|

시장보고서

상품코드

1936490

정밀 농업용 드론 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Precision Agriculture Drone Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

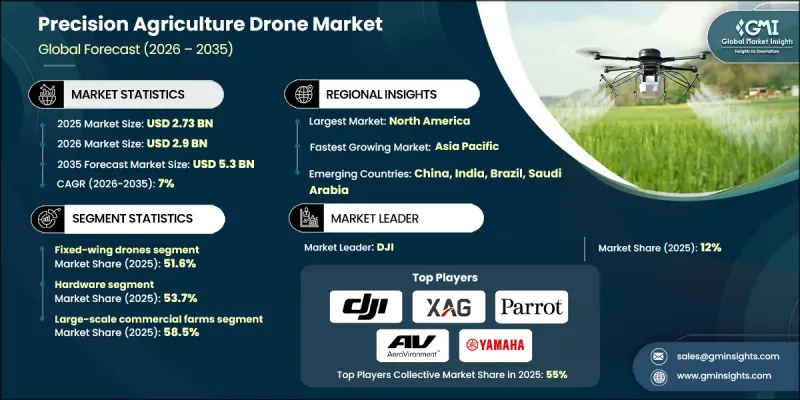

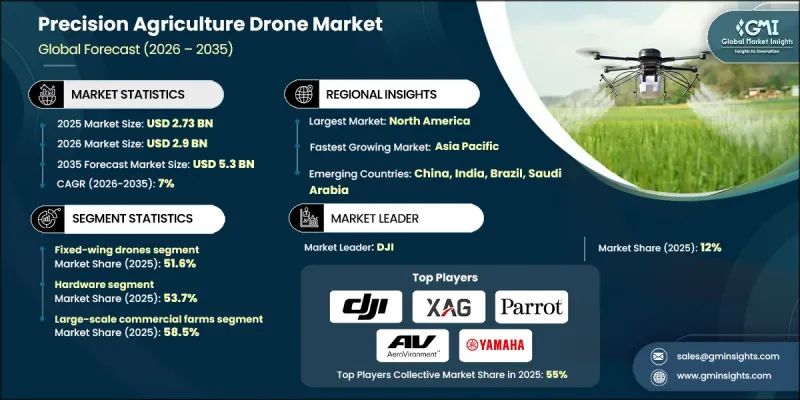

세계의 정밀 농업용 드론 시장은 2025년에 27억 3,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7%로 성장할 전망이며, 53억 달러에 이를 것으로 예측됩니다.

시장 성장은 작물의 수명주기 관리 및 수율 최적화에 대한 관심이 높아지고 현대적인 농장에서 운영 효율성 향상의 필요성에 의해 견인되고 있습니다. 생산자가 실시간 지식과 정확한 현장 평가를 요구하는 가운데 고급 공중 모니터링 및 살포 솔루션에 대한 수요가 증가하고 있습니다. 주요 제조업체 간 전략적 제휴 및 통합 활동 증가가 업계의 기세를 더욱 뒷받침하고 있으며, 이로써 혁신이 가속화되고 솔루션의 제공 범위가 확대되고 있습니다. 확립된 드론 개발 기업과 농업 인텔리전스 제공업체의 협력 강화로 기술 능력이 향상되고 업계 전반의 제품 포트폴리오가 확대되고 있습니다. 기존의 작물 검사 방법은 대규모 농업 경영에서 비효율로 간주되는 경향이 강해지고 자동화된 드론 기반 시스템으로의 전환이 진행되고 있습니다. 연결성, 인공지능(AI) 구동형 분석, 클라우드 대응 데이터 처리의 진보에 의해 의사 결정의 정밀도가 향상되는 동시에, 농가의 투입 자재 낭비 삭감 및 종합적인 생산성 향상에 공헌하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 27억 3,000만 달러 |

| 예측 금액 | 53억 달러 |

| CAGR | 7% |

2025년 하드웨어 부문은 53.7%의 점유율을 차지하여, 15억 달러를 창출했습니다. 고급 센서, 긴 수명 전원 시스템, 경량 구조 설계 등의 핵심 하드웨어 구성 요소는 정밀 농업 작업에 필요한 기본 성능과 적재 용량을 제공합니다. 향상된 포지셔닝 기술은 내비게이션 정확도 및 운영 신뢰성을 향상시킵니다. 하드웨어 부문의 이점은 데이터 중심의 농업 실천에 따른 자동화된 매핑, 모니터링 및 용도 활동을 지원하는 견고한 물리적 인프라에 대한 산업 의존도를 반영합니다.

대규모 상업 농장 부문은 2025년 58.5%의 점유율을 차지했습니다. 이 분야의 도입은 광대한 농지를 효율적으로 관리하면서 노동력을 최소화할 필요성에 의해 추진되고 있습니다. 이러한 사업은 광대하고 연속적인 농업지역 전체에서 신속한 농장 평가, 자동화된 데이터 수집, 일관된 살포 프로세스를 실현하는 드론 솔루션이 우선되어 고성능 정밀 농업용 드론 시스템에 대한 강한 수요를 지원하고 있습니다.

미국의 정밀 농업용 드론 시장은 2025년 75.6%의 점유율을 차지했습니다. 시장의 주도적 지위는 조기 기술 도입, 유리한 규제 환경, 대규모 농업 기업에서 드론 기반 모니터링의 광범위한 활용에 의해 지원됩니다. 농업 경영자가 광대한 제작 면적에 있어서의 효율성 향상, 비용 관리, 생산성 향상을 도모하는 가운데, 자동화된 농장 관리 및 데이터 구동형 투입 자재 최적화에 중점이, 계속해서 수요를 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 수동 작물 조사에서 자동화된 작물 조사로의 전환

- AI 및 엣지 컴퓨팅의 보급

- 정부 보조금과 '드론 샤크티'

- 업계의 잠재적 위험 및 과제

- 고급 페이로드에 대한 높은 초기 설비 투자(CAPEX)

- 인정 드론 조종사의 부족

- 기회

- AI를 활용한 처방 분석

- 구독형 '서비스로서의 데이터'

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증 기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품별(2022-2035년)

- 고정날개 드론

- 회전날개 드론

- 하이브리드 드론

제6장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

- 하드웨어

- 소프트웨어

- 서비스

제7장 시장 추계 및 예측 : 농장 규모별(2022-2035년)

- 대규모 상업 농장

- 중소규모 농장

제8장 시장 추계 및 예측 : 시스템별(2022-2035년)

- 내장형

- 진동 분석기

- 진동계

제9장 시장 추계 및 예측 : 용도별(2022-2035년)

- 필드 매핑

- 가변율 시비

- 작물 정찰

- 기타

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 3D Robotics

- AeroVironment, Inc.

- AGCO Corporation

- AgEagle Aerial Systems

- Agribotix

- Delair

- DJI

- DroneDeploy

- Parrot

- PrecisionHawk

- Quantum Systems

- senseFly

- Sentera

- Skeycatch

- Yamaha Motor Co., Ltd.

The Global Precision Agriculture Drone Market was valued at USD 2.73 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 5.3 billion by 2035.

Market growth is driven by increasing awareness around crop lifecycle management, yield optimization, and the need for higher operational efficiency across modern farms. Demand for advanced aerial monitoring and spraying solutions is rising as growers seek real-time insights and accurate field assessments. Industry momentum is further supported by an increase in strategic collaborations and consolidation activities among leading manufacturers, which has accelerated innovation and broadened solution offerings. The strengthening market presence of established drone developers, combined with agricultural intelligence providers, has enhanced technological capabilities and expanded product portfolios across the sector. Traditional crop inspection methods are increasingly viewed as inefficient for large-scale farming operations, prompting a shift toward automated drone-based systems. Advances in connectivity, artificial intelligence-driven analytics, and cloud-enabled data processing are improving decision-making accuracy while helping farmers reduce input waste and improve overall productivity.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.73 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 7% |

In 2025, the hardware segment accounted for 53.7% share, generating USD 1.5 billion. Core hardware components, including advanced sensors, extended-life power systems, and lightweight structural designs, provide the essential performance and payload capacity required for precision farming tasks. Enhanced positioning technologies are improving navigation accuracy and operational reliability. The dominance of the hardware segment reflects the industry's dependence on robust physical infrastructure to support automated mapping, monitoring, and application activities aligned with data-driven agricultural practices.

The large-scale commercial farms segment held 58.5% share in 2025. Adoption within this segment is driven by the need to manage extensive farmland efficiently while minimizing labor requirements. These operations prioritize drone solutions for rapid field assessment, automated data collection, and consistent application processes across large and continuous agricultural areas, reinforcing strong demand for high-performance precision drone systems.

United States Precision Agriculture Drone Market held 75.6% share in 2025. Market leadership is supported by early technology adoption, a favorable regulatory environment, and widespread utilization of drone-based monitoring across large farming enterprises. Emphasis on automated farm management and data-driven input optimization continues to drive demand as agricultural operators seek to improve efficiency, control costs, and enhance productivity across extensive crop areas.

Key companies operating in the Global Precision Agriculture Drone Market include DJI, PrecisionHawk, Parrot, AeroVironment, Inc., AGCO Corporation, AgEagle Aerial Systems, DroneDeploy, Yamaha Motor Co., Ltd., senseFly, Sentera, Quantum Systems, Delair, 3D Robotics, Agribotix, and Skeycatch. Companies in the precision agriculture drone market are reinforcing their competitive position through technology innovation, strategic partnerships, and targeted acquisitions. Leading players are investing in research and development to enhance flight endurance, data accuracy, and analytics capabilities. Many are expanding integrated software and hardware ecosystems to deliver end-to-end farming solutions. Firms are also focusing on geographic expansion and collaborations with agritech providers to strengthen distribution networks. Customization of drone platforms for specific crop types and farming scales, along with improved after-sales support and training services, is helping companies build long-term customer relationships and secure sustained market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Monitoring Process

- 2.2.4 Application

- 2.2.5 System

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift from manual to automated crop scouting

- 3.2.1.2 Proliferation of AI & Edge Computing

- 3.2.1.3 Government Subsidies & "Drone Shakti"

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial CAPEX for advanced payloads

- 3.2.2.2 Shortage of certified drone pilots

- 3.2.3 Opportunities

- 3.2.3.1 AI-Powered prescriptive analytics

- 3.2.3.2 Subscription-based "Data-as-a-Service"

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Fixed-wing Drones

- 5.3 Rotary-wing Drones

- 5.4 Hybrid Drones

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By Farm Size, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Large-scale Commercial Farms

- 7.3 Small and Medium Farms

Chapter 8 Market Estimates and Forecast, By System, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Embedded

- 8.3 Vibration Analyzers

- 8.4 Vibration Meter

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Field mapping

- 9.3 Variable rate application

- 9.4 Crop Scouting

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3D Robotics

- 11.2 AeroVironment, Inc.

- 11.3 AGCO Corporation

- 11.4 AgEagle Aerial Systems

- 11.5 Agribotix

- 11.6 Delair

- 11.7 DJI

- 11.8 DroneDeploy

- 11.9 Parrot

- 11.10 PrecisionHawk

- 11.11 Quantum Systems

- 11.12 senseFly

- 11.13 Sentera

- 11.14 Skeycatch

- 11.15 Yamaha Motor Co., Ltd.