|

시장보고서

상품코드

1810319

카테터 시장 : 유형별, 적응증별, 최종 사용자별, 지역별 예측(-2030년)Catheters Market by Type (Cardiovascular, Intravenous, Urological, Neurovascular), Indication - Global Forecast to 2030 |

||||||

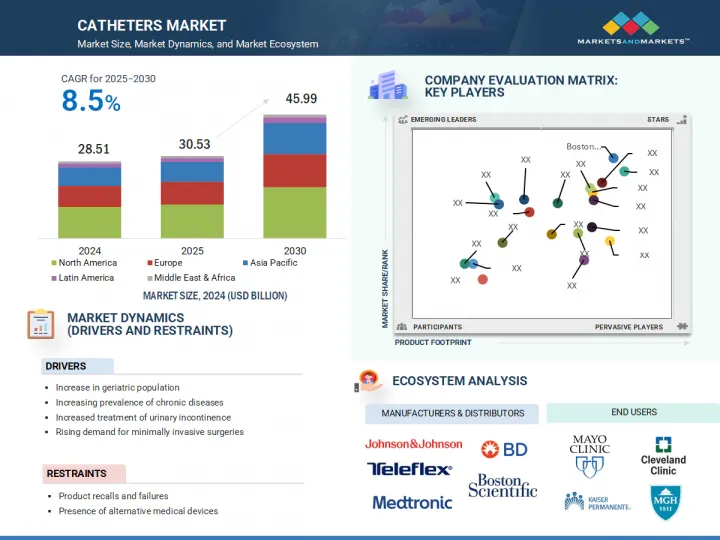

카테터 시장 규모는 심혈관, 비뇨기, 신경의 각 용도에서 이미지 유도 카테터 및 저침습 카테터를 이용한 절차의 채용이 증가하고 있기 때문에 견조한 성장이 예측됩니다.

스티어러블 카테터 및 감압 카테터, 약물 코팅 기술, 항균 코팅 등의 기술 혁신은 절차의 결과를 개선하고 합병증 발생률을 감소시킵니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문 | 유형별, 적응증별, 최종 사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

게다가 인터벤셔널 심장병학 및 신경학에서는 AI를 활용한 내비게이션과 실시간 영상의 도입이 진행되고 있어 특히 복잡한 사례에서의 수술 정밀도가 향상되고 있습니다. 게다가 3차 의료 환경에서의 하이브리드 수술실 및 카테터 랩의 개발에 의해 고도의 개입이 가능하게 되어, 수요에 박차가 걸리고 있습니다. 이러한 전문적인 진보는 특히 수기량이 많아 생활 습관병 증가에 직면하고 있는 지역에서 시장의 일관된 성장 궤도를 뒷받침하고 있습니다.

심혈관 카테터 부문은 2024년 최대 시장을 차지했으며, 이 동향은 예측 기간 동안 계속될 것으로 예측됩니다. 이 부문의 성장은 특히 노인에서 관상 동맥 질환, 심부전, 부정맥과 같은 심장 질환의 발생률이 증가하고 있으며, 혈관 성형술과 절제와 같은 카테터를 사용하는 저침습 절차를 필요로 하는 경우가 많다는 것이 배경에 있습니다. 약물 용출 카테터 및 화상 적합 카테터와 같은 카테터 기술의 진보로 절차의 안전성과 치료 성적이 향상되었습니다. 또한, 조기 심장 치료에 대한 사람들의 의식 증가 및 유리한 상환 정책은 주요 기업의 지속적인 연구개발 투자를 촉진하고 이 분야의 성장을 더욱 강화하고 있습니다.

2024년 세계 카테터 시장에서 병원 부문은 가장 큰 점유율을 차지했습니다. 이 부문의 지위는 이러한 환경에서 수행되는 치료량이 많고 고급 의료 인프라를 사용할 수 있기 때문입니다. 병원에서는 심혈관, 비뇨기, 신경 등 다양한 카테터를 이용한 치료가 이루어지고 있으며, 숙련된 전문가나 특수 기기가 필요합니다. 심장병 및 신장 질환과 같은 만성 질환으로 인한 입원 환자 수 증가도 이 수요에 기여합니다. 병원은 첨단 카테터 기술을 도입하고 적절한 감염 관리를 수행하는 설비를 갖추고 있습니다. 게다가 많은 나라에서 병원에서의 수술에 대한 강력한 상환 지원이 이용을 더욱 뒷받침하고 있습니다. 이 모든 요인이 결합되어 병원은 카테터의 가장 큰 최종 사용자가 되었습니다.

북미가 세계의 카테터 시장에서 가장 큰 시장을 차지한 것은 주로 첨단 헬스케어 인프라, 높은 헬스케어 지출, 혁신적인 의료 기술의 조기 도입으로 인한 것입니다. 또한 이 지역에서는 심혈관 장애, 신부전, 요실금 등 만성 질환의 유병률이 높아 다양한 유형의 카테터 수요를 크게 견인하고 있습니다. 또한 주요 카테터 제조업체, 강력한 유통망, 확립된 상환 정책이 병원, 클리닉 및 외래수술센터(ASC)에서 광범위한 사용을 지원합니다. 유리한 규제 당국의 승인, 저침습 절차에 대한 선호도 증가, 노인 인구 증가가 시장을 더욱 밀어 올리고 있습니다. 이러한 요인들이 함께 북미는 세계 카테터 시장을 독점하고 있습니다.

이 보고서는 세계 카테터 시장을 조사했으며, 유형별, 적응증별, 최종 사용자별, 지역별 동향, 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 서문

- 시장 역학

- 기술 분석

- 규제 상황

- 특허 분석

- 무역 분석

- 상환 시나리오

- 주된 회의 및 이벤트(2025-2026년)

- 주요 이해관계자 및 구매 기준

- 가격 분석

- 밸류체인 분석

- 생태계 분석

- AI 및 생성형 AI가 카테터 시장에 미치는 영향

- 고객의 비즈니스에 영향을 미치는 동향 및 혼란

- 투자 및 자금조달 시나리오

- 카테터 시장 : 미국 관세의 영향(2025년)

제6장 카테터 시장 : 유형별

- 서문

- 심혈관 카테터

- 정맥 카테터

- 비뇨기 카테터

- 특수 카테터

- 신경혈관 카테터

제7장 카테터 시장 : 적응증별

- 서문

- 심장 질환

- 신경혈관 질환

- 요로 질환

- 혈관질환

- IV 약제 투여 및 체액 관리

- 신장 질환

- 수혈

- 기타

제8장 카테터 시장 : 최종 사용자별

- 서문

- 병원

- 외래수술센터(ASC)

- 장기 요양 시설

- 진단 이미지 센터

- 외래 진료소

- 기타

제9장 카테터 시장 : 지역별

- 서문

- 북미

- 북미의 거시경제 전망

- 북미 : 정맥 카테터의 유형별 수량 분석(2023-2030년)(1,000개)

- 미국

- 캐나다

- 유럽

- 유럽의 거시 경제 전망

- 유럽 : 정맥 카테터의 유형별 수량 분석(2023-2030년)(1,000개)

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타

- 아시아태평양

- 아시아태평양의 거시 경제 전망

- 아시아태평양 : 정맥 카테터의 유형별 수량 분석(2023-2030년)(1,000개)

- 일본

- 중국

- 인도

- 호주

- 한국

- 기타

- 라틴아메리카

- 라틴아메리카의 거시 경제 전망

- 라틴아메리카 : 정맥 카테터의 유형별 수량 분석(2023-2030년)(1,000개)

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- 중동 및 아프리카 : 정맥 카테터의 유형별 수량 분석(2023-2030년)(1,000개)

- GCC 국가

- 기타

제10장 경쟁 구도

- 개요

- 주요 진입기업의 전략 및 강점

- 카테터 시장에서 주요 기업의 수익 분석(2022-2024년)

- 시장 점유율 분석

- 기업 평가 매트릭스 : 주요 진입기업(2024년)

- 기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

- 브랜드 및 제품 비교

- 주요 기업의 연구 개발비

- 기업 평가 및 재무지표

- 경쟁 시나리오

제11장 기업 프로파일

- 주요 진출기업

- BOSTON SCIENTIFIC CORPORATION

- MEDTRONIC PLC

- B. BRAUN SE

- BECTON, DICKINSON AND COMPANY

- STRYKER CORPORATION

- ABBOTT LABORATORIES

- TERUMO CORPORATION

- COLOPLAST A/S

- CONVATEC GROUP PLC

- MERIT MEDICAL SYSTEMS, INC.

- JOHNSON & JOHNSON

- COOK

- EDWARDS LIFESCIENCES CORPORATION

- NIPRO CORPORATION

- TELEFLEX INCORPORATED

- CARDINAL HEALTH, INC.

- HOLLISTER INCORPORATED

- INTEGRA LIFESCIENCES HOLDINGS CORPORATION

- KONINKLIJKE PHILIPS NV

- MICROPORT SCIENTIFIC CORPORATION

- 기타 기업

- AMECATH

- SIS MEDICAL AG

- ANGIPLAST PRIVATE LIMITED

- RELISYS MEDICAL DEVICES LIMITED

- CAGENT VASCULAR

- BIOTRONIK

- ADVIN HEALTH CARE

- ALVIMEDICA

- INGENION MEDICAL LIMITED

- SUMMA THERAPEUTICS, LLC

제12장 부록

AJY 25.09.19The catheters market is projected to grow steadily, driven by the increasing adoption of image-guided and minimally invasive catheter-based procedures across cardiovascular, urological, and neurological applications. Innovations such as steerable and pressure-sensitive catheters, drug-coated technologies, and antimicrobial coatings improve procedural outcomes and reduce complication rates.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Type, Indication, End User, Region |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa |

Additionally, the rising deployment of AI-powered navigation and real-time imaging in interventional cardiology and neurology enhances procedural precision, particularly in complex cases. Demand is further fueled by the development of hybrid operating rooms and catheter labs in tertiary care settings, enabling advanced interventions. These specialized advancements propel the market's consistent growth trajectory, especially in regions facing high procedural volumes and increasing lifestyle-related diseases.

"By type, the cardiovascular catheters segment accounted for the largest market in 2024."

The cardiovascular catheters segment accounted for the largest market in 2024, and this trend is projected to continue during the forecast period. The growth of this segment is fueled by the increasing incidence of heart conditions, such as coronary artery disease, heart failure, and arrhythmias, particularly among older adults, often requiring minimally invasive procedures like angioplasty and ablation, which involve the use of catheters. Advancements in catheter technologies, including drug-eluting and imaging-compatible catheters, have improved procedure safety and outcomes. Additionally, the rising awareness of people regarding early cardiac care and favorable reimbursement policies is driving continuous R&D investments by key players, further boosting the segment's growth.

"By end user, the hospitals segment accounted for the largest share in the catheters market in 2024."

The hospitals segment accounted for the largest share of the global catheters market in 2024. The segment's position can be attributed to the high volume of procedures performed in these settings and the availability of advanced medical infrastructure. Hospitals handle various catheter-based treatments, including cardiovascular, urinary, and neurological procedures requiring skilled professionals and specialized equipment. The rising number of inpatient admissions for chronic conditions, such as heart disease and kidney disorders, is also contributing to this demand. Hospitals are better equipped to adopt advanced catheter technologies and ensure proper infection control practices. Additionally, many countries' strong reimbursement support for hospital-based procedures further boosts utilization. All these factors collectively make hospitals the largest end users of catheters.

"North America accounted for the largest share of the global catheters market in 2024."

North America accounted for the largest market in the global catheters market, mainly due to its advanced healthcare infrastructure, high healthcare spending, and early adoption of innovative medical technologies. Additionally, the region sees a high prevalence of chronic diseases like cardiovascular disorders, kidney failure, and urinary incontinence, which significantly drives the demand for various catheter types. Moreover, leading catheter manufacturers, strong distribution networks, and well-established reimbursement policies support widespread usage across hospitals, clinics, and ambulatory surgical centers. Favorable regulatory approvals, growing preference for minimally invasive procedures, and rising geriatric population further boost the market. These combined factors make North America the dominant global catheter market in the region.

Breakdown of Supply-side Primary Interviews:

- By Company Type: Tier 1 - 45%, Tier 2 - 20%, and Tier 3 - 35%

- By Designation: C-level Executives - 35%, Directors - 25%, and Other Designations - 40%

- By Region: North America - 40%, Europe - 25%, Asia Pacific - 20%, Latin America - 10%, Middle East & Africa - 5%

Research Coverage

This report studies the catheters market in terms of type, indication, end user, and region. It also studies market growth factors (drivers, restraints, opportunities, and challenges). The report further analyzes the market's opportunities and challenges and details the competitive landscape for market leaders. It analyzes micro markets concerning their growth trends and forecasts the revenue of the market segments concerning five main regions and respective countries.

Reasons to Buy the Report

The report can help established and new entrants/smaller firms gauge the market's pulse, which, in turn, would help them garner a greater share. The report provides insights into the following pointers:

- Analysis of key drivers, restraints, opportunities, and challenges influencing the growth of the catheters market

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the catheters market

- Market Development: Comprehensive information about lucrative emerging markets across regions

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the catheters market

- Competitive Assessment: In-depth assessment of market share, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the catheters market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 MARKETS COVERED

- 1.2.2 INCLUSIONS & EXCLUSIONS

- 1.2.3 YEARS CONSIDERED

- 1.3 CURRENCY

- 1.4 UNIT CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 TOP-DOWN APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 RISK ASSESSMENT

- 2.7 RESEARCH LIMITATIONS

- 2.7.1 METHODOLOGY-RELATED LIMITATIONS

- 2.7.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 CATHETERS MARKET OVERVIEW

- 4.2 NORTH AMERICA: CATHETERS MARKET OVERVIEW

- 4.3 CATHETERS MARKET: REGIONAL MIX

- 4.4 CATHETERS MARKET: GEOGRAPHICAL GROWTH OPPORTUNITIES

- 4.5 CATHETERS MARKET: DEVELOPING VS. DEVELOPED MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising geriatric population

- 5.2.1.2 Increasing prevalence of chronic diseases

- 5.2.1.3 Increased awareness and treatment of urinary incontinence

- 5.2.1.4 Rising demand for minimally invasive surgeries

- 5.2.2 RESTRAINTS

- 5.2.2.1 Product recalls and failures

- 5.2.2.2 Presence of substitute medical devices

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing demand in emerging markets

- 5.2.3.2 Technological advancements and product innovation

- 5.2.4 CHALLENGES

- 5.2.4.1 Integration complexity with existing production lines

- 5.2.1 DRIVERS

- 5.3 TECHNOLOGY ANALYSIS

- 5.3.1 KEY TECHNOLOGIES

- 5.3.1.1 Antimicrobial-coated catheters

- 5.3.1.2 Drug-eluting catheters

- 5.3.2 COMPLEMENTARY TECHNOLOGIES

- 5.3.2.1 Hydrophilic coatings for catheters

- 5.3.2.2 Ultrasound-guided insertion systems

- 5.3.3 ADJACENT TECHNOLOGIES

- 5.3.3.1 Minimally invasive surgical devices

- 5.3.1 KEY TECHNOLOGIES

- 5.4 PORTER'S FIVE FORCES ANALYSIS

- 5.4.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.4.2 BARGAINING POWER OF BUYERS

- 5.4.3 BARGAINING POWER OF SUPPLIERS

- 5.4.4 THREAT OF SUBSTITUTES

- 5.4.5 THREAT OF NEW ENTRANTS

- 5.5 REGULATORY LANDSCAPE

- 5.5.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.5.2 REGULATORY FRAMEWORK

- 5.5.2.1 North America

- 5.5.2.1.1 US

- 5.5.2.1.2 Canada

- 5.5.2.2 Europe

- 5.5.2.3 Asia Pacific

- 5.5.2.3.1 China

- 5.5.2.3.2 Japan

- 5.5.2.3.3 India

- 5.5.2.4 Latin America

- 5.5.2.4.1 Brazil

- 5.5.2.4.2 Mexico

- 5.5.2.5 Middle East

- 5.5.2.6 Africa

- 5.5.2.1 North America

- 5.6 PATENT ANALYSIS

- 5.6.1 INSIGHTS ON PATENT PUBLICATION TRENDS, TOP APPLICANTS AND JURISDICTION FOR CATHETERS MARKET, JANUARY 2015-DECEMBER 2025

- 5.6.2 LIST OF MAJOR PATENTS, 2023-2024

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 901839, 2020-2024

- 5.7.2 EXPORT DATA FOR HS CODE 901839, 2020-2024

- 5.8 REIMBURSEMENT SCENARIO

- 5.9 KEY CONFERENCES & EVENTS, 2025-2026

- 5.10 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.10.2 KEY BUYING CRITERIA

- 5.11 PRICING ANALYSIS

- 5.11.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TYPE, 2022-2024

- 5.11.2 AVERAGE SELLING PRICE TREND OF CATHETERS, BY REGION, 2022-2024

- 5.12 VALUE CHAIN ANALYSIS

- 5.13 ECOSYSTEM ANALYSIS

- 5.14 IMPACT OF AI/GEN AI ON CATHETERS MARKET

- 5.15 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.16 INVESTMENT & FUNDING SCENARIO

- 5.17 CATHETERS MARKET: IMPACT OF 2025 US TARIFF

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 North America

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.5 IMPACT ON END USERS

- 5.17.5.1 Hospitals

- 5.17.5.2 Ambulatory surgical centers

- 5.17.5.3 Long-term care facilities

- 5.17.5.4 Diagnostic imaging centers

- 5.17.5.5 Outpatient clinics

- 5.17.5.6 Other end users

6 CATHETERS MARKET, BY TYPE

- 6.1 INTRODUCTION

- 6.2 CARDIOVASCULAR CATHETERS

- 6.2.1 HIGH PREVALENCE OF CARDIOVASCULAR DISEASES AND GROWING INTERVENTIONAL PROCEDURES TO FUEL DEMAND

- 6.2.2 ELECTROPHYSIOLOGY CATHETERS

- 6.2.2.1 Increasing prevalence of atrial fibrillation and expansion of electrophysiology labs to drive segment

- 6.2.3 ANGIOGRAPHY CATHETERS

- 6.2.3.1 Growing use of minimally invasive diagnostics and better imaging outcomes to propel growth

- 6.2.4 CORONARY BALLOON CATHETERS

- 6.2.4.1 Rapid growth in percutaneous coronary interventions and technological innovation to support growth

- 6.2.5 IVUS/OCT CATHETERS

- 6.2.5.1 Integration of intravascular imaging into PCI and clinical guidelines to drive uptake

- 6.2.6 GUIDING CATHETERS

- 6.2.6.1 Versatility in access and support during complex interventions to boost demand

- 6.2.7 OTHER CARDIOVASCULAR CATHETERS

- 6.3 INTRAVENOUS CATHETERS

- 6.3.1 INCREASING USE IN LONG-TERM THERAPIES AND HOSPITAL-ACQUIRED INFECTION PREVENTION EFFORTS TO DRIVE GROWTH

- 6.3.2 GLOBAL VOLUME ANALYSIS OF INTRAVENOUS CATHETER TYPES, 2023-2030 (THOUSAND UNITS)

- 6.3.3 CENTRAL VENOUS CATHETERS

- 6.3.3.1 Rising use in intensive and emergency care, along with multi-lumen design advancements, to drive demand

- 6.3.3.2 Peripherally inserted central catheters

- 6.3.3.2.1 Preference for long-term, outpatient IV therapy and reduced complication rates to drive use

- 6.3.3.3 Non-tunneled central venous catheters

- 6.3.3.3.1 Immediate access in emergency and ICU settings supports continued use

- 6.3.3.4 Skin-tunneled central venous catheters

- 6.3.3.4.1 Low infection risk and suitability for long-term therapies drive adoption

- 6.3.3.5 Implantable ports

- 6.3.3.5.1 Rise in cancer prevalence and demand for discreet, low-maintenance access devices drive use

- 6.3.4 PERIPHERAL INTRAVENOUS CATHETERS

- 6.3.4.1 High frequency of use and cost-effectiveness drive widespread adoption

- 6.3.5 MIDLINE PERIPHERAL CATHETERS

- 6.3.5.1 Rising preference in infection-prone patients and long-duration therapies to fuel market growth

- 6.4 UROLOGICAL CATHETERS

- 6.4.1 AGING POPULATION AND RISE IN RENAL AND UROLOGICAL DISORDERS TO DRIVE DEMAND

- 6.4.2 URINARY CATHETERS

- 6.4.2.1 Rising geriatric population and increased incidence of urinary incontinence - key drivers of growth

- 6.4.2.2 Indwelling catheters

- 6.4.2.2.1 Hospital-acquired urinary retention cases and long-term catheterization needs to drive demand

- 6.4.2.3 Intermittent catheters

- 6.4.2.3.1 Rising preference for self-catheterization and reduced infection risk accelerates adoption

- 6.4.2.4 External catheters

- 6.4.2.4.1 Growing use of non-invasive options in female and bedridden patients to fuel demand

- 6.4.3 DIALYSIS CATHETERS

- 6.4.3.1 Rising prevalence of end-stage renal disease and need for immediate vascular access to drive use

- 6.4.3.2 Peritoneal dialysis catheters

- 6.4.3.2.1 Preference for home-based renal therapy to support segment growth

- 6.4.3.3 Hemodialysis catheters

- 6.4.3.3.1 Increasing prevalence of end-stage renal disease and urgency for rapid vascular access to drive demand

- 6.5 SPECIALTY CATHETERS

- 6.5.1 DIVERSE CLINICAL UTILITY AND ADVANCEMENTS IN MINIMALLY INVASIVE MONITORING TO SUPPORT GROWTH

- 6.5.2 PRESSURE & HEMODYNAMIC CATHETERS

- 6.5.2.1 Precision in critical care and expanding cardiac monitoring - key drivers

- 6.5.3 TEMPERATURE MONITORING CATHETERS

- 6.5.3.1 Segment to gain traction due to need for precise core temperature control in critical illness

- 6.5.4 INTRAUTERINE INSEMINATION CATHETERS

- 6.5.4.1 Rising use of assisted reproduction and favorable clinical outcomes support growth of segment

- 6.5.5 OTHER SPECIALTY CATHETERS

- 6.6 NEUROVASCULAR CATHETERS

- 6.6.1 INCREASING STROKE BURDEN AND SHIFT TOWARD ENDOVASCULAR THERAPY TO ACCELERATE DEMAND

7 CATHETERS MARKET, BY INDICATION

- 7.1 INTRODUCTION

- 7.2 CARDIAC DISEASES

- 7.2.1 GROWING CARDIOVASCULAR DISEASE BURDEN TO DRIVE DOMINANCE OF SEGMENT

- 7.3 NEUROVASCULAR CONDITIONS

- 7.3.1 INCREASING STROKE INCIDENCE AND ADVANCED NEURO-INTERVENTION TECHNIQUES TO FUEL SEGMENT

- 7.4 URINARY CONDITIONS

- 7.4.1 RISING CASES OF URINARY INCONTINENCE AND UROLOGICAL DISORDERS TO DRIVE DEMAND

- 7.5 VASCULAR DISEASES

- 7.5.1 PREVALENCE OF PERIPHERAL ARTERY DISEASE AND DEEP VEIN THROMBOSIS AIDS GROWTH OF SEGMENT

- 7.6 IV MEDICATION DELIVERY & FLUID MANAGEMENT

- 7.6.1 GROWING USE OF LONG-TERM IV THERAPY IN CHRONIC CONDITIONS TO SUPPORT EXPANSION OF SEGMENT

- 7.7 KIDNEY DISEASES

- 7.7.1 HIGH GLOBAL BURDEN OF END-STAGE RENAL DISEASE TO ACCELERATE GROWTH

- 7.8 BLOOD TRANSFUSION

- 7.8.1 INCREASE IN SURGICAL VOLUME AND CRITICAL CARE NEEDS TO DRIVE DEMAND

- 7.9 OTHER INDICATIONS

8 CATHETERS MARKET, BY END USER

- 8.1 INTRODUCTION

- 8.2 HOSPITALS

- 8.2.1 RAPID EXPANSION OF HOSPITAL CAPACITY AND INFRASTRUCTURE TO DRIVE MARKET

- 8.3 AMBULATORY SURGICAL CENTERS

- 8.3.1 SURGE IN OUTPATIENT PROCEDURES AND REGULATORY SUPPORT TO SPUR GROWTH

- 8.4 LONG-TERM CARE FACILITIES

- 8.4.1 AGING POPULATION AND ASSISTED LIVING DEMAND INCREASED CATHETER USE

- 8.5 DIAGNOSTIC IMAGING CENTERS

- 8.5.1 HIGH VOLUME OF IMAGING PROCEDURES BOOSTS CATHETER DEMAND

- 8.6 OUTPATIENT CLINICS

- 8.6.1 RISING OUTPATIENT VISIT VOLUMES AND PROCEDURAL SHIFT INCREASE CATHETER USE

- 8.7 OTHER END USERS

9 CATHETERS MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 9.2.2 NORTH AMERICA: VOLUME ANALYSIS OF INTRAVENOUS CATHETER TYPES, 2023--2030 (THOUSAND UNITS)

- 9.2.3 US

- 9.2.3.1 Rising chronic disease burden spurs innovation demand in catheter use

- 9.2.4 CANADA

- 9.2.4.1 Aging population and rising hypertension & urinary conditions lift catheter demand

- 9.3 EUROPE

- 9.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 9.3.2 EUROPE: VOLUME ANALYSIS OF INTRAVENOUS CATHETER TYPES, 2023-2030 (THOUSAND UNITS)

- 9.3.3 GERMANY

- 9.3.3.1 Aging population and high PCI volume to drive catheter usage

- 9.3.4 UK

- 9.3.4.1 High prevalence of long-term urinary catheter use maintained by community nursing demand

- 9.3.5 FRANCE

- 9.3.5.1 Widespread use of intermittent urinary catheters to support second-largest share

- 9.3.6 SPAIN

- 9.3.6.1 Rising UTI burden in nursing homes boosts urinary catheter demand

- 9.3.7 ITALY

- 9.3.7.1 Recent heightened CAUTI risk in ICUs underpins demand for safer urinary catheters

- 9.3.8 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 9.4.2 ASIA PACIFIC VOLUME ANALYSIS OF INTRAVENOUS CATHETER TYPES, 2023-2030 (THOUSAND UNITS)

- 9.4.3 JAPAN

- 9.4.3.1 Aging population and rising cardiovascular care needs to boost demand for catheters

- 9.4.4 CHINA

- 9.4.4.1 High cardiovascular disease burden and expanding care access to drive demand

- 9.4.5 INDIA

- 9.4.5.1 Set to be fastest-growing market with escalating CVD incidence

- 9.4.6 AUSTRALIA

- 9.4.6.1 High cardiovascular disease burden and strong government support to drive growth

- 9.4.7 SOUTH KOREA

- 9.4.7.1 Rising arrhythmia treatments and expanding interventional cardiology infrastructure bolster catheter demand

- 9.4.8 REST OF ASIA PACIFIC

- 9.5 LATIN AMERICA

- 9.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 9.5.2 LATIN AMERICA: VOLUME ANALYSIS OF INTRAVENOUS CATHETER TYPES, 2023-2030 (THOUSAND UNITS)

- 9.5.3 BRAZIL

- 9.5.3.1 Robust public healthcare infrastructure and high cardiovascular procedure volume drive dominance

- 9.5.4 MEXICO

- 9.5.4.1 High diabetes and cardiovascular disease prevalence spurs catheter demand

- 9.5.5 REST OF LATIN AMERICA

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 9.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS OF INTRAVENOUS CATHETER TYPES, 2023-2030 (THOUSAND UNITS)

- 9.6.3 GCC COUNTRIES

- 9.6.3.1 Market uplift through strategic healthcare investments and rising procedure volumes

- 9.6.3.2 Kingdom of Saudi Arabia (KSA)

- 9.6.3.2.1 Market gains strength from healthcare transformation and NCD burden

- 9.6.3.3 United Arab Emirates (UAE)

- 9.6.3.3.1 Market growth anchored in advanced hospital infrastructure and medical tourism

- 9.6.3.4 Other GCC Countries

- 9.6.4 REST OF MIDDLE EAST & AFRICA

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 10.3 REVENUE ANALYSIS OF KEY PLAYERS IN CATHETERS MARKET (2022-2024)

- 10.4 MARKET SHARE ANALYSIS

- 10.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.5.1 STARS

- 10.5.2 EMERGING LEADERS

- 10.5.3 PERVASIVE PLAYERS

- 10.5.4 PARTICIPANTS

- 10.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.5.5.1 Company footprint

- 10.5.5.2 Region footprint

- 10.5.5.3 Type footprint

- 10.5.5.4 Indication footprint

- 10.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.6.1 PROGRESSIVE COMPANIES

- 10.6.2 DYNAMIC COMPANIES

- 10.6.3 STARTING BLOCKS

- 10.6.4 RESPONSIVE COMPANIES

- 10.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.6.5.1 Detailed list of key startups/SMEs

- 10.6.5.2 Competitive benchmarking of key emerging players/startups

- 10.7 BRAND/PRODUCT COMPARISON

- 10.8 R&D EXPENDITURE OF KEY PLAYERS

- 10.9 COMPANY VALUATION & FINANCIAL METRICS

- 10.9.1 COMPANY VALUATION

- 10.9.2 FINANCIAL METRICS

- 10.10 COMPETITIVE SCENARIO

- 10.10.1 PRODUCT APPROVALS/LAUNCHES

- 10.10.2 DEALS

- 10.10.3 EXPANSIONS

- 10.10.4 OTHER DEVELOPMENTS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 BOSTON SCIENTIFIC CORPORATION

- 11.1.1.1 Business overview

- 11.1.1.2 Products offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches & approvals

- 11.1.1.3.2 Deals

- 11.1.1.4 MnM view

- 11.1.1.4.1 Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 MEDTRONIC PLC

- 11.1.2.1 Business overview

- 11.1.2.2 Products offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Product launches & approvals

- 11.1.2.3.2 Deals

- 11.1.2.4 MnM view

- 11.1.2.4.1 Right to win

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses and competitive threats

- 11.1.3 B. BRAUN SE

- 11.1.3.1 Business overview

- 11.1.3.2 Products offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Deals

- 11.1.3.3.2 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 BECTON, DICKINSON AND COMPANY

- 11.1.4.1 Business overview

- 11.1.4.2 Products offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches & approvals

- 11.1.4.3.2 Deals

- 11.1.4.3.3 Expansions

- 11.1.4.4 MnM view

- 11.1.4.4.1 Right to win

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses and competitive threats

- 11.1.5 STRYKER CORPORATION

- 11.1.5.1 Business overview

- 11.1.5.2 Products offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Product launches & approvals

- 11.1.5.3.2 Deals

- 11.1.5.4 MnM view

- 11.1.5.4.1 Right to win

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses and competitive threats

- 11.1.6 ABBOTT LABORATORIES

- 11.1.6.1 Business overview

- 11.1.6.2 Products offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Product launches & approvals

- 11.1.6.3.2 Deals

- 11.1.6.3.3 Other developments

- 11.1.7 TERUMO CORPORATION

- 11.1.7.1 Business overview

- 11.1.7.2 Products offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Product launches & approvals

- 11.1.7.3.2 Deals

- 11.1.7.3.3 Expansions

- 11.1.8 COLOPLAST A/S

- 11.1.8.1 Business overview

- 11.1.8.2 Products offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Product launches & approvals

- 11.1.8.3.2 Expansions

- 11.1.9 CONVATEC GROUP PLC

- 11.1.9.1 Business overview

- 11.1.9.2 Products offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Product launches & approvals

- 11.1.10 MERIT MEDICAL SYSTEMS, INC.

- 11.1.10.1 Business overview

- 11.1.10.2 Products offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Product launches & approvals

- 11.1.10.3.2 Deals

- 11.1.11 JOHNSON & JOHNSON

- 11.1.11.1 Business overview

- 11.1.11.2 Products offered

- 11.1.11.3 Recent developments

- 11.1.11.3.1 Product launches & approvals

- 11.1.11.3.2 Deals

- 11.1.12 COOK

- 11.1.12.1 Business overview

- 11.1.12.2 Products offered

- 11.1.12.3 Recent developments

- 11.1.12.3.1 Product launches & approvals

- 11.1.12.3.2 Deals

- 11.1.13 EDWARDS LIFESCIENCES CORPORATION

- 11.1.13.1 Business overview

- 11.1.13.2 Products offered

- 11.1.14 NIPRO CORPORATION

- 11.1.14.1 Business overview

- 11.1.14.2 Products offered

- 11.1.14.3 Recent developments

- 11.1.14.3.1 Expansions

- 11.1.15 TELEFLEX INCORPORATED

- 11.1.15.1 Business overview

- 11.1.15.2 Products offered

- 11.1.15.3 Recent developments

- 11.1.15.3.1 Product launches & approvals

- 11.1.15.3.2 Deals

- 11.1.16 CARDINAL HEALTH, INC.

- 11.1.16.1 Business overview

- 11.1.16.2 Products offered

- 11.1.16.3 Recent developments

- 11.1.16.3.1 Expansions

- 11.1.17 HOLLISTER INCORPORATED

- 11.1.17.1 Business overview

- 11.1.17.2 Products offered

- 11.1.17.3 Recent developments

- 11.1.17.3.1 Expansions

- 11.1.18 INTEGRA LIFESCIENCES HOLDINGS CORPORATION

- 11.1.18.1 Business overview

- 11.1.18.2 Products offered

- 11.1.19 KONINKLIJKE PHILIPS N.V.

- 11.1.19.1 Business overview

- 11.1.19.2 Products offered

- 11.1.19.3 Recent developments

- 11.1.19.3.1 Expansions

- 11.1.20 MICROPORT SCIENTIFIC CORPORATION

- 11.1.20.1 Business overview

- 11.1.20.2 Products offered

- 11.1.20.3 Recent developments

- 11.1.20.3.1 Product launches & approvals

- 11.1.1 BOSTON SCIENTIFIC CORPORATION

- 11.2 OTHER PLAYERS

- 11.2.1 AMECATH

- 11.2.2 SIS MEDICAL AG

- 11.2.3 ANGIPLAST PRIVATE LIMITED

- 11.2.4 RELISYS MEDICAL DEVICES LIMITED

- 11.2.5 CAGENT VASCULAR

- 11.2.6 BIOTRONIK

- 11.2.7 ADVIN HEALTH CARE

- 11.2.8 ALVIMEDICA

- 11.2.9 INGENION MEDICAL LIMITED

- 11.2.10 SUMMA THERAPEUTICS, LLC

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.3.1 PRODUCT ANALYSIS

- 12.3.2 GEOGRAPHIC ANALYSIS

- 12.3.3 COMPANY INFORMATION

- 12.3.4 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 12.3.5 COUNTRY-LEVEL VOLUME ANALYSIS

- 12.3.6 PRODUCT TYPE MARKET SHARE ANALYSIS (TOP 5 PLAYERS)

- 12.3.7 ANY CONSULTS/CUSTOM STUDIES AS PER CLIENT REQUIREMENTS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS