|

시장보고서

상품코드

2045784

비유전자 변형 요거트 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Non-GMO Yogurt Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

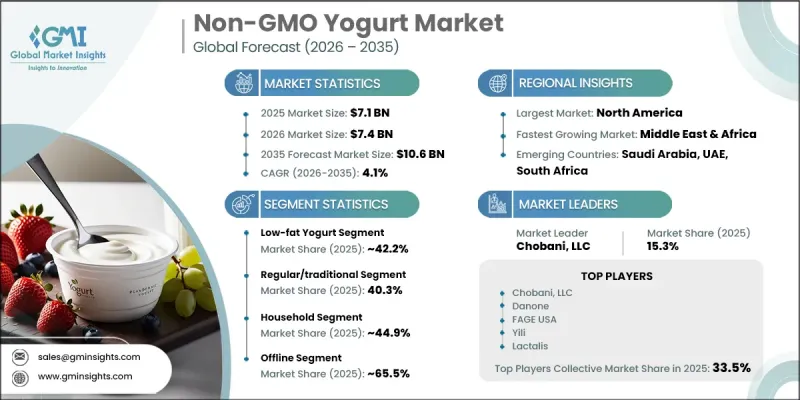

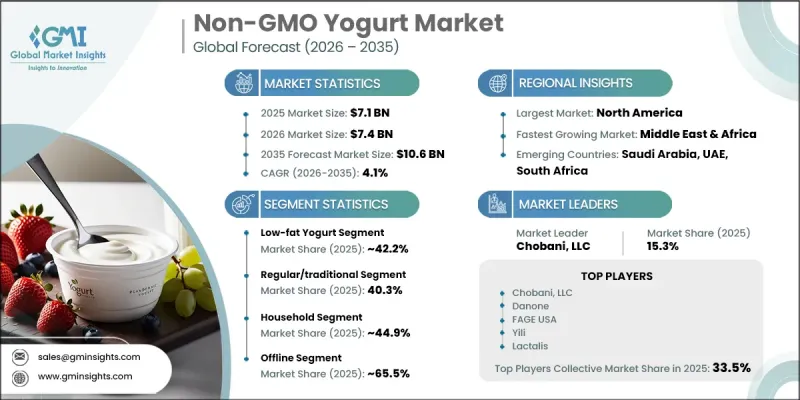

세계의 비유전자 변형 요거트 시장은 2025년에 71억 달러로 평가되었고 CAGR 4.1%를 나타내 2035년까지 106억 달러에 이를 것으로 추정되고 있습니다.

소비자들이 일상적인 식생활에서 건강 지향적인 식습관과 더 깨끗한 원료 구성을 점점 더 중요시함에 따라 시장은 꾸준히 성장하고 있습니다. 식품의 품질, 영양 성분의 투명성, 장기적인 건강에 대한 인식이 높아지면서 천연 유제품으로의 전환이 가속화되고 있습니다. 또한, 보다 안전하고, 가공을 최소화하고, 유전자 변형 성분을 포함하지 않은 식품에 대한 선호도가 높아진 것도 수요를 뒷받침하고 있습니다. 또한, 소비자들은 윤리적 조달과 지속 가능한 농업 관행에 따라 생산된 유제품에 대한 관심이 높아지고 있습니다. 이 카테고리는 기능성 영양과 소화 용이성이 구매의 주요 요인이 되고 있는 식습관 변화의 수혜를 받고 있습니다. 또한, 가처분 소득 증가와 도시 생활양식의 변화로 인해 프리미엄 유제품의 소비 확대가 촉진되고 있습니다. 시장 진출기업들은 원재료의 품질을 확보하면서 맛, 식감, 영양가 향상을 목표로 지속적인 제품 개발에 힘쓰고 있습니다. 소매점 판매망 확대와 강력한 브랜딩 전략도 이 카테고리의 인지도 향상에 기여하고 있습니다. 전반적으로, 이 시장은 건강 지향적인 소비 패턴과 전 세계 소비자층의 클린 라벨 유제품 대체품에 대한 수요 증가에 힘입어 장기적으로 꾸준한 성장이 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 71억 달러 |

| 예측 금액 | 106억 달러 |

| CAGR | 4.1% |

2025년에는 일반/전통 부문이 40.3%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 2.9%를 나타낼 것으로 예측됩니다. 이 부문은 소비자의 폭넓은 수용성, 친숙한 맛, 그리고 높은 영양학적 평가로 인해 지속적으로 선두를 유지하고 있습니다. 자연스럽고 크리미한 맛과 단백질 함량으로 건강을 중시하는 소비자뿐만 아니라 균형 잡힌 일일 영양을 원하는 소비자들에게도 선호되는 제품입니다. 이 부문은 접근성이 용이하고 유제품 카테고리에서 확고한 위치를 차지하고 있어 모든 연령층에서 안정적인 수요를 유지하고 있습니다.

오프라인 유통 채널은 2025년 65.5%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 4.2%를 나타낼 것으로 예측됩니다. 소비자들이 상품을 직접 확인할 수 있고 즉각적인 가용성을 선호하기 때문에 오프라인 매장은 여전히 주요 구매 채널로 남아 있습니다. 슈퍼마켓, 전문점, 편의점은 제품 인지도 향상과 신뢰 구축에 있어 중요한 역할을 계속하고 있습니다. 또한, 오프라인 소매는 체계적인 상품 배치, 판촉 활동, 인증된 유제품에 쉽게 접근할 수 있다는 장점이 있어 안정적인 판매 실적을 뒷받침하고 있습니다.

북미의 비유전자 변형 요거트 시장은 2025년 33.2%의 점유율을 차지했습니다. 이 지역의 성장은 영양, 원재료의 투명성, 지속 가능한 식품 조달에 대한 소비자의 높은 인식에 힘입어 성장하고 있습니다. 미국은 높은 식품 품질 기준과 프리미엄 유제품 대체품에 대한 수요 증가로 인해 지역 내 소비를 주도하고 있습니다. 이 지역의 소비자들은 천연 성분, 높은 영양가 및 기능적 이점을 중시하는 요구르트 제품을 점점 더 선호하고 있으며, 이는 이 카테고리의 지속적인 확장을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 지방 함유량별(2022-2035년)

제6장 시장 규모 및 예측 : 제품 유형별(2022-2035년)

제7장 시장 규모 및 예측 : 용도별(2022-2035년)

제8장 시장 규모 및 예측 : 유통 채널별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.06.10The Global Non-GMO Yogurt Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 10.6 billion by 2035.

The market is witnessing steady expansion as consumers increasingly prioritize health-focused eating patterns and cleaner ingredient profiles in daily diets. Rising awareness regarding food quality, nutrition transparency, and long-term wellness is strengthening the shift toward naturally derived dairy products. Demand is further supported by the growing preference for food options that are perceived to be safer, minimally processed, and free from genetically altered components. Consumers are also showing stronger inclination toward dairy products that align with ethical sourcing and sustainable agricultural practices. The category benefits from evolving dietary habits, where functional nutrition and digestive comfort are becoming central purchasing factors. In addition, rising disposable incomes and urban lifestyle changes are encouraging higher consumption of premium dairy offerings. Market participants are responding with continuous product development efforts aimed at improving taste, texture, and nutritional value while ensuring ingredient integrity. Expanding retail penetration and stronger branding strategies are also contributing to category visibility. Overall, the market is positioned for consistent long-term growth driven by wellness-oriented consumption patterns and increasing demand for clean-label dairy alternatives across global consumer segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $10.6 Billion |

| CAGR | 4.1% |

The regular/traditional segment accounted for 40.3% share in 2025 and is forecasted to grow at a CAGR of 2.9% between 2026 and 2035. This segment continues to lead due to its widespread consumer acceptance, familiar taste profile, and strong nutritional perception. Its naturally creamy consistency and protein content make it a preferred choice among health-focused consumers as well as those seeking balanced daily nutrition. The segment maintains steady demand across age groups due to its accessibility and established presence in the dairy category.

The offline distribution channel held a 65.5% share in 2025 and is projected to grow at a CAGR of 4.2% through 2035. Physical retail formats remain the primary purchasing channel due to consumer preference for direct product evaluation and immediate availability. Supermarkets, specialty outlets, and convenience stores continue to play a key role in driving product visibility and trust. Offline retail also benefits from structured product placement, promotional activities, and easier access to verified dairy options, supporting consistent sales performance.

North America Non-GMO Yogurt Market accounted for a 33.2% share in 2025. Growth in this region is driven by strong consumer awareness regarding nutrition, ingredient transparency, and sustainable food sourcing. The United States leads regional consumption due to established food quality standards and rising demand for premium dairy alternatives. Consumers in the region increasingly prefer yogurt products that emphasize natural composition, high nutritional value, and functional benefits, supporting sustained category expansion.

Major players operating in the Global Non-GMO Yogurt Industry include Danone US, LLC, Yili Group, Brown Cow Yogurt, Lactalis, FAGE USA, Chobani, LLC, Wallaby Organic, Maia Yogurt, Nancy's Yogurt, Maple Hill Creamery, Junlebao Dairy, Mengniu Dairy, The Greek Gods. Companies operating in the non-GMO yogurt market are focusing on strengthening product innovation by improving taste profiles, nutritional density, and ingredient sourcing transparency. Many players are expanding their portfolios with premium dairy offerings to meet rising demand for healthier food alternatives. Strategic investments in branding and consumer education are helping build stronger trust in clean-label positioning. Manufacturers are also enhancing distribution networks across retail and online channels to increase product availability. Partnerships with suppliers supporting sustainable dairy farming practices are gaining importance to reinforce ethical sourcing. In addition, firms are prioritizing packaging improvements to enhance shelf appeal and product differentiation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fat content

- 2.2.3 Product type

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Size and Forecast, By Fat Content, 2022-2035 (USD Billion, Tons)

- 5.1 Key trends

- 5.2 Full-fat yogurt

- 5.3 Low-fat yogurt

- 5.4 Non-fat yogurt

Chapter 6 Market Size and Forecast, By Product Type, 2022-2035 (USD Billion, Tons)

- 6.1 Key trends

- 6.2 Regular yogurt

- 6.3 Greek/strained yogurt

- 6.4 Protein-fortified yogurt

- 6.5 Drinkable yogurt

- 6.6 Others

Chapter 7 Market Size and Forecast, By Application, 2022-2035 (USD Billion, Tons)

- 7.1 Key trends

- 7.2 Household

- 7.3 Foodservice (HoReCa)

- 7.4 Bakery

- 7.5 Sports and fitness centers

- 7.6 Catering services

Chapter 8 Market Size and Forecast, By Distribution channel, 2022-2035 (USD Billion, Tons)

- 8.1 Key trends

- 8.2 Offline

- 8.2.1 Supermarkets/hypermarkets

- 8.2.2 Convenience stores

- 8.2.3 Specialty stores

- 8.2.4 Others

- 8.3 Online retailers

- 8.3.1 E-commerce

- 8.3.2 Company website

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Brown Cow Yogurt

- 10.2 Chobani, LLC

- 10.3 Danone US, LLC

- 10.4 FAGE USA

- 10.5 Junlebao Dairy

- 10.6 Lactalis

- 10.7 Maia Yogurt

- 10.8 Maple Hill Creamery

- 10.9 Mengniu Dairy

- 10.10 Nancy's Yogurt

- 10.11 The Greek Gods

- 10.12 Wallaby Organic

- 10.13 Yili Group