|

시장보고서

상품코드

2071222

도심 항공 모빌리티 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Urban Air Mobility (UAM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

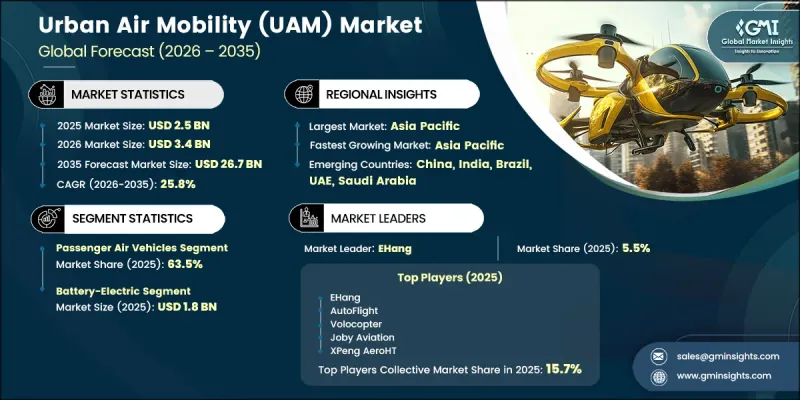

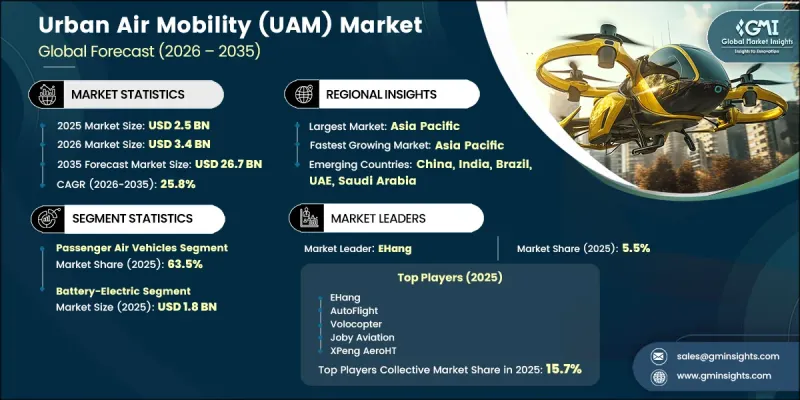

세계 도심 항공 모빌리티 시장은 2025년에 25억 달러 규모가 되어, 25.8%의 연평균 복합 성장률(CAGR)로 확대되어 2035년까지 267억 달러에 이를 것으로 추정되고 있습니다.

첨단 항공 운송 솔루션의 급속한 발전으로 인해 도심 항공 모빌리티 업계 전반에 걸쳐 큰 성장 기회가 생겨나고 있습니다. 교통 정체가 심각한 대도시권에서 더 빠른 대체 교통수단에 대한 수요가 높아짐에 따라, 이동 효율 향상과 소요 시간 단축을 목적으로 한 혁신적인 항공 모빌리티 플랫폼의 도입이 촉진되고 있습니다. 차세대 항공 기술의 발전과 이를 뒷받침하는 규제 체계가 맞물리면서 상용화로 가는 길이 가속화되고 있습니다. 업계 관계자들의 자금 투자 확대와 전략적 제휴는 기술의 성숙과 운영 준비를 뒷받침함으로써 시장 발전을 더욱 공고히 하고 있습니다. 또한, 이 업계는 지속 가능한 교통 솔루션과 환경 부담 저감이 점점 더 중요시되는 추세의 혜택을 받고 있으며, 보다 친환경적인 모빌리티 기술의 도입이 촉진되고 있습니다. 도시 교통 시스템이 지속적으로 발전함에 따라, 이해관계자들은 장기적인 상용화를 뒷받침할 인프라, 차량 개발 및 생태계 통합을 위한 노력에 대한 투자를 점점 더 늘리고 있습니다. 기술 혁신, 우호적인 정책 지원, 그리고 효율적인 모빌리티 서비스에 대한 수요 증가가 맞물리면서, 예측 기간 동안 전 세계 도심 항공 모빌리티 시장 전체가 지속적인 성장을 이룰 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 25억 달러 |

| 예측 금액 | 267억 달러 |

| CAGR | 25.8% |

도시 지역의 교통 체증이 심화되고 도시 교통망에 가해지는 부담이 증가함에 따라, 대체 이동 수단에 대한 수요가 높아지면서 도심 항공 이동 수단 시장이 성장세를 보이고 있습니다. 시장의 확대는 선진적인 항공 운송 서비스를 대규모로 전개하기 위해 필요한 인프라의 지속적인 확충에 힘입어 이루어지고 있습니다. 운영 생태계에 대한 지속적인 투자를 통해 개발 단계에서 상용화로의 전환이 촉진되고 있습니다. 항공우주 기업, 기술 제공업체, 인프라 개발업체, 규제 관련 이해관계자간의 협력을 통해 기술 발전이 가속화되고, 도입 효율이 향상되며, 신흥 모빌리티 플랫폼에 대한 신뢰도가 높아지고 있습니다. 설비 투자 증가와 업계 전반의 파트너십은 도심 항공 모빌리티 사업의 확대와 장기적인 시장 성장을 뒷받침하는 데 있어 계속해서 중요한 역할을 하고 있습니다. 에어 모빌리티 서비스를 보다 광범위한 교통 시스템에 통합하기 위해서는 전용 시설과 지원 네트워크가 필수적이기 때문에 인프라 개발은 여전히 업계를 형성하는 가장 영향력 있는 동향 중 하나입니다. 이러한 능력의 확대로 인해 향후 몇 년 동안 운영 효율이 향상되고, 보다 광범위한 보급이 촉진될 것으로 예측됩니다.

2025년, 여객기 부문은 63.5%의 점유율을 차지했습니다. 도시 지역에서는 증가하는 모빌리티 문제에 대처하기 위한 보다 효율적인 방안이 요구되고 있으며, 첨단 여객 운송 솔루션에 대한 강력한 수요가 이 부문의 성장을 지속적으로 견인하고 있습니다. 여객용 항공기는 수송 효율 향상과 이동 시간 단축이 기대됨에 따라, 사업자와 공공기관으로부터 큰 주목을 받고 있습니다. 상호 연결된 교통 네트워크에의 통합이 진행되고, 상업용 여객 운항에 대한 집중도가 높아짐에 따라, 이 부문 시장의 주도적 지위는 더욱 공고해지고 있습니다.

수소 연료전지 부문은 2026년부터 2035년까지 연평균 성장률(CAGR) 29%로 성장할 것으로 전망됩니다. 이 부문의 성장은 다른 추진 기술에 비해 더 높은 에너지 효율과 주행 거리 연장을 실현할 수 있는 능력에 힘입어 이루어지고 있습니다. 수소 기반 시스템은 적재량 증가에 대응하면서도 더 오랜 시간 동안 운용할 수 있게 해주기 때문에 다양한 모빌리티 용도에 적합합니다. 청정 에너지 기술과 지속 가능한 항공 솔루션에 대한 관심이 높아짐에 따라 도입이 더욱 가속화되고 있으며, 수소 연료전지는 지속적으로 진화하는 도심 항공 모빌리티 분야에서 중요한 기술 분야로서의 입지를 확고히 다져가고 있습니다.

2025년, 북미의 도심 항공 모빌리티 시장은 36.5%의 점유율을 차지했습니다. 이 지역의 성장은 항공우주 분야의 확고한 혁신 기업들의 존재와 첨단 항공 운송 플랫폼의 상용화를 향한 지속적인 진전에 힘입어 이루어지고 있습니다. 지속적인 시험 활동, 인증 진행 상황, 그리고 항공 안전 요건 준수가 개발 단계에서 운용 단계로의 전환을 가속화하는 데 기여하고 있습니다. 또한, 이 시장은 항공 모빌리티 이니셔티브 추진에 초점을 맞춘 강력한 정부 지원과 협력적인 노력의 혜택을 받고 있습니다. 규제 관련 지침, 인프라 계획 추진, 그리고 공역 관리 프로그램이 보다 원활한 상용화를 위한 기반을 마련하는 데 기여하고 있으며, 도심 항공 모빌리티 기술 분야의 주요 시장으로서 북미의 위상을 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 플랫폼 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 추진 방식별, 2022-2035년

제7장 시장 추산 및 예측 : 오퍼레이션 모드별, 2022-2035년

제8장 시장 추산 및 예측 : 운영 범위별, 2022-2035년

제9장 시장 추산 및 예측 : 최종 사용자별, 2022-2035년

제10장 시장 추산 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

JHS 26.07.01The Global Urban Air Mobility Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 25.8% to reach USD 26.7 billion by 2035.

The rapid evolution of advanced aerial transportation solutions is creating significant growth opportunities across the urban air mobility industry. Increasing demand for faster transportation alternatives in congested metropolitan areas is encouraging the adoption of innovative air mobility platforms designed to improve travel efficiency and reduce transit times. Advancements in next-generation aviation technologies, coupled with supportive regulatory frameworks, are accelerating the path toward commercial deployment. Growing financial investments and strategic collaborations among industry participants are further strengthening market development by supporting technology maturation and operational readiness. The industry is also benefiting from rising emphasis on sustainable transportation solutions and reduced environmental impact, encouraging the adoption of cleaner mobility technologies. As urban transportation systems continue to evolve, stakeholders are increasingly investing in infrastructure, vehicle development, and ecosystem integration initiatives that support long-term commercialization. The convergence of technological innovation, favorable policy support, and increasing demand for efficient mobility services is expected to drive sustained growth across the global urban air mobility market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $26.7 Billion |

| CAGR | 25.8% |

The urban air mobility market is gaining momentum as rising traffic congestion and growing pressure on urban transportation networks increase demand for alternative mobility solutions. Market expansion is being supported by the ongoing development of the infrastructure required to enable large-scale deployment of advanced air transportation services. Continued investments in operational ecosystems are facilitating the transition from development stages to commercial implementation. Collaboration among aerospace companies, technology providers, infrastructure developers, and regulatory stakeholders is accelerating technology advancement, improving deployment efficiency, and strengthening confidence in emerging mobility platforms. Increasing capital investment and industry-wide partnerships continue to play a critical role in scaling urban air mobility operations and supporting long-term market growth. Infrastructure development remains one of the most influential trends shaping the industry, as dedicated facilities and supporting networks become essential for integrating air mobility services into broader transportation systems. The expansion of these capabilities is expected to enhance operational efficiency and support wider adoption over the coming years.

The passenger air vehicles segment held a 63.5% share in 2025. Strong demand for advanced passenger transportation solutions continues to drive growth within this segment as cities seek more efficient ways to address increasing mobility challenges. Passenger-focused air vehicles are receiving significant attention from operators and public authorities due to their potential to improve transportation efficiency and reduce travel times. Their growing incorporation into interconnected transportation networks and increasing focus on commercial passenger operations continue to strengthen the segment's leading market position.

The hydrogen fuel cell segment is projected to grow at a CAGR of 29% during 2026-2035. The segment's growth is being driven by its capability to deliver greater energy efficiency and extended operational range compared to alternative propulsion technologies. Hydrogen-based systems support longer-duration operations while accommodating increased payload requirements, making them well suited for a broader range of mobility applications. Growing interest in clean energy technologies and sustainable aviation solutions is further accelerating adoption, positioning hydrogen fuel cells as an important technology segment within the evolving urban air mobility landscape.

North America Urban Air Mobility Market accounted for 36.5% share in 2025. Regional growth is being supported by the presence of established aerospace innovators and ongoing progress toward the commercial deployment of advanced aerial transportation platforms. Continued testing activities, certification advancements, and alignment with aviation safety requirements are helping accelerate the transition from development to operational implementation. The market is also benefiting from strong governmental support and coordinated efforts focused on advancing air mobility initiatives. Regulatory guidance, infrastructure planning efforts, and airspace management programs are contributing to a more streamlined commercialization pathway, strengthening North America's position as a leading market for urban air mobility technologies.

Key companies operating in the Global Urban Air Mobility Market include Archer Aviation, Joby Aviation, Vertical Aerospace, EHang, Beta Technologies, Volocopter, Wisk Aero, AutoFlight, XPeng AeroHT, SkyDrive, and Electra.aero, Overair, Elroy Air, Dronamics, Pipistrel, TCab Tech, Volant Aerotech, Doroni Aerospace, Apeleon, Aergility, Natilus, and Jump Aero. Companies participating in the urban air mobility industry are pursuing a variety of strategic initiatives to strengthen their market position and expand their competitive advantage. Research and development investments remain a primary focus as manufacturers work to enhance aircraft performance, operational safety, energy efficiency, and commercial viability. Strategic collaborations with aerospace organizations, infrastructure developers, technology providers, and regulatory stakeholders are helping accelerate product development and market entry. Companies are also prioritizing certification milestones and operational readiness programs to support commercialization efforts. Expanding production capabilities, strengthening supply chain networks, and developing integrated mobility ecosystems are further supporting growth strategies. In addition, organizations are investing in advanced propulsion technologies, digital flight systems, and infrastructure partnerships to improve service scalability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Propulsion type trends

- 2.2.3 Operation mode trends

- 2.2.4 Operational range trends

- 2.2.5 End User trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing urban congestion and demand for faster transportation

- 3.2.1.2 Advancements in eVTOL and autonomous light technologies

- 3.2.1.3 Growing government support and regulatory development

- 3.2.1.4 Rising investments and strategic partnerships

- 3.2.1.5 Increasing focus on sustainable and low-emission transportation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure development and operational costs

- 3.2.2.2 Regulatory uncertainty and airspace integration complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption in logistics and emergency services

- 3.2.3.2 Expansion of inter-city and regional air mobility services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Passenger air vehicles

- 5.2.1 Air taxis

- 5.2.2 Air shuttles

- 5.2.3 Personal air vehicles

- 5.3 Cargo air vehicles

- 5.3.1 Last-mile delivery vehicles

- 5.3.2 Heavy cargo UAVs

- 5.4 Specialized service vehicles

- 5.4.1 Air ambulance

- 5.4.2 Emergency/disaster support

Chapter 6 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Battery-electric

- 6.3 Hybrid-electric

- 6.4 Hydrogen fuel cell

Chapter 7 Market Estimates and Forecast, By Operation Mode, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Piloted operations

- 7.3 Semi-autonomous / remotely supervised operations

- 7.4 Fully autonomous operations

Chapter 8 Market Estimates and Forecast, By Operational Range, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Short range (0-50km)

- 8.3 Medium range (50-150km)

- 8.4 Long range (150-300km)

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial mobility operators

- 9.3 Logistics operators

- 9.4 Medical & emergency agencies

- 9.5 Private/corporate operators

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 EHang

- 11.1.2 AutoFlight

- 11.1.3 Volocopter

- 11.1.4 Joby Aviation

- 11.1.5 XPeng AeroHT

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Wisk Aero

- 11.2.1.2 Archer Aviation

- 11.2.1.3 Beta Technologies

- 11.2.1.4 Electra.aero

- 11.2.1.5 Overair

- 11.2.1.6 Elroy Air

- 11.2.1.7 Doroni Aerospace

- 11.2.1.8 Jump Aero

- 11.2.1.9 Natilus

- 11.2.2 Asia Pacific

- 11.2.2.1 SkyDrive

- 11.2.2.2 TCab Tech

- 11.2.2.3 Volant Aerotech

- 11.2.3 Europe

- 11.2.3.1 Vertical Aerospace

- 11.2.3.2 Pipistrel

- 11.2.3.3 Dronamics

- 11.2.4 Middle East & Africa

- 11.2.4.1 Apeleon

- 11.2.4.2 Aergility

- 11.2.1 North America