|

시장보고서

상품코드

1858876

자동차 엣지 AI 가속기 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Edge AI Accelerators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

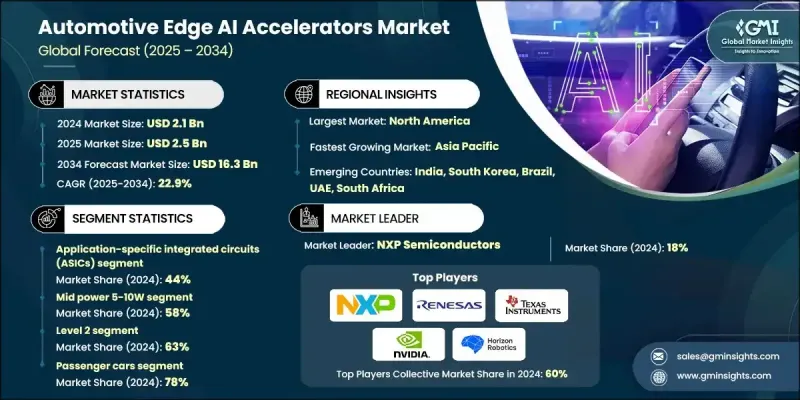

세계의 자동차 엣지 AI 가속기 시장 규모는 2024년에 21억 달러로 평가되었고, CAGR 22.9%로 성장할 전망이며, 2034년에는 163억 달러에 이를 것으로 예측되고 있습니다.

시장 확대는 최신 자동차에 실시간 처리 기능이 구현되고 있는 것과 관련이 있습니다. GPU와 FPGA에서 ASIC과 NPU에 이르는 엣지 AI 가속기는 ADAS, 드라이버 의식 모니터링, 인텔리전트 인포테인먼트, 음성 대화 기능 등의 복잡한 차재 시스템을 실현하는 데 필수적입니다. 자동차가 소프트웨어로 정의된 커넥티드 플랫폼으로 이동함에 따라, 빠르고 효율적이며 지역화된 AI 컴퓨팅에 대한 수요가 급속히 가속화되고 있습니다. 전기자동차, 반자동차, 자율주행차로의 이동은 엣지 기반 AI 가속의 필요성을 더욱 높여주고 있습니다. LiDAR, 레이더, 카메라 등의 센서에서 엄청난 데이터 흐름을 초저지연으로 처리하는 것은 안전 및 차량 성능에 필수적입니다. 또한 사이버 보안, 기능 안전 및 실시간 무선 소프트웨어 업데이트와 관련된 규제 요구 사항은 엣지에서 고성능 AI 하드웨어의 필요성을 강화하고 있습니다. 전기자동차는 배터리에 최적화된 프로세서에 대한 수요가 증가하고 있으며, 이 분야의 기술 혁신을 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 21억 달러 |

| 예측 금액 | 163억 달러 |

| CAGR | 22.9% |

특정 용도용 집적 회로(ASIC) 부문은 2024년에 44%의 점유율을 차지하였고, 2034년까지 24.1%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다. 이 칩은 작업에 특화된 AI 처리를 최대한의 에너지 효율과 최소한의 지연으로 실현하도록 설계되었습니다. 이러한 아키텍처는 지각 모델링, 의사 결정, 실시간 센서 데이터 처리와 같은 작업의 원활한 처리를 지원하며 고급 자동차 용도에 매우 적합합니다.

중전력(5-10W) 부문은 2024년에 58%의 점유율을 차지했으며, 예측 기간을 통해 CAGR 23.8%로 성장할 전망입니다. 이 출력 범위는 성능, 효율 및 열 밸런스 스위트 스팟에 해당합니다. 차량 설계의 제약 내에서 관리 가능한 열과 전력 소비 레벨을 유지하면서 멀티 카메라 입력 처리 및 라이브 물체 검출 등의 고급 운전 지원 기능에 충분한 능력을 제공합니다. 이 부문은 성능과 에너지 절약 모두를 선호하는 최신 차량 아키텍처 수요 증가에 대응하기에 적합한 위치에 있습니다.

북미의 자동차 엣지 AI 가속기 시장은 34%의 점유율을 차지했으며, 2024년에는 7억 340만 달러를 창출했습니다. 이 리더십은 진화하는 규제 프레임워크, AI 개발에 대한 엄청난 투자, 고도로 성숙한 자동차 기술 생태계의 조합에 기인합니다. 이 지역의 하이테크 기업과 자동차 관련 기업에 의한 강력한 제도적 지원 및 적극적인 혁신으로 상용차와 승용차의 두 부문에서 엣지 AI 하드웨어의 전개가 가속화되고 있습니다.

세계의 자동차 엣지 AI 가속기 시장에서 사업을 전개하는 주요 기업으로는 Renesas Electronics, Qualcomm, NVIDIA, Arm, Horizon Robotics, Texas Instruments(TI), Infineon Technologies, NXP Semiconductors, STMicroelectronics, Mobileye 등이 있습니다. 세계 자동차 엣지 AI 가속기 시장의 주요 기업은 경쟁 우위를 확보하기 위해 통합 칩 설계, 전략적 제휴 및 성능 최적화에 주력하고 있습니다. 많은 기업들이 커스텀 AI 칩 개발에 투자하고 있으며, 에너지 소비를 최소화하면서 컴퓨팅 파워를 극대화하고 EV 및 자율 주행 플랫폼에서의 엣지 처리 수요 증가에 대응하고 있습니다. OEM 및 Tier 1 공급업체와의 제휴를 통해 ADAS 및 인포테인먼트 시스템에 맞는 플랫폼별 가속기를 공동 개발할 수 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 정보원

- 세계

- 지역 및 국가

- 기본 추정 및 계산

- 기준 연도의 산출

- 시장 추계의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측

- 조사의 전제조건 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- ADAS(선진 운전 지원 시스템) 수요 증가

- 자율주행차의 채용 증가

- 자동차의 안전성 및 보안에 대한 주목 고조

- 자동차 자동화를 촉진하는 정부 규제

- 커넥티드카 기술 확대

- AI 칩 기술의 진보

- 업계의 잠재적 위험 및 과제

- 첨단 AI 하드웨어의 고비용

- 엣지 AI 시스템 통합의 복잡성

- 시장 기회

- 성장하는 전기자동차(EV) 시장

- 스마트 플릿 관리에 대한 수요 증가

- 자동차 AI에 투자하는 신흥 시장

- 칩 제조업체 및 자동차 제조업체의 콜라보레이션

- 성장 촉진요인

- 성장 가능성 분석

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 코스트 내역 분석

- 기술 및 정세

- 현재의 기술 동향

- 신흥 기술

- 규제 상황

- ISO 26262 기능 안전 요구사항

- AUTOSAR 적응 플랫폼 대응

- ASPICE 소프트웨어 개발 표준

- 사이버 보안 표준(ISO 21434)

- 가격 동향

- 지역별

- 프로세서별

- 지속가능성 및 환경 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경 친화적인 노력

- 투자 및 자금 동향 분석

- 보안 및 사이버 보안 프레임워크 분석

- 하드웨어 보안 모듈(HSM) 통합

- 보안 부팅 및 신뢰할 수 있는 실행 환경

- 무선(OTA) 업데이트 보안

- 생태계 파트너십 및 얼라이언스 분석

- 칩과 OEM의 전략적 파트너십

- 소프트웨어 플랫폼의 콜라보레이션

- 총소유 비용(TCO) 분석

- 하드웨어 취득 비용

- 소프트웨어 개발 및 통합 비용

- 검증 및 인증 비용

- 제조 및 전개 비용

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발표

- 확장 계획 및 자금 조달

제5장 시장 추계 및 예측 : 프로세서별(2021-2034년)

- 주요 동향

- 중앙처리장치(CPU)

- 그래픽 프로세싱 유닛(GPU)

- 특정 용도용 집적 회로(ASIC)

- 필드 프로그래머블 게이트 어레이(FPGA)

제6장 시장 추계 및 예측 : 전력별(2021-2034년)

- 주요 동향

- 5W 미만의 저전력

- 미드 파워 5-10 W

- 10W 이상의 고출력

제7장 시장 추계 및 예측 : 자율성 레벨별(2021-2034년)

- 주요 동향

- 레벨 1

- 레벨 2

- 레벨 3

- 레벨 4

- 레벨 5

제8장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 인도네시아

- 필리핀

- 태국

- 한국

- 싱가포르

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Arm

- Horizon Robotics

- Infineon Technologies

- MediaTek

- Mobileye

- NVIDIA

- NXP Semiconductors

- Qualcomm

- Renesas Electronics

- Samsung Electronics

- STMicroelectronics

- Texas Instruments(TI)

- 지역 기업

- CEVA

- GlobalFoundries

- HiSilicon

- Nextchip

- SemiDrive

- Socionext

- Tsinghua Unigroup

- Verisilicon

- 신흥 기업 및 디스랩터

- Ambarella

- Hailo Technologies

- Kneron

- Mythic

- SiMa.ai

The Global Automotive Edge AI Accelerators Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 22.9% to reach USD 16.3 billion by 2034.

The market's expansion is tied to the growing implementation of real-time processing capabilities in modern vehicles. Edge AI accelerators ranging from GPUs and FPGAs to ASICs and NPUs are becoming indispensable in enabling complex in-vehicle systems such as ADAS, driver awareness monitoring, intelligent infotainment, and voice interaction features. As vehicles transition into software-defined, connected platforms, the demand for fast, efficient, localized AI computation has accelerated sharply. The shift toward electric, semi-autonomous, and autonomous vehicles further intensifies the need for edge-based AI acceleration. Handling massive data flows from sensors like LiDAR, radar, and cameras with ultra-low latency is critical to safety and vehicle performance. Additionally, regulatory requirements tied to cybersecurity, functional safety, and real-time over-the-air software updates are reinforcing the need for high-performance AI hardware at the edge. The increasing demand for battery-optimized processors in electric vehicles further drives innovation in this space.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $16.3 Billion |

| CAGR | 22.9% |

The application-specific integrated circuits (ASICs) segment held a 44% share in 2024 and is anticipated to grow at a 24.1% CAGR through 2034. These chips are engineered to deliver task-specific AI processing with maximum energy efficiency and minimal delay. Their tailored architecture supports seamless handling of tasks such as perception modeling, decision-making, and real-time sensor data processing, making them highly suitable for advanced automotive applications.

The mid-power (5-10W) segment held 58% share in 2024 and will grow at a CAGR of 23.8% through the forecast period. This power range hits the sweet spot between performance, efficiency, and thermal balance. It offers adequate capacity for advanced driver assistance functions like multi-camera input handling and live object detection while maintaining heat and power consumption levels manageable within vehicle design constraints. The segment is well-positioned to cater to rising demands from modern vehicle architectures that prioritize both performance and energy savings.

North America Automotive Edge AI Accelerators Market held a 34% share and generated USD 703.4 million in 2024. This leadership stems from a combination of evolving regulatory frameworks, substantial investments in AI development, and a highly mature automotive technology ecosystem. Strong institutional support and aggressive innovation by tech and automotive players in the region have accelerated the deployment of edge AI hardware across both commercial and passenger vehicle segments.

Key players operating in the Global Automotive Edge AI Accelerators Market include Renesas Electronics, Qualcomm, NVIDIA, Arm, Horizon Robotics, Texas Instruments (TI), Infineon Technologies, NXP Semiconductors, STMicroelectronics, and Mobileye. Leading companies in the Global Automotive Edge AI Accelerators Market are focusing on integrated chip design, strategic collaborations, and performance optimization to gain a competitive edge. Many players are investing in custom AI chip development to maximize computing power while minimizing energy consumption, addressing the growing demand for edge processing in EVs and autonomous platforms. Partnerships with OEMs and Tier 1 suppliers are enabling co-development of platform-specific accelerators tailored to ADAS and infotainment systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Processor

- 2.2.3 Power

- 2.2.4 Level of autonomy

- 2.2.5 Vehicle

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for advanced driver assistance systems (ADAS)

- 3.2.1.2 Rising adoption of autonomous vehicles

- 3.2.1.3 Increased focus on vehicle safety and security

- 3.2.1.4 Government regulations promoting vehicle automation

- 3.2.1.5 Expansion of connected car technologies

- 3.2.1.6 Advancements in AI chip technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced AI hardware

- 3.2.2.2 Complexity in integrating edge AI systems

- 3.2.3 Market opportunities

- 3.2.3.1 Growing electric vehicle (EV) market

- 3.2.3.2 Rising demand for smart fleet management

- 3.2.3.3 Emerging markets investing in automotive AI

- 3.2.3.4 Collaborations between chipmakers and automakers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Cost breakdown analysis

- 3.8 Technology landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Regulatory landscape

- 3.9.1 ISO 26262 functional safety requirements

- 3.9.2 AUTOSAR adaptive platform compliance

- 3.9.3 ASPICE software development standards

- 3.9.4 Cybersecurity standards (ISO 21434)

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By processor

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Investment & funding trends analysis

- 3.13 Security & cybersecurity framework analysis

- 3.13.1 Hardware security module (HSM) integration

- 3.13.2 Secure boot & trusted execution environment

- 3.13.3 Over-the-air (OTA) update security

- 3.14 Ecosystem partnerships & alliance analysis

- 3.14.1 Chip-OEM strategic partnerships

- 3.14.2 Software platform collaborations

- 3.15 Total cost of ownership (TCO) analysis

- 3.15.1 Hardware acquisition costs

- 3.15.2 Software development & integration costs

- 3.15.3 Validation & certification expenses

- 3.15.4 Manufacturing & deployment costs

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Processor, 2021 - 2034 (USD Bn, Units)

- 5.1 Key trends

- 5.2 Central processing unit (CPU)

- 5.3 Graphics processing unit (GPU)

- 5.4 Application-specific integrated circuits (ASICs)

- 5.5 Field-programmable gate array (FPGA)

Chapter 6 Market Estimates & Forecast, By Power, 2021 - 2034 (USD Bn, Units)

- 6.1 Key trends

- 6.2 Low power <5W

- 6.3 Mid power 5-10W

- 6.4 High power >10W

Chapter 7 Market Estimates & Forecast, By Level of autonomy, 2021 - 2034 (USD Bn, Units)

- 7.1 Key trends

- 7.2 Level 1

- 7.3 Level 2

- 7.4 Level 3

- 7.5 Level 4

- 7.6 Level 5

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Bn, Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCV)

- 8.3.2 Medium commercial vehicles (MCV)

- 8.3.3 Heavy commercial vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Indonesia

- 9.4.6 Philippines

- 9.4.7 Thailand

- 9.4.8 South Korea

- 9.4.9 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Arm

- 10.1.2 Horizon Robotics

- 10.1.3 Infineon Technologies

- 10.1.4 MediaTek

- 10.1.5 Mobileye

- 10.1.6 NVIDIA

- 10.1.7 NXP Semiconductors

- 10.1.8 Qualcomm

- 10.1.9 Renesas Electronics

- 10.1.10 Samsung Electronics

- 10.1.11 STMicroelectronics

- 10.1.12 Texas Instruments (TI)

- 10.2 Regional Players

- 10.2.1 CEVA

- 10.2.2 GlobalFoundries

- 10.2.3 HiSilicon

- 10.2.4 Nextchip

- 10.2.5 SemiDrive

- 10.2.6 Socionext

- 10.2.7 Tsinghua Unigroup

- 10.2.8 Verisilicon

- 10.3 Emerging Players / Disruptors

- 10.3.1 Ambarella

- 10.3.2 Hailo Technologies

- 10.3.3 Kneron

- 10.3.4 Mythic

- 10.3.5 SiMa.ai