 진료소

- 조사연구기관

- 기타 최종 사용

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Alnylam Pharmaceuticals

- Arbutus Biopharma

- Arrowhead Pharmaceuticals

- Atalanta Therapeutics

- Benitec Biopharma

- Creative Biogene

- Novartis

- Novo Nordisk

- OliX Pharmaceuticals

- Sanofi

- Silence Therapeutics

- Sirnaomics

The Global RNA Interference Therapeutics Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 15.4% to reach USD 11.2 billion by 2034.

The growing importance of RNAi-based therapies stems from a surge in genetic research, the rising burden of chronic diseases, and increasing diagnoses of rare genetic disorders. These therapies work by silencing disease-related genes, offering a precise and targeted approach to treatment. Technological innovations, particularly in delivery methods like lipid nanoparticles and conjugate systems, have significantly enhanced the safety and effectiveness of RNAi therapies. This has widened the scope for clinical application and encouraged collaborations within the biopharmaceutical industry. The expansion of RNAi into therapeutic areas previously difficult to reach, especially beyond the liver, marks a pivotal shift in its clinical utility. Personalized medicine, advancements in gene editing, and growing international momentum for gene therapies are key contributors to the market's momentum. Favorable regulatory conditions, especially those geared toward orphan drug development, offer accelerated pathways and longer exclusivity, making the RNAi space more attractive for pharmaceutical investments. The market continues to evolve with strong backing from both public and private sectors, supporting the transition of RNAi from niche science to mainstream therapy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $11.2 Billion |

| CAGR | 15.4% |

The small interfering RNA (siRNA) segment held a 59.8% share in 2024 and is projected to reach USD 6.8 billion by 2034, driven by a CAGR of 15.5%. siRNA therapies are at the forefront of RNAi advancements due to their gene-silencing precision and lower off-target risks. The development of more sophisticated delivery technologies and a deeper understanding of gene expression patterns has enabled expansion into new therapeutic targets outside the liver. The ability of siRNA to modulate gene expression in cardiovascular, metabolic, and rare inherited disorders is contributing significantly to its rapid growth. This segment remains the most clinically mature and scientifically validated within the broader RNAi market.

The genetic disorders segment generated USD 684 million in 2024. This dominance is attributed to the precision of siRNA therapies in targeting genes responsible for various inherited conditions. These therapies hold strong potential for addressing diseases that previously lacked effective treatment options. The proven efficacy of siRNA-based solutions in treating rare and genetically rooted conditions supports continued clinical expansion and commercial interest in this application area.

North America RNA Interference Therapeutics Market held a 45.7% share in 2024. This leadership is primarily driven by a combination of advanced healthcare infrastructure, a highly developed research ecosystem, and early adoption of innovative treatments. Significant funding from major institutions like the National Institutes of Health, along with active participation from major pharmaceutical players and CDMOs, has accelerated drug development in the region. The growing demand for precision-based therapeutics and rising rates of genetic diseases further support regional dominance in this space.

Key companies contributing to the Global RNA Interference Therapeutics Market include Silence Therapeutics, Sirnaomics, Arrowhead Pharmaceuticals, Alnylam Pharmaceuticals, Novartis, Creative Biogene, Arbutus Biopharma, OliX Pharmaceuticals, Benitec Biopharma, Sanofi, Novo Nordisk, and Atalanta Therapeutics. To establish a stronger presence in the RNAi therapeutics market, leading firms are focusing heavily on strategic partnerships, technology sharing, and R&D investments. Collaborations between biotech innovators and large pharmaceutical firms enable rapid drug development, access to advanced delivery systems, and broader market reach. Companies are also prioritizing pipeline diversification to include therapies targeting both common and rare diseases. By securing orphan drug status and fast-track regulatory designations, firms gain competitive advantages such as extended exclusivity and reduced time-to-market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 Route of administration trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of genetic disorders

- 3.2.1.2 Advancements in RNA delivery technologies

- 3.2.1.3 Rising investment in RNAi-based research

- 3.2.1.4 Approval of RNAi therapeutics for chronic and rare diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Challenges in effective delivery of RNAi molecules

- 3.2.2.2 High cost of RNAi therapeutics development

- 3.2.3 Market opportunities

- 3.2.3.1 RNAi applications in neurology and neurodegenerative diseases

- 3.2.3.2 Personalized RNAi therapies for genetic diseases

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Small interfering RNA (siRNA)

- 5.3 MicroRNA (miRNA)

- 5.4 Short hairpin RNA (shRNA)

- 5.5 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cancer

- 6.3 Genetic disorders

- 6.4 Cardiovascular diseases

- 6.5 Viral infections

- 6.6 Neurodegenerative diseases

- 6.7 Ophthalmic disorders

- 6.8 Respiratory disorders

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Intravenous (IV)

- 7.3 Subcutaneous (SC)

- 7.4 Other route of administration

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Research laboratories

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alnylam Pharmaceuticals

- 10.2 Arbutus Biopharma

- 10.3 Arrowhead Pharmaceuticals

- 10.4 Atalanta Therapeutics

- 10.5 Benitec Biopharma

- 10.6 Creative Biogene

- 10.7 Novartis

- 10.8 Novo Nordisk

- 10.9 OliX Pharmaceuticals

- 10.10 Sanofi

- 10.11 Silence Therapeutics

- 10.12 Sirnaomics