|

시장보고서

상품코드

1885866

초고속 EV 충전 시스템 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Ultra-Fast EV Charging (350kW+) Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

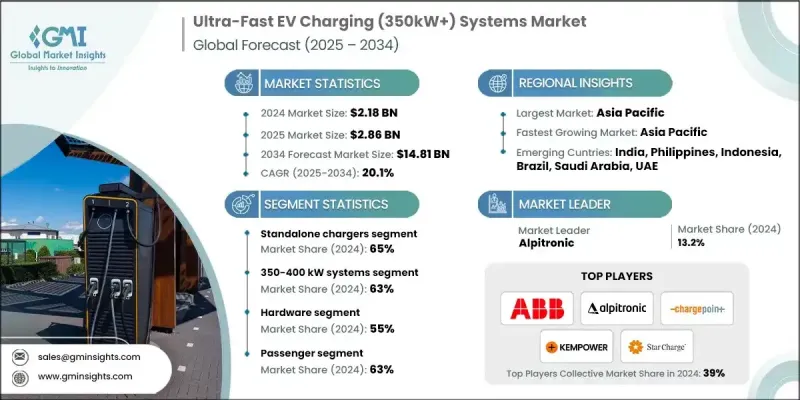

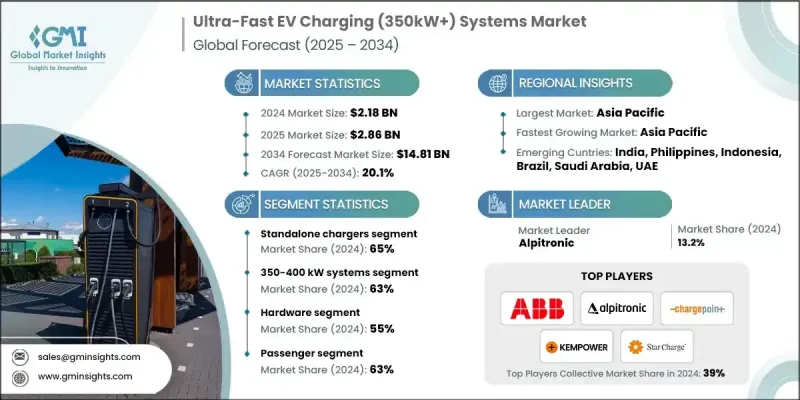

세계의 초고속 EV 충전 시스템(350kW 이상) 시장은 2024년에 21억 8,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 20.1%를 나타낼 것으로 예측되며 148억 1,000만 달러로 성장할 전망입니다.

초고속 전기차 충전기(350kW+)에 대한 수요 급증은 전 세계 전기차 인프라를 재편하고 있습니다. 이러한 고출력 충전기는 호환 차량이 20분 이내에 배터리 용량의 80%까지 충전할 수 있게 하여 대기 시간을 크게 줄이고 전기차 보급을 가속화합니다. 고전압 작동, 확장 가능한 모듈식 설계, 고급 열 관리 기능을 제공하여 승용차 및 상용 전기차 부문 모두에 필수적입니다. 충전기 제조사, 전력 전자 부품 공급업체 및 유틸리티 파트너들은 기술 통합 간소화, 설치 비용 절감, 시스템 신뢰성 향상을 위해 전략적으로 투자하고 있습니다. 코로나19 팬데믹은 정부가 저배출 모빌리티, 지속가능성 및 청정 교통을 강조하며 고출력 충전 네트워크 확장을 위한 인센티브를 도입함에 따라 인프라 투자를 간접적으로 촉진했습니다. 전기차 보급 증가로 상용차와 승용차 모두를 효율적으로 서비스할 수 있는 350kW+ 충전 시스템에 대한 수요가 더욱 증가했습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 21억 8,000만 달러 |

| 예측 가치 | 148억 1,000만 달러 |

| CAGR | 20.1% |

독립형 충전기 부문은 2024년 65%의 점유율을 기록했으며, 2034년까지 연평균 20.5%의 성장률을 보일 것으로 예상됩니다. 독립형 충전기는 배치 유연성, 낮은 설치 복잡성, 공공 및 고속도로 네트워크 적합성으로 시장을 주도합니다. 독립적으로 운영되며, 주유소, 소매 허브, 휴게소에 설치 가능하며 초고속 350kW+ 충전을 제공하여 전기차 사용자들의 급증하는 빠른 충전 수요를 충족시킵니다.

350-400kW 시스템 부문은 2024년 63%의 점유율을 기록했으며, 2025년부터 2034년까지 연평균 20.5%의 성장률을 보일 것으로 예상됩니다. 이 시스템들은 비용 대비 성능 균형과 대부분의 800V 전기차 아키텍처와의 호환성으로 선호됩니다. 20분 이내에 배터리 용량의 70-80%를 재충전할 수 있어 승용차 및 경상용차에 이상적입니다. 광범위한 전기차 호환성으로 전 세계 공공 및 고속도로 충전 네트워크에 채택이 확대되고 있습니다.

중국의 초고속 EV 충전(350kW 이상) 시스템 시장은 40%의 점유율을 차지하며 3억 6,660만 달러의 수익을 창출했습니다. 이 같은 중국 시장의 우위는 대규모 전기차 생산, 정부 지원 인프라 프로그램, 비용 효율적인 제조 생태계 덕분입니다. ‘신에너지차(NEV)’ 프로그램 하의 정책 추진과 충전 인프라에 150억 달러 이상 투자된 것이 주요 도시와 고속도로에 초고속 충전기의 보급을 가속화했습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 승용차 및 상용차 부문의 세계 EV 보급 급증

- 초고속 충전 인프라 구축을 위한 정부 자금 지원 및 인센티브 확대

- 대규모 도입을 위한 OEM 및 충전 네트워크 협력 증가

- 전력 전자기기, 변환기 및 열 관리 기술 발전의 성장

- 대용량 충전 수요를 주도하는 차량 군 전기화 계획 증가

- 업계의 잠재적 위험 및 과제

- 초고속 충전 인프라의 고액의 설비 투자와 설치 비용

- 여러 지역의 제한된 전력망 용량 및 에너지 공급 문제

- 시장 기회

- 초고속 충전기와 에너지 저장 및 재생에너지 통합 증가

- 신흥 및 개발도상국 시장의 초고속 충전 인프라 확산 증가

- 전용 차량 및 물류 충전 허브에 대한 수요 증가

- 모듈형, 멀티 포트, 확장 가능한 충전 시스템 개발 급증

- 인프라 투자를 촉진하는 기업 및 정부의 지속가능성 이니셔티브 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 분석

- 가격 동향

- 지역별

- 컴포넌트별

- 비용 내역 분석

- 지속가능성과 환경영향 분석

- 지속가능한 실천

- 폐기물 감축 전략

- 생산의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 투자 및 자금 조달 분석

- 정부 자금 지원 프로그램

- NEVI 공식 프로그램(50억 달러)

- 유럽연합(EU) 유럽연결시설(CEF)

- 대체 연료 인프라 시설(AFIF)

- 중국의 신에너지차 보조금 제도

- 주 및 지방자치단체의 인센티브

- 민간 투자 동향

- 관민 제휴 모델

- 그린 본드와 지속 가능한 금융

- 인프라 펀드 및 REIT

- 정부 자금 지원 프로그램

- 비즈니스 모델 분석

- CPO 소유 및 운영 모델

- OEM 소유 충전 네트워크

- 유틸리티자가 소유하는 인프라

- 소매 및 상업시설 소유자 소유

- 충전 서비스(CaaS) 모델

- 하이브리드 및 신흥 모델

- 설치 및 시운전 공정

- 설치 전 계획

- 토목 공사 및 현장 준비

- 전기 설비 공사

- 시운전 및 시험

- 전력 레벨별 타임라인 분석

- 설치비용 내역

- 전망과 기회

- 새로운 용도

- 차세대 혁신

- 투자 기회

- 리스크 평가

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 하드웨어

- 파워 모듈

- 케이블 및 커넥터

- 냉각 시스템

- 케이스 및 마운트

- 소프트웨어

- 에너지 관리 시스템

- 결제 및 접근 제어

- 원격 감시 및 분석

- 서비스

- 설치 및 시운전

- 유지보수 및 업그레이드

- 네트워크 관리

제6장 시장 추계 및 예측 : 설비별(2021-2034년)

- 주요 동향

- 독립형 충전기

- 통합 시스템

제7장 시장 추계 및 예측 : 출력별(2021-2034년)

- 주요 동향

- 350-400kW 시스템

- 400-500kW 시스템

- 500kW 초과 시스템

제8장 시장 추계 및 예측 : 구성별(2021-2034년)

- 주요 동향

- 싱글 포트 시스템

- 멀티포트 시스템(2-4포트)

- 모듈형 확장형 시스템

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 공공 충전소

- 상용차 충전 서비스

- 주택 및 개인 충전

- 고속도로 및 장거리 충전 네트워크

제10장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백 자동차

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- 세계적 기업

- ABB

- Alpitronic

- ChargePoint

- Delta

- Enel X

- Exicom Power Solutions

- Huawei

- Kempower

- Phoenix Contact

- StarCharge

- Webasto

- 지역 기업

- BTC Power

- Circontrol

- Compleo Charging Solutions

- EVTEC

- Heliox

- Ingeteam

- Phihong

- SK Signet

- TELD(TGood Electric)

- Tritium DCFC

- 신흥 기업

- Blink Charging

- Designwerk Technologies

- Gravity

- HICI Digital Power Technology

- Nxu

- Qingdao Hardhitter Electric

- Rhombus Energy Solutions(BorgWarner)

- Shijiazhuang Tonhe Electronics

- Zerova(Noodoe EV)

The Global Ultra-Fast EV Charging (350kW+) Systems Market was valued at USD 2.18 billion in 2024 and is estimated to grow at a CAGR of 20.1% to reach USD 14.81 billion by 2034.

The surge in demand for ultra-fast EV chargers (350kW+) is reshaping the electric vehicle infrastructure worldwide. These high-power chargers allow compatible vehicles to reach 80% battery capacity in under 20 minutes, significantly reducing downtime and accelerating EV adoption. They are essential for both passenger and commercial EV segments, offering high-voltage operation, scalable modular designs, and advanced thermal management. Charger manufacturers, power electronics suppliers, and utility partners are investing strategically to simplify technology integration, lower installation costs, and enhance system reliability. The COVID-19 pandemic indirectly boosted infrastructure investments, as governments emphasized low-emission mobility, sustainability, and clean transportation, introducing incentives to expand high-power charging networks. Rising EV adoption has further increased the demand for 350 kW+ charging systems capable of servicing both commercial and passenger vehicles efficiently.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.18 Billion |

| Forecast Value | $14.81 Billion |

| CAGR | 20.1% |

The standalone chargers segment held a 65% share in 2024 and is expected to grow at a CAGR of 20.5% through 2034. Standalone chargers dominate the market due to their deployment flexibility, lower installation complexity, and suitability for public and highway networks. Operating independently, they can be installed across service stations, retail hubs, and rest areas while providing ultra-fast 350 kW+ charging, meeting the growing demand for rapid turnaround among EV users.

The 350-400 kW systems segment captured 63% share in 2024 and is anticipated to grow at a CAGR of 20.5% between 2025 and 2034. These systems are favored for their cost-performance balance and compatibility with most 800 V EV architectures. They can recharge 70-80% of battery capacity in under 20 minutes, making them ideal for passenger and light commercial vehicles. Their broad EV compatibility has driven adoption across public and highway charging networks globally.

China Ultra-Fast EV Charging (350kW+) Systems Market held a 40% share, generating USD 366.6 million. The country's dominance is attributed to its large-scale EV production, government-supported infrastructure programs, and cost-effective manufacturing ecosystem. Policy initiatives under the "New Energy Vehicle (NEV)" program, coupled with investments exceeding USD 15 billion in charging infrastructure, have accelerated the deployment of ultra-fast chargers across major cities and highways.

Key players in the Ultra-Fast EV Charging (350kW+) Systems Market include Siemens, ABB, Alpitronic, Delta, Huawei, ChargePoint, Heliox, Kempower, StarCharge, and Tritium. Market players are investing heavily in R&D to improve charger efficiency, modularity, and thermal management while reducing installation and maintenance costs. Companies are forming strategic partnerships with utility providers, EV manufacturers, and infrastructure developers to expand charging networks and ensure compatibility with diverse EV models. Geographic expansion, particularly in regions with high EV adoption, strengthens market presence. Mergers and acquisitions allow firms to consolidate technology and enhance service capabilities. Companies are also integrating digital platforms for real-time monitoring, predictive maintenance, and user-friendly payment solutions to enhance customer experience.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Installation

- 2.2.3 Power rating

- 2.2.4 Component

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.2.7 Configuration

- 2.3 TAM Analysis, 2026-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in global EV adoption across passenger and commercial segments

- 3.2.1.2 Increase in government funding and infrastructure incentives for ultra-fast charging deployment

- 3.2.1.3 Rise in OEM and charging network collaborations for large-scale rollouts

- 3.2.1.4 Growth in advancements of power electronics, converters, and thermal management technologies

- 3.2.1.5 Increase in fleet electrification initiatives driving high-throughput charging demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital expenditure and installation costs for ultra-fast charging infrastructure

- 3.2.2.2 Limited grid capacity and energy supply challenges in several regions

- 3.2.3 Market opportunities

- 3.2.3.1 Increase in integration of energy storage and renewables with ultra-fast chargers

- 3.2.3.2 Rise in ultra-fast charging deployment across emerging and developing markets

- 3.2.3.3 Growth in demand for dedicated fleet and logistics charging hubs

- 3.2.3.4 Surge in development of modular, multi-port, and scalable charging systems

- 3.2.3.5 Increase in corporate and government sustainability initiatives boosting infrastructure investment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By component

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

- 3.13 Investment and funding analysis

- 3.13.1 Government funding programs

- 3.13.1.1 NEVI formula program ($5 billion)

- 3.13.1.2 EU connecting Europe facility (CEF)

- 3.13.1.3 Alternative fuels infrastructure facility (AFIF)

- 3.13.1.4 China NEV subsidy programs

- 3.13.1.5 State and provincial incentives

- 3.13.2 Private investment trends

- 3.13.3 Public-private partnership models

- 3.13.4 Green bonds and sustainable finance

- 3.13.5 Infrastructure funds and REITs

- 3.13.1 Government funding programs

- 3.14 Business model analysis

- 3.14.1 CPO-owned & operated model

- 3.14.2 OEM-owned charging networks

- 3.14.3 Utility-owned infrastructure

- 3.14.4 Retail & commercial host-owned

- 3.14.5 Charging-as-a-service (CaaS) model

- 3.14.6 Hybrid & emerging models

- 3.15 Installation & commissioning process

- 3.15.1 Pre-installation planning

- 3.15.2 Civil works & site preparation

- 3.15.3 Electrical installation

- 3.15.4 Commissioning & testing

- 3.15.5 Timeline analysis by power level

- 3.15.6 Installation cost breakdown

- 3.16 Future outlook & opportunities

- 3.16.1 Emerging Applications

- 3.16.2 Next-Generation Innovations

- 3.16.3 Investment Opportunities

- 3.16.4 Risk Assessment

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LAMEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Power modules

- 5.2.2 Cables & connectors

- 5.2.3 Cooling systems

- 5.2.4 Enclosures & mounts

- 5.3 Software

- 5.3.1 Energy management systems

- 5.3.2 Payment & access control

- 5.3.3 Remote monitoring & analytics

- 5.4 Services

- 5.4.1 Installation & commissioning

- 5.4.2 Maintenance & upgrades

- 5.4.3 Network management

Chapter 6 Market Estimates & Forecast, By Installation, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Standalone chargers

- 6.3 Integrated systems

Chapter 7 Market Estimates & Forecast, By Power rating, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 350-400 kW systems

- 7.3 400-500 kW systems

- 7.4 500+ kW systems

Chapter 8 Market Estimates & Forecast, By Configuration, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Single-port systems

- 8.3 Multi-port systems (2-4 ports)

- 8.4 Modular expandable systems

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Public charging stations

- 9.3 Commercial fleet charging

- 9.4 Residential / private charging

- 9.5 Highway and long-distance charging networks

Chapter 10 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Passenger vehicles

- 10.2.1 Hatchbacks

- 10.2.2 Sedans

- 10.2.3 SUV

- 10.3 Commercial vehicles

- 10.3.1 Light commercial vehicles (LCV)

- 10.3.2 Medium commercial vehicles (MCV)

- 10.3.3 Heavy commercial vehicles (HCV)

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 ABB

- 12.1.2 Alpitronic

- 12.1.3 ChargePoint

- 12.1.4 Delta

- 12.1.5 Enel X

- 12.1.6 Exicom Power Solutions

- 12.1.7 Huawei

- 12.1.8 Kempower

- 12.1.9 Phoenix Contact

- 12.1.10 StarCharge

- 12.1.11 Webasto

- 12.2 Regional Players

- 12.2.1 BTC Power

- 12.2.2 Circontrol

- 12.2.3 Compleo Charging Solutions

- 12.2.4 EVTEC

- 12.2.5 Heliox

- 12.2.6 Ingeteam

- 12.2.7 Phihong

- 12.2.8 SK Signet

- 12.2.9 TELD (TGood Electric)

- 12.2.10 Tritium DCFC

- 12.3 Emerging Players

- 12.3.1 Blink Charging

- 12.3.2 Designwerk Technologies

- 12.3.3 Gravity

- 12.3.4 HICI Digital Power Technology

- 12.3.5 Nxu

- 12.3.6 Qingdao Hardhitter Electric

- 12.3.7 Rhombus Energy Solutions (BorgWarner)

- 12.3.8 Shijiazhuang Tonhe Electronics

- 12.3.9 Zerova (Noodoe EV)