|

시장보고서

상품코드

1876651

선외 보트 엔진 시장 : 시장 비즈니스 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Outboard Boats Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

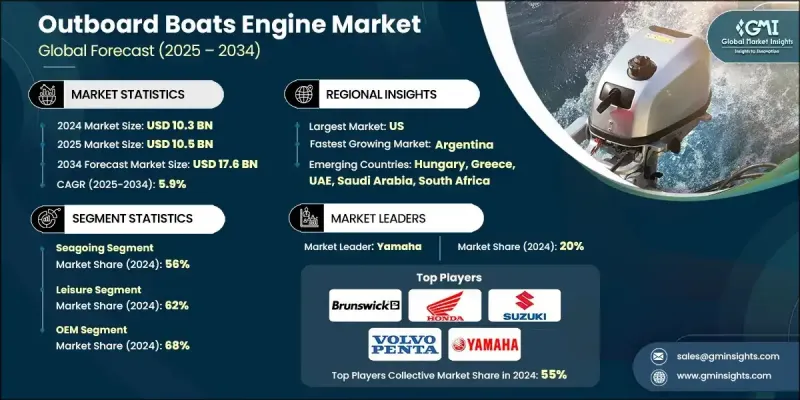

세계의 선외 보트 엔진 시장은 2024년에 103억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.9%로 성장할 전망이며, 176억 달러에 이를 것으로 예측되고 있습니다.

해안 및 내륙 지역에서 레크리에이션 보트와 수상 활동의 인기가 높아짐에 따라 수요는 계속 증가하고 있습니다. 레저 기기에 대한 소비자 지출 증가, 마리나 인프라의 확충, 관광 개발의 진전이 함께, 예측 기간을 통해 선외 보트 엔진의 채용이 가속하고 있습니다. 또한 제조업체가 상업 운영 및 레크리에이션 보트 모두에 적합한 가볍고 연비 효율이 높으며, 배출 가스가 적은 기술을 도입하는 것도 시장 진전에 기여하고 있습니다. 특히 배출 기준이 엄격화되는 가운데 4행정 시스템과 직분사 설계로의 전환이 장기적인 성장을 강화하고 있습니다. 상업 어업, 소규모 해상 운송, 해안 물류의 신뢰성이 높은 선외 보트 엔진의 의존도가 높아짐에 따라 선진적이고 고성능인 모델에 대한 수요가 더욱 높아지고 있습니다. 연안 개발에 대한 투자 증가와 소규모 어업 및 양식 활동 확대도 엔진 공급업체의 기회를 확대하여 안정적인 시장 전망을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 103억 달러 |

| 예측 금액 | 176억 달러 |

| CAGR | 5.9% |

해상 부문은 2024년에 56%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 5.9% 이상으로 성장할 것으로 예측됩니다. 해안 여행, 해안 여행, 수상 스포츠 활동에 대한 관심이 높아짐에 따라 높은 내구성, 장거리 이동, 강력한 해양 성능을 갖춘 외양용 선외 보트 엔진의 이용이 촉진되고 있습니다. 해상 보안 활동 및 상업 수송에 있어서의 사용 증가 또한 신속한 대응과 신뢰성이 높은 성능에 의해 더욱 보급을 뒷받침하고 있습니다.

레저 분야는 2024년에 62%의 점유율을 차지했으며, 2025-2034년 CAGR 5%로 성장할 것으로 예측됩니다. 레크리에이션 보트, 가족 외출, 주말 수상 활동에 대한 관심 증가가 소형 및 중형 보트용 선외 보트 엔진에 대한 수요를 지속적으로 밀어 올리고 있습니다. 가처분소득 증가, 도시형 라이프스타일 동향, 해양레크리에이션 참여 확대는 호수, 해안, 하천시스템에서의 판매를 촉진하고 있습니다.

미국의 선외 보트 엔진 시장은 2024년에 86%의 점유율을 차지하였고, 35억 7,000만 달러의 수익을 창출했습니다. 소비자 구매력의 힘과 급속히 확대되는 선착장 네트워크로 인해 레크리에이션 보트 이용은 여전히 활발합니다. 어선, 수상 오토바이, 레저선에 대한 수요는 해수역과 담수역 모두에서 계속 증가하고 있습니다. 미국 제조업체는 연비 향상, 배출 가스 감소, 부드러운 작동성을 제공하는 기술적으로 강화된 4행정 및 디지털 제어 선외 보트 엔진에 주력하고 있습니다.

세계 선외 보트 엔진 시장의 주요 기업으로는 Brunswick, Oxe Marine, Yamaha, Honda, Suzuki Motor, Cox Powertrain, Parsun Power Machine, Hidea Power, Volvo Penta 및 Tohatsu 등이 있습니다. 선외 보트 엔진 제조업체 각사는 변화하는 소비자의 요구와 규제 요건에 대응하기 위해 고연비 효율, 저배출 가스, 경량 구조를 갖춘 엔진 개발을 통해 시장에서의 지위를 강화하고 있습니다. 많은 기업들이 최종 사용자를 위한 성능 향상과 유지 보수 간소화를 목적으로 디지털 제어 시스템과 첨단 진단 기술에 대한 투자를 추진하고 있습니다. 보트 제조업체와의 전략적 제휴는 유통망의 확대 및 장기적인 OEM 파트너십 확보에 기여하고 있습니다. 또한 4 스트로크 엔진과 고출력 엔진에 대한 수요 증가에 대응하기 위해 생산 능력을 강화하기 위해 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위 및 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별 및 국가별

- 기본 추정치 및 계산

- 기준 연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건 및 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 레크리에이션 피싱 및 수상 스포츠 수요 증가

- 소형 풍선 보트 및 휴대용 보트의 보급 확대

- 범용성 향상을 위한 선내에서 선외 보트 엔진으로의 이행

- 연안 관광 및 해양 레저 산업의 확대

- 경량으로 연료 효율이 높은 추진 시스템에 대한 수요

- 업계의 잠재적 위험 및 과제

- 엄격한 선박 배출 규제

- 소음 및 진동에 관한 우려 사항

- 전동 선외 보트 엔진의 적용 범위 제한

- 고출력 모델에 있어서 높은 초기 비용

- 시장 기회

- 전동화 및 하이브리드 통합

- 신흥 시장에 있어서 휴대용 선외 보트 엔진 수요

- 에코 투어리즘 및 지속 가능한 보트 활동의 성장

- 노후화한 선대로부터의 대체 수요

- 성장 촉진요인

- 성장 가능성 분석

- 주요 시장 동향과 변화

- 장래 시장 동향

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신의 전망

- 현행 기술

- 첨단 연료 분사 시스템

- 염수 환경용 내식성 재료

- 디지털 엔진 모니터링 및 스마트 제어

- 신흥 기술

- 전기식 및 하이브리드식 선외 보트 엔진 추진 시스템

- 경량 복합재료

- 모듈식 및 휴대용 전원 유닛

- 커넥티드 아웃보드(IoT 통합)

- 현행 기술

- 특허 분석

- 생산 통계

- 생산 거점

- 소비 거점

- 수출 및 수입

- 가격 동향

- 지역별

- 추진력별

- 가격 분석 및 밸류체인 경제성

- 마력 부문별 선외 보트 엔진 가격 동향

- 고출력 모델에 있어서 프리미엄 가격 전략

- 비용 구조의 내역

- 지역별 가격 감응도

- 비용 내역 분석

- 부품 레벨에서의 비용 구조 분석

- 제조 비용 요인 및 최적화

- 지역별 비용 차이 및 경쟁상의 영향

- 비용 관리 전략 및 경쟁적 포지셔닝

- 이용 사례

- 정부 및 공공 안전 분야에서의 용도

- 상업 항만 및 항만 운영

- 레크리에이션 및 관광 용도

- 전동화 및 하이브리드 통합 용도

- 대체 연료 및 지속 가능한 추진 시스템에의 용도

- 최상의 시나리오

- 인프라 지원에 의한 가속적인 전동화

- 지속가능한 연료의 통합 및 순환형 경제

- 프리미엄 성능 및 기술 리더십

- 세계 시장 확대 및 신흥 시장 개발

- 통합된 지속가능성 및 탁월한 성능

- 국제무역 및 수출입 분석

- 지역별 수입 의존도

- 무역규제 및 관세의 영향

- 지속가능성 및 환경면

- 물리적 프로토타입 및 테스트 감소

- 에너지 효율 개선

- 전동화 및 배출 감축 기술에 대한 지원

- 라이프사이클 및 전자폐기물 관리

- 환경 규제에 대한 대응

- 제품 로드맵의 틀

- 혁신 요건 분석

- 규제 주도의 제품 개발

- 성능 향상 기회

- 지속가능성 및 바이오 솔루션

- 프리미엄 제품 라인 확장

- 지속가능성 및 바이오 솔루션 로드맵

- 단기적인 지속가능경영 실시 계획(2025-2027년)

- 중기 이행 전략(2027-2035년)

- 장기 비전 및 탄소 중립(2035-2050년)

- 고성능 선박 엔진 용도

- 바이오 베이스 및 지속 가능한 선박용 윤활유

- 전략적 시사

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획 및 자금 조달

- 프리미엄 포지셔닝 전략

- 전략적 OEM 파트너십 기회

- 기술기준 및 인증요건

- 전략적 시장 기회

제5장 엔진 오일 유통의 현상

- 주요 유통 채널

- 채널 구조

- 유통에 있어서 주요 기업

- 유통 채널의 경제성

- 유통의 동향

- 유통에 있어서 과제

- 기회

제6장 시장 추계 및 예측 : 수운별(2021-2034년)

- 주요 동향

- 외항

- 레저

- 화물 수송

- 여객 수송

- 어업

- 정부기관용

- 내륙

- 레저

- 화물 수송

- 여객 수송

- 어업

- 정부기관용

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 레저

- 화물 수송

- 여객 수송

- 어업

- 정부기관용

제8장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 가솔린

- 디젤

- 전기식

제9장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 엔진별(2021-2034년)

- 주요 동향

- 2스트로크

- 4스트로크

- 전기자동차

제11장 시장 추계 및 예측 : 출력별(2021-2034년)

- 주요 동향

- 저출력

- 중출력

- 고출력

제12장 시장 추계 및 예측 : 이그니션별(2021-2034년)

- 주요 동향

- 전기자동차

- 매뉴얼

제13장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 헝가리

- 그리스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제14장 기업 프로파일

- 세계 기업

- Mercury Marine

- Yamaha Motor Company

- Honda Marine

- Suzuki Marine

- Tohatsu

- 지역 선도기업

- Aquamot

- BRP/Evinrude

- ePropulsion

- Hidea

- Lehr Propane Engines

- Mariner

- OXE Marine

- Parsun

- Powertec Outboards

- Rad Propulsion

- Ray Electric Outboards

- Selva Marine

- Torqeedo

- Volvo Penta

- 신흥 기업 및 업계 변혁 기업

- Aquawatt

- Bixpy

- Candela

- Cox Marine

- Elco Motor Yachts

- Evoy

- Flux Marine

- FPT Neander Motors

- Remigo

- Temo

- Vision Marine Technologies

- Zerojet

The Global Outboard Boats Engine Market was valued at USD 10.3 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 17.6 billion by 2034.

Demand continues to rise as recreational boating and water-based activities gain popularity across coastal and inland regions. Higher consumer spending on leisure equipment, along with expanding marina infrastructure and tourism development, is accelerating the adoption of outboard engines throughout the forecast timeline. The market is also advancing as manufacturers introduce lighter, more fuel-efficient, and lower-emission technologies suitable for both commercial operations and recreational boating. Transitioning toward four-stroke systems and direct fuel-injection designs is strengthening long-term growth, particularly as emission standards continue to tighten. Growing dependence on reliable outboard engines for commercial fishing, small-scale marine transport, and coastal logistics is reinforcing demand for advanced, high-performance models. Rising investments in coastal development, along with expanding artisanal and aquaculture activities, are also enhancing opportunities for engine suppliers and supporting a steady market outlook.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.3 Billion |

| Forecast Value | $17.6 Billion |

| CAGR | 5.9% |

The seagoing segment held a 56% share in 2024 and is expected to grow at a CAGR above 5.9% through 2034. Interest in coastal travel, offshore excursions, and water-sport activities is boosting the utilization of seagoing outboard engines designed for high durability, long-distance travel, and stronger offshore capabilities. Their growing use in marine security operations and commercial transport is further driving adoption due to their fast response and dependable performance.

The leisure segment held a 62% share in 2024 and is projected to grow at a CAGR of 5% from 2025 to 2034. Rising enthusiasm for recreational boating, family outings, and weekend water activities continues to elevate demand for outboard engines across small and mid-sized boats. Higher disposable income, urban lifestyle trends, and expanding participation in marine recreation are fueling sales across lakes, coasts, and river systems.

US Outboard Boats Engine Market held an 86% share and generated USD 3.57 billion in 2024. Recreational boating remains highly active due to strong consumer purchasing power and a rapidly growing marina network. Demand for fishing boats, personal watercraft, and leisure vessels continues to rise across saltwater and freshwater environments. Manufacturers in the US are focusing on technologically enhanced four-stroke and digitally controlled outboard engines that deliver improved fuel economy, lower emissions, and smoother handling.

Major companies in the Global Outboard Boats Engine Market include Brunswick, Oxe Marine, Yamaha, Honda, Suzuki Motor, Cox Powertrain, Parsun Power Machine, Hidea Power, Volvo Penta, and Tohatsu. Companies in the Outboard Boats Engine Market are reinforcing their market position by developing engines with higher fuel efficiency, reduced emissions, and lightweight construction to meet shifting consumer and regulatory expectations. Many firms are investing in digital control systems and advanced diagnostics to elevate performance and simplify maintenance for end users. Strategic collaborations with boat manufacturers help expand distribution networks and secure long-term OEM partnerships. Firms are also enhancing their production capabilities to meet growing demand for four-stroke and high-horsepower engines.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Waterways

- 2.2.3 Application

- 2.2.4 Propulsion

- 2.2.5 Engine

- 2.2.6 Power

- 2.2.7 Ignition

- 2.2.8 Sales channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for recreational fishing & water sports

- 3.2.1.2 Growing popularity of small inflatable & portable boats

- 3.2.1.3 Shift from inboard to outboard engines for versatility

- 3.2.1.4 Expansion of coastal tourism & marine leisure industry

- 3.2.1.5 Demand for lightweight, fuel-efficient propulsion systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent marine emission regulations

- 3.2.2.2 Noise & vibration concerns

- 3.2.2.3 Limited range for electric outboards

- 3.2.2.4 High upfront cost of high-horsepower models

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification & hybrid integration

- 3.2.3.2 Demand for portable outboards in emerging markets

- 3.2.3.3 Growth in eco-tourism & sustainable boating

- 3.2.3.4 Replacement demand from aging fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and disruptions

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current Technologies

- 3.9.1.1 Advanced Fuel Injection Systems

- 3.9.1.2 Corrosion-Resistant Materials for Saltwater Use

- 3.9.1.3 Digital Engine Monitoring & Smart Controls

- 3.9.2 Emerging Technologies

- 3.9.2.1 Electric & Hybrid Outboard Propulsion

- 3.9.2.2 Lightweight Composite Materials

- 3.9.2.3 Modular & Portable Power Units

- 3.9.2.4 Connected Outboards (IoT Integration)

- 3.9.1 Current Technologies

- 3.10 Patent analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Price trends

- 3.12.1 By region

- 3.12.2 By propulsion

- 3.13 Pricing analysis and value chain economics

- 3.13.1 Outboard pricing trends by hp segment

- 3.13.2 Premium pricing strategies in high-hp models

- 3.13.3 Cost structure breakdown

- 3.13.4 Regional price sensitivity

- 3.14 Cost breakdown analysis

- 3.14.1 Component-level cost structure analysis

- 3.14.2 Manufacturing cost drivers and optimization

- 3.14.3 Regional cost variations and competitive implications

- 3.14.4 Cost management strategies and competitive positioning

- 3.15 Use cases

- 3.15.1 Government and Public Safety Applications

- 3.15.2 Commercial Harbor and Port Operations

- 3.15.3 Recreational and Tourism Applications

- 3.15.4 Electrification and Hybrid Integration Applications

- 3.15.5 Alternative Fuel and Sustainable Propulsion Applications

- 3.16 Best-case scenario

- 3.16.1 Accelerated Electrification with Infrastructure Support

- 3.16.2 Sustainable Fuel Integration and Circular Economy

- 3.16.3 Premium Performance and Technology Leadership

- 3.16.4 Global Market Expansion and Emerging Market Development

- 3.16.5 Integrated Sustainability and Performance Excellence

- 3.17 Global trade and import/export analysis

- 3.17.1 Import Dependencies by Region

- 3.17.2 Trade Regulations and Tariff Impact

- 3.18 Sustainability and environmental aspects

- 3.18.1 Reduction of Physical Prototyping and Testing

- 3.18.2 Energy Efficiency Improvements

- 3.18.3 Support for Electrification and Emission Reduction Technologies

- 3.18.4 Lifecycle and E-Waste Management

- 3.18.5 Compliance with Environmental Regulations

- 3.19 Product roadmap framework

- 3.19.1 Innovation Requirements Analysis

- 3.19.2 Regulatory-Driven Product Development

- 3.19.3 Performance Enhancement Opportunities

- 3.19.4 Sustainability and Bio-Based Solutions

- 3.19.5 Premium Product Line Extensions

- 3.20 Sustainability and bio-based solutions roadmap

- 3.20.1 Near-Term Sustainability Implementation (2025-2027)

- 3.20.2 Medium-Term Transition Strategy (2027-2035)

- 3.20.3 Long-Term Vision and Carbon Neutrality (2035-2050)

- 3.21 High-performance marine engine applications

- 3.22 Bio-based and sustainable marine lubricants

- 3.23 Strategic implications

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Premium Positioning Strategies

- 4.8 Strategic OEM Partnership Opportunities

- 4.9 Technical Standards and Certification Requirements

- 4.10 Strategic Market Opportunities

Chapter 5 Landscape of Engine Oil Distribution

- 5.1 Key distribution channels

- 5.2 Channel structure

- 5.3 Key players in distribution

- 5.4 Channel economics

- 5.5 Trends in distribution

- 5.6 Challenges in distribution

- 5.7 Opportunities

Chapter 6 Market Estimates & Forecast, By Waterways, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Seagoing

- 6.2.1 Leisure

- 6.2.2 Transport Of goods

- 6.2.3 Transport Of people

- 6.2.4 Fishing

- 6.2.5 Government use

- 6.3 Inland

- 6.3.1 Leisure

- 6.3.2 Transport Of goods

- 6.3.3 Transport Of people

- 6.3.4 Fishing

- 6.3.5 Government use

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Leisure

- 7.2 Transport Of goods

- 7.3 Transport Of people

- 7.4 Fishing

- 7.5 Government use

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Gasoline

- 8.3 Diesel

- 8.4 Electric

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 2-stroke

- 10.3 4-stroke

- 10.4 Electric

Chapter 11 Market Estimates & Forecast, By Power, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 Low

- 11.3 Mid

- 11.4 High

Chapter 12 Market Estimates & Forecast, By Ignition, 2021 - 2034 ($Bn, Units)

- 12.1 Key trends

- 12.2 Electric

- 12.3 Manual

Chapter 13 Market Estimates & Forecast, By Region, 2021-2034 ($Bn, Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 US

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 UK

- 13.3.2 Germany

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Russia

- 13.3.7 Nordics

- 13.3.8 Hungary

- 13.3.9 Greece

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 ANZ

- 13.4.6 Southeast Asia

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global Players

- 14.1.1 Mercury Marine

- 14.1.2 Yamaha Motor Company

- 14.1.3 Honda Marine

- 14.1.4 Suzuki Marine

- 14.1.5 Tohatsu

- 14.2 Regional Champions

- 14.2.1 Aquamot

- 14.2.2 BRP/Evinrude

- 14.2.3 ePropulsion

- 14.2.4 Hidea

- 14.2.5 Lehr Propane Engines

- 14.2.6 Mariner

- 14.2.7 OXE Marine

- 14.2.8 Parsun

- 14.2.9 Powertec Outboards

- 14.2.10 Rad Propulsion

- 14.2.11 Ray Electric Outboards

- 14.2.12 Selva Marine

- 14.2.13 Torqeedo

- 14.2.14 Volvo Penta

- 14.3 Emerging Players & Disruptors

- 14.3.1 Aquawatt

- 14.3.2 Bixpy

- 14.3.3 Candela

- 14.3.4 Cox Marine

- 14.3.5 Elco Motor Yachts

- 14.3.6 Evoy

- 14.3.7 Flux Marine

- 14.3.8 FPT Neander Motors

- 14.3.9 Remigo

- 14.3.10 Temo

- 14.3.11 Vision Marine Technologies

- 14.3.12 Zerojet