|

시장보고서

상품코드

2038472

버티포트 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Vertiports Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

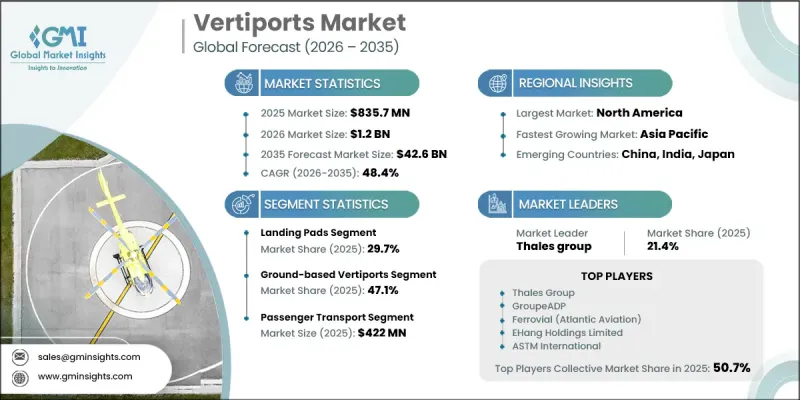

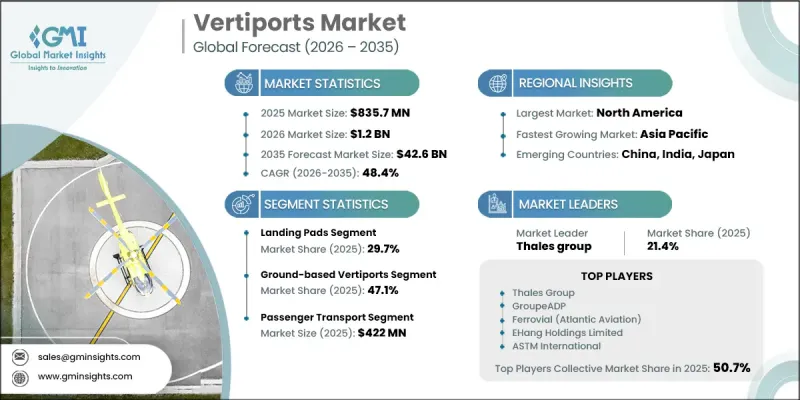

세계의 버티포트 시장은 2025년에 8억 3,570만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 48.4%로 성장할 전망이며, 426억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 첨단 항공 모빌리티 인프라에 대한 투자 증가와 도시 교통의 틀을 바꾸고 있는 전기 수직이착륙기(eVTOL)의 도입 확대에 의해 주도되고 있습니다. 이해관계자들이 승객과 화물의 원활한 이동을 지원하는 상호 연결된 교통 네트워크 구축에 초점을 맞추고 있는 가운데, 버티포트를 더 넓은 모빌리티 생태계에 통합하려는 움직임이 개발을 가속화하고 있습니다. 인프라 계획의 지속적인 발전과 효율적이고 시간을 절약할 수 있는 운송 솔루션에 대한 수요 증가와 함께 시장 상황은 더욱 강화되고 있습니다. 또한, 교통 체증 완화와 도시 이동성 효율화에 대한 관심이 높아지면서 차세대 항공 운송 시스템 도입이 가속화되고 있습니다. 그 결과, 버티포트는 미래 교통 생태계의 중요한 구성 요소로 부상하고 있으며, 빠르게 진화하는 도시 환경에서 확장성이 높고 효율적이며 기술적으로 진보된 모빌리티 솔루션을 실현하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 8억 3,570만 달러 |

| 예측 시장 규모 | 426억 달러 |

| CAGR | 48.4% |

시장의 성장은 밸류체인 전반의 협력 강화로 인해 더욱 촉진되고 있습니다. 인프라 개발자, 항공기 제조업체, 도시 계획 당국이 각자의 역량을 통합하고, 높은 성장 기회를 찾아내어 개발을 가속화하고 있습니다. 전략적 파트너십을 통해 프로젝트 실행을 가속화하고 첨단 안전 시스템과 효율적인 교통 관리 솔루션을 갖춘 첨단 시설의 개발을 촉진하고 있습니다. 승객 중심의 인프라 설계에 대한 투자가 증가하고 있으며, 이는 운영 효율성과 사용자 경험의 향상으로 이어지고 있습니다. 동시에 안전하고 표준화된 운영을 지원하기 위한 규제 프레임워크가 진화하고 있으며, 이는 투자자의 신뢰를 높이고 장기적인 시장 발전을 가능하게 하고 있습니다. 기술 혁신, 협업 생태계, 그리고 지원적인 정책 환경의 조합은 지속적인 시장 확대를 위한 탄탄한 기반을 구축하고 있습니다.

2025년 랜딩 패드(착륙 패드) 부문은 항공기 운항을 지원하는 근본적인 역할로 인해 29.7%의 점유율을 차지했으며, 선두 자리를 지켰습니다. 이러한 구성 요소는 효율적인 처리 시간을 보장하고 운항 안전 기준을 유지하는 데 필수적입니다. 버티포트 인프라에 대한 통합은 연결성 향상과 운영 효율성 향상에 기여하며, 여객과 화물 이동을 모두 지원합니다. 첨단 항공 모빌리티 시스템의 도입이 확대됨에 따라 잘 설계된 착륙 인프라에 대한 수요가 증가하고 있으며, 이는 전체 시장 성장에 있어 이 부문의 중요성을 더욱 높이고 있습니다. 설계 및 운영 효율성의 지속적인 개선은 업계에서 이 부문의 입지를 더욱 공고히 하고 있습니다.

지상형 버티포트 부문은 운영 유연성과 도입 용이성을 바탕으로 2025년 47.1%의 점유율을 차지했습니다. 이 카테고리는 건설의 복잡성이 상대적으로 낮고 기존 인프라 네트워크와 효율적으로 통합할 수 있다는 장점이 있습니다. 확장성과 증가하는 교통량에 대응할 수 있는 능력으로 인해 첨단 모빌리티 시스템의 초기 도입 단계에서 선호되는 선택이 되고 있습니다. 지상 시설은 여객 및 물류 운영을 지원하여 안정적이고 효율적인 서비스 제공을 보장하는 데 있어 매우 중요한 역할을 합니다. 도시형 항공 모빌리티에 대한 수요가 지속적으로 증가함에 따라 이 부문은 강력한 성장세를 유지할 것으로 예측됩니다.

북미의 버티포트 시장은 2025년 38.5%의 점유율을 차지했으며, 이는 규제 발전과 대규모 투자에 힘입어 이 지역의 강력한 보급을 반영하고 있습니다. 이 지역에서는 첨단 모빌리티 솔루션에 대한 관심이 높아지면서 인프라 계획과 실행이 가속화되고 있습니다. 운영 기준과 안전 가이드라인을 확립하려는 정부의 이니셔티브는 시장 성장에 유리한 환경을 조성하고 있습니다. 민관 양측의 막대한 자금 유입으로 최신 기술을 갖춘 첨단 시설의 개발이 가능해졌습니다. 이러한 요인들이 복합적으로 작용하여 이 지역은 세계 시장에서 선도적인 지위를 확립하고 지속적으로 확장하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 솔루션별(2022-2035년)

제6장 시장 추산 및 예측 : 지역별(2022-2035년)

제7장 시장 추산 및 예측 : 유형별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 시장 추산 및 예측 : 용도별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

AJY 26.06.11The Global Vertiports Market was valued at USD 835.7 million in 2025 and is estimated to grow at a CAGR of 48.4% to reach USD 42.6 billion by 2035.

Market expansion is driven by rising investments in advanced air mobility infrastructure and the increasing deployment of electric vertical takeoff and landing aircraft, which are reshaping urban transportation frameworks. The integration of vertiports into broader mobility ecosystems is accelerating development, as stakeholders focus on building interconnected transit networks that support seamless passenger and cargo movement. Continuous advancements in infrastructure planning, combined with growing demand for efficient and time-saving transport solutions, are strengthening the market outlook. Additionally, increasing emphasis on reducing congestion and enhancing urban mobility efficiency is encouraging the adoption of next-generation air transport systems. As a result, vertiports are emerging as a critical component of future transportation ecosystems, enabling scalable, efficient, and technologically advanced mobility solutions across rapidly evolving urban landscapes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $835.7 Million |

| Forecast Value | $42.6 Billion |

| CAGR | 48.4% |

Market growth is further supported by rising collaboration across the value chain, where infrastructure developers, aircraft manufacturers, and urban planning authorities are aligning their capabilities to identify high-growth opportunities and accelerate deployment. Strategic partnerships enabling faster project execution and facilitating the development of advanced facilities equipped with enhanced safety systems and efficient traffic management solutions. Increasing investments in passenger-focused infrastructure designs are improving operational efficiency and user experience. At the same time, regulatory frameworks are evolving to support safe and standardized operations, which is strengthening investor confidence and enabling long-term market development. The combination of technological innovation, collaborative ecosystems, and supportive policy environments is creating a strong foundation for sustained market expansion.

The landing pads segment accounted for a share of 29.7% in 2025, maintaining its leadership position due to its fundamental role in supporting aircraft operations. These components are essential for ensuring efficient turnaround times and maintaining operational safety standards. Their integration within the vertiport infrastructure contributes to improved connectivity and streamlined operations, supporting both passenger and cargo movement. The increasing deployment of advanced air mobility systems is driving the demand for well-designed landing infrastructure, reinforcing the segment's importance in overall market growth. Continuous enhancements in design and operational efficiency are further strengthening the segment's position within the industry.

The ground-based vertiports segment held a share of 47.1% in 2025, driven by its operational flexibility and ease of deployment. This category benefits from relatively lower construction complexity and the ability to integrate efficiently with existing infrastructure networks. Its scalability and capability to accommodate increasing traffic volumes make it a preferred choice for early-stage deployment of advanced mobility systems. Ground-based facilities play a crucial role in supporting both passenger and logistics operations, ensuring reliable and efficient service delivery. As demand for urban air mobility continues to rise, this segment is expected to maintain strong growth momentum.

North America Vertiports Market accounted for 38.5% share in 2025, reflecting strong regional adoption supported by regulatory developments and substantial investments. The region is witnessing accelerated progress in infrastructure planning and implementation, driven by increasing focus on advanced mobility solutions. Government initiatives aimed at establishing operational standards and safety guidelines are creating a favorable environment for market growth. Significant capital inflows from both public and private sectors are enabling the development of advanced facilities equipped with modern technologies. These factors collectively contribute to the region's leading position and continued expansion within the global market.

Prominent players operating in the Global Vertiports Industry include Aeroauto LLC, Airnova, airsight, Archer Aviation (Infrastructure Division), ASTM International, Bayards Vertiports Solutions, EHang Holdings Limited, eVertiSKY Corp., Ferrovial (Atlantic Aviation), Jaunt Air Mobility (Vertiport Tech), Joby Aviation, Inc., Skyports Infrastructure Limited, SKYSCAPE Co., Ltd., Tavistock (Lilium GmbH), Urban-Air Port, UrbanV S.p.A, Varon Vehicles Corporation, Vports, Altaport Inc., BETA Technologies, Groupe ADP, Skyway Technologies Corp., and Thales Group. Companies operating in the Global Vertiports Market are focusing on strategic initiatives to enhance their competitive positioning and expand their global footprint. Key strategies include forming long-term partnerships with technology providers, infrastructure developers, and mobility solution companies to accelerate deployment capabilities. Organizations are investing heavily in research and development to improve design efficiency, scalability, and operational safety of vertiport infrastructure. Additionally, companies are emphasizing digital integration, including advanced traffic management systems and smart infrastructure solutions, to optimize performance. Expansion into emerging markets, along with the development of standardized and modular infrastructure models, is enabling faster adoption. Firms are also prioritizing sustainability by incorporating energy-efficient systems and environmentally friendly designs, aligning their offerings with evolving regulatory requirements and future mobility trends.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution trends

- 2.2.2 Location trends

- 2.2.3 Type trends

- 2.2.4 Landscape trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization and congestion creating demand for vertiports

- 3.2.1.2 Technological advancements in e-VTOL aircraft framing the rise in vertiports

- 3.2.1.3 Governmental support and regulatory frameworks

- 3.2.1.4 Sustainability and environmental concerns

- 3.2.1.5 Investment and infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory hurdles

- 3.2.2.2 Concerns for safety and air traffic management

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of vertiports with multimodal transport hubs

- 3.2.3.2 Deployment of sustainable and energy-efficient vertiports

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Landing pads

- 5.3 Terminal gates

- 5.4 Ground support equipment

- 5.5 Charging stations

- 5.6 Ground control stations

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Location, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Ground-based Vertiports

- 6.3 Rooftop/Elevated Vertiports

- 6.4 Floating Vertiports

Chapter 7 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Vertihubs

- 7.3 Vertibases

- 7.4 Vertipads

Chapter 8 Market Estimates and Forecast, By Landscape, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Urban vertiports

- 8.3 Regional vertiports

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Passenger Transport

- 9.3 Cargo & Logistics

- 9.4 Emergency & Medical Services

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Thales Group

- 11.1.2 ASTM International

- 11.1.3 EHang Holdings Limited

- 11.1.4 Ferrovial (Atlantic Aviation)

- 11.1.5 Groupe ADP

- 11.1.6 Skyports Infrastructure Limited

- 11.1.7 Joby Aviation, Inc.

- 11.1.8 Archer Aviation (Infrastructure Division)

- 11.1.9 BETA Technologies

- 11.2 Regional key players

- 11.2.1 Tavistock (Lilium GmbH)

- 11.2.2 Urban-Air Port

- 11.2.3 UrbanV S.p.A

- 11.2.4 SKYSCAPE Co., Ltd.

- 11.2.5 Vports

- 11.2.6 Altaport Inc.

- 11.2.7 Skyway Technologies, Corp.

- 11.2.8 Bayards Vertiports Solutions

- 11.2.9 Jaunt Air Mobility (Vertiport Tech)

- 11.3 Niche Players/Disruptors

- 11.3.1 Aeroauto LLC

- 11.3.2 Airnova

- 11.3.3 airsight

- 11.3.4 eVertiSKY Corp.

- 11.3.5 Varon Vehicles Corporation