|

시장보고서

상품코드

1782036

원격의료 및 원격 진료용 AI 시장 예측(-2030년) : 컴포넌트(소프트웨어, 서비스), 기능(가상 케어, 챗봇, RPM, 관리자, 환자 참여), 용도(원격 신경 진료, 원격 ICU, 원격 방사선 진단), 최종사용자별(의료 제공자, 보험자)AI in Telehealth & Telemedicine Market by Component (Software, Service), Function (Virtual Care, Chatbot, RPM, Admin, Patient Engagement), Application (Teleneurology, TeleICU, Teleradiology), End User (Provider, Payer, Patient) - Global Forecast to 2030 |

||||||

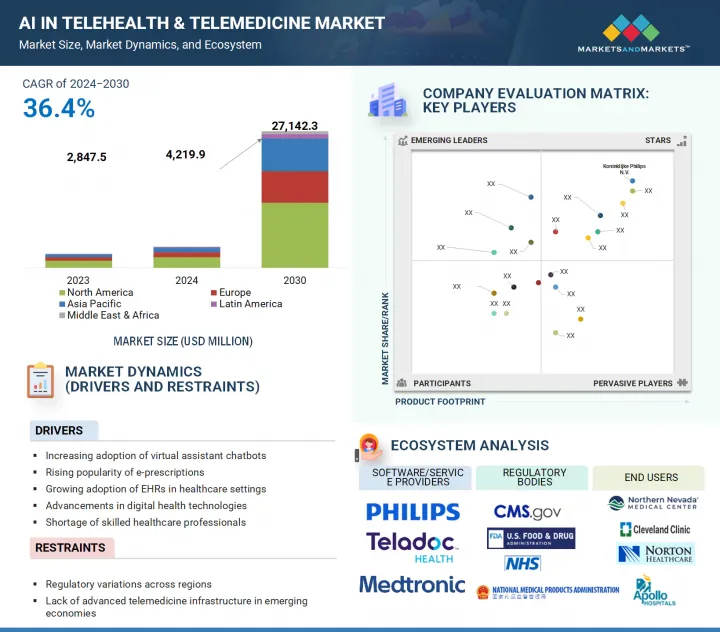

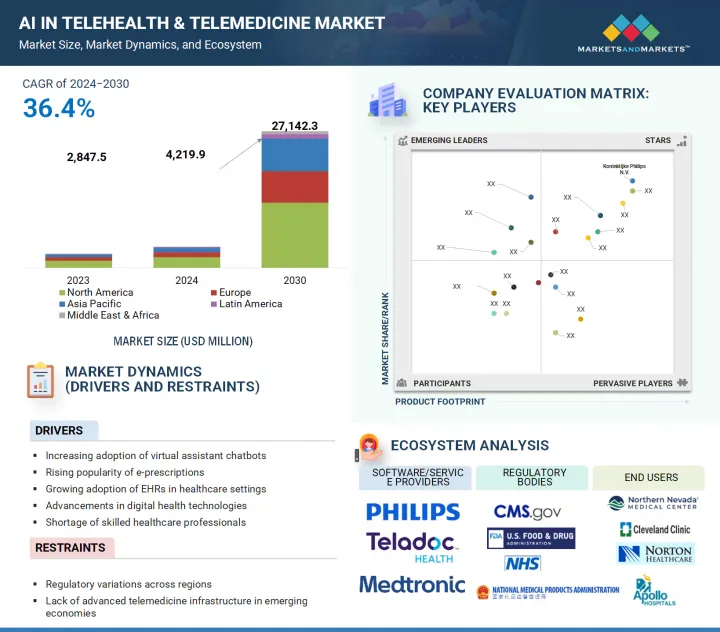

세계의 원격의료 및 원격 진료용 AI 시장 규모는 2024-2030년에 CAGR 36.4%로 성장할 것으로 예측됩니다.

원격의료 및 원격진료 분야의 AI 시장은 통신 기술 발전, 유리한 정부 지원 및 규제 정책, RPM 시스템 확대 등 다양한 요인으로 인해 빠르게 성장하고 있습니다. 노인 인구 증가로 인해 만성질환에 대한 지속적인 모니터링이 필요하고, 비용 효율적인 헬스케어 솔루션에 대한 수요가 증가하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2024-2030년 |

| 기준연도 | 2023년 |

| 예측 기간 | 2024-2030년 |

| 단위 | 금액(달러) |

| 부문 | 컴포넌트·기능·용도·최종사용자·지역 |

| 대상 지역 | 북미·유럽·아시아태평양·라틴아메리카·중동 & 아프리카 |

당뇨병, 심장질환 등 만성질환 진단에 대한 관심이 높아지면서 원격의료기기에 대한 수요가 증가하고 있습니다. 가상 비서, 예측 분석, 자동 기록과 같은 AI 기술은 원격의료 서비스의 효과와 제공 가능성을 향상시키고 있습니다. 예를 들어 2025년 3월 미국의 Eli Lilly and Company는 알츠하이머병 진단 및 치료를 위해 LillyDirect라는 원격 진료 서비스를 시작했습니다. 원격의료기기는 전문의 부족, 환자 대기시간 등의 문제를 해결하고 의료의 질과 환자의 고급 의료에 대한 접근성을 향상시키고 있습니다.

컴포넌트별로는 소프트웨어 부문이 예측 기간 중 가장 빠른 성장률을 보일 것으로 예측됩니다.

기업은 인프라 개발에 필요한 자본을 절감할 수 있다는 이유로 원격의료 소프트웨어 도입을 추진해 왔습니다. AI와 머신러닝(ML)을 탑재한 고급 소프트웨어 플랫폼은 예측 분석, 개인화, 맞춤형 케어 전략 등의 기능을 갖추고 있으며, 기업이 원격의료 솔루션을 보급하는 데 기여하고 있습니다.

최종사용자별로는 의료 프로바이더 부문이 2023년 가장 큰 점유율을 차지할 것으로 보입니다.

원격 환자 모니터링(RPM), 인공지능(AI), 클라우드 시스템을 통해 의료 서비스의 개인화 및 적시 제공이 가능해져 원격 진료 도입과 만성질환 관리 증가에 대한 대응을 촉진하고 있습니다. 많은 의료기관들이 대기시간 단축과 관리 업무의 부담을 줄이기 위해 원격의료 플랫폼을 도입하고 있습니다.

지역별로는 아시아태평양이 예측 기간 중 가장 빠른 CAGR을 나타낼 것으로 예측됩니다.

아시아태평양은 빠르게 발전하는 의료 인프라와 기술 혁신의 혜택을 받아 예측 기간 중 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 또한 고령 인구 증가에 따른 의료 수요 증가, 만성질환 발병률 증가, 디지털 헬스 제품 이용 확대 등이 지역 시장 성장을 촉진하고 있습니다. 정부의 정책도 시장 확대에 기여하고 있습니다.

원격의료 및 원격 진료용 AI 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인의 분석, 기술·특허의 동향, 법규제 환경, 사례 연구, 시장 규모 추이·예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

- 고객 사업에 영향을 미치는 동향/혼란

- 업계 동향

- 에코시스템 분석

- 밸류체인 분석

- 기술 분석

- 관세 및 규제 분석

- 무역 분석

- 가격 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 특허 분석

- 미충족 요구와 최종사용자 기대

- 2025-2026년의 주요 컨퍼런스와 이벤트

- 사례 연구 분석

- 투자와 자금조달 시나리오

- 비즈니스 모델 분석

- 상환 시나리오 분석

제6장 원격의료 및 원격 진료용 AI 시장 : 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스

제7장 원격의료 및 원격 진료용 AI 시장 : 기능별

- 가상 케어 상담

- 챗봇과 가상 비서

- 원격 환자 모니터링

- 가상 간호 케어 플랫폼

- 임상 문서

- 관리 워크플로우

- 분석·리포팅

- 환자 참여

- 기타

제8장 원격의료 및 원격 진료용 AI 시장 : 용도별

- 1차 의료

- 전문 케어

- 원격 방사선 진단

- 원격 심장 진료

- 원격 신경 진료

- 당뇨병

- 호흡기질환

- 고혈압

- 원격 피부과 진료

- 원격 정신과진료

- 기타 전문 분야

- 원격 ICU

- 기타

제9장 원격의료 및 원격 진료용 AI 시장 : 최종사용자별

- 의료 제공자

- 병원

- 외래 수술 센터, 외래 진료 센터, 기타 외래 시설

- 장기요양시설·어시스티드 리빙 시설

- 재택 의료

- 기타

- 의료보험자

- 환자

- 제약·바이오테크놀러지 기업

- 의료 기술 기업

- 기타

제10장 원격의료 및 원격 진료용 AI 시장 : 지역별

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 거시경제 전망

- 중국

- 일본

- 인도

- 기타

- 라틴아메리카

- 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 거시경제 전망

- GCC 국가

- 기타

제11장 경쟁 구도

- 주요 참여 기업의 전략/강점

- 매출 분석

- 2023년 시장 점유율 분석

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업/중소기업

- 기업 평가와 재무 지표

- 브랜드/소프트웨어 비교

- 경쟁 시나리오

제12장 기업 개요

- 주요 기업

- MEDTRONIC

- TELADOC HEALTH, INC.

- KONINKLIJKE PHILIPS N.V.

- CISCO SYSTEMS, INC.

- GE HEALTHCARE

- EPIC SYSTEMS CORPORATION

- ORACLE

- DOXIMITY, INC.

- INCLUDED HEALTH, INC.

- ZOOM COMMUNICATIONS, INC.

- AMERICAN WELL

- SIEMENS HEALTHINEERS AG

- AMC HEALTH

- TELESPECIALISTS

- WALGREENS BOOTS ALLIANCE, INC.(WALGREEN CO.)

- CAREGILITY

- CVS HEALTH

- ALIVECOR, INC.

- ELATION

- HEALTHTAP, INC.

- 기타 기업

- CURAI HEALTH

- ANDOR HEALTH

- K HEALTH

- TRANSCARENT

- BIOINTELLISENSE, INC.

제13장 부록

KSA 25.08.11The global AI in telehealth & telemedicine market is projected to grow at a CAGR of 36.4% between 2024 and 2030. The AI in telehealth & telemedicine market is rapidly expanding due to various factors such as advancements in telecommunication technologies, favorable government support and regulatory policies, and the expansion of RPM systems. An increase in the geriatric population necessitates the continuous monitoring of chronic conditions, creating a growing demand for cost-effective healthcare solutions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2023 |

| Forecast Period | 2024-2030 |

| Units Considered | Value (USD billion) |

| Segments | Component, Function, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

An increasing focus on the diagnosis of chronic illnesses such as diabetes and heart disease has led to an increased need for telehealth devices. AI technologies such as virtual assistants, predictive analytics, and automated note-taking help improve the effectiveness and availability of telehealth services. For instance, in March 2025, Eli Lilly and Company (US) introduced LillyDirect remote consultations to diagnose and treat Alzheimer's. Telehealth devices solve problems such as a lack of specialists and patient wait times, improving healthcare and patient access to advanced medical solutions.

The software segment is expected to have the fastest growth rate in the AI in telehealth market during the forecast period, by component.

By component, the software segment is expected to be the fastest growing market during the forecast period. Companies have promoted telehealth software due to the need for less capital for infrastructural development. Advanced software platforms enhanced with AI and ML have predictive analytics, personalization, and tailored care strategies, which also help companies promote telehealth solutions. Companies such as Cisco Systems, Inc. (US) offer Cisco HealthPresence 2.5 software solutions. Additionally, in February 2025, Teladoc Health Inc. (US) acquired Catapult Health (US), a provider of virtual preventive care solutions, for USD 65 million; this acquisition supports Teladoc Health Inc. in strengthening its market position.

The healthcare providers segment accounted for the largest market share in 2023.

On the basis of end users, the healthcare providers segment accounted for the largest market share in 2023. RPM, AI, and cloud systems allow for the personalization and timely delivery of healthcare services, which helps manage the increasing adoption of remote consultations and chronic disease management. Many healthcare facilities have adopted the telehealth platform to reduce waiting periods and can handle large patient pools with less administrative workflow. For instance, Mercy Health (US) offers Mercy Virtual Care Services, serving over 600,000 patients across seven US states with more than 300 clinicians, delivering care through advanced technologies such as two-way video, online-enabled instruments, and real-time vital sign monitoring. The program enhances patient access and outcomes while reducing healthcare costs by enabling earlier interventions and continuous remote monitoring for those with chronic or complex conditions.

The Asia Pacific is estimated to register the fastest CAGR during the forecast period.

The AI in telemedicine market is geographically segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific market is projected to register the fastest CAGR during the forecast period as it benefits from the fast-developing healthcare infrastructure and technological advancements. In addition, the rising use of digital healthcare products, growing healthcare needs resulting from large geriatric populations, and an increasing incidence of chronic diseases drive regional growth. Government initiatives also promote market growth. In February 2024, South Korea's health ministry announced it would fully allow telemedicine services at all hospitals and clinics. In addition, India offers universal health coverage through the national telemedicine service (eSanjeevani), which covers 130 specialties. The platform has created 17,084 telemedicine hubs and serviced 364,497,645 patients to date. Government initiatives promoting telemedicine and improvements in digital health infrastructure also contributed to market growth.

Breakdown of supply-side primary interviews by company type, designation, and region:

- By Company Type: Tier 1 (40%), Tier 2 (35%), and Tier 3 (25%)

- By Designation: Managers (40%), Directors (35%), and Other Designations (25%)

- By Region: North America (45%), Europe (30%), Asia Pacific (20%), Latin America (3%), and Middle East & Africa (2%)

List of Companies Profiled in the Report:

- 1. Koninklijke Philips N.V. (Netherlands)

- 2. Medtronic (Ireland)

- 3. GE Healthcare (US)

- 4. Epic Systems Corporation (US)

- 5. Oracle (US)

- 6. Doximity, Inc. (US)

- 7. Teladoc Health, Inc. (US)

- 8. American Well (US)

- 9. Siemens Healthineers AG (Germany)

- 10. Cisco Systems Inc. (US)

- 11. Included Health, Inc. (US)

- 12. AMC Health (US)

- 13. TeleSpecialists (US)

- 14. Walgreen Co. (US)

- 15. Caregility (US)

- 16. CVS Health (US)

- 17. AliveCor, Inc. (US)

- 18. Elation (US)

- 19. HealthTap, Inc. (US)

- 20. ZoomCommunications, Inc. (US)

Research Coverage:

This research report categorizes the AI in telehealth & telemedicine market by component [hardware, software {(by modality: EHR-centric, Non-EHR-centric), (by integration type: integrated software, standalone software), (by deployment: on-premise deployment, cloud-based deployment)}, and services], by function [virtual care consultations, chatbots & virtual assistants, remote patient monitoring, virtual nursing care platform, clinical documentation, administrative workflows, analytics & reporting, patient engagement, and other functions[, by application [primary care, speciality care {teleradiology, telecardiology, teleneurology, diabetes, respiratory disorders, hypertension, teledermatology, telepsychiatry, other specialty care applications}, teleICU, and other applications], by end user [healthcare providers {hospitals; ambulatory surgery centers, ambulatory care centers, and other outpatient settings; long-term care & assisted living facilities; home healthcare; and other healthcare providers}, healthcare payers, patients, pharmaceutical & biotechnology companies, medtech companies, and other end users], and region. The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the AI in telehealth & telemedicine market. A thorough analysis of the key industry players has provided insights into their business overview, offerings, and key strategies, such as acquisitions, collaborations, partnerships, mergers, product/service launches & enhancements, and approvals in the AI in telehealth & telemedicine market. This report covers the competitive analysis of upcoming startups in the AI in telehealth & telemedicine market ecosystem.

Reasons to Buy the Report

The report will help market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall AI in telehealth and telemedicine market and its subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers: (increasing adoption of virtual assistant chatbots, rising popularity of e-prescriptions, growing adoption of EHRs in healthcare settings, advancements in digital health technologies, and shortage of skilled healthcare professionals), restraints (Regulatory variations across regions and lack of advanced telemedicine infrastructure in emerging economies), opportunities (growing popularity of virtual healthcare solutions, emergence of AI and ML, favorable government initiatives and reimbursement policies, rising focus on home healthcare, and expansion of remote patient monitoring markets), and challenges (Increasing data breaches and medical identity theft cases and complexities of big data in healthcare) influencing the growth of the AI in telehealth & telemedicine market.

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and new product & service launches in the AI in telehealth & telemedicine market.

- Market Development: Comprehensive information about lucrative markets-the report analyses the AI in telehealth & telemedicine market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the AI in telehealth & telemedicine market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Koninklijke Philips N.V. (Netherlands), Medtronic (Ireland), GE Healthcare (US), Epic Systems Corporation (US), Oracle (US), Doximity, Inc. (US), and Teladoc Health, Inc. (US), among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 TELEHEALTH

- 1.2.2 TELEMEDICINE

- 1.3 STUDY SCOPE

- 1.3.1 SEGMENTS CONSIDERED & GEOGRAPHICAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key sources for secondary data

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key sources for primary data

- 2.1.2.2 Key objectives of primary research

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Insights from primary experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 SUPPLY-SIDE ANALYSIS (REVENUE SHARE ANALYSIS)

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.6.1 METHODOLOGY-RELATED LIMITATIONS

- 2.6.2 SCOPE-RELATED LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 AI IN TELEHEALTH & TELEMEDICINE MARKET OVERVIEW

- 4.2 NORTH AMERICA: AI IN TELEHEALTH & TELEMEDICINE MARKET, BY COMPONENT AND COUNTRY

- 4.3 AI IN TELEHEALTH & TELEMEDICINE MARKET: GEOGRAPHIC SNAPSHOT

- 4.4 AI IN TELEHEALTH & TELEMEDICINE MARKET: DEVELOPED VS. EMERGING MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing adoption of virtual assistant chatbots

- 5.2.1.2 Rising popularity of e-prescriptions

- 5.2.1.3 Growing adoption of EHRs in healthcare settings

- 5.2.1.4 Advancements in digital health technologies

- 5.2.1.5 Shortage of skilled healthcare professionals

- 5.2.2 RESTRAINTS

- 5.2.2.1 Regulatory variations across regions

- 5.2.2.2 Lack of advanced telemedicine infrastructure in emerging economies

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing popularity of virtual healthcare solutions

- 5.2.3.2 Emergence of AI and ML

- 5.2.3.3 Favorable government initiatives and reimbursement policies

- 5.2.3.4 Rising focus on home healthcare

- 5.2.3.5 Expansion of remote patient monitoring markets

- 5.2.4 CHALLENGES

- 5.2.4.1 Increasing data breaches and medical identity theft cases

- 5.2.4.2 Complexities of big data in healthcare

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.4 INDUSTRY TRENDS

- 5.4.1 GEN AI FOR MEDICAL DOCUMENTATION

- 5.4.2 INNOVATIONS IN REMOTE PATIENT MONITORING DEVICES

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 ROLE IN ECOSYSTEM

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Video conferencing and real-time communication platforms

- 5.7.1.2 Virtual assistants and chatbots

- 5.7.1.3 Voice recognition and natural language processing

- 5.7.1.4 EHR integration

- 5.7.1.5 Remote patient monitoring systems

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Cloud computing

- 5.7.2.2 mHealth applications

- 5.7.2.3 Wearable devices, sensors, and IoT

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Digital therapeutics

- 5.7.3.2 Blockchain technologies

- 5.7.3.3 Augmented reality and virtual reality

- 5.7.1 KEY TECHNOLOGIES

- 5.8 TARIFF & REGULATORY ANALYSIS

- 5.8.1 TARIFF DATA ANALYSIS

- 5.8.1.1 Average tariff for HS code 9018

- 5.8.1.2 Average tariff for HS code 9021

- 5.8.1.3 Average tariff for HS code 9022

- 5.8.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.8.3 REGULATORY STANDARDS

- 5.8.4 REGULATORY REQUIREMENTS

- 5.8.1 TARIFF DATA ANALYSIS

- 5.9 TRADE ANALYSIS

- 5.9.1 TRADE ANALYSIS FOR HSN CODE 90189099, 2019-2023

- 5.9.1.1 Top 10 importers for HSN code 90189099

- 5.9.1.2 Top 10 exporters for HSN code 90189099

- 5.9.2 TRADE ANALYSIS FOR HSN CODE 9021, 2019-2023

- 5.9.2.1 Top 10 importers for HSN code 9021

- 5.9.2.2 Top 10 exporters for HSN code 9021

- 5.9.3 TRADE ANALYSIS FOR HSN CODE 9022, 2019-2023

- 5.9.3.1 Top 10 importers for HSN code 9022

- 5.9.3.2 Top 10 exporters for HSN code 9022

- 5.9.1 TRADE ANALYSIS FOR HSN CODE 90189099, 2019-2023

- 5.10 PRICING ANALYSIS

- 5.10.1 INDICATIVE PRICE FOR AI-BASED TELEHEALTH & TELEMEDICINE DEVICES, BY COMPONENT, 2023

- 5.10.2 AVERAGE PRICING TREND OF AI-BASED TELEHEALTH & TELEMEDICINE DEVICES, BY REGION, 2022-2024

- 5.10.3 PRICING MODELS

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.11.2 THREAT OF NEW ENTRANTS

- 5.11.3 THREAT OF SUBSTITUTES

- 5.11.4 BARGAINING POWER OF BUYERS

- 5.11.5 BARGAINING POWER OF SUPPLIERS

- 5.12 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 KEY BUYING CRITERIA

- 5.13 PATENT ANALYSIS

- 5.13.1 PATENT PUBLICATION TRENDS FOR AI-BASED TELEHEALTH & TELEMEDICINE DEVICES

- 5.13.2 INSIGHTS: JURISDICTION & TOP APPLICANT ANALYSIS

- 5.14 UNMET NEEDS & END-USER EXPECTATIONS

- 5.14.1 UNMET NEEDS

- 5.14.2 END-USER EXPECTATIONS

- 5.15 KEY CONFERENCES & EVENTS, 2025-2026

- 5.16 CASE STUDY ANALYSIS

- 5.16.1 TRANSFORMING PATIENT CARE AND OPERATIONAL EFFICIENCY WITH CAREGILITY VIRTUAL NURSING SOLUTION

- 5.16.2 TELADOC HEALTH TO PROVIDE MEDICARE ADVANTAGE PLAN FOR CLOSING GAPS AND BOOSTING QUALITY RATINGS

- 5.16.3 LMH HEALTH TO REDUCE NURSE WORKLOAD WITH VIRTUAL NURSING

- 5.17 INVESTMENT & FUNDING SCENARIO

- 5.18 BUSINESS MODEL ANALYSIS

- 5.18.1 DIRECT-TO-PATIENT (D2P) MODELS

- 5.18.2 BUSINESS-TO-BUSINESS (B2B) MODELS

- 5.18.3 EMPLOYER-SPONSORED MODELS

- 5.18.4 SUBSCRIPTION-BASED MODELS

- 5.18.5 HYBRID TELEMEDICINE MODELS

- 5.18.6 PLATFORM-AS-A-SERVICE (PAAS) MODELS

- 5.18.7 VALUE-BASED CARE MODELS

- 5.19 REIMBURSEMENT SCENARIO ANALYSIS

6 AI IN TELEHEALTH & TELEMEDICINE MARKET, BY COMPONENT

- 6.1 INTRODUCTION

- 6.2 HARDWARE

- 6.2.1 HIGH DEMAND FOR REMOTE PATIENT MONITORING DEVICES TO SPUR MARKET GROWTH

- 6.3 SOFTWARE

- 6.3.1 AI IN TELEHEALTH & TELEMEDICINE SOFTWARE MARKET, BY MODALITY

- 6.3.1.1 EHR-centric software

- 6.3.1.1.1 EHR-centric software to facilitate better care coordination and streamline administrative tasks

- 6.3.1.2 Non-EHR-centric software

- 6.3.1.2.1 Non-EHR-centric software to conduct virtual consultations and facilitate remote telehealth services

- 6.3.1.1 EHR-centric software

- 6.3.2 AI IN TELEHEALTH & TELEMEDICINE SOFTWARE MARKET, BY INTEGRATION TYPE

- 6.3.2.1 Integrated software

- 6.3.2.1.1 Better accessibility and efficiency in integrated software to revolutionize patient care

- 6.3.2.2 Standalone software

- 6.3.2.2.1 Flexibility and ease of usage to fuel uptake for high-quality remote patient care

- 6.3.2.1 Integrated software

- 6.3.3 AI IN TELEHEALTH & TELEMEDICINE SOFTWARE MARKET, BY DEPLOYMENT

- 6.3.3.1 On-premises deployment

- 6.3.3.1.1 On-premises deployment to enhance safety and control of inventory data

- 6.3.3.2 Cloud-based deployment

- 6.3.3.2.1 Cost-effectiveness and easy optimization of complex IT systems to boost market growth

- 6.3.3.1 On-premises deployment

- 6.3.1 AI IN TELEHEALTH & TELEMEDICINE SOFTWARE MARKET, BY MODALITY

- 6.4 SERVICES

- 6.4.1 TELEHEALTH SERVICES TO REDUCE IN-PERSON CLINIC VISITS AND ENSURE BETTER TREATMENT ACCESSIBILITY FOR REMOTE AREAS

7 AI IN TELEHEALTH & TELEMEDICINE MARKET, BY FUNCTION

- 7.1 INTRODUCTION

- 7.2 VIRTUAL CARE CONSULTATION

- 7.2.1 AI-BASED VIRTUAL CARE PLANS TO AUTOMATE DOCUMENTATION AND OFFER BETTER CLINICAL DECISION SUPPORT

- 7.3 CHATBOTS & VIRTUAL ASSISTANTS

- 7.3.1 CHATBOTS & VIRTUAL ASSISTANTS TO ENHANCE PATIENT ENGAGEMENT AND PROVIDE REAL-TIME HEALTH SUPPORT

- 7.4 REMOTE PATIENT MONITORING

- 7.4.1 EFFECTIVE REAL-TIME DISEASE MONITORING WITHOUT IN-PATIENT VISITS TO DRIVE MARKET

- 7.5 VIRTUAL NURSING CARE PLATFORMS

- 7.5.1 VIRTUAL NURSING PLATFORMS TO ELIMINATE NURSING SHORTAGES, REDUCE BURNOUT, AND PROVIDE HIGH-QUALITY CARE

- 7.6 CLINICAL DOCUMENTATION

- 7.6.1 NEED FOR ACCURATE AND COMPLIANT MEDICAL RECORDS FOR VIRTUAL CONSULTATIONS TO AUGMENT MARKET GROWTH

- 7.7 ADMINISTRATIVE WORKFLOW

- 7.7.1 EFFECTIVE RESOURCE MANAGEMENT AND OPERATIONAL EFFICIENCY TO AID MARKET GROWTH

- 7.8 ANALYTICS & REPORTING

- 7.8.1 ADVANCED ANALYTICS & REPORTING TOOLS TO FOSTER BETTER CARE COORDINATION AND PROVIDE PERSONALIZED TREATMENTS

- 7.9 PATIENT ENGAGEMENT

- 7.9.1 BETTER PATIENT ENGAGEMENT TO ADVANCE HEALTHCARE DELIVERY AND PROMOTE BETTER ADHERENCE TO TREATMENT PLANS

- 7.10 OTHER FUNCTIONS

8 AI IN TELEHEALTH & TELEMEDICINE MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 PRIMARY CARE APPLICATIONS

- 8.2.1 TECHNOLOGICAL ADVANCEMENTS AND DEMAND FOR PERSONALIZED HEALTHCARE DELIVERY TO PROPEL MARKET GROWTH

- 8.3 SPECIALTY CARE APPLICATIONS

- 8.3.1 TELERADIOLOGY

- 8.3.1.1 Reduced turnaround time for imaging reports and better access to radiologists in remote areas to support market growth

- 8.3.2 TELECARDIOLOGY

- 8.3.2.1 Real-time ECG interpretations and remote cardiac care for chronic patients to augment market growth

- 8.3.3 TELENEUROLOGY

- 8.3.3.1 Growing focus on advanced neurological care without in-person visits to aid market growth

- 8.3.4 DIABETES

- 8.3.4.1 Rising prevalence of diabetes to drive market

- 8.3.5 RESPIRATORY DISORDERS

- 8.3.5.1 Increasing incidence of respiratory diseases among geriatric population to propel market growth

- 8.3.6 HYPERTENSION

- 8.3.6.1 Need for constant monitoring and high prevalence of hypertension to boost market growth

- 8.3.7 TELEDERMATOLOGY

- 8.3.7.1 Increased occurrence of skin cancer to fuel market growth

- 8.3.8 TELEPSYCHIATRY

- 8.3.8.1 Shortage of mental health practitioners in rural areas to fuel uptake

- 8.3.9 OTHER SPECIALTY CARE APPLICATIONS

- 8.3.1 TELERADIOLOGY

- 8.4 TELEICU

- 8.4.1 INCREASE IN EMERGENCY DEPARTMENT VISITS AND UNEVEN DISTRIBUTION OF ER SPECIALISTS TO PROPEL MARKET GROWTH

- 8.5 OTHER APPLICATIONS

9 AI IN TELEHEALTH & TELEMEDICINE MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 HEALTHCARE PROVIDERS

- 9.2.1 HOSPITALS

- 9.2.1.1 Growing incidence of chronic diseases and increasing demand for high-quality care to aid market growth

- 9.2.2 AMBULATORY SURGERY CENTERS, AMBULATORY CARE CENTERS, AND OTHER OUTPATIENT SETTINGS

- 9.2.2.1 Cost-effectiveness and reduced patient downtime to augment market growth

- 9.2.3 LONG-TERM CARE & ASSISTED LIVING FACILITIES

- 9.2.3.1 Need for prolonged treatment for chronic diseases to support market growth

- 9.2.4 HOME HEALTHCARE

- 9.2.4.1 Demand for cost-effective solutions and low hospital readmissions to propel segment growth

- 9.2.5 OTHER HEALTHCARE PROVIDERS

- 9.2.1 HOSPITALS

- 9.3 HEALTHCARE PAYERS

- 9.3.1 HEALTHCARE PAYERS TO REDUCE OVERHEAD COSTS, MINIMIZE PAPER TRAILS, AND IMPROVE MEMBER SERVICES

- 9.4 PATIENTS

- 9.4.1 EMERGENCE OF ADVANCED WEARABLE DEVICES AND USE OF AI IN PERSONALIZED PATIENT CARE TO FUEL MARKET GROWTH

- 9.5 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 9.5.1 NEED FOR STREAMLINED DRUG DEVELOPMENT PROCESSES AND ENHANCED CLINICAL TRIAL PARTICIPATION TO DRIVE MARKET

- 9.6 MEDTECH COMPANIES

- 9.6.1 MEDTECH COMPANIES TO IMPROVE DIAGNOSTIC ACCURACY AND FACILITATE PERSONALIZED TREATMENT PLANS

- 9.7 OTHER END USERS

10 AI IN TELEHEALTH & TELEMEDICINE MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 US to dominate North American market during forecast period

- 10.2.3 CANADA

- 10.2.3.1 Government initiatives on digital health integration to drive adoption of telehealth and mHealth applications

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 Favorable government initiatives to support market growth

- 10.3.3 UK

- 10.3.3.1 Growing reliance on digital healthcare platforms and increasing investments in remote mental health services to drive market

- 10.3.4 FRANCE

- 10.3.4.1 Favorable reimbursement for telemedicine solutions to spur market growth

- 10.3.5 ITALY

- 10.3.5.1 Strategic government regulations and high investments in healthcare digitalization to augment market growth

- 10.3.6 SPAIN

- 10.3.6.1 Rapid expansion of eHealth sector and increased adoption of wearable technologies to favor market growth

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 CHINA

- 10.4.2.1 Increasing private sector investments in digital infrastructure to boost market growth

- 10.4.3 JAPAN

- 10.4.3.1 High geriatric population and strong technological infrastructure to propel market growth

- 10.4.4 INDIA

- 10.4.4.1 Increased government focus on digital transformation in rural areas to aid market growth

- 10.4.5 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.5.2 BRAZIL

- 10.5.2.1 Increasing adoption of digital health solutions in public and private systems to aid market growth

- 10.5.3 MEXICO

- 10.5.3.1 Favorable regulatory scenario to fuel market growth

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 10.6.2 GCC COUNTRIES

- 10.6.2.1 Shortage of skilled healthcare workforce to support market growth

- 10.6.3 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN AI IN TELEHEALTH & TELEMEDICINE MARKET

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2023

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- 11.5.5.1 Company footprint

- 11.5.5.2 Region footprint

- 11.5.5.3 Function footprint

- 11.5.5.4 Application footprint

- 11.5.5.5 Component footprint

- 11.5.5.6 End-user footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

- 11.6.5.1 Detailed list of key startups/SMEs

- 11.6.5.2 Competitive benchmarking of key startups/SMEs, by region

- 11.7 COMPANY VALUATION & FINANCIAL METRICS

- 11.7.1 FINANCIAL METRICS

- 11.7.2 COMPANY VALUATION

- 11.8 BRAND/SOFTWARE COMPARISON

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES & APPROVALS

- 11.9.2 DEALS

12 COMPANY PROFILE

- 12.1 KEY PLAYERS

- 12.1.1 MEDTRONIC

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Services/Solutions offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches and approvals

- 12.1.1.3.2 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses & competitive threats

- 12.1.2 TELADOC HEALTH, INC.

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Services/Solutions offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches and upgrades

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses & competitive threats

- 12.1.3 KONINKLIJKE PHILIPS N.V.

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Services/Solutions offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product approvals

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses & competitive threats

- 12.1.4 CISCO SYSTEMS, INC.

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Services/Solutions offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses & competitive threats

- 12.1.5 GE HEALTHCARE

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Services/Solutions offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches and approvals

- 12.1.5.3.2 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses & competitive threats

- 12.1.6 EPIC SYSTEMS CORPORATION

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Services/Solutions offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches and upgrades

- 12.1.6.3.2 Deals

- 12.1.7 ORACLE

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Services/Solutions offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches

- 12.1.7.3.2 Deals

- 12.1.8 DOXIMITY, INC.

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Services/Solutions offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product upgrades

- 12.1.8.3.2 Deals

- 12.1.8.3.3 Other developments

- 12.1.9 INCLUDED HEALTH, INC.

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Services/Solutions offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Deals

- 12.1.9.3.2 Other developments

- 12.1.10 ZOOM COMMUNICATIONS, INC.

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Services/Solutions offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Deals

- 12.1.11 AMERICAN WELL

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Services/Solutions offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Product launches

- 12.1.11.3.2 Deals

- 12.1.11.3.3 Other developments

- 12.1.12 SIEMENS HEALTHINEERS AG

- 12.1.12.1 Business overview

- 12.1.12.2 Products/Services/Solutions offered

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Product approvals

- 12.1.13 AMC HEALTH

- 12.1.13.1 Business overview

- 12.1.13.2 Products/Services/Solutions offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Deals

- 12.1.14 TELESPECIALISTS

- 12.1.14.1 Business overview

- 12.1.14.2 Products/Services/Solutions offered

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Product launches

- 12.1.14.3.2 Deals

- 12.1.14.3.3 Other developments

- 12.1.15 WALGREENS BOOTS ALLIANCE, INC. (WALGREEN CO.)

- 12.1.15.1 Business overview

- 12.1.15.2 Products/Services/Solutions offered

- 12.1.15.3 Recent developments

- 12.1.15.3.1 Product launches

- 12.1.15.3.2 Expansions

- 12.1.16 CAREGILITY

- 12.1.16.1 Business overview

- 12.1.16.2 Products/Services/Solutions offered

- 12.1.16.3 Recent developments

- 12.1.16.3.1 Product launches and upgrades

- 12.1.16.3.2 Deals

- 12.1.16.3.3 Other developments

- 12.1.17 CVS HEALTH

- 12.1.17.1 Business overview

- 12.1.17.2 Products/Services/Solutions offered

- 12.1.17.3 Recent developments

- 12.1.17.3.1 Product launches and upgrades

- 12.1.18 ALIVECOR, INC.

- 12.1.18.1 Business overview

- 12.1.18.2 Products/Services/Solutions offered

- 12.1.18.3 Recent developments

- 12.1.18.3.1 Product launches and approvals

- 12.1.18.3.2 Deals

- 12.1.18.3.3 Other developments

- 12.1.19 ELATION

- 12.1.19.1 Business overview

- 12.1.19.2 Products/Services/Solutions offered

- 12.1.19.3 Recent developments

- 12.1.19.3.1 Deals

- 12.1.20 HEALTHTAP, INC.

- 12.1.20.1 Business overview

- 12.1.20.2 Products/Services/Solutions offered

- 12.1.20.3 Recent developments

- 12.1.20.3.1 Product launches

- 12.1.20.3.2 Deals

- 12.1.1 MEDTRONIC

- 12.2 OTHER PLAYERS

- 12.2.1 CURAI HEALTH

- 12.2.2 ANDOR HEALTH

- 12.2.3 K HEALTH

- 12.2.4 TRANSCARENT

- 12.2.5 BIOINTELLISENSE, INC.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS