|

시장보고서

상품코드

1885873

스마트 EV 충전 네트워크 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Smart EV Charging Networks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

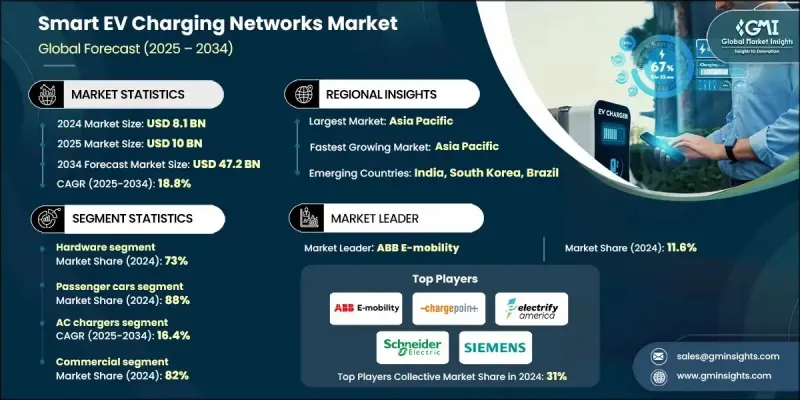

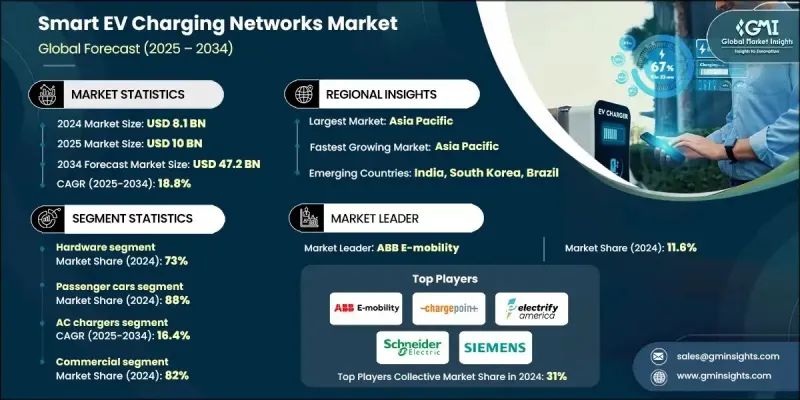

세계의 스마트 EV 충전 네트워크 시장은 2024년 81억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 18.8%를 나타낼 것으로 예측되며 472억 달러로 성장할 전망입니다.

시장 확장은 전기 모빌리티의 가속화와 디지털로 조정된 충전 생태계의 채택과 밀접한 관련이 있습니다. 네트워크 운영사들은 충전기 성능 향상, 전력망 상호작용 강화, 전반적인 사용자 경험 개선을 위해 지능형 부하 관리 시스템, 실시간 분석, 클라우드 기반 플랫폼을 점점 더 통합하고 있습니다. 교통 수단의 전기화가 확대됨에 따라 최적화된 충전 기능과 효율적인 에너지 공급에 대한 수요가 증가하고 있습니다. 전력망 현대화와 차량 군 전기화는 스마트 충전 네트워크 전반에 걸쳐 인프라 우선순위를 계속해서 형성하고 있습니다. 이러한 시스템은 실시간 전력 균형 조정, 수요 대응, 저장 장치 최적화, 재생 에너지 통합을 용이하게 합니다. 인공지능 기반 기술(고급 에너지 오케스트레이션, 사이버 보안 계층, V2G(차량-전력망) 기능, 예측 운영 등)은 확장 가능하고 탄력적인 생태계를 지원합니다. 유틸리티 기업, 충전 네트워크 공급업체, 제조업체 간의 협력이 구축 속도를 가속화하는 한편, 표준화된 프로토콜과 로밍 협정은 광범위한 상호운용성을 위한 기반을 마련하고 있습니다. 정책 주도적 투자와 결합된 예측 분석은 충전 및 에너지 관리 부문의 새로운 서비스 모델을 촉진할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 81억 달러 |

| 예측 가치 | 472억 달러 |

| CAGR | 18.8% |

하드웨어 부문은 2024년 73%의 점유율을 차지했습니다. 대규모 충전 포트 수요가 지속적으로 증가함에 따라 물리적 인프라 확장은 여전히 네트워크 확장의 핵심 요소입니다. 저출력 AC 충전기가 필요한 장치의 대부분을 차지하며, 예상되는 2,800만 대의 충전기 중 약 2,680만 대가 주거용, 직장용, 커뮤니티 충전 수요를 충족시킬 것으로 전망됩니다.

승용차 부문은 2024년 88%의 점유율을 차지했으며, 이는 전기차 소비자 채택 증가로 인해 가정용 및 공공 충전 수요가 모두 증가함에 따른 결과입니다. 주거용 AC 충전 및 직장 내 설치는 일상적인 통근 수요를 지원하며, 스마트 충전 플랫폼을 통해 사용자는 소비 관리, 충전 세션 예약, 에너지 비용 절감 및 지역 전력망 부담 완화를 위한 동적 가격 책정 기능 활용이 가능합니다.

미국의 스마트 EV 충전 네트워크 시장은 89.7%의 점유율을 차지했으며, 2024년에는 8억 5,690만 달러 시장 규모를 창출했습니다. 주 및 연방 차원의 강력한 정책 지원이 계속해서 채택을 촉진하고 있으며, 국가 차원의 입법으로 충전 인프라 확장과 전력망 용량 증강을 위한 상당한 자원이 배정되고 있습니다. 전기차 판매 증가로 공공 및 사설 장소 전반에 걸친 광범위한 충전 인프라 필요성이 더욱 부각되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전기차 보급 증가 및 충전 인프라 구축 가속화

- 스마트 그리드 연동 충전으로의 전환 확대

- 공공 및 준공공 충전 인프라 구축을 위한 정부 인센티브

- 업계의 잠재적 위험 및 과제

- 높은 인프라 설치 비용 및 복잡한 전력망 통합

- 충전기, OCPP 표준 및 청구 시스템 간 상호운용성 격차

- 시장 기회

- AI 기반 충전 최적화 및 예측 부하 관리 성장

- 로밍 네트워크 및 사업자 간 충전 상호운용성에 대한 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 비용 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 탄소발자국 평가

- 순환형 경제에의 통합

- 전자폐기물 관리 요건

- 그린 제조 이니셔티브

- 원재료 및 중요 부품의 의존도 분석

- 탄화규소(SiC) 및 질화갈륨(GaN)공급 전망

- 구리, 희토류 자석, 프린트 기판에의 의존도

- 가격 변동 예측(2025-2034년)

- 리사이클 및 세컨드 라이프 활용의 기회

- 고객 구매 행동과 조달 동향

- CPO 대 차량 대 소매 대 유틸리티 구매자 부문

- 의사결정 기준 순위(총소유비용, 가동률, 상호운용성, 브랜드)

- 턴키 솔루션과 프레임워크 계약으로의 전환

- 로밍 허브와 플랫폼의 정착성의 영향

- 채널 및 유통 전략 분석

- 직접 판매 루트 vs. 유통업체 루트 vs. 전기 도매업체 루트

- 시스템 통합자 및 EPC 파트너의 상승

- 온라인 구성 툴과 전자상거래의 침투

- 지역별 채널 우위성

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 하드웨어

- 교류 충전기(레벨1/레벨2)

- 직류 급속 충전기(50kW)

- DC 초급속 충전기(=150kW)

- 충전 포인트/충전소(실내/실외)

- 소프트웨어

- 충전 포인트 관리 시스템(CPMS)

- 에너지 관리 및 부하 분산 소프트웨어

- 결제, 청구 및 로밍 플랫폼

- 원격 측정, OTA, 펌웨어 및 사이버 보안

- 모빌리티 앱(예약, 경로 안내)

- 서비스

- 설치 및 시운전

- 운용 및 보수(O&M)/관리 서비스

- 사이트 설계 및 계통 연계 서비스

- 차량 및 사이트 최적화(컨설팅)

- 서비스로 충전(CaaS) 및 구독

제6장 시장 추계 및 예측 : 충전기별(2021-2034년)

- 주요 동향

- 교류 충전기

- 저속(=3.7 kW)

- 준고속(3.7-22kW)

- 고속(단상/삼상 레벨2)

- 직류 충전기

- 고속 DC(25-150kW)

- 초고속 DC(=150kW)

- 메가와트 충전(대형 차량용)

제7장 시장 추계 및 예측 : 도입 형태별(2021-2034년)

- 주요 동향

- 주택용

- 상업용

제8장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 말레이시아

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 충전 네트워크 운영사(CPO)

- Blink Charging

- ChargePoint

- EnBW

- EVgo

- Fastned

- IONITY

- Mercedes-Benz

- Rivian

- Shell

- Tesla

- Volkswagen

- BP Pulse

- Electrify America

- EVBox

- Schneider Electric

- 충전 하드웨어 및 인프라 제조사

- ABB E-mobility

- BYD

- Delta Electronics

- Eaton

- FreeWire Technologies

- Kempower

- Siemens

- StarCharge

- Tritium

- Wallbox

- 소프트웨어 플랫폼 및 네트워크 관리

- Ampeco

- Gireve

- Hubject

- Monta

- 에너지 유틸리티, 통합 충전 공급자

- Ample

- E.ON

- Enel(Enel X Way)

- Momentum Dynamics

The Global Smart EV Charging Networks Market was valued at USD 8.1 billion in 2024 and is estimated to grow at a CAGR of 18.8% to reach USD 47.2 billion by 2034.

Market expansion is closely linked to the acceleration of electric mobility and the adoption of digitally coordinated charging ecosystems. Network operators are increasingly integrating intelligent load management systems, real-time analytics, and cloud-driven platforms to enhance charger performance, strengthen grid interaction, and improve overall user experience. As transportation electrification grows, demand is rising for optimized charging capabilities and streamlined energy delivery. Grid modernization and fleet electrification continue to shape infrastructure priorities across smart charging networks. These systems facilitate real-time power balancing, demand response, storage optimization, and renewable energy integration. Technologies enabled by artificial intelligence, such as advanced energy orchestration, cybersecurity layers, vehicle-to-grid functions, and predictive operations support scalable and resilient ecosystems. Collaboration among utilities, charging network providers, and manufacturers is accelerating deployment, while standardized protocols and roaming agreements are paving the way for broader interoperability. Predictive analytics, combined with policy-driven investment, is expected to spur new service models in charging and energy management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $47.2 Billion |

| CAGR | 18.8% |

The hardware segment held 73% share in 2024. Physical infrastructure remains fundamental to network expansion, as the projected need for large numbers of charging ports continues to rise. Lower-powered AC chargers make up the majority of required units, with approximately 26.8 million of the anticipated 28 million chargers expected to serve residential, workplace, and community charging needs.

The passenger vehicles segment held an 88% share in 2024, fueled by increasing consumer adoption of electric cars, driving demand for both home-based and public charging. Residential AC charging and workplace installations support day-to-day commuting needs, while smart charging platforms allow users to manage consumption, schedule charging sessions, and utilize dynamic pricing features that reduce energy costs and alleviate stress on local grids.

United States Smart EV Charging Networks Market held a 89.7% share, generating USD 856.9 million in 2024. Strong policy support at both state and federal levels continues to propel adoption, with national legislation allocating substantial resources toward expanding charging infrastructure and enhancing grid capacity. Rising EV sales are reinforcing the need for widespread charging availability across public and private locations.

Key companies in the Smart EV Charging Networks Market include ABB E-mobility, EVBox, BP Pulse, ChargePoint, Delta Electronics, Electrify America, EVgo, Schneider Electric, Siemens eMobility, and Shell. Companies in the Smart EV Charging Networks Market are strengthening their foothold through strategic investments in interoperability, advanced power management, and expanded infrastructure deployment. Many firms are adopting open standards to improve compatibility across networks and ensure seamless user access. Partnerships with utilities and automakers are becoming central to scaling grid-connected solutions and accelerating charger rollout. Businesses are also integrating AI-powered analytics to optimize charger performance, forecast demand, and improve energy efficiency. Enhanced cybersecurity, load-balancing capabilities, and vehicle-to-grid technologies are being prioritized to meet regulatory expectations and support grid stability.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Charger

- 2.2.4 Deployment

- 2.2.5 Vehicle

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising EV adoption and accelerated charging infrastructure rollout

- 3.2.1.2 Growing shift toward smart, grid-interactive charging

- 3.2.1.3 Government incentives for public and semi-public charging deployments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure installation cost & complex grid integration

- 3.2.2.2 Interoperability gaps across chargers, OCPP standards & billing systems

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of AI-enabled charging optimization & predictive load management

- 3.2.3.2 Rising demand for roaming networks & cross-operator charging interoperability

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability & environmental aspects

- 3.12.1 Carbon footprint assessment

- 3.12.2 Circular economy integration

- 3.12.3 E-waste management requirements

- 3.12.4 Green manufacturing initiatives

- 3.13 Raw material and critical component dependency analysis

- 3.13.1 Silicon carbide (SiC) and gallium nitride (GaN) supply outlook

- 3.13.2 Copper, rare-earth magnets, and PCB dependency

- 3.13.3 Price volatility forecast 2025-2034

- 3.13.4 Recycling and second-life opportunities

- 3.14 Customer buying behavior and procurement trends

- 3.14.1 CPO vs. fleet vs. retail vs. utility buyer segments

- 3.14.2 Decision criteria ranking (TCO, uptime, interoperability, brand)

- 3.14.3 Shift toward turnkey solutions and framework agreements

- 3.14.4 Influence of roaming hubs and platform stickiness

- 3.15 Channel and distribution strategy analysis

- 3.15.1 Direct sales vs. distributor vs. electrical wholesaler routes

- 3.15.2 Rise of system integrators and EPC partners

- 3.15.3 Online configurators and e-commerce penetration

- 3.15.4 Regional channel dominance

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 AC chargers (Level 1 / Level 2)

- 5.2.2 DC fast chargers (50 kW)

- 5.2.3 DC ultra-fast chargers (=150 kW)

- 5.2.4 Charge points / charging stations (indoor/outdoor)

- 5.3 Software

- 5.3.1 Charge point management systems (CPMS)

- 5.3.2 Energy management & load-balancing software

- 5.3.3 Payment, billing & roaming platforms

- 5.3.4 Telemetry, OTA, firmware & cybersecurity

- 5.3.5 Mobility apps (reservation, routing)

- 5.4 Services

- 5.4.1 Installation & commissioning

- 5.4.2 Operation & maintenance (O&M) / managed services

- 5.4.3 Site design & grid connection services

- 5.4.4 Fleet & site optimization (consulting)

- 5.4.5 Charging-as-a-Service (CaaS) and subscriptions

Chapter 6 Market Estimates & Forecast, By Charger, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 AC Chargers

- 6.2.1 Slow (=3.7 kW)

- 6.2.2 Semi-fast (3.7-22 kW)

- 6.2.3 Fast (single-phase / three-phase Level 2)

- 6.3 DC Chargers

- 6.3.1 Fast DC (25-150 kW)

- 6.3.2 Ultra-fast DC (=150 kW)

- 6.3.3 Megawatt charging (for heavy vehicles)

Chapter 7 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger Cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCV)

- 8.3.2 Medium commercial vehicles (MCV)

- 8.3.3 Heavy commercial vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.4.8 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Charging Network Operators (CPOs)

- 10.1.1 Blink Charging

- 10.1.2 ChargePoint

- 10.1.3 EnBW

- 10.1.4 EVgo

- 10.1.5 Fastned

- 10.1.6 IONITY

- 10.1.7 Mercedes-Benz

- 10.1.8 Rivian

- 10.1.9 Shell

- 10.1.10 Tesla

- 10.1.11 Volkswagen

- 10.1.12 BP Pulse

- 10.1.13 Electrify America

- 10.1.14 EVBox

- 10.1.15 Schneider Electric

- 10.2 Charging Hardware & Infrastructure Manufacturers

- 10.2.1 ABB E-mobility

- 10.2.2 BYD

- 10.2.3 Delta Electronics

- 10.2.4 Eaton

- 10.2.5 FreeWire Technologies

- 10.2.6 Kempower

- 10.2.7 Siemens

- 10.2.8 StarCharge

- 10.2.9 Tritium

- 10.2.10 Wallbox

- 10.3 Software Platforms & Network Management

- 10.3.1 Ampeco

- 10.3.2 Gireve

- 10.3.3 Hubject

- 10.3.4 Monta

- 10.4 Energy Utilities, Integrated Charging Providers

- 10.4.1 Ample

- 10.4.2 E.ON

- 10.4.3 Enel (Enel X Way)

- 10.4.4 Momentum Dynamics