|

시장보고서

상품코드

2066484

농업용 분무기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agriculture Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

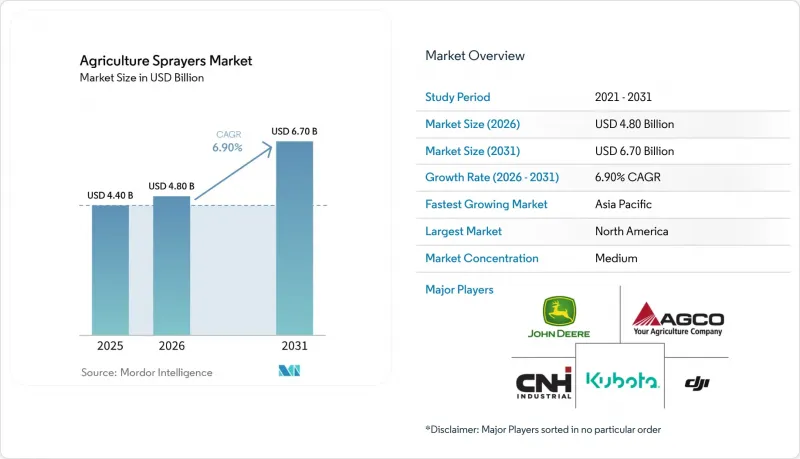

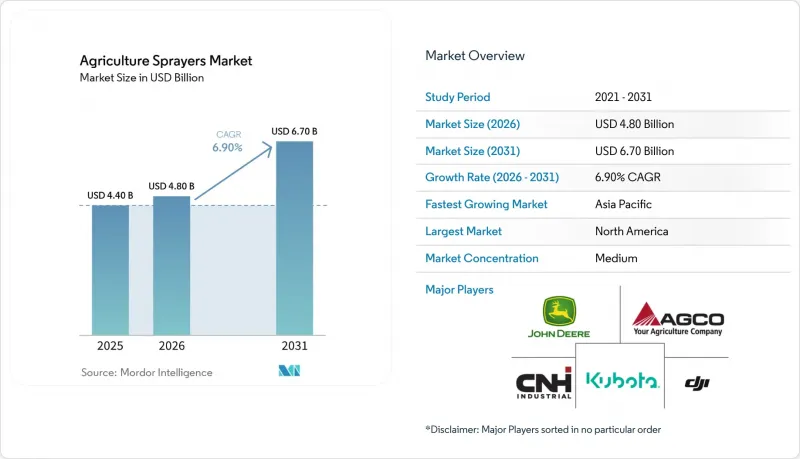

Mordor Intelligence에 의하면, 농업용 분무기 시장 규모는 2025년 44억 달러로 평가되었습니다. 2026년에는 48억 달러에 이르고, 2031년까지 67억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 6.9%를 나타낼 것으로 예측됩니다.

본 보고서는 동력원별(수동식, 태양광 발전식 등), 제품 유형별(트랙터 탑재식 등), 용도별(밭작물 등), 분무 용량별(저용량 등), 기술 수준별(기존 등), 펌프 구조별(다이어프램 펌프 등), 지역별(북미, 아프리카 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 농업용 분무기 시장 동향 및 분석

농약 사용량 증가

농약 살포 빈도가 증가하고 있는 것이 농업용 분무기 시장의 기본적인 장비 수요를 지속적으로 견인하고 있습니다. 미국 농무부 경제조업체국(USDA, ERS)에 따르면, 2024년 및 2025년 미국의 제초제 내성 대두 재배 면적은 전체 재배 면적의 96%를 차지했으며, 대규모 농업 시스템에서 작물 보호용 화학 약품 살포에 대한 의존이 여전히 지속되고 있음을 여실히 보여주고 있습니다. 광역 작물의 살포 빈도가 높아짐에 따라 장비의 가동 시간이 늘어나고, 노즐, 펌프, 호스, 붐 어셈블리 등의 부품 마모가 가속화되고 있습니다. 이러한 추세는 농업용 분무기 및 애프터마켓 소모품에 대한 안정적인 교체 수요를 뒷받침하고 있으며, 특히 생육기 동안 여러 차례의 살포가 일반화된 집약적인 줄 재배 지역에서 두드러지게 나타납니다.

센서를 활용한 정밀 살포로 업그레이드

센서를 활용한 업그레이드는 농업용 분무기 시장의 기회를 확대되고 있습니다. 많은 생산자들이 기계 전체를 새로 구입하는 대신, 기존 장비를 사후 개조할 수 있기 때문입니다. Deere &Company사는 2026년형 및 그 이전 모델에 대한 업그레이드 옵션과 붐 구성의 확충을 발표했는데, 이는 사후 개조가 틈새 시장용 해결책이 아니라 중요한 도입 경로로 자리 잡고 있음을 보여줍니다. 감지 정밀도의 향상과 도입 비용의 합리화가 진행됨에 따라, 정밀 살포는 상업 농업 경영에서 단순한 프리미엄 기능에서 표준적인 생산성 향상 도구로 전환되고 있습니다.

막대한 초기 투자와 자금 조달의 장벽

자본 비용은 농업용 살포기 시장에 있어 여전히 큰 과제로 남아 있습니다. 특히, 2-3시즌 이내에 첨단 장비에 대한 투자 비용을 회수하지 못하는 농장의 경우라면 더욱 그렇습니다. EXEL Industries사는 2024-2025 회계연도 상반기 농업용 살포기 관련 매출이 15.7% 감소했다고 보고했으며, 북미 시장의 부진에 대해서는 경제 전망이 불투명하여 농가들이 신중한 태도를 보이고 있는 것이 원인이라고 지적했습니다. 이 과제는 AI 탑재형 및 자율형 기기 분야에서 더욱 두드러집니다. 이 분야에서는 구매 결정 시 단일 기계 비용뿐만 아니라 하드웨어, 소프트웨어 및 서비스 비용을 종합적으로 고려하는 경우가 많기 때문입니다. 이 때문에 업그레이드를 통해 얻을 수 있는 기술적 이점이 분명하더라도, 일부 생산자들은 기존 장비를 개조하거나, 장비 교체를 미루거나, 외부 서비스 제공업체에 의존하는 경향을 보입니다. 대출 조건 완화나 리스 모델의 보급이 진전되지 않는 한, 몇몇 주요 농업 지역에서는 첨단 기술 도입률이 잠재적 수준에 미치지 못한 채 머물 가능성이 높습니다.

부문별 분석

2025년, 농업용 분무기 시장에서 연료 구동형 부문 시장 점유율은 36.0%로 가장 높은 비중을 차지했습니다. 이 분무기들은 가동 시간이 길고, 광활한 농지에서 대규모 붐이나 자가주행용으로 사용하기에 적합하기 때문에 그 우위를 유지하고 있습니다. 북미, 남미, 유럽 등의 지역에서는 농지 규모가 크기 때문에 제한된 살포 기간 동안 중단 없이 살포를 진행해야 하므로, 이러한 분무기가 널리 선호되고 있습니다. 수동식 및 태양광 보조식 시스템은 소규모 농가와 온실 재배 분야에서 여전히 틈새 시장을 차지하고 있습니다. 이 부문의 안정성은 주요 농업 경제권 내의 확고한 유통업체 네트워크, 유지보수 노하우, 그리고 기존 연료 인프라에 의해 더욱 뒷받침되고 있습니다.

농업용 분무기 시장에서 배터리 구동 부문 시장 규모는 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 12.1%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 이러한 성장은 드론 및 경량 자율형 플랫폼의 도입 확대와 리튬 이온 배터리의 효율 향상에 힘입어 이루어지고 있습니다. 배터리 구동 시스템은 과수원에서의 살포, 온실 작업 및 좁은 농지에서 점점 더 적합해지고 있으며, 저소음과 배기가스 저감이 큰 장점으로 꼽히고 있습니다. 또한, 각 제조업체는 정밀도와 성능을 향상시키기 위해 디지털 모니터링 및 자동 살포 시스템을 배터리 구동 플랫폼에 통합하고 있습니다. 이러한 성장에도 불구하고, 생산성을 유지하기 위해 장시간 가동해야 하는 대용량 작물 보호 용도의 경우, 연료 구동 시스템은 여전히 필수적입니다.

2025년에는 트랙터 탑재형 시스템이 41.4%로 가장 높은 점유율을 차지했습니다. 이러한 살포기는 기존 트랙터 군과의 원활한 통합과 정밀 살포 기술 도입에 따른 높은 비용 효율성 덕분에 확고한 입지를 유지하고 있습니다. 이 제품들은 북미와 유럽에서 널리 사용되고 있으며, 확립된 농업 기계 인프라가 안정적인 교체 수요를 뒷받침하고 있습니다. 또한, 견인식 및 자가주행식 살포기는 더 큰 탱크 용량과 더 넓은 붐 살포 범위가 필요한 대규모 농지 작업에서 여전히 중요한 역할을 하고 있습니다. 이 부문은 탄탄한 애프터마켓 지원, 유지보수의 용이성, 그리고 상업 농업에서 일반적으로 사용되는 안내 기술 및 사후 장착 기술과의 호환성 등의 장점을 가지고 있습니다.

무인 항공기(UAV) 살포기는 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 28.1%라는 가장 빠른 속도로 성장할 것으로 전망됩니다. 이러한 성장은 노동력 부족의 심화, 정밀 살포에 대한 수요 증가, 그리고 과수원, 논, 특산 작물 분야에서 항공 살포의 보급 확대에 힘입어 이루어지고 있습니다. 무인항공기(UAV) 살포기에는 지형에 대한 적응성, 인력 의존도 감소, 살포 가능 기간이 짧은 시기에 신속한 전개가 가능하다는 등의 장점이 있습니다. 각 제조업체는 훈련 지원, 차량 관리 소프트웨어, 자율 경로 계획 시스템을 제공함으로써 상업적 도입을 촉진하고 있습니다. 지상형 살포기가 여전히 전 세계 도입 대수에서 높은 비중을 차지하는 반면, 속도, 표적에 대한 살포 정밀도, 그리고 운용 효율이 농업 종사자들에게 큰 경제적 가치를 가져다주는 용도에서는 드론 시스템의 도입이 점점 더 확대되고 있습니다.

지역별 분석

2025년에는 북미가 32.0%로 가장 큰 점유율을 차지했습니다. 이러한 선도적 지위는 옥수수, 대두, 밀, 카놀라 등의 작물을 대상으로 한 대규모 생산 시스템에 기인하며, 이러한 작물에는 대용량 살포 작업이 필요합니다. 미국에서는 자가주행형 살포기, 정밀 살포 기술, 디지털 농장 관리 시스템의 광범위한 도입을 통해 지역 수요를 견인하고 있습니다. 캐나다도 큰 기여를 하고 있으며, 대규모 상업용 곡물 생산에서는 광범위한 농경지를 커버할 수 있는 첨단 살포 장비가 필수적입니다. 확립된 딜러 네트워크, 정기적인 장비 교체 주기, 정밀 농업 기술의 적극적인 도입과 같은 요인들이 해당 지역의 대규모 상업 농업 사업 전반에 걸쳐 첨단 농업용 살포 플랫폼에 대한 안정적인 수요를 지속적으로 뒷받침하고 있습니다.

아시아태평양은 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 8.5%를 기록하며 가장 높은 성장률을 보일 것으로 전망됩니다. 이러한 성장은 농업 기계화의 진전, 농업용 드론 도입 확대, 그리고 정밀 농업 기술에 대한 정부 지원 확대에 힘입어 이루어지고 있습니다. 중국은 식물 보호용 드론 및 스마트 농업 기술을 장려하는 보조금 프로그램을 통해 농업 기계의 현대화를 추진하고 있습니다. 인도, 일본, 호주에서도 인력 부족과 기복이 심한 지형으로 인해 항공 살포의 경제적 가치가 높아지고 있어, 무인항공기(UAV) 살포 시스템의 도입이 확대되고 있습니다. 지역 제조업체들은 작업자 교육, 딜러 지원, 디지털 살포 생태계 확충에 주력하고 있으며, 아시아태평양은 전 세계적으로 볼 때 첨단 농업용 살포 솔루션의 생산 및 개발 분야에서 성장의 거점으로서의 입지를 확고히 하고 있습니다.

유럽은 여전히 규제 체계의 영향을 받는 성숙한 시장이며, 규정 준수 요건 및 살포 제어 기능의 개선에 따라 장비의 정기적인 교체가 진행되고 있습니다. 유럽집행위원회가 2025년 12월에 제시한 규제 간소화안에서는 특정 위험 조건 하에서 드론에 대한 일반적인 적용 예외 조항이 도입될 가능성이 시사되었으며, 2026년 이후 무인항공기(UAV)를 활용한 살포 시장의 확대가 예상됩니다. 남미에서는 브라질의 방대한 상업 농업 기반과 트랙터 탑재형 및 자행식 장비에 대한 활발한 수요 덕분에 이 지역이 중요한 위치를 차지하고 있습니다. 한편, 중동 및 아프리카는 아직 발전의 초기 단계에 있지만, 식량 안보 목표와 수출 잔류 기준이 선택적인 정밀화 개선을 촉진하고 있어 그 중요성이 커지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the agriculture sprayers market size is projected to grow from USD 4.4 billion in 2025 to USD 4.8 billion in 2026 and USD 6.7 billion by 2031, registering a CAGR of 6.9% from 2026 to 2031.

This report is Segmented by Source of Power (Manual, Solar-Powered, and More), by Product Type (Tractor-Mounted, and More), by Application (Field Crops And, More), by Spray Volume (Low Volume and More), by Technology Level (Conventional and More), by Pump Mechanism (Diaphragm Pumps and More), and by Geography (North America, Africa and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Agriculture Sprayers Market Trends and Insights

Growth in Agrochemical Usage

Increasing pesticide application intensity continues to drive baseline equipment demand in the agriculture sprayers market. According to the United States Department of Agriculture Economic Research Service (USDA, ERS), herbicide-tolerant soybean acreage in the United States accounted for 96% of the planted area in 2024 and 2025, highlighting the ongoing reliance on crop protection chemical applications in large-scale farming systems. Higher spraying frequency in broadacre crops leads to increased equipment operating hours and accelerates wear on components such as nozzles, pumps, hoses, and boom assemblies. This trend supports consistent replacement demand for agricultural sprayers and aftermarket consumable components, particularly in intensive row-crop production regions where multiple spray applications are standard during the growing season.

Precision Spraying Upgrades Using Sensors

Sensor-based upgrades are expanding opportunities in the agriculture sprayers market, as many growers can retrofit their existing equipment instead of replacing entire machines. Deere & Company has introduced expanded upgrade options and boom configurations for Model Year 2026 equipment and earlier models, indicating that retrofitting is becoming a significant adoption pathway rather than a niche solution. As sensing accuracy improves and installation costs become more justifiable, precision spraying is transitioning from a premium feature to a standard productivity tool for commercial farming operations.

High Upfront Capital Expenditure and Financing Hurdles

Capital costs continue to pose a significant challenge for the agriculture sprayers market, particularly for farms unable to recoup the investment in advanced equipment within two to three seasons. EXEL Industries reported a 15.7% decline in agricultural spraying revenue during the first half of the fiscal year 2024-2025, attributing the weakness in North America to farmers adopting a cautious approach due to limited economic visibility. The challenge is more pronounced in the segment of AI-enabled and autonomous equipment, where purchase decisions often encompass hardware, software, and service costs rather than a single machine expense. This has led some growers to opt for retrofits, delay equipment replacement, or rely on external service providers, even when the technical benefits of upgrading are evident. Without an easing of credit conditions or broader adoption of leasing models, the uptake of advanced technologies is likely to remain below its potential in several established farming regions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Labor Costs and Operator Shortages

- Government Mechanization and Smart-Farming Subsidies

- Limited Operator and Agronomy Data Skills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The agriculture sprayers market share for the fuel-operated segment held the largest 36.0% in 2025. These sprayers maintain their dominance due to their longer operating endurance and suitability for large boom and self-propelled applications in broadacre farming systems. They are widely preferred in regions such as North America, South America, and Europe, where large field sizes necessitate uninterrupted spraying during narrow application windows. Manual and solar-assisted systems continue to serve niche roles in smallholder agriculture and greenhouse production. The segment's stability is further supported by established dealer networks, maintenance familiarity, and existing fuel infrastructure in major agricultural economies.

The agriculture sprayers market size for the battery-operated segment is forecasted to grow at the fastest 12.1% CAGR from 2026 to 2031. This growth is driven by increasing adoption of drones, lightweight autonomous platforms, and advancements in lithium-ion battery efficiency. Battery-powered systems are becoming increasingly suitable for orchard spraying, greenhouse operations, and compact field applications, where their lower operating noise and reduced emissions offer significant advantages. Manufacturers are also incorporating digital monitoring and automated application systems into battery-operated platforms to enhance precision and performance. Despite this growth, fuel-operated systems remain essential for high-capacity crop protection applications, where extended operating hours are critical for maintaining productivity.

Tractor-mounted systems accounted for the largest 41.4% share in 2025. These sprayers maintain a strong position due to their seamless integration with existing tractor fleets and their cost-effective approach to adopting precision spraying technologies. They are widely used in North America and Europe, where established agricultural machinery infrastructure supports consistent replacement demand. Additionally, trailed and self-propelled sprayers remain relevant for large-scale field operations that require higher tank capacities and wider boom coverage. This segment benefits from robust aftermarket support, easier maintenance, and compatibility with guidance and retrofit technologies commonly used in commercial farming operations.

Unmanned aerial vehicle sprayers are forecasted to expand at the fastest 28.1% CAGR from 2026 to 2031. This growth is driven by increasing labor shortages, rising demand for precision application, and the expanding adoption of aerial spraying in orchards, rice fields, and specialty crops. Unmanned aerial vehicle (UAV) sprayers offer advantages such as terrain adaptability, reduced reliance on labor, and rapid deployment during narrow treatment windows. Manufacturers are enhancing commercial adoption by providing training support, fleet management software, and autonomous route-planning systems. While ground-based sprayers continue to dominate global installed capacity, drone systems are increasingly being adopted for applications where speed, targeted spraying accuracy, and operational efficiency deliver greater economic value to agricultural operators.

Geography Analysis

North America held the largest 32.0% share in 2025. This leadership is attributed to extensive production systems for crops such as corn, soybean, wheat, and canola, which require high-capacity spraying operations. The United States drives regional demand through the widespread adoption of self-propelled sprayers, precision application technologies, and digital farm management systems. Canada also contributes significantly, with large commercial grain operations necessitating advanced spraying equipment capable of high field coverage. Factors such as an established dealer network, recurring equipment replacement cycles, and strong adoption of precision agriculture technologies continue to support stable demand for advanced agricultural spraying platforms across large-scale commercial farming operations in the region.

Asia-Pacific is forecast to grow at the fastest 8.5% CAGR from 2026 to 2031. This growth is driven by increasing farm mechanization, rising deployment of agricultural drones, and expanding government support for precision agriculture technologies. China is advancing agricultural equipment modernization through subsidy programs that promote plant protection drones and smart farming technologies. India, Japan, and Australia are also increasing the adoption of Unmanned Aerial Vehicle (UAV) spraying systems, as labor shortages and challenging terrain enhance the economic value of aerial spraying. Regional manufacturers are focusing on expanding operator training, dealer support, and digital spraying ecosystems, solidifying Asia-Pacific's position as a growing hub for the production and development of advanced agricultural spraying solutions globally.

Europe remains a mature market influenced by regulatory frameworks, where recurring equipment renewal is driven by compliance requirements and improved application control. The European Commission's December 2025 simplification proposal has introduced the possibility of general drone derogations under specific risk conditions, potentially expanding the market for Unmanned Aerial Vehicle (UAV) spraying after 2026. In South America, Brazil's extensive commercial farming base and strong demand for tractor-mounted and self-propelled equipment make the region significant. Meanwhile, the Middle East and Africa, though at an earlier stage, are becoming increasingly relevant as food security objectives and export residue standards encourage selective precision upgrades.

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Limited

- SZ DJI Technology Co., Ltd.

- EXEL Industries

- Maquinas Agricolas Jacto S.A.

- AMAZONEN-WERKE H. DREYER SE & Co. KG

- Bucher Industries AG

- Yamaha Motor Co., Ltd.

- XAG Co., Ltd.

- HORSCH Maschinen GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in agrochemical usage

- 4.2.2 Precision spraying upgrades using sensors

- 4.2.3 Rising labor costs and operator shortages

- 4.2.4 Government mechanization and smart-farming subsidies

- 4.2.5 Artificial Intelligence (AI) spot-spraying economics improve chemical-use payback

- 4.2.6 Growth of specialized drone and orchard spray-service fleets

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure and financing hurdles

- 4.3.2 Limited operator and agronomy data skills

- 4.3.3 Mixed-fleet software and control-system interoperability gaps

- 4.3.4 Battery lifecycle, charging, and uptime constraints in peak spray windows

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Source of Power

- 5.1.1 Manual

- 5.1.2 Battery-Operated

- 5.1.3 Solar-Powered

- 5.1.4 Fuel-Operated

- 5.2 By Product Type

- 5.2.1 Handheld

- 5.2.2 Tractor-Mounted

- 5.2.3 Trailed

- 5.2.4 Self-Propelled

- 5.2.5 Unmanned Aerial Vehicle Sprayers

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Spray Volume Capacity

- 5.4.1 Ultra-Low Volume

- 5.4.2 Low Volume

- 5.4.3 High Volume

- 5.5 By Technology Level

- 5.5.1 Conventional

- 5.5.2 Precision and GPS-Guided

- 5.5.3 Artificial Intelligence-Enabled and Autonomous

- 5.6 By Pump Mechanism

- 5.6.1 Diaphragm Pumps

- 5.6.2 Piston Pumps

- 5.6.3 Centrifugal Pumps

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 Australia

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra Limited

- 6.4.6 SZ DJI Technology Co., Ltd.

- 6.4.7 EXEL Industries

- 6.4.8 Maquinas Agricolas Jacto S.A.

- 6.4.9 AMAZONEN-WERKE H. DREYER SE & Co. KG

- 6.4.10 Bucher Industries AG

- 6.4.11 Yamaha Motor Co., Ltd.

- 6.4.12 XAG Co., Ltd.

- 6.4.13 HORSCH Maschinen GmbH