|

시장보고서

상품코드

2061370

농업용 분무기 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Agricultural Sprayers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

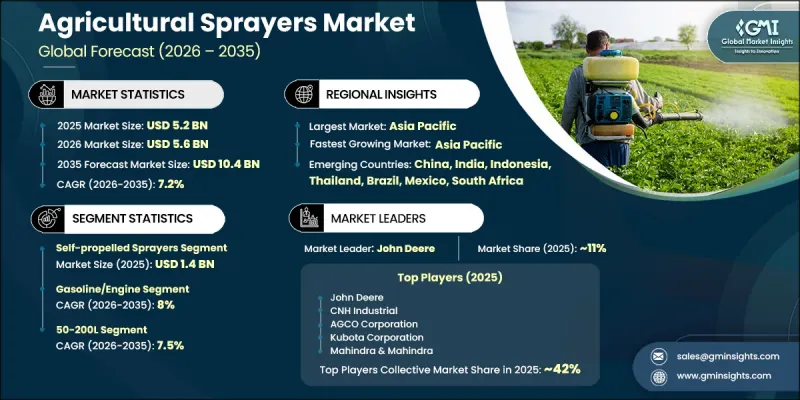

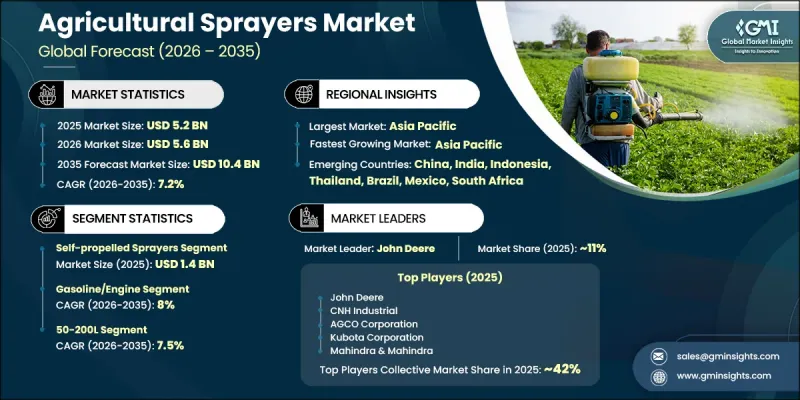

세계의 농업용 분무기 시장은 2025년에 52억 달러로 평가되고 CAGR 7.2%로 성장하며, 2035년까지 104억 달러에 달할 것으로 추정되고 있습니다.

시장의 성장은 정밀농업의 실천이 널리 보급되고 있으며, 효율적인 작물 보호 기법에 대한 관심이 높아지고 있는 데 힘입고 있습니다. 살포 기술은 작물 보호, 시비, 해충 방제 등 각 활동에서 살포 정밀도 향상, 작업 시간 단축, 화학 약품 낭비 최소화를 실현하기 위해 널리 받아들여지고 있습니다. 농업용 분무기는 현대 농업 시스템에서 없어서는 안 될 요소가 되었습니다. 특히 아프리카, 아시아·태평양, 라틴아메리카 등 개발도상 지역에서 효율적인 작물 보호가 농업 생산성 유지와 식량안보 확보에 중요한 역할을 하고 있으므로 그 중요성은 더욱 커지고 있습니다. 농업기계화를 촉진하기 위한 정부의 지원 프로그램과 농업기계 도입에 대한 재정적 인센티브 역시 시장 확대를 가속화하고 있습니다. 또한 세계 인구 증가와 식량 수요 증가로 인해 농업 생산량 증대가 그 어느 때보다 절실해지고 있습니다. 농업용 분무기는 합리적인 가격을 유지하면서 생산성을 높임으로써 중소규모 농가에게 비용 대비 효과가 높은 솔루션을 제공합니다. 휴대용 장치부터 첨단 자가 주행 시스템에 이르기까지 다양한 분무기를 활용할 수 있으므로 농가에서는 수작업 방식의 살포에서 기술적으로 더 발전된 농업 방식으로 전환할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 52억 달러 |

| 예측 시장 규모 | 104억 달러 |

| CAGR | 7.2% |

자주식 분무기 부문은 2025년에 26.6%의 시장 점유율을 차지하고, 14억 달러 규모의 시장에 도달하며, 2026-2035년 연평균 성장률(CAGR) 6.6%로 성장할 것으로 전망됩니다. 이 부문은 대규모 농업 경영에 적합하므로 확고한 입지를 다지고 있습니다. 이 기계들은 통합 섀시 시스템, 대용량 탱크, 광범위한 살포 붐, 그리고 GPS 내비게이션 및 가변 살포량 시스템과 같은 정밀농업 기술을 갖추고 있습니다. 대규모 상업 농장에서는 작업 효율 향상, 트랙터 탑재형에 비해 토양 다짐 현상이 적으며, 추가 농기계에 의존하지 않고 자율적으로 작동할 수 있다는 점 때문에 자가주행식 살포기가 선호되고 있습니다.

50-200L 부문은 2025년에 29.2%의 시장 점유율을 차지하며, 2026-2035년 연평균 성장률(CAGR) 7.5%로 성장할 것으로 전망됩니다. 이 부문이 주도적인 위치를 차지하고 있는 이유는 전 세계에서, 특히 아시아·태평양, 아프리카, 라틴아메리카와 같이 평균 농지 규모가 비교적 작은 지역에서 중소규모 농장이 집중되어 있기 때문입니다. 휴대용, 배낭형, 컴팩트 마운트형 등 저용량 범주에 속하는 기기는 합리적인 가격과 실용성 덕분에 널리 사용되고 있습니다. 이러한 시스템은 일상적인 살포 작업에 있으며, 효율적이고 비용 대비 효과가 높은 솔루션을 필요로 하는 농가에게 가장 적합합니다.

미국의 농업용 분무기 시장은 2025년에 13억 달러에 달하며, 2026-2035년 연평균 성장률(CAGR) 6.9%로 성장할 것으로 전망됩니다. 시장 확대는 대규모 상업 농업 경영, 넓은 평균 농지 규모, 그리고 정밀농업 기술의 적극적인 도입에 힘입어 이루어지고 있습니다. 곡물 생산, 특수 작물, 원예 등 각 분야에서 수요는 계속해서 높은 수준을 유지하고 있습니다. 농가에서는 GPS 안내 시스템, 가변 살포량 기술, 자동 붐 제어 등 첨단 시스템을 탑재한 자가주행식 살포기에 대한 투자가 증가하고 있습니다. 센서 및 데이터베이스 농업 솔루션의 통합이 진행되고 있는 점도 기술적으로 고도로 발전된 살포 장비에 대한 수요를 더욱 부추기고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품 유형별, 2022-2035년

제6장 시장 추산·예측 : 동력원별, 2022-2035년

제7장 시장 추산·예측 : 기술별, 2022-2035년

제8장 시장 추산·예측 : 용량별, 2022-2035년

제9장 시장 추산·예측 : 사용법별, 2022-2035년

제10장 시장 추산·예측 : 작물 유형별, 2022-2035년

제11장 시장 추산·예측 : 최종사용자별, 2022-2035년

제12장 시장 추산·예측 : 유통 채널별, 2022-2035년

제13장 시장 추산·예측 : 지역별, 2022-2035년

제14장 기업 개요

KSA 26.06.25The Global Agricultural Sprayers Market was valued at USD 5.2 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 10.4 billion by 2035.

Market growth is supported by the rising adoption of precision agriculture practices and the increasing emphasis on efficient crop protection methods. Spraying technologies are gaining widespread acceptance as they improve application accuracy, reduce operational time, and minimize chemical wastage across crop protection, fertilization, and pest control activities. Agricultural sprayers have become an essential component of modern farming systems, particularly as efficient crop protection plays a critical role in sustaining agricultural productivity and ensuring food security across developing regions such as Africa, Asia Pacific, and Latin America. Government support programs promoting farm mechanization and financial incentives for agricultural equipment adoption are also accelerating market expansion. In addition, rising global population levels and increasing food demand are further intensifying the need for higher agricultural output. Agricultural sprayers offer cost-efficient solutions for small and medium-scale farmers by improving productivity while maintaining affordability. The availability of multiple sprayer formats, ranging from portable units to advanced self-propelled systems, is enabling farmers to transition from manual application methods to more technologically advanced farming practices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.2 Billion |

| Forecast Value | $10.4 Billion |

| CAGR | 7.2% |

The self-propelled sprayers segment accounted for 26.6% share in 2025, reaching a value of USD 1.4 billion, and is expected to grow at a CAGR of 6.6% from 2026 to 2035. This segment holds a strong position due to its suitability for large-scale agricultural operations. These machines are equipped with integrated chassis systems, high-capacity tanks, wide spray booms, and precision farming technologies such as GPS-based navigation and variable rate application systems. Large commercial farms prefer self-propelled sprayers as they enhance operational efficiency, reduce soil compaction compared to tractor-mounted alternatives, and operate independently without reliance on additional farm machinery.

The 50-200L segment held 29.2% share in 2025 and is projected to grow at a CAGR of 7.5% from 2026 to 2035. This segment leads due to the high concentration of small and medium-scale farms globally, especially across Asia Pacific, Africa, and Latin America, where average landholding sizes remain relatively limited. Equipment within the low-volume category, including handheld, knapsack, and compact mounted sprayers, is widely adopted due to its affordability and practicality. These systems are well-suited for farmers requiring efficient yet cost-effective solutions for routine spraying operations.

U.S. Agricultural Sprayers Market reached USD 1.3 billion in 2025 and is expected to grow at a CAGR of 6.9% from 2026 to 2035. Market expansion is driven by large-scale commercial farming operations, expansive average farm sizes, and strong adoption of precision agriculture technologies. Demand remains high across grain production, specialty crops, and horticulture. Farmers are increasingly investing in self-propelled sprayers equipped with advanced systems such as GPS guidance, variable rate technology, and automated boom controls. The growing integration of sensors and data-driven farming solutions is further supporting demand for technologically advanced spraying equipment.

Major players operating in the Global Agricultural Sprayers Industry include John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, Mahindra & Mahindra, Bucher Industries (Kuhn Group), CLAAS KGaA, New Holland Agriculture, Massey Ferguson, Valtra, Horsch Maschinen, Jacto, DJI Agriculture, XAG Co., Ltd., Excel Industries, Alamo Group, SDF Group, TAFE Motors & Tractors, Changfa Agricultural Equipment, Lovol Heavy Industries, Yamaha Motor Co., and YTO Group. Companies in the agricultural sprayers market are focusing on strengthening precision agriculture capabilities by integrating GPS, sensor-based systems, and variable rate technology into their product offerings. Manufacturers are investing in automation and smart spraying solutions that enhance accuracy and reduce chemical usage. Expansion of electric and hybrid sprayer models is supporting sustainability goals and lowering operating costs. Firms are also improving durability and machine efficiency to suit diverse farm sizes and climatic conditions. Strategic collaborations with agricultural cooperatives and distribution networks are helping expand market reach. In addition, companies are emphasizing after-sales service, training programs, and digital farm management integration to enhance customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Power Source

- 2.2.4 Technology

- 2.2.5 Capacity

- 2.2.6 Usage

- 2.2.7 Crop Type

- 2.2.8 End User

- 2.2.9 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.3.1 Price volatility and market unpredictability

- 3.3.2 Quality assurance and equipment reliability concerns

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.6.3 Average Selling Price by Product Type & Capacity

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Paid Database)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 HS Code Classification & Trade Flow Analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Traditional Spraying Methods

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Farm Size

- 3.11.3 Risks, Limitations & Regulatory Considerations for AI-Enabled Sprayers

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Manufacturing Capacity by Region & Key Producer (Driven by Primary Research)

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Handheld sprayer

- 5.3 Knapsack sprayer

- 5.4 Trailed sprayer

- 5.5 Mounted sprayer

- 5.6 Self-propelled sprayer

- 5.7 Aerial sprayer

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Battery

- 6.3 Gasoline/Engine

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Hydraulic nozzles

- 7.3 Air-assisted electrostatic

- 7.4 Ultra-Low Volume (ULV) spraying

- 7.5 Precision spraying

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Capacity, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Below 50L

- 8.3 50-200L

- 8.4 200-500 L

- 8.5 Above 500L

Chapter 9 Market Estimates & Forecast, By Usage, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Insecticides/Pesticides

- 9.3 Herbicides

- 9.4 Fungicides

- 9.5 Fertilizers

Chapter 10 Market Estimates & Forecast, By Crop Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Cereals & Grains

- 10.3 Oilseeds & Pulses

- 10.4 Fruits & Flowers

- 10.5 Stem & Tubers

- 10.6 Other (Plantation Crops, Forestry, etc.)

Chapter 11 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Small Farmers

- 11.3 Medium Farmers

- 11.4 Large Farms

- 11.5 Institutions & Commercial Farms

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Online

- 12.3 Offline

Chapter 13 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 Japan

- 13.4.3 India

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 Middle East and Africa

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Top Global Player

- 14.1.1 John Deere

- 14.1.2 CNH Industrial

- 14.1.3 Kubota Corporation

- 14.1.4 AGCO Corporation

- 14.1.5 Mahindra & Mahindra

- 14.1.6 Claas Group

- 14.1.7 Bucher Industries (Kuhn Group)

- 14.2 Regional Player

- 14.2.1 Jacto

- 14.2.2 Excel Industries

- 14.2.3 Horsch Maschinen

- 14.2.4 Changfa Agricultural Equipment

- 14.2.5 TAFE Motors & Tractors

- 14.3 Emerging Players

- 14.3.1 DJI Agriculture

- 14.3.2 XAG Co., Ltd.

- 14.3.3 Yamaha Motor Co. (Agriculture Division)

- 14.3.4 Alamo Group

- 14.3.5 SDF Group

- 14.3.6 New Holland Agriculture

- 14.3.7 Massey Ferguson

- 14.3.8 Valtra

- 14.3.9 YTO Group

- 14.3.10 Lovol Heavy Industries