|

시장보고서

상품코드

2071348

심장 보철 장치 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Cardiac Prosthetic Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

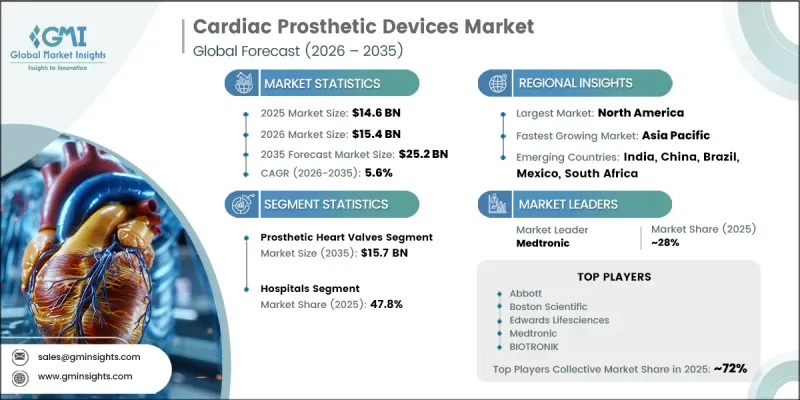

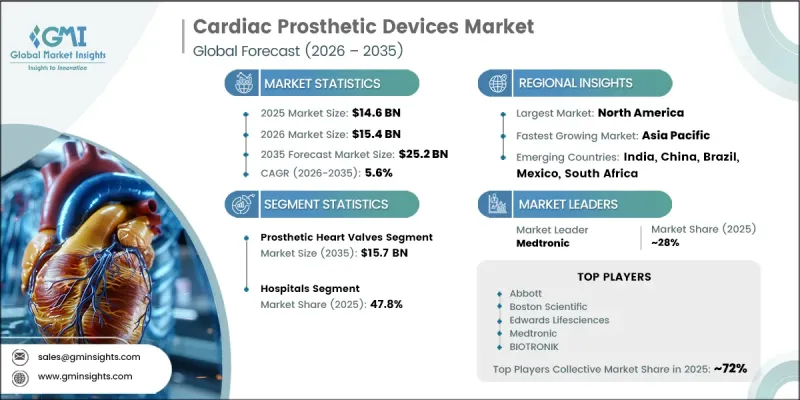

세계의 심장 보철 장치 시장은 2025년에 146억 달러로 평가되었고 CAGR 5.6%로 성장하여 2035년까지 252억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 심혈관 질환 유병률 증가, 최소 침습 심장 수술의 보급 확대, 의료기기 기술의 지속적인 발전, 그리고 전 세계적인 고령화 추세에 힘입어 이루어지고 있습니다. 그 밖의 성장 요인으로는 최신 보철 솔루션에 따른 임상 성과 향상과, 복잡한 심장 중재술에 대응할 수 있는 의료 인프라 확충을 들 수 있습니다. 또한, 이식형 심장 보철 장치에 대한 임상적 의존도가 높아지고 있는 점도 전 세계 의료 시스템에서 수요를 더욱 부추기고 있습니다. 의료기기의 소재, 내구성 및 혈역학적 성능에 대한 기술적 진보 또한 도입률 향상에 기여하고 있습니다. 또한, 심장 질환의 조기 진단 및 치료에 대한 인식이 높아짐에 따라 병원 및 전문 심장 센터의 시술 건수가 지속적으로 증가하고 있으며, 이는 예측 기간 동안 꾸준한 시장 성장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 146억 달러 |

| 예측 금액 | 252억 달러 |

| CAGR | 5.6% |

심장 보철 장치는 심장에 구조적 또는 전기적 이상이 발생했을 때, 정상적인 심장 기능을 회복하거나 대체하도록 설계된 이식형 의료 기술입니다. 이러한 기기에는 주로 인공 심장 판막이나 심박조율기 등의 심장 리듬 관리 시스템이 포함되어 있으며, 심장 판막증, 부정맥, 심부전 등의 치료에 널리 사용되고 있습니다. 경카테터 치료를 포함한 최소 침습 수술의 보급으로 인해, 현대 순환기학 분야의 치료 접근 방식은 크게 변화했습니다. 기기 공학, 생체적합성 재료 및 수술 기술의 지속적인 혁신을 통해 환자의 예후와 시술의 안전성이 더욱 향상되었습니다. 또한, 진단 능력의 확대와 중재적 심장학(심장 카테터 치료) 인프라 구축이 임상 현장에서의 보다 광범위한 도입을 뒷받침하고 있습니다. 특히 고령화 사회에서 심혈관 질환이 전 세계적으로 미치는 부담이 커짐에 따라, 판막 기능 부전이나 부정맥 등의 질환에 대한 첨단 이식형 치료 솔루션의 필요성이 높아지고 있으며, 이것이 지속적인 수요를 이끌고 있습니다.

심장 판막 시장은 2035년까지 157억 달러에 달하고, 2026년부터 2035년까지 연평균 성장률(CAGR) 6.1%로 성장할 것으로 전망됩니다. 이 부문의 성장은 주로 대동맥판막 협착증 및 승모판 역류증을 포함한 심장 판막 질환의 유병률 증가에 힘입은 것입니다. 이러한 질환들은 고령화와 밀접한 관련이 있으며, 대부분의 경우 외과적 또는 경카테터 방식의 판막 치환술이 필요합니다. 첨단 인공판막 솔루션에 대한 임상 현장의 선호도가 높아지고 있는 점도 이 부문의 지속적인 성장을 뒷받침하고 있습니다.

2025년, 병원 부문의 점유율은 47.8%를 차지했습니다. 이 병원은 첨단 인프라, 카테터 검사실, 전문 심장 의료진을 갖추고 있어 심장 인공 장치 수술의 주요 치료 기관으로 자리매김하고 있습니다. 이러한 시설들은 판막 교체술이나 심박조율기 이식술과 같은 복잡한 시술을 수행하는 데 있어 필수적입니다. 환자 수가 많을 뿐만 아니라, 첨단 영상 진단 기술과 수술 기술을 이용할 수 있기 때문에 이 병원은 계속해서 심혈관 치료의 중심 거점으로서의 위상을 유지하고 있습니다.

2025년, 북미의 심장 인공 장치 시장은 43.1%의 점유율을 차지했습니다. 이 지역의 경쟁력은 관상동맥 질환, 심부전, 부정맥, 판막 질환 등 심혈관 질환의 높은 유병률에 기인합니다. 비만, 고혈압, 부적절한 식습관, 운동 부족과 같은 생활 습관과 관련된 위험 요인들이 계속해서 질병의 유병률을 높이고 있습니다. 탄탄한 의료 인프라와 첨단 심장 의료 체계가 해당 지역 전체에서 심장 인공 기기 도입을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제7장 시장 추산 및 예측 : 지역별, 2022-2035년

제8장 기업 개요

JHS 26.07.01The Global Cardiac Prosthetic Devices Market was valued at USD 14.6 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 25.2 billion by 2035.

Market expansion is driven by the rising prevalence of cardiovascular diseases, increasing adoption of minimally invasive cardiac procedures, continuous advancements in device technologies, and a growing geriatric population worldwide. Additional growth factors include improved clinical outcomes associated with modern prosthetic solutions and expanding healthcare infrastructure capable of supporting complex cardiac interventions. The increasing clinical reliance on implantable cardiac support devices is further strengthening demand across global healthcare systems. Technological progress in device materials, durability, and hemodynamic performance is also enhancing adoption rates. Furthermore, rising awareness of early diagnosis and treatment of cardiac conditions continues to support procedural volumes across hospitals and specialized cardiac centers, reinforcing steady market growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.6 Billion |

| Forecast Value | $25.2 Billion |

| CAGR | 5.6% |

Cardiac prosthetic devices are implantable medical technologies designed to restore or replace normal cardiac function when structural or electrical heart abnormalities occur. These devices primarily include prosthetic heart valves and cardiac rhythm management systems such as pacemakers, which are widely used in treating conditions like heart valve disorders, arrhythmias, and heart failure. Growing adoption of minimally invasive procedures, including transcatheter interventions, has significantly reshaped treatment approaches in modern cardiology. Continuous innovation in device engineering, biocompatible materials, and surgical techniques has further improved patient outcomes and procedural safety. In addition, expanding diagnostic capabilities and interventional cardiology infrastructure have supported wider clinical adoption. The rising global burden of cardiovascular diseases, particularly among aging populations, continues to drive sustained demand, as conditions such as valve dysfunction and rhythm disorders increasingly require advanced implantable therapeutic solutions.

The heart valves segment is expected to reach USD 15.7 billion by 2035, advancing at a CAGR of 6.1% during 2026-2035. Growth in this segment is primarily supported by the increasing incidence of valvular heart diseases, including aortic stenosis and mitral regurgitation. These conditions are strongly associated with aging populations and often require surgical or transcatheter valve replacement procedures. Rising clinical preference for advanced prosthetic valve solutions continues to support sustained segment expansion.

The hospitals segment accounted for a share of 47.8% in 2025. Hospitals remain the primary care setting for cardiac prosthetic device procedures due to the availability of advanced infrastructure, catheterization laboratories, and specialized cardiac teams. These facilities are essential for performing complex interventions such as valve replacement and pacemaker implantation. High patient inflow, coupled with access to advanced imaging and surgical technologies, continues to position hospitals as the central hub for cardiovascular treatment.

North America Cardiac Prosthetic Devices Market held a 43.1% share in 2025. The region's dominance is supported by the high burden of cardiovascular diseases, including coronary artery disease, heart failure, arrhythmia, and valvular disorders. Lifestyle-related risk factors such as obesity, hypertension, poor dietary habits, and sedentary behavior continue to contribute to disease prevalence. Strong healthcare infrastructure and advanced cardiac care capabilities further support the adoption of prosthetic cardiac devices across the region.

Prominent players operating in the global cardiac prosthetic devices industry include Abbott, Artivion, BIOTRONIK, Boston Scientific, Colibri Heart Valve, CORCYM, Edwards Lifesciences, Labcor Laboratorios, Lepu Medical, Medtronic, Meril Life Sciences, MicroPort, Pacetronix, and Venus Medtech. Companies in the cardiac prosthetic devices market are strengthening their position through continuous innovation in minimally invasive technologies and next-generation implantable solutions. A major focus remains on improving the durability, biocompatibility, and long-term clinical performance of prosthetic valves and rhythm management devices. Firms are actively investing in research and development to introduce advanced transcatheter systems and patient-specific solutions. Strategic partnerships with hospitals and cardiac centers are expanding clinical adoption and procedural training programs. Manufacturers are also enhancing global distribution networks and regulatory compliance capabilities to accelerate market entry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases globally

- 3.2.1.2 Growing adoption of minimally invasive procedures

- 3.2.1.3 Technological advancements in cardiac prosthetic devices

- 3.2.1.4 Increasing geriatric population and associated cardiac disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and procedures

- 3.2.2.2 Shortage of skilled healthcare professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Advancement in leadless pacemakers and miniaturized device technology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing trend analysis (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Patent analysis (Driven by primary research)

- 3.12 Value chain analysis (Driven by primary research)

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Prosthetic heart valves

- 5.2.1 Mechanical heart valves

- 5.2.2 Tissue heart valves

- 5.2.3 Transcatheter heart valves (TAVR/TMVR)

- 5.3 Pacemakers

- 5.3.1 Implantable pacemakers

- 5.3.1.1 Single-chamber pacemakers

- 5.3.1.2 Dual-chamber pacemakers

- 5.3.1.3 Biventricular/CRT pacemakers

- 5.3.2 External pacemakers

- 5.3.1 Implantable pacemakers

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Specialty cardiac centers

- 6.4 Ambulatory surgical centers

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Artivion

- 8.3 BIOTRONIK

- 8.4 Boston Scientific

- 8.5 Colibri Heart Valve

- 8.6 CORCYM

- 8.7 Edwards Lifesciences

- 8.8 Labcor Laboratorios

- 8.9 Lepu Medical

- 8.10 Medtronic

- 8.11 Meril Life Sciences

- 8.12 MicroPort

- 8.13 Pacetronix

- 8.14 Venus Medtech