|

시장보고서

상품코드

1859654

크레인 렌탈 시장 : 유형별, 리프팅 능력별, 최종 이용 산업별, 지역별 - 예측(-2030년)Crane Rental Market by Type (Fixed Cranes, Mobile Cranes), Weightlifting Capacity (Low, Low to Medium, Heavy, Extremely Heavy), End-use Industry (Building & Construction, Infrastructure, Other End-use Industries), and Region - Global Forecast to 2030 |

||||||

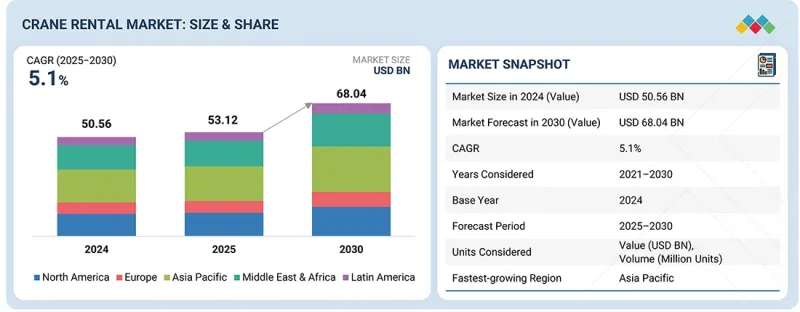

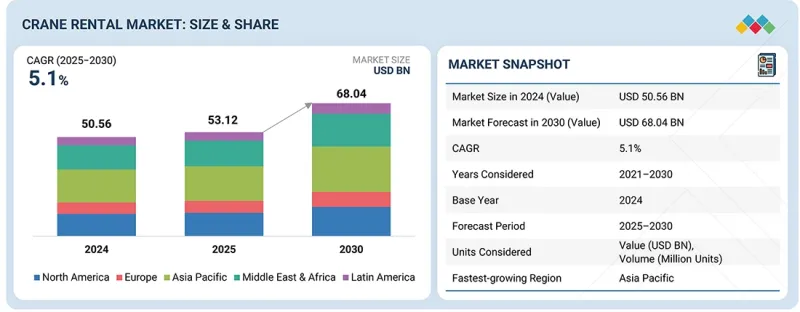

크레인 렌탈 시장 규모는 2025년 531억 2,000만 달러에서 2030년에는 680억 4,000만 달러에 달할 것으로 예측되며, 2025년부터 2030년까지 CAGR은 5.1%로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러), 수량(100만 대) |

| 부문 | 유형별, 리프팅 능력별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

크레인 렌탈 분야는 전 세계적으로 건설 및 인프라 개발이 증가함에 따라 성장이 예상됩니다. 크레인 소유에는 많은 초기 비용과 지속적인 유지보수 비용이 들기 때문에 많은 기업들이 크레인 구매보다 렌탈을 선호하고 있습니다. 또한, 신재생에너지, 석유 및 가스, 각종 산업 프로젝트가 활성화되면서 크레인 렌탈 수요가 증가하고 있습니다.

이동식 크레인 분야는 높은 유연성과 빠른 속도로 현장을 이동하는 능력으로 인해 예측 기간 동안 크레인 렌탈 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다. 이동식 크레인은 건설 및 산업 유지보수 등 다양한 용도로 사용할 수 있습니다. 이동식 크레인은 설치가 간편하고 다재다능하기 때문에 렌탈업체와 건설업체들이 선호하고 있습니다.

크레인은 운반, 사용 및 유지보수가 용이하고 단기적으로 사용하기에 저렴하기 때문에 예측 기간 동안 크레인 렌탈 시장에서 저하중 용량 부문이 가장 높은 CAGR을 기록할 것으로 예상됩니다. 또한 소형이기 때문에 공간이 제한된 도시 지역의 건설 현장에서도 사용할 수 있습니다.

건설 현장에서는 자재 리프팅 및 취급을 위해 크레인이 필요하기 때문에 건축 및 건설 부문은 크레인 렌탈 시장에서 가장 큰 최종 사용 산업입니다. 주거, 상업, 공공 인프라 프로젝트의 빠른 속도로 인해 크레인 수요가 증가하고 있습니다. 크레인 대여를 통해 건설회사는 많은 투자를 하지 않고도 비용을 관리하고 최신 설비를 이용할 수 있습니다.

아시아태평양은 높은 도시화율, 산업화, 대규모 인프라 지출로 인해 크레인 렌탈 시장에서 높은 성장세를 보이고 있습니다. 중국, 인도, 인도네시아 등의 국가들은 건설 및 운송 공사에 많은 투자를 하고 있습니다. 정부의 스마트 시티 및 재생에너지 계획도 크레인 대여에 대한 수요를 증가시키고 있습니다.

대상 기업 : Liebherr(독일), United Rentals Inc.(미국), PALFINGER AG(오스트리아), Sarens NV(벨기에), Mammoet(네덜란드), The Manitowoc Company, Inc.(미국) 등을 다루고 있습니다.

크레인 렌탈 시장의 주요 업체들의 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석도 수록되어 있습니다.

조사 대상

이 보고서는 크레인 렌탈 시장을 유형(이동식 크레인, 고정식 크레인), 중량(저중량, 중저중량, 중량, 초중량), 최종사용 산업(건축/건설, 인프라, 석유/가스, 에너지/전력, 해양/해상, 광업/시추, 운송, 기타 최종사용 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)을 기준으로 분류하고 있습니다. 보고서 범위는 크레인 렌탈 시장의 성장에 영향을 미치는 촉진요인, 시장 억제요인, 과제 및 기회에 대한 자세한 정보를 다룹니다. 주요 업계 진출업체를 상세히 분석하여 사업 개요, 제공 제품, 크레인 렌탈 시장 관련 제휴, 제품 출시, 사업 확장, 인수 등 주요 전략에 대한 인사이트를 제공합니다. 본 보고서는 크레인 렌탈 시장 생태계에서 향후 신흥 기업의 경쟁 분석을 다루고 있습니다.

이 보고서는 시장 리더/신규 진입자에게 전체 크레인 렌탈 시장 및 하위 부문의 수익 수에 대한 가장 가까운 근사치에 대한 정보를 제공합니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 사업 포지셔닝을 개선하고, 적절한 시장 진입 전략을 계획하는 데 도움이 될 것입니다. 이 보고서는 이해관계자들이 시장을 이해하고 주요 시장 촉진요인, 과제 및 기회에 대한 정보를 제공하는 데 도움이 될 것입니다.

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 미충족 수요와 공백

- 상호 접속된 시장과 분야 횡단적인 기회

제6장 업계 동향

- Porter's Five Forces 분석

- 거시경제 분석

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 2025-2026년의 주요 회의와 이벤트

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 투자와 자금 조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세가 크레인 렌탈 시장에 미치는 영향

제7장 기술, 특허, 디지털, AI의 도입별 전략적 파괴

- 주요 기술

- 보완적 기술

- 인접 기술

- 기술/제품 로드맵

- 특허 분석

- 향후 응용

- AI/생성형 AI가 크레인 렌탈 시장에 미치는 영향

- 성공 사례와 실세계에 대한 응용

제8장 지속가능성과 규제 상황

- 지역 규제와 컴플라이언스

- 지속가능성에 대한 대처

- 지속가능성에 대한 영향과 규제 정책의 대처

- 인증, 라벨, 환경기준

제9장 고객 상황과 구매 행동

- 의사결정 프로세스

- 구매자 이해관계자와 구입 평가 기준

- 채용 장벽과 내부 과제

- 다양한 최종 이용 산업으로부터의 미충족 수요

- 시장 수익성

제10장 크레인 렌탈 시장(유형별)

- 소개

- 고정식 크레인

- 이동식 크레인

제11장 크레인 렌탈 시장(리프팅 능력별)

- 소개

- 저

- 저-중

- 중

- 초중량

제12장 크레인 렌탈 시장(최종 이용 산업별)

- 소개

- 건축·건설

- 인프라

- 석유 및 가스

- 에너지와 전력

- 선박·오프쇼어

- 광업과 굴착

- 운송

- 기타

제13장 크레인 렌탈 시장(지역별)

- 소개

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 스웨덴

- 오스트리아

- 스위스

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제14장 경쟁 구도

- 개요

- 주요 진출 기업 전략/강점

- 매출 분석

- 시장 점유율 분석

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 진출 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제15장 기업 개요

- 주요 진출 기업

- UNITED RENTALS, INC.

- LIEBHERR

- PALFINGER AG

- SARENS NV

- MAMMOET

- THE MANITOWOC COMPANY INC.

- MAXIM CRANE WORKS

- ACTION CONSTRUCTION EQUIPMENT LTD.

- LEAVITT CRANES

- WASEL GMBH

- 기타 기업

- WELDEX(INTERNATIONAL) OFFSHORE LTD.

- MEDIACO GROUP

- BUCKNER HEAVYLIFT CRANES, LLC

- VMS EQUIPMENT

- DAIKYO KENKI CO., LTD.

- EUROGRUAS

- SHINSEI MACHINERY CO., LTD.

- AMERICAN CRANE RENTAL, INC.

- SANGHVI MOVERS LIMITED

- DEEP SOUTH CRANE & RIGGING LLC

- STARLOG ENTERPRISES LIMITED

- MYCRANE

- LAMPSON INTERNATIONAL LLC

- IMPERIAL CRANES

- BKL BAUKRAN LOGISTIK GMBH

제16장 부록

KSM 25.11.17The crane rental market size is projected to reach USD 68.04 billion by 2030 from USD 53.12 billion in 2025, at a CAGR of 5.1% from 2025 to 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) Volume (Million Units) |

| Segments | Type, Weightlifting Capacity, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

The crane rental sector is expected to grow due to rising construction and infrastructure development worldwide. Many companies prefer renting cranes over purchasing them because of the significant initial costs and ongoing maintenance expenses associated with ownership. Additionally, the demand for crane rentals is increasing as a result of heightened activity in renewable energy, oil and gas, and various industrial projects.

"Mobile cranes segment is projected to exhibit the highest CAGR from 2025 to 2030"

The mobile cranes segment is expected to record the highest CAGR in the crane rental market during the forecast period, owing to their high flexibility and ability to move around job sites at high speed. Mobile cranes can be used in a wide variety of applications, including construction and industrial maintenance. They are easy to set up and versatile, and hence, they are preferred by rental companies and contractors.

"Low weightlifting capacity segment is projected to exhibit the highest CAGR during the forecast period"

The low weightlifting capacity segment is expected to record the highest CAGR in the crane rental market during the forecast period since they are simple to carry, use, and maintain, and they are affordable when used on a short-term basis. They are also small in size and can be used in urban construction sites where space is limited.

"Building & construction segment is projected to account for the largest market share in 2030"

The building & construction segment is the largest end-use industry in the crane rental market, as construction sites need cranes to lift and handle materials. The rapid pace of residential, commercial, and public infrastructure projects increases the demand for cranes. Renting cranes helps construction companies manage costs and access modern equipment without making significant investments.

"The Asia Pacific crane rental market is projected to grow at the highest CAGR during the forecast period"

Asia Pacific is experiencing high growth in the crane rental market due to its high rate of urbanization, industrialization, and extensive infrastructure spending. Countries such as China, India, and Indonesia are immensely investing in construction and transportation works. The government's smart city and renewable energy programs are also increasing the demand for crane rental.

By Company Type: Tier 1 - 25%, Tier 2 - 42%, and Tier 3 - 33%

By Designation: C-level Executives - 20%, Directors - 30%, and Others - 50%

By Region: North America - 20%, Europe - 10%, Asia Pacific - 40%, South America - 10%, and the Middle East & Africa - 20%

Companies Covered: Liebherr (Germany), United Rentals Inc. (US), PALFINGER AG (Austria), Sarens NV (Belgium), Mammoet (Netherlands), and The Manitowoc Company, Inc. (US), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the crane rental market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the crane rental market based on type (mobile cranes and fixed cranes), weightlifting capacity (low, low to medium, heavy, and extremely heavy), end-use industry (building & construction, infrastructure, oil & gas, energy & power, marine & offshore, mining & excavation, transportation, and other end-use industries), and region (Asia Pacific, North America, Europe, South America, and the Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the crane rental market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, product launches, expansions, and acquisitions, associated with the crane rental market. This report covers a competitive analysis of upcoming startups in the crane rental market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall crane rental market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (surge in construction and infrastructure projects), restraints (elevated maintenance and operational expenses for rental providers), opportunities (rapid infrastructure growth across emerging markets), and challenges (heightened market competition and pricing pressures)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the crane rental market

- Market Development: Comprehensive information about profitable markets-the report analyzes the crane rental market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the crane rental market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product/service offerings of leading players, such as Liebherr (Germany), United Rentals Inc. (US), PALFINGER AG (Austria), Sarens NV (Belgium), Mammoet (Netherlands), and The Manitowoc Company, Inc. (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.3.6 STAKEHOLDERS

- 1.4 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RISK ASSESSMENT

- 2.6 GROWTH RATE ASSUMPTIONS

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 3.3 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 3.4 SNAPSHOT: ASIA PACIFIC MARKET SIZE AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CRANE RENTAL MARKET

- 4.2 CRANE RENTAL MARKET, BY TYPE AND REGION

- 4.3 CRANE RENTAL MARKET, BY WEIGHTLIFTING CAPACITY

- 4.4 CRANE RENTAL MARKET, BY END-USE INDUSTRY

- 4.5 CRANE RENTAL MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising offshore oil and gas development activities

- 5.2.1.2 Growing emphasis on smart city developments

- 5.2.1.3 Surge in construction and infrastructure projects

- 5.2.2 RESTRAINTS

- 5.2.2.1 Intense price wars and reduced profit margins creating barriers for new entrants

- 5.2.2.2 Fluctuating demand due to economic cycles

- 5.2.2.3 High maintenance and operational costs for rental companies

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expansion in emerging economies

- 5.2.3.2 Technological advancements and digitalization

- 5.2.3.3 Expanding wind energy sector

- 5.2.4 CHALLENGES

- 5.2.4.1 Volatility in raw material and fuel prices

- 5.2.4.2 Shortage of skilled workforce

- 5.2.1 DRIVERS

- 5.3 UNMET NEEDS AND WHITE SPACES

- 5.3.1 UNMET NEEDS IN CRANE RENTAL MARKET

- 5.3.1.1 Greater availability of specialized and high-capacity cranes

- 5.3.1.2 Digitalization and fleet management systems

- 5.3.1.3 Improved service, maintenance, and technical support

- 5.3.1.4 Flexible and transparent pricing models

- 5.3.1.5 Skilled operators and safety assurance

- 5.3.2 WHITE SPACE OPPORTUNITIES

- 5.3.2.1 Expansion into emerging and underserved markets

- 5.3.2.2 Green and sustainable crane fleets

- 5.3.2.3 Digital platforms and smart fleet management

- 5.3.2.4 Enhanced value-added services

- 5.3.2.5 Integrated lifting and project solutions

- 5.3.1 UNMET NEEDS IN CRANE RENTAL MARKET

- 5.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 5.4.1 INTERCONNECTED MARKETS

- 5.4.2 CROSS-SECTOR OPPORTUNITIES

- 5.4.3 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 5.4.4 KEY MOVES AND STRATEGIC FOCUS

6 INDUSTRY TRENDS

- 6.1 PORTER'S FIVE FORCES' ANALYSIS

- 6.1.1 THREAT OF NEW ENTRANTS

- 6.1.2 THREAT OF SUBSTITUTES

- 6.1.3 BARGAINING POWER OF SUPPLIERS

- 6.1.4 BARGAINING POWER OF BUYERS

- 6.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.2 MACROECONOMIC ANALYSIS

- 6.2.1 INTRODUCTION

- 6.2.2 GDP TRENDS AND FORECASTS

- 6.2.3 URBANIZATION AND DEMOGRAPHIC SHIFTS

- 6.2.4 TRADE AND GLOBAL SUPPLY CHAIN DYNAMICS

- 6.3 VALUE CHAIN ANALYSIS

- 6.4 ECOSYSTEM ANALYSIS

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY

- 6.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 6.6 TRADE ANALYSIS

- 6.6.1 IMPORT SCENARIO

- 6.6.2 EXPORT SCENARIO

- 6.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.9 INVESTMENT AND FUNDING SCENARIO

- 6.10 CASE STUDY ANALYSIS

- 6.10.1 INSTALLATION OF 7MW WIND MACHINE HOUSING IN SINGLE LIFT

- 6.10.2 PAPERPAK'S REFINED BAG FOR HARPER, INC. TO MEET SUSTAINABILITY DEMAND

- 6.10.3 GAS-FIRED POWER PLANT MAINTENANCE PROJECT: MAMMOET'S SUCCESS IN MINIMIZING DOWNTIME

- 6.11 IMPACT OF 2025 US TARIFF ON CRANE RENTAL MARKET

- 6.11.1 INTRODUCTION

- 6.11.2 KEY TARIFF RATES

- 6.11.3 PRICE IMPACT ANALYSIS

- 6.11.4 KEY IMPACT ON VARIOUS REGIONS

- 6.11.5 IMPACT ON END-USE INDUSTRIES

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 7.1 KEY TECHNOLOGIES

- 7.1.1 TELEMATICS SYSTEMS (FLEET OPTIMIZATION)

- 7.1.2 IOT SENSORS (PREDICTIVE MAINTENANCE)

- 7.1.3 DIGITAL PLATFORMS AND SOFTWARE SOLUTIONS (CUSTOMER SERVICE EXCELLENCE)

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 ELECTRIC AND HYBRID CRANES

- 7.2.2 SIMULATOR-BASED TRAINING SYSTEMS

- 7.2.3 DIGITAL SAFETY TOOLS

- 7.2.4 SUSTAINABLE AND ECO-FRIENDLY LIFTING EQUIPMENT (GREEN CRANES)

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 REMOTE MONITORING SYSTEM

- 7.3.2 AUTOMATED LIFTING SYSTEMS

- 7.4 TECHNOLOGY/PRODUCT ROADMAP

- 7.4.1 SHORT-TERM (2025-2027) | DIGITAL TRANSITION AND FLEET OPTIMIZATION PHASE

- 7.4.2 MID-TERM (2027-2030): SUSTAINABLE FLEETS AND SMART CONSTRUCTION INTEGRATION

- 7.4.3 LONG-TERM (2030-2035+): FULLY AUTOMATED, INTELLIGENT, AND SUSTAINABLE LIFTING ECOSYSTEMS

- 7.5 PATENT ANALYSIS

- 7.5.1 INTRODUCTION

- 7.5.2 APPROACH

- 7.5.3 TOP APPLICANTS

- 7.6 FUTURE APPLICATIONS

- 7.6.1 FULLY AUTOMATED AND INTELLIGENT CRANE RENTAL SYSTEMS

- 7.7 IMPACT OF AI/GEN AI ON CRANE RENTAL MARKET

- 7.7.1 TOP USE CASES AND MARKET POTENTIAL

- 7.7.2 BEST PRACTICES IN CRANE RENTAL

- 7.7.3 CASE STUDIES OF AI IMPLEMENTATION IN CRANE RENTAL MARKET

- 7.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN CRANE RENTAL MARKET

- 7.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 7.8.1 DEEP SOUTH DELIVERS SEAMLESS EXECUTION IN SOUTHEAST PETROCHEMICAL TURNAROUND

- 7.8.2 LAMPSON INTERNATIONAL DEMONSTRATES EXCEPTIONAL PERFORMANCE IN SEATTLE HOTEL CONSTRUCTION PROJECT

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF CRANE RENTAL

- 8.2.1.1 Carbon Impact Reduction

- 8.2.1.2 Eco-Applications

- 8.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF CRANE RENTAL

- 8.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 8.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

9 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 9.1 DECISION-MAKING PROCESS

- 9.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 9.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 9.2.2 BUYING CRITERIA

- 9.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 9.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 9.5 MARKET PROFITIBILITY

- 9.5.1 REVENUE POTENTIAL

- 9.5.2 COST DYNAMICS

- 9.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

10 CRANE RENTAL MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 FIXED CRANES

- 10.2.1 HIGH STABILITY, HEIGHT, AND LIFTING POWER TO DRIVE DEMAND

- 10.3 MOBILE CRANES

- 10.3.1 UNMATCHED MOBILITY, VERSATILITY, AND ADAPTABILITY ACROSS JOB SITES TO DRIVE DEMAND

11 CRANE RENTAL MARKET, BY WEIGHTLIFTING CAPACITY

- 11.1 INTRODUCTION

- 11.2 LOW

- 11.2.1 SUITABILITY FOR WIDE ARRAY OF TASKS IN VARIOUS INDUSTRIES TO FUEL MARKET GROWTH

- 11.3 LOW TO MEDIUM

- 11.3.1 AFFORDABILITY AND VERSATILITY FOR WIDE RANGE OF APPLICATIONS TO DRIVE MARKET

- 11.4 HEAVY

- 11.4.1 ADOPTION IN INTRICATE AND SPECIALIZED APPLICATIONS TO DRIVE DEMAND

- 11.5 EXTREME HEAVY

- 11.5.1 DEMAND FOR PRECISE, EFFICIENT, AND SAFE HANDLING IN CONSTRUCTION AND ENERGY SECTORS TO DRIVE MARKET

12 CRANE RENTAL MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 BUILDING & CONSTRUCTION

- 12.2.1 RESIDENTIAL CONSTRUCTION

- 12.2.1.1 Growing preference for rental over ownership of cranes to drive market

- 12.2.2 COMMERCIAL CONSTRUCTION

- 12.2.2.1 Need to reduce downtime and improve project efficiency to drive market

- 12.2.1 RESIDENTIAL CONSTRUCTION

- 12.3 INFRASTRUCTURE

- 12.3.1 IMPLEMENTATION OF VARIOUS INFRASTRUCTURE PROJECTS IN MAJOR ECONOMIES TO FUEL MARKET GROWTH

- 12.4 OIL & GAS

- 12.4.1 EXPANSION OF OIL & GAS SECTOR TO FUEL SEGMENTAL GROWTH

- 12.5 ENERGY & POWER

- 12.5.1 ONGOING RENEWABLE ENERGY SECTOR EXPANSION TO DRIVE MARKET GROWTH

- 12.6 MARINE & OFFSHORE

- 12.6.1 GROWING EMPHASIS ON OFFSHORE WIND FARMS AND RENEWABLE ENERGY PROJECTS TO DRIVE DEMAND

- 12.7 MINING & EXCAVATION

- 12.7.1 REQUIREMENT FOR SPECIALIZED LIFTING SOLUTIONS IN REMOTE AND CHALLENGING TERRAINS TO FUEL DEMAND

- 12.8 TRANSPORTATION

- 12.8.1 INFRASTRUCTURE DEVELOPMENT ACTIVITIES IN MAJOR ECONOMIES TO SUPPORT MARKET GROWTH

- 12.9 OTHER END-USE INDUSTRIES

13 CRANE RENTAL MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Rapid infrastructure expansion and industrial modernization to drive market

- 13.2.2 INDIA

- 13.2.2.1 Government infrastructure programs and urban development to drive market

- 13.2.3 JAPAN

- 13.2.3.1 Urban development and reconstruction to drive market

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Growth of construction and energy sectors to drive market

- 13.2.5 AUSTRALIA

- 13.2.5.1 Expansion of modern retail and convenience stores to drive market

- 13.2.6 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 NORTH AMERICA

- 13.3.1 US

- 13.3.1.1 Increasing implementation of infrastructure, energy, and urban development projects to propel market

- 13.3.2 CANADA

- 13.3.2.1 Growing infrastructure, energy, and offshore development activities to drive market

- 13.3.3 MEXICO

- 13.3.3.1 Expanding construction and energy infrastructure activities driving market growth

- 13.3.1 US

- 13.4 EUROPE

- 13.4.1 GERMANY

- 13.4.1.1 Increase in construction and infrastructure investments to drive market

- 13.4.2 FRANCE

- 13.4.2.1 Implementation of construction and infrastructure modernization initiatives to fuel demand

- 13.4.3 UK

- 13.4.3.1 Expanding infrastructure and urban development projects to support market growth

- 13.4.4 ITALY

- 13.4.4.1 Infrastructure and offshore energy projects to augment market growth

- 13.4.5 SPAIN

- 13.4.5.1 Urban renewal and tourism-led construction growth to drive demand

- 13.4.6 SWEDEN

- 13.4.6.1 Strong infrastructure investments and sustainable construction initiatives to drive market

- 13.4.7 AUSTRIA

- 13.4.7.1 Expansion of urban infrastructure and regulatory framework supporting crane rental growth

- 13.4.8 SWITZERLAND

- 13.4.8.1 Steady industrial growth and technological advancements to drive market

- 13.4.9 REST OF EUROPE

- 13.4.1 GERMANY

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Development of mega infrastructure and offshore energy projects to drive market

- 13.5.1.2 UAE

- 13.5.1.2.1 Economic diversification and expansion of large-scale energy and infrastructure projects to drive market

- 13.5.1.3 Rest of GCC countries

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Large-scale infrastructure development and expanding industrial projects strengthening crane rental demand

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Increase in construction and offshore energy development activities fueling demand

- 13.6.2 ARGENTINA

- 13.6.2.1 Significant infrastructure development to support market growth

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES'/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 Weightlifting capacity footprint

- 14.7.5.5 End-use industry footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 UNITED RENTALS, INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 LIEBHERR

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 PALFINGER AG

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 SARENS NV

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 MAMMOET

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 THE MANITOWOC COMPANY INC.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.4 MnM view

- 15.1.6.4.1 Key strengths

- 15.1.6.4.2 Strategic choices

- 15.1.6.4.3 Weaknesses and competitive threats

- 15.1.7 MAXIM CRANE WORKS

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.4 MnM view

- 15.1.7.4.1 Key strengths

- 15.1.7.4.2 Strategic choices

- 15.1.7.4.3 Weaknesses and competitive threats

- 15.1.8 ACTION CONSTRUCTION EQUIPMENT LTD.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 MnM view

- 15.1.8.3.1 Key strengths

- 15.1.8.3.2 Strategic choices

- 15.1.8.3.3 Weaknesses and competitive threats

- 15.1.9 LEAVITT CRANES

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 MnM view

- 15.1.9.3.1 Right to win

- 15.1.9.3.2 Strategic choices

- 15.1.9.3.3 Weaknesses and competitive threats

- 15.1.10 WASEL GMBH

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.4 MnM view

- 15.1.10.4.1 Right to win

- 15.1.10.4.2 Strategic choices

- 15.1.10.4.3 Weaknesses and competitive threats

- 15.1.1 UNITED RENTALS, INC.

- 15.2 OTHER PLAYERS

- 15.2.1 WELDEX (INTERNATIONAL) OFFSHORE LTD.

- 15.2.2 MEDIACO GROUP

- 15.2.3 BUCKNER HEAVYLIFT CRANES, LLC

- 15.2.4 VMS EQUIPMENT

- 15.2.5 DAIKYO KENKI CO., LTD.

- 15.2.6 EUROGRUAS

- 15.2.7 SHINSEI MACHINERY CO., LTD.

- 15.2.8 AMERICAN CRANE RENTAL, INC.

- 15.2.9 SANGHVI MOVERS LIMITED

- 15.2.10 DEEP SOUTH CRANE & RIGGING LLC

- 15.2.11 STARLOG ENTERPRISES LIMITED

- 15.2.12 MYCRANE

- 15.2.13 LAMPSON INTERNATIONAL LLC

- 15.2.14 IMPERIAL CRANES

- 15.2.15 BKL BAUKRAN LOGISTIK GMBH

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS