|

시장보고서

상품코드

2038693

우주 태양에너지 발전 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Space-Based Solar Power Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

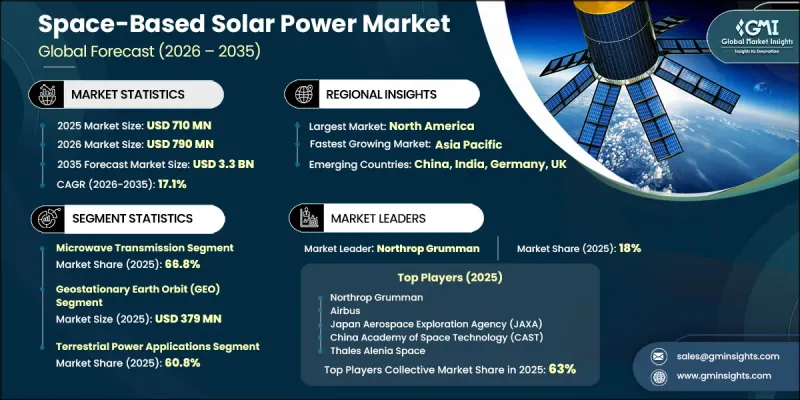

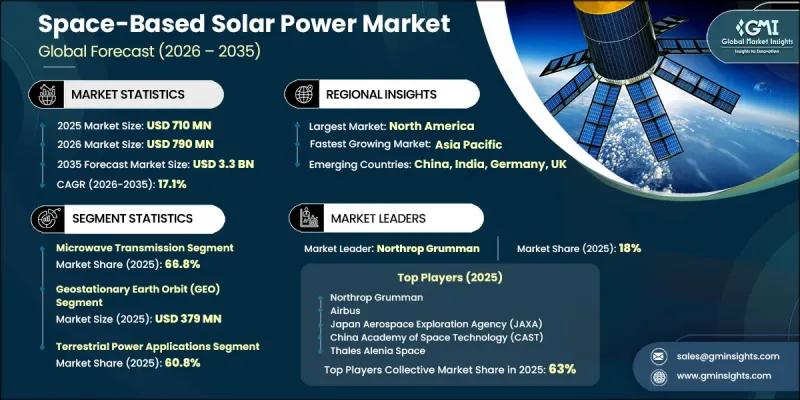

세계의 우주 태양에너지 발전 시장은 2025년에 7억 1,000만 달러로 평가되었고, CAGR 17.1%로 성장할 전망이며, 2035년까지 33억 달러에 이를 것으로 추정되고 있습니다.

지상 재생에너지의 한계를 넘어 중단 없는 지속 가능한 발전에 대한 수요가 증가함에 따라 이 시장은 점점 더 큰 추진력을 얻고 있습니다. 기존 태양광 및 풍력 시스템에 대한 의존도가 높아지면서 간헐성 문제가 부각되면서 지속적인 전력 공급이 가능한 궤도 에너지 플랫폼에 대한 관심이 높아지고 있습니다. 재사용 가능한 발사 시스템과 대형 발사 능력의 발전으로 우주에 대규모 에너지 인프라를 배치할 수 있는 가능성이 높아지고 있습니다. 실증 미션과 자금 지원 이니셔티브를 통한 정부의 지원 확대는 기술 검증 및 상용화 노력을 가속화하고 있습니다. 이와 함께 안전하고 신뢰할 수 있는 에너지 공급 시스템에 대한 국방 관련 관심도 시장 확대를 더욱 부추기고 있습니다. 무선 전력 전송 기술과 궤도상 조립 기술의 지속적인 발전으로 시스템의 효율성과 확장성이 향상되고 있습니다. 에너지 안보, 탈탄소화, 차세대 인프라에 대한 전 세계의 관심이 높아지는 가운데, 우주 태양에너지 발전은 장기적인 에너지 공급 모델을 변화시킬 수 있는 유망한 솔루션으로 떠오르고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 7억 1,000만 달러 |

| 예측 시장 규모 | 33억 달러 |

| CAGR | 17.1% |

우주 태양에너지 발전 시장은 지상의 환경 조건에 영향을 받지 않고 안정적으로 운영되는 기저부하 재생에너지에 대한 수요가 증가함에 따라 더욱 견인되고 있습니다. 지속적인 에너지 공급으로의 전환은 중단 없는 발전과 송전이 가능한 궤도 플랫폼에 대한 투자를 촉진하고 있습니다. 재사용 가능한 로켓 기술을 통해 실현된 발사 비용 절감은 배치 비용 절감과 발사 빈도 증가를 뒷받침하고 있습니다. 이를 통해 대규모 궤도 인프라의 상업적 실현 가능성을 높이고 있습니다. 연구, 파일럿 프로그램 및 타당성 평가에 대한 투자 확대도 기술 발전을 가속화하고 있습니다. 위성 제조 능력의 향상과 송전 시스템의 개선은 효율성과 신뢰성 향상에 기여하고 있으며, 시장 전망을 더욱 견고하게 하고 있습니다.

마이크로파 전송 부문은 기술 성숙도와 장거리 에너지 전송의 우수한 성능을 반영하여 2025년 66.8%의 점유율을 차지했습니다. 이 방식은 다른 전송 방식에 비해 대기 손실이 적고 효율이 높기 때문에 초기 단계에서 선호되는 방식입니다. 대규모 지상 수신 시스템과의 호환성 또한 도입을 촉진하고 있으며, 전송 기술의 지속적인 발전으로 신뢰성과 확장성은 더욱 향상되고 있습니다.

정지 궤도 부문은 일관된 태양광 조사와 안정적인 에너지 송전을 제공할 수 있기 때문에 2025년 3억 7,900만 달러에 달했습니다. 이 궤도에서 운영되는 시스템은 수신 스테이션과의 지속적인 정렬을 통해 중단 없는 전력 공급을 가능하게 합니다. 이러한 안정성으로 인해 장기적인 임무나 대규모 발전 프로젝트에 특히 적합합니다. 일정한 위치를 유지할 수 있는 능력은 운영상의 복잡성을 줄이고, 전체 시스템의 효율성을 높이며, 견고한 수요를 뒷받침합니다.

북미의 우주 태양에너지 발전 시장은 에너지 자립, 지속가능성 목표, 기술 혁신에 대한 관심 증가에 힘입어 2025년 37.1%의 점유율을 차지했습니다. 이 지역은 궤도상 에너지 시스템 개발 및 시험에 적극적으로 참여하고 있는 우주 기관과 선진 항공우주 조직의 강력한 참여의 혜택을 누리고 있습니다. 차세대 발사 인프라 및 연구 프로그램에 대한 투자로 무선 전력 전송 및 궤도 조립과 같은 주요 기술의 발전이 가속화되고 있습니다. 항공우주 생태계가 잘 구축되어 있고, 지속 가능한 재생 에너지 솔루션에 대한 관심이 높아지면서 이 지역 시장 성장에 더욱 박차를 가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 에너지 전송 방식별(2022-2035년)

제6장 시장 추산 및 예측 : 궤도 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 발전 용량별(2022-2035년)

제8장 시장 추산 및 예측 : 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

AJY 26.06.11The Global Space-Based Solar Power Market was valued at USD 710 million in 2025 and is estimated to grow at a CAGR of 17.1% to reach USD 3.3 billion by 2035.

The market is gaining momentum as demand rises for uninterrupted and sustainable energy generation beyond the limitations of ground-based renewable sources. Increasing reliance on conventional solar and wind systems has highlighted intermittency challenges, driving interest in orbital energy platforms capable of delivering continuous power. Advancements in reusable launch systems and heavy-lift capabilities are improving the feasibility of deploying large-scale energy infrastructure into space. Growing government support through demonstration missions and funding initiatives is accelerating technology validation and commercialization efforts. In parallel, defense-related interest in secure and reliable energy supply systems is further supporting market expansion. Continuous progress in wireless power transmission technologies and in-orbit assembly methods is enhancing system efficiency and scalability. As global focus intensifies on energy security, decarbonization, and next-generation infrastructure, space-based solar power is emerging as a promising solution capable of transforming long-term energy supply models.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $710 Million |

| Forecast Value | $3.3 Billion |

| CAGR | 17.1% |

The space-based solar power market is further driven by increasing demand for reliable baseload renewable energy that operates independently of terrestrial environmental conditions. The shift toward continuous energy availability is encouraging investment in orbital platforms capable of generating and transmitting power without disruption. Improvements in launch economics, enabled by reusable vehicle technologies, are reducing deployment costs and supporting higher launch frequency. This is making large-scale orbital infrastructure more commercially viable. Growing investment in research, pilot programs, and feasibility assessments is also accelerating technological progress. Enhanced satellite manufacturing capabilities and improvements in power transmission systems are contributing to increased efficiency and reliability, strengthening the market outlook.

The microwave transmission segment accounted for 66.8% share in 2025, reflecting its technological maturity and strong performance in long-distance energy transfer. This method offers lower atmospheric loss and greater efficiency compared to alternative transmission approaches, making it a preferred option for early-stage deployment. Its compatibility with large-scale ground receiving systems further supports its adoption, while ongoing advancements in transmission technologies continue to improve reliability and scalability.

The geostationary Earth orbit segment reached USD 379 million in 2025, owing to its ability to provide consistent solar exposure and stable energy transmission. Systems operating in this orbit benefit from continuous alignment with receiving stations, enabling uninterrupted power delivery. This stability makes it particularly suitable for long-duration missions and large-scale energy generation projects. The ability to maintain constant positioning reduces operational complexity and enhances overall system efficiency, supporting strong demand.

North America Space-Based Solar Power Market accounted for 37.1% share in 2025, driven by increasing focus on energy independence, sustainability goals, and technological innovation. The region benefits from strong participation by space agencies and advanced aerospace organizations that are actively developing and testing orbital energy systems. Investments in next-generation launch infrastructure and research programs are accelerating progress in key technologies such as wireless power transmission and in-orbit assembly. A well-established aerospace ecosystem and growing interest in continuous renewable energy solutions are further strengthening regional market growth.

Key companies operating in the Global Space-Based Solar Power Market include Airbus, SpaceX, Boeing, Lockheed Martin, Northrop Grumman, Mitsubishi Electric Corporation, Thales Alenia Space, Blue Origin, OHB SE, Solaren Corporation, Space Solar Ltd, Emrod, China Academy of Space Technology (CAST), and Japan Aerospace Exploration Agency (JAXA).Companies in the Space-Based Solar Power Market are focusing on strategic developments to enhance their competitive position and accelerate commercialization. A major priority is investment in research and development to improve energy conversion efficiency, wireless transmission capabilities, and large-scale orbital system design. Firms are forming partnerships with government agencies, defense organizations, and research institutions to secure funding and support pilot projects. Emphasis is also being placed on developing modular and scalable system architectures that can be deployed efficiently in space. Companies are leveraging advancements in reusable launch technologies to reduce deployment costs and improve project feasibility. Additionally, efforts are being made to strengthen supply chains and manufacturing capabilities for satellite components.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Energy transmission type trends

- 2.2.2 Orbit type trends

- 2.2.3 Power capacity trends

- 2.2.4 Application trends

- 2.2.5 End-user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising baseload renewable demand beyond terrestrial intermittency

- 3.2.1.2 Advancements in reusable launch vehicles lowering deployment costs

- 3.2.1.3 Increasing defense interest in uninterrupted orbital power supply

- 3.2.1.4 Government-funded SBSP pilot missions in US, China, Japan

- 3.2.1.5 Net-zero targets driving investment in scalable clean energy

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Extremely high upfront capital and orbital deployment costs

- 3.2.2.2 Atmospheric losses and safety concerns in power beaming

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with lunar missions and deep-space infrastructure

- 3.2.3.2 Public-private partnerships accelerating SBSP commercialization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Energy Transmission Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Microwave transmission

- 5.3 Laser transmission

Chapter 6 Market Estimates and Forecast, By Orbit Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Geostationary earth orbit (GEO)

- 6.3 Low earth orbit (LEO)

- 6.4 Medium earth orbit (MEO)

Chapter 7 Market Estimates and Forecast, By Power Capacity, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Below 10 MW

- 7.3 10 to 100 MW

- 7.4 100 to 1,000 MW

- 7.5 Above 1,000 MW

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Terrestrial power applications

- 8.3 Space-based power applications

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Government & defense

- 9.3 Commercial

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Airbus

- 11.1.2 Boeing

- 11.1.3 Lockheed Martin

- 11.1.4 Northrop Grumman

- 11.1.5 Thales Alenia Space

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Blue Origin

- 11.2.1.2 Solaren Corporation

- 11.2.1.3 SpaceX

- 11.2.2 Asia Pacific

- 11.2.2.1 China Academy of Space Technology (CAST)

- 11.2.2.2 Japan Aerospace Exploration Agency (JAXA)

- 11.2.2.3 Mitsubishi Electric Corporation

- 11.2.3 Europe

- 11.2.3.1 OHB SE

- 11.2.3.2 Space Solar Ltd

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Emrod