|

시장보고서

상품코드

1871096

석유 및 가스 열교환기 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Oil and Gas Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

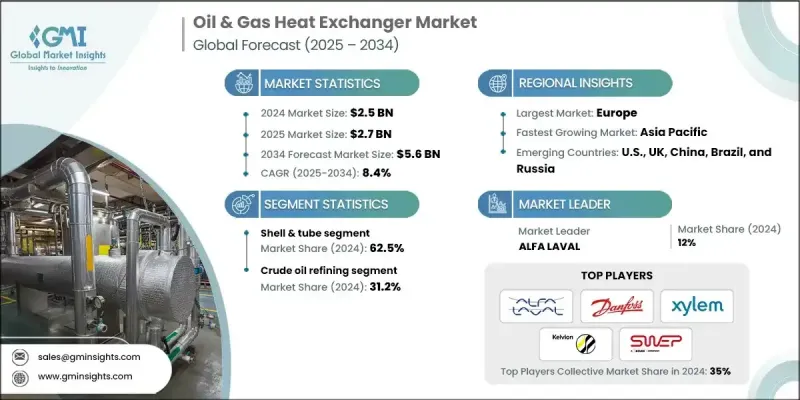

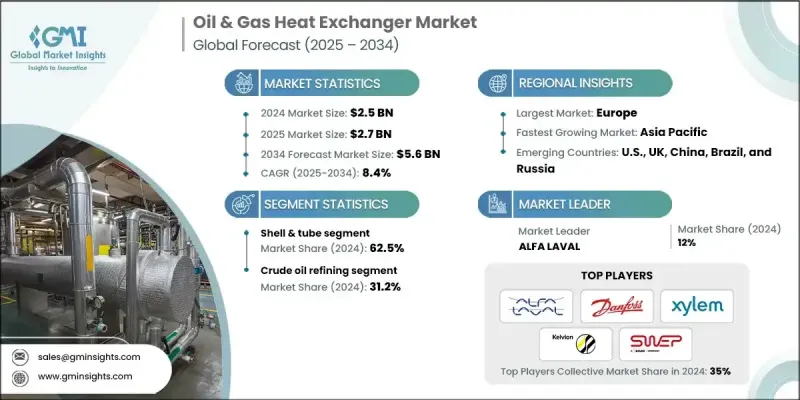

세계의 석유 및 가스 열교환기 시장은 2024년에 25억 달러로 평가되었고 2034년까지 연평균 복합 성장률(CAGR)은 8.4%를 나타낼 것으로 예측되며 56억 달러에 달할 전망입니다.

석유 및 가스 인프라에 대한 지속적인 투자와 효율적인 냉난방 시스템에 대한 수요 증가가 성장을 주도함에 따라 업계 전망은 여전히 밝습니다. 열교환기는 유체 흐름 간 효과적인 에너지 전달을 보장함으로써 석유 및 가스 운영 전반에 걸쳐 열적 균형을 유지하는 데 핵심적인 역할을 수행합니다. 이는 생산성을 향상시키고 운영 비용을 절감합니다. 정제, 가공 및 탐사 활동 전반에 걸쳐 에너지 효율적인 열 관리에 대한 관심이 증가하고 기술 발전이 더해지면서 시장 확장이 더욱 촉진되고 있습니다. 정밀한 온도 제어와 운영 신뢰성을 보장하는 프로젝트별 맞춤형 열교환기의 채택 증가 역시 시장 침투를 강화하고 있습니다. 또한 복잡하거나 공간 제약이 있는 시설에 적합한 소형화 및 적응형 설계에 대한 선호도가 높아지면서 제품 채택이 가속화되고 있습니다. 에너지 성능 개선과 배출량 감소를 목표로 한 지속 가능하고 비용 효율적인 열 기술로의 전환은 산업 동향과 경쟁력을 재정의하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 25억 달러 |

| 예측 금액 | 56억 달러 |

| CAGR | 8.4% |

쉘 및 튜브 부문은 2024년에 62.5%의 점유율을 차지하며, 2034년까지 연평균 복합 성장률(CAGR) 8%를 보일 것으로 예측됩니다. 이 부문은 원유 정제 및 가스 처리 응용 부문에서 광범위하게 활용되며, 특히 높은 내구성과 극한의 압력 및 온도 조건에서도 작동 가능한 능력 덕분에 지속적으로 주목받고 있습니다. 상류 및 하류 인프라에 대한 투자 확대와 안정적이고 효율적인 열 성능에 대한 지속적인 수요가 이러한 성장 추세를 뒷받침하고 있습니다. 내식성 소재의 도입, 열전달 효율 향상을 위한 튜브 구성 개선, 예측 유지보수 및 운영 최적화를 위해 설계된 첨단 모니터링 시스템의 통합은 제품 수요와 운영 전반의 효율성을 높이고 있습니다.

원유 정제 용도 부문은 2024년에 31.2%의 점유율을 차지하고 2034년까지 연평균 복합 성장률(CAGR) 7.5%를 보일 것으로 예측됩니다. 전 세계 정제 능력 증가와 플랜트 성능 최적화에 대한 강조가 이 부문의 성장에 크게 기여하고 있습니다. 에너지 효율 향상과 배출량 감소를 장려하는 더욱 엄격한 환경 규범이 시장 환경을 더욱 형성하고 있습니다. 신뢰성 향상과 장비 수명 연장을 위해 설계된 디지털 기술, 예측 유지보수 도구, 고효율 열교환기의 통합 확대가 이러한 성장을 촉진하고 있습니다.

미국의 석유 및 가스 열교환기 시장은 2024년에 78%의 점유율을 차지해 4억 5,280만 달러의 규모가 되었습니다. 미국 시장의 성장은 강력한 석유 및 가스 인프라, 셰일 추출 기술 발전, 정제 및 가공 설비에 대한 투자 증가에 기인합니다. 지속가능성 목표에 부합하는 에너지 인프라 현대화와 에너지 효율적 솔루션으로의 전환에 대한 관심 증대가 주요 성장 동력입니다. 진화하는 환경 기준과 탄소중립 목표 추진은 해당 지역 전반에 걸쳐 첨단 열교환기 시스템의 광범위한 채택을 더욱 뒷받침하고 있습니다.

세계의 석유 및 가스 열교환기 시장에서 주요 기업으로는 ALFA LAVAL, API Heat Transfer, BARRIQUAND Heat Exchanger, Bronswerk, Danfoss, Funke Warmeaustauscher Apparatebau GmbH, HFM, HISAKA WORKS LTD., HRS 열교환기, KAM Thermal Equipment LTD, Kelvion Holding GmbH, Mersen, Metalforms LLC, Nexson Group, SPX Flow, SWEP International, Thermofin, TITAN Metal Fabricators, Tranter, Turnbull & Scott Group, Xylem 등이 있습니다. 석유 및 가스 열교환기 시장의 주요 업체들은 시장 입지와 경쟁력을 강화하기 위해 여러 전략을 적극적으로 채택하고 있습니다. 기업들은 증가하는 수요를 충족시키기 위해 글로벌 생산 능력 확대와 공급망 강화에 주력하고 있습니다. 전략적 협력 및 합병을 통해 기술 공유와 포트폴리오 다각화가 가능해지고 있습니다. 기업들은 진화하는 산업 요구사항에 맞춰 고성능, 내식성, 에너지 효율적인 열교환기 개발을 위해 연구개발(R&D)에 막대한 투자를 하고 있습니다. 운영 신뢰성 향상과 가동 중단 시간 감소를 위해 디지털 모니터링 시스템과 예측 유지보수 기술의 통합이 우선순위로 추진되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 원재료 가용성 및 조달 분석

- 밸류체인에 영향을 주는 주요 요인

- 혁신

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 억제요인 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 석유 및 가스 열교환기의 코스트 구조 분석

- 새로운 기회와 동향

- IoT 기술을 활용한 디지털 전환

- 신흥 시장 진출

- 투자분석과 전망

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 노력

- 주요 제휴 및 협력관계

- 주요 M&A 활동

- 제품 혁신과 신제품 출시

- 시장 확대 전략

- 경쟁 벤치마킹

- 전략적 대시보드

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 기술별(2021-2034년)

- 주요 동향

- 쉘 및 튜브

- 플레이트

- 공냉식

- 기타

제6장 시장 규모와 예측 : 용도별(2021-2034년)

- 주요 동향

- 육상 생산 시설

- 원유 정제

- 석유화학

- LNG시설

- 파이프라인 시스템

- 기타

제7장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 이탈리아

- 스페인

- 폴란드

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 인도네시아

- 말레이시아

- 태국

- 베트남

- 필리핀

- 호주

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이집트

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

- 콜롬비아

- 칠레

제8장 기업 프로파일

- ALFA LAVAL

- API Heat Transfer

- BARRIQUAND Heat Exchanger

- Bronswerk

- Danfoss

- Funke Warmeaustauscher Apparatebau GmbH

- HFM

- HISAKA WORKS LTD.

- HRS Heat Exchangers

- KAM Thermal Equipment, LTD

- Kelvion Holding GmbH

- Mersen

- Metalforms, LLC

- Nexson Group

- SPX Flow

- SWEP International

- Thermofin

- TITAN Metal Fabricators

- Tranter

- Turnbull & Scott Group

- Xylem

The Global Oil & Gas Heat Exchanger Market was valued at USD 2.5 Billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 5.6 Billion by 2034.

The industry's outlook remains strong as continuous investments in oil and gas infrastructure and rising demand for efficient heating and cooling systems continue to drive growth. Heat exchangers play a vital role in maintaining thermal balance across oil and gas operations by ensuring effective energy transfer between fluid streams, which enhances productivity and reduces operational costs. The growing focus on energy-efficient thermal management across refining, processing, and exploration activities, coupled with technological advancements, is further stimulating market expansion. Increasing adoption of project-specific, customized heat exchangers that ensure precise temperature control and operational reliability is also enhancing market penetration. Moreover, the growing preference for compact and adaptable designs suitable for complex or space-constrained facilities is accelerating product adoption. The shift toward sustainable and cost-effective thermal technologies aimed at improving energy performance and reducing emissions is redefining industry trends and competitiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 8.4% |

The shell and tube segment held a 62.5% share in 2024 and is forecasted to grow at a CAGR of 8% through 2034. This segment continues to gain traction due to its robust use in both crude oil refining and gas processing applications, primarily driven by its high durability and ability to operate under extreme pressure and temperature conditions. Expanding investments in upstream and downstream infrastructure and the continuous need for reliable and efficient thermal performance are supporting this growth trajectory. The introduction of corrosion-resistant materials, improved tube configurations for enhanced heat transfer, and the integration of advanced monitoring systems designed for predictive maintenance and operational optimization are boosting product demand and efficiency across operations.

The crude oil refining application segment held a 31.2% share in 2024 and is expected to grow at a CAGR of 7.5% through 2034. Rising refining capacities worldwide, coupled with an increasing emphasis on optimizing plant performance, are contributing significantly to the segment's growth. Stricter environmental norms encouraging better energy utilization and reduced emissions are further shaping the market landscape. The growing integration of digital technologies, predictive maintenance tools, and high-efficiency heat exchangers designed to improve reliability and extend equipment life is fueling this expansion.

United States Oil & Gas Heat Exchanger Market held a 78% share in 2024, generating USD 452.8 million. The U.S. market is expanding due to the country's strong oil and gas infrastructure, advancements in shale extraction, and rising investments in refining and processing capacities. Increasing focus on modernizing energy infrastructure and the transition toward energy-efficient solutions in alignment with sustainability goals are major drivers behind this growth. Evolving environmental standards and the push toward net-zero objectives are further supporting widespread adoption of advanced heat exchanger systems across the region.

Leading companies operating in the Global Oil & Gas Heat Exchanger Market include ALFA LAVAL, API Heat Transfer, BARRIQUAND Heat Exchanger, Bronswerk, Danfoss, Funke Warmeaustauscher Apparatebau GmbH, HFM, HISAKA WORKS LTD., HRS Heat Exchangers, KAM Thermal Equipment LTD, Kelvion Holding GmbH, Mersen, Metalforms LLC, Nexson Group, SPX Flow, SWEP International, Thermofin, TITAN Metal Fabricators, Tranter, Turnbull & Scott Group, and Xylem. Key players in the Oil & Gas Heat Exchanger Market are actively adopting several strategies to enhance their market presence and competitiveness. Companies are focusing on expanding their global production capabilities and strengthening their supply chains to meet increasing demand. Strategic collaborations and mergers are enabling technology sharing and portfolio diversification. Firms are heavily investing in R&D to develop high-performance, corrosion-resistant, and energy-efficient heat exchangers tailored to evolving industry requirements. Integration of digital monitoring systems and predictive maintenance technologies is being prioritized to enhance operational reliability and reduce downtime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 Cost structure analysis of oil & gas heat exchangers

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Shell & tube

- 5.3 Plate

- 5.4 Air cooled

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Onshore production facilities

- 6.3 Crude oil refining

- 6.4 Petrochemical processing

- 6.5 LNG facilities

- 6.6 Pipeline systems

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Russia

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Poland

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Indonesia

- 7.4.6 Malaysia

- 7.4.7 Thailand

- 7.4.8 Vietnam

- 7.4.9 Philippines

- 7.4.10 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Egypt

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Colombia

- 7.6.4 Chile

Chapter 8 Company Profiles

- 8.1 ALFA LAVAL

- 8.2 API Heat Transfer

- 8.3 BARRIQUAND Heat Exchanger

- 8.4 Bronswerk

- 8.5 Danfoss

- 8.6 Funke Warmeaustauscher Apparatebau GmbH

- 8.7 HFM

- 8.8 HISAKA WORKS LTD.

- 8.9 HRS Heat Exchangers

- 8.10 KAM Thermal Equipment, LTD

- 8.11 Kelvion Holding GmbH

- 8.12 Mersen

- 8.13 Metalforms, LLC

- 8.14 Nexson Group

- 8.15 SPX Flow

- 8.16 SWEP International

- 8.17 Thermofin

- 8.18 TITAN Metal Fabricators

- 8.19 Tranter

- 8.20 Turnbull & Scott Group

- 8.21 Xylem