|

시장보고서

상품코드

2038690

버킷 트럭 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bucket Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

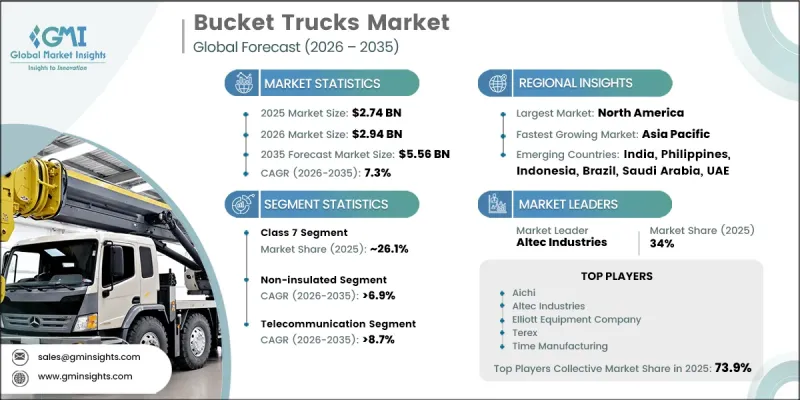

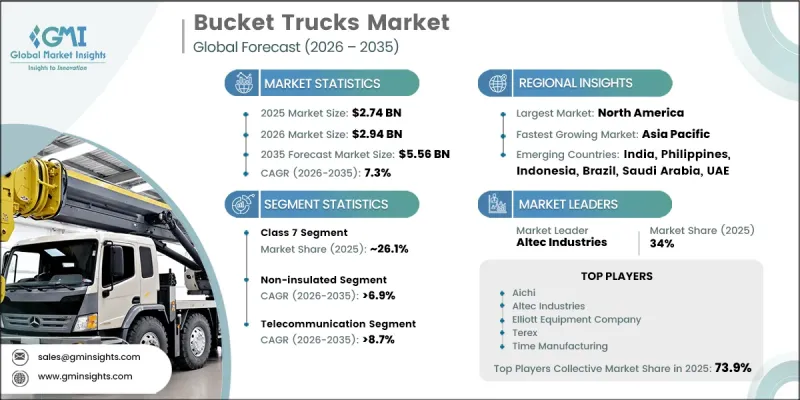

세계의 버킷 트럭 시장은 2025년에 27억 4,000만 달러로 평가되었고, CAGR 7.3%로 성장할 전망이며, 2035년까지 55억 6,000만 달러에 이를 것으로 예측됩니다.

시장 확대는 선진국과 신흥국 모두에서 공공 인프라 개발에 대한 투자 증가와 도시 유지관리에 대한 수요 증가에 의해 주도되고 있습니다. 신뢰할 수 있는 배전 시스템에 대한 수요 증가, 통신 네트워크의 확장 및 지속적인 지자체 서비스 개선은 시장 성장에 크게 기여하고 있습니다. 급속한 도시화, 스마트시티 개발 노력, 노후화된 전력망 인프라의 지속적인 현대화로 인해 고소작업차에 대한 수요는 더욱 증가하고 있습니다. 과거 사다리 등 수동 승강 방식에 의존하던 유틸리티 및 서비스 산업은 업무 생산성을 높이고 인력 의존도를 낮추며 고소 작업의 작업장 안전을 높이기 위해 버킷 트럭과 같은 기계화 승강 솔루션의 도입이 증가하고 있습니다. 동시에, 근로자의 안전 표준에 대한 강조와 규제 프레임워크의 강화로 인해 여러 최종 사용 부문에서 도입이 가속화되고 있습니다. 송전선로 유지보수, 통신설비 점검, 도로 인프라 보수와 같은 작업은 위험도가 높기 때문에 기업들은 보다 안전하고 제어 가능한 작업 솔루션에 투자하고 있습니다. 현대식 버킷 트럭은 절연 붐 시스템, 안정화된 플랫폼, 인체공학적 조작 인터페이스, 강화된 안전 메커니즘을 통해 열악한 현장 환경에서도 높은 효율성과 신뢰성을 유지하면서 보다 안전하게 작업할 수 있도록 합니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 27억 4,000만 달러 |

| 예측 시장 규모 | 55억 6,000만 달러 |

| CAGR | 7.3% |

클래스 7 부문은 2025년 26.1%의 점유율을 차지했으며, 2035년까지 연평균 7.8%의 성장률을 보일 것으로 전망됩니다. 이 부문은 적재 능력, 운영 유연성, 성능 효율성의 강력한 조합으로 시장을 선도하고 있습니다. 도시 및 교외 환경에서도 효과적으로 작동하고 중량물 운반 시스템에 대응할 수 있어 유틸리티 유지보수, 통신 및 지자체 용도에 널리 도입되고 있습니다. 또한, 이 부문은 유압 리프트 시스템 및 확장형 붐 작동을 지원하며, 큰 구성 변경 없이도 다양한 산업 분야의 복잡한 고소 작업에 적합합니다.

비절연 부문은 2025년 57.7%의 점유율을 차지했으며, 2026-2035년 연평균 복합 성장률(CAGR) 6.9%를 나타낼 것으로 예측됩니다. 이 부문은 건설, 통신, 지자체 유지보수, 일반 서비스 업무 등 다양한 분야에 적용될 수 있다는 점에서 시장을 독점하고 있습니다. 절연형에 비해 비절연형은 비용 효율이 높고, 설계가 간단하며, 유지보수 요구사항이 적기 때문에 비절연형이 선호되고 있습니다. 이러한 특성으로 인해 비절연 버킷 트럭은 감전 방지가 주요 운영 요구 사항이 아닌 일상적인 고소 작업에 매우 적합합니다.

미국의 버킷 트럭 시장은 2025년 8억 2,440만 달러 규모로, 북미 시장에서 83.58%의 점유율을 차지했습니다. 이 나라 시장 성장은 전력망 현대화, 노후화된 인프라 교체, 유틸리티 사업자의 유지보수 활동 증가에 대한 대규모 투자에 의해 주도되고 있습니다. 전력회사들은 신뢰성을 높이고 정전 위험을 줄이기 위해 송배전 시스템을 업그레이드하고 있으며, 이로 인해 고소작업차에 대한 수요가 크게 증가하고 있습니다. 잦은 날씨로 인한 혼란과 긴급 복구 활동도 차량 수요를 더욱 증가시키고 있습니다. 또한, 주요 제조업체의 존재는 미국 전역의 지속적인 제품 혁신과 차량 현대화를 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별(2022-2035년)

제6장 시장 추산 및 예측 : 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

AJY 26.06.11The Global Bucket Trucks Market was valued at USD 2.74 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 5.56 billion by 2035.

Market expansion is driven by increasing investments in utility infrastructure development and rising urban maintenance requirements across both developed and emerging economies. Growing demand for reliable electricity distribution systems, expanding telecommunication networks, and ongoing municipal service upgrades are significantly contributing to market growth. Rapid urbanization, smart city development initiatives, and continuous modernization of aging power grid infrastructure are further increasing the need for advanced aerial access equipment. Utility and service industries, which previously depended on manual lifting methods such as ladders, are increasingly adopting mechanized lifting solutions like bucket trucks to improve operational productivity, reduce labor dependency, and enhance workplace safety in elevated operations. At the same time, growing emphasis on worker safety standards and stricter regulatory frameworks is accelerating adoption across multiple end-use sectors. Activities such as power line maintenance, telecom servicing, and street infrastructure repair involve elevated risk exposure, prompting companies to invest in safer, more controlled working solutions. Modern bucket trucks now incorporate insulated boom systems, stabilized platforms, ergonomic control interfaces, and enhanced safety mechanisms, enabling safer operations while maintaining high efficiency and reliability in demanding field environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.74 Billion |

| Forecast Value | $5.56 Billion |

| CAGR | 7.3% |

The Class 7 segment held a 26.1% share in 2025 and is projected to grow at a CAGR of 7.8% through 2035. This segment leads the market due to its strong combination of load-handling capability, operational flexibility, and performance efficiency. It is widely deployed across utility maintenance, telecommunications, and municipal applications because it can accommodate heavy lifting systems while still operating effectively in urban and semi-urban environments. The segment also supports hydraulic lift systems and extended boom operations, making it suitable for complex elevated tasks across multiple industries without requiring major configuration changes.

The non-insulated segment accounted for 57.7% share in 2025 and is expected to grow at a CAGR of 6.9% between 2026 and 2035. This segment dominates due to its broad applicability across construction, telecom, municipal maintenance, and general service operations. It is favored for its cost efficiency, simpler design, and reduced maintenance requirements compared to insulated alternatives. These characteristics make non-insulated bucket trucks highly suitable for routine aerial operations where electrical hazard protection is not a primary operational requirement.

U.S. Bucket Trucks Market generated USD 824.4 million in 2025 and held 83.58% share in North America. Market growth in the country is being driven by extensive investments in power grid modernization, replacement of aging infrastructure, and rising utility maintenance activities. Utility operators are upgrading transmission and distribution systems to improve reliability and reduce outage risks, significantly boosting demand for aerial work platforms. Frequent weather-related disruptions and emergency restoration activities further strengthen fleet requirements. The presence of leading manufacturers also supports continuous product innovation and fleet modernization across the country.

Key companies operating in the Global Bucket Trucks Industry include Terex, Altec Industries, JLG Industries, Palfinger, Aichi, Tadano, Haulotte, Elliott Equipment Company, Bronto Skylift, and Time Manufacturing. Companies in the bucket trucks market are focusing on advancing product safety, improving operational efficiency, and integrating smart hydraulic and control systems to strengthen their competitive position. Continuous investment in R&D is enabling the development of lightweight yet high-capacity aerial platforms with improved stability and reach. Manufacturers are also prioritizing electrification and hybrid powertrain solutions to align with sustainability goals and reduce operating emissions. Expansion of rental and leasing models is helping companies increase market penetration and cater to cost-sensitive customers. Strengthening after-sales service networks and mobile maintenance support is further enhancing customer retention.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Type

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Power & Utility Infrastructure

- 3.2.1.2 Growth in Telecommunication Networks

- 3.2.1.3 Rising Urbanization & Smart City Projects

- 3.2.1.4 Emphasis on Worker Safety & Regulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Investment Costs

- 3.2.2.2 Maintenance & Operational Costs

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of Electric & Hybrid Bucket Trucks

- 3.2.3.2 Emerging Markets Infrastructure Development

- 3.2.3.3 Fleet Modernization & Replacement Demand

- 3.2.3.4 Integration with Smart Fleet Management Systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and Innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory guideline

- 3.6.1 North America

- 3.6.1.1 US - OSHA Aerial Lift Standard (29 CFR 1910.67)

- 3.6.1.2 Canada - CSA C225 Aerial Device Standard

- 3.6.2 Europe

- 3.6.2.1 Germany - DGUV Regulation 52 (Cranes & Lifting Equipment)

- 3.6.2.2 UK - LOLER 1998 (Lifting Operations and Lifting Equipment Regulations)

- 3.6.2.3 France - INRS ED 828 (Aerial Work Platform Guidelines)

- 3.6.2.4 Nordics - EN 280 Standard (Mobile Elevating Work Platforms)

- 3.6.3 Asia Pacific

- 3.6.3.1 China - GB/T 9465 Aerial Work Platform Safety Standard

- 3.6.3.2 India - IS 13367 (Part 1 & 2) Aerial Platforms Standard

- 3.6.3.3 Japan - Industrial Safety and Health Act (Aerial Work Platforms)

- 3.6.4 Latin America

- 3.6.4.1 Brazil - NR-12 Machinery and Equipment Safety Regulation

- 3.6.5 MEA

- 3.6.5.1 Saudi Arabia - SASO ISO 16368 Aerial Work Platform Standard

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent Landscape (Driven by Primary Research)

- 3.10 Trade Data Analysis (Based on Paid Database)

- 3.10.1 Import/Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.11 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Production Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.14.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Class 4

- 5.2.1 Insulated

- 5.2.2 Non-insulated

- 5.3 Class 5

- 5.3.1 Insulated

- 5.3.2 Non-insulated

- 5.4 Class 6

- 5.4.1 Insulated

- 5.4.2 Non-insulated

- 5.5 Class 7

- 5.5.1 Insulated

- 5.5.2 Non-insulated

- 5.6 Class 8

- 5.6.1 Insulated

- 5.6.2 Non-insulated

Chapter 6 Market Estimates & Forecast, By Type, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Insulated

- 6.3 Non-insulated

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Utility

- 7.3.1 Electric

- 7.3.2 Water

- 7.4 Telecommunication

- 7.5 Forestry

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Netherlands

- 8.3.8 Belgium

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Philippines

- 8.4.7 Indonesia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Aichi

- 9.1.2 Altec Industries

- 9.1.3 Bronto Skylift

- 9.1.4 Elliott Equipment Company

- 9.1.5 Haulotte

- 9.1.6 JLG Industries

- 9.1.7 Palfinger

- 9.1.8 Tadano

- 9.1.9 Terex

- 9.1.10 Time Manufacturing Company

- 9.2 Regional Players

- 9.2.1 CMC

- 9.2.2 CTE

- 9.2.3 Dur-A-Lift

- 9.2.4 GSR

- 9.2.5 Multitel Pagliero

- 9.2.6 Niftylift

- 9.2.7 Oil&Steel

- 9.2.8 Platform Basket

- 9.2.9 Posi-Plus Technologies

- 9.2.10 Socage

- 9.3 Emerging Players

- 9.3.1 Klubb

- 9.3.2 Manitex International

- 9.3.3 Omme Lift

- 9.3.4 Sinoboom

- 9.3.5 Zhejiang Dingli Machinery