|

시장보고서

상품코드

2038694

리튬 코발트 산화물 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Lithium Cobalt Oxide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

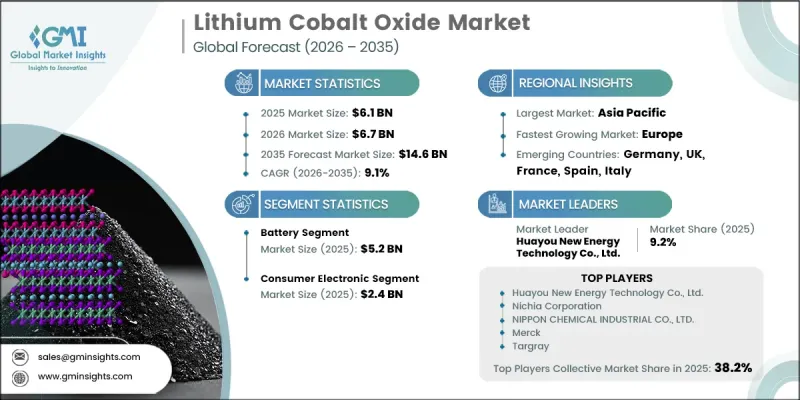

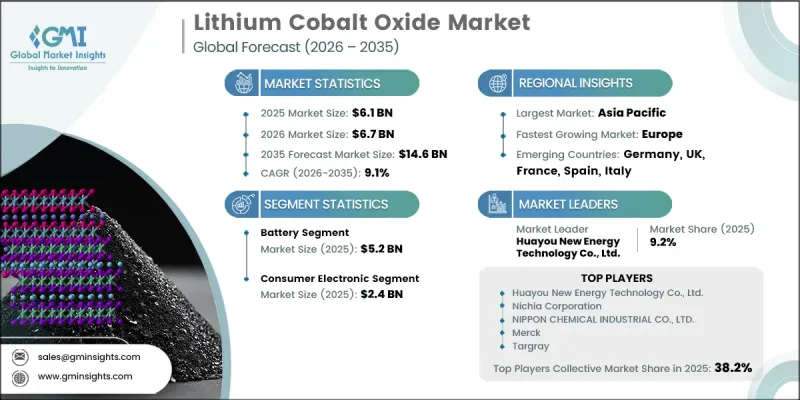

세계의 리튬 코발트 산화물 시장은 2025년에 61억 달러로 평가되었고, CAGR 9.1%로 성장할 전망이며, 2035년까지 146억 달러에 이를 것으로 추정되고 있습니다.

이 산업은 광범위한 휴대용 전원 공급 장치 용도를 지원하는 광범위한 리튬 이온 배터리 생태계의 필수적인 부분을 구성하고 있습니다. 시장 성장에는 원자재 가용성, 요구되는 성능 기준, 배터리 설계의 지속적인 개선 등의 요인이 영향을 미치고 있습니다. 리튬 코발트 산화물은 확립된 제조 공정과 안정적인 전기 화학적 성능으로 인해 계속해서 견고한 지위를 유지하고 있습니다. 리튬, 코발트, 산소로 구성된 안정된 층상 구조는 충방전 사이클 동안 효율적인 이온 이동을 지원하여 신뢰할 수 있는 양극 소재입니다. 이 소재는 높은 에너지 밀도와 장기적인 작동 안정성이 요구되는 용도에 특히 적합합니다. 지속적인 기술 발전으로 효율이 점차 향상되고 있으며, 코발트 의존도를 낮추기 위해 재료 구성의 최적화가 진행되고 있습니다. 그 결과, 시장은 성능, 비용, 지속가능성의 균형을 중시하면서 계속 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 61억 달러 |

| 예측 시장 규모 | 146억 달러 |

| CAGR | 9.1% |

2025년, 배터리 분야는 52억 달러에 달했습니다. 재료의 순도와 균일성에 대한 요구가 높아짐에 따라, 특히 정밀도와 신뢰성이 요구되는 용도 분야에서 생산 표준을 형성하고 있습니다. 각 제조업체는 엄격한 품질 및 안전 요구 사항을 충족시키기 위해 공급 계약을 강화하고 생산 기술을 개선하고 있습니다. 동시에 기능성을 유지하면서 코발트 사용량을 최소화할 수 있는 고에너지 밀도 솔루션을 개발하기 위한 노력이 진행되고 있습니다. 입자 공학, 표면 코팅 및 재활용 공정의 발전은 성능의 안정성과 수명 주기를 연장하는 데 기여하고 있습니다.

2025년, 가전기기 부문은 24억 달러 시장 규모를 기록했습니다. 코발트 리튬 산화물은 장치의 안정적인 작동을 지원하는 소형 고에너지 배터리 솔루션을 실현하는 데 중요한 역할을 합니다. 재료 정제 및 코팅 기술의 향상으로 제조업체는 장기간 신뢰할 수 있는 성능을 발휘하는 경량 부품을 생산할 수 있게 되었습니다. 정밀 기기 용도 분야에서 안정적인 전압 출력의 필요성은 이 소재에 대한 지속적인 수요를 더욱 촉진하고 있습니다.

북미의 리튬 코발트 산화물 시장은 2025년 18억 달러로 평가되었고, 2035년까지 45억 달러로 성장할 것으로 예측됩니다. 이 지역에서는 이미 구축된 배터리 생산 능력과 재활용 인프라를 바탕으로 안정적인 수요가 예상됩니다. 중점 분야는 자원의 효율적 활용, 투명한 공급망, 재활용 재료를 배터리 제조 공정에 통합하여 장기적인 시장 안정에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 등급별(2022-2035년)

제6장 시장 추산 및 예측 : 용도별(2022-2035년)

제7장 시장 추산 및 예측 : 지역별(2022-2035년)

제8장 기업 개요

AJY 26.06.11The Global Lithium Cobalt Oxide Market was valued at USD 6.1 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 14.6 billion by 2035.

The industry forms an integral part of the broader lithium-ion battery ecosystem, supporting a wide range of portable power applications. Market growth is influenced by factors such as raw material accessibility, required performance standards, and continuous improvements in battery design. Lithium cobalt oxide continues to maintain a strong position due to its well-established production processes and consistent electrochemical performance. Its stable layered structure, composed of lithium, cobalt, and oxygen, supports efficient ion movement during charge and discharge cycles, making it a reliable cathode material. The material is particularly suited for applications requiring high energy density and long-term operational consistency. Ongoing technological advancements are gradually improving efficiency while optimizing material composition to reduce reliance on cobalt. As a result, the market continues to evolve with a focus on balancing performance, cost, and sustainability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.1 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 9.1% |

The battery segment accounted for USD 5.2 billion in 2025. Increasing demand for higher material purity and uniformity is shaping production standards, particularly for applications that require precision and reliability. Manufacturers are strengthening supply agreements and refining production techniques to align with strict quality and safety requirements. At the same time, efforts are being directed toward developing energy-dense solutions that minimize cobalt usage without compromising functionality. Advances in particle engineering, surface coating, and recycling processes are contributing to improved performance stability and longer lifecycle characteristics.

The consumer electronics segment captured USD 2.4 billion in 2025. Lithium cobalt oxide plays a critical role in enabling compact and high-energy battery solutions that support consistent device operation. Enhanced material refinement and coating technologies allow manufacturers to produce lightweight components with dependable performance over extended periods. The need for stable voltage output in precision-based applications further supports the material's continued demand.

North America Lithium Cobalt Oxide Market is expected to grow from USD 1.8 billion in 2025 to USD 4.5 billion by 2035. The region demonstrates steady demand supported by established battery production capabilities and recycling infrastructure. Focus areas include efficient resource utilization, transparent supply chains, and the integration of recycled materials into battery manufacturing processes, contributing to long-term market stability.

Key companies operating in the Global Lithium Cobalt Oxide Market include Targray, Merck, Stanford Advanced Materials, Nichia Corporation, Tokyo Chemical Industry, NIPPON CHEMICAL INDUSTRIAL CO., LTD., Cosmo AM&T Co. Ltd., Huayou New Energy Technology Co. Ltd., Elcan Industries Inc., Otto Chemie Pvt. Ltd., and Horiba Scientific. Companies in the Lithium Cobalt Oxide Market are reinforcing their market position through sustained investment in research and development aimed at improving material efficiency and reducing cobalt dependency. Strategic partnerships and long-term supply agreements are being established to secure raw material availability and strengthen value chains. Manufacturers are focusing on advanced processing techniques, including particle engineering and coating technologies, to enhance product performance and durability. Expansion of recycling capabilities is also becoming a priority to support sustainability goals and resource optimization.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Grade

- 2.2.2 Application

- 2.2.3 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High energy density battery demand

- 3.2.1.2 Widespread use in consumer electronics

- 3.2.1.3 Established lithium-ion battery infrastructure

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Cobalt supply chain uncertainty issues

- 3.2.2.2 High material and processing costs

- 3.2.3 Opportunities

- 3.2.3.1 Material optimization through reduced cobalt

- 3.2.3.2 Recycling and recovery process development

- 3.2.3.3 Demand from compact electronic devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By grade

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Industrial

- 5.3 Battery

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Consumer electronic

- 6.3 Electric vehicle

- 6.4 Medical devices

- 6.5 Energy storage system

- 6.6 Telecommunication

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Cosmo AM&T Co.Ltd

- 8.2 Targray

- 8.3 Huayou New Energy technology Co Ltd

- 8.4 Elcan Industries Inc.

- 8.5 Stanford Advanced Materials

- 8.6 Nichia corporation

- 8.7 NIPPON CHEMICAL INDUSTRIAL CO.,LTD.

- 8.8 Tokyo Chemical Industry

- 8.9 Merck

- 8.10 Otto Chemie Pvt. Ltd.

- 8.11 Horiba Scientific