|

시장보고서

상품코드

1986228

크립토 쿨링 시장 예측(-2032년) : 냉각 방식(공랭, 수냉), 하드웨어 유형(CPU 마이닝, GPU 마이닝, ASIC 마이닝), 마이닝 규모(개인 마이너, 소규모 상용 마이너, 대규모 마이너), 지역별Crypto Cooling Market by Type of Cooling (Air Cooling, Liquid Cooling), Hardware Type (CPU Mining, GPU Mining, ASIC Mining), Crypto Mining Scale (Home Miner, Small Commercial Miner, Large Scale Miners), and Region - Global Forecast to 2032 |

||||||

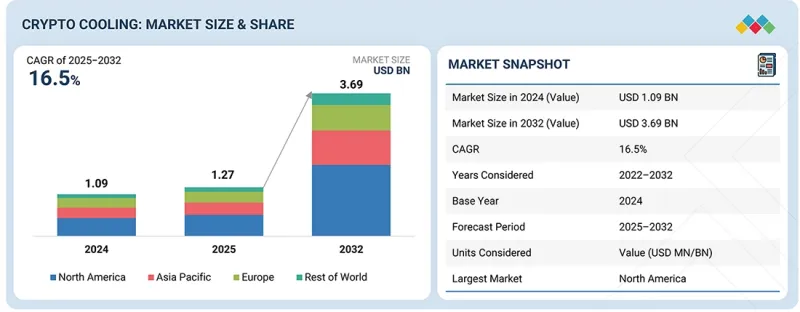

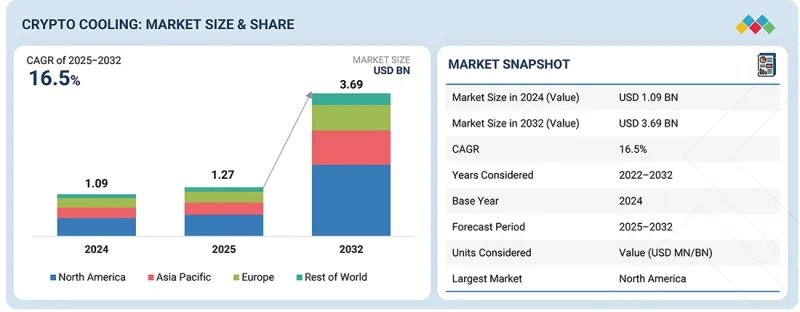

크립토 쿨링 시장 규모는 예측 기간 중 CAGR 16.5%로 확대하며, 2025년 12억 7,000만 달러에서 2032년에는 36억 9,000만 달러에 달할 것으로 전망되고 있습니다.

세계 크립토 쿨링 시장은 암호자산 채굴 기업이 사업을 유지하기 위해 상시 냉각이 필요한 산업 시설을 건설하면서 확대되고 있습니다. 더 높은 해시율과 소형화를 실현하는 채굴 장비의 개발로 인해 채굴 작업의 발열량이 증가하고 있으며, 첨단 냉각 시스템이 요구되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2032년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 단위 | 금액(달러) |

| 부문 | 냉각 방식, 하드웨어 유형, 채굴 규모, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 기타 지역 |

온도 변화는 데이터 처리 능력에 직접적인 영향을 미치며, 장비의 손상을 방지하기 위해 사업자는 시스템 성능을 유지해야 합니다. 시장 경쟁으로 인해 냉각 운영에 따른 2차 에너지 수요를 줄여야 하므로 채굴 기업은 총비용을 최적화해야 합니다. 첨단 냉각 기술이 주도하는 효율적인 냉각 시스템에 대한 세계 시장 수요는 모듈형 데이터센터 설계의 부상과 성능 중심의 마이닝 방식을 우선시하는 마이닝 사업에서 더욱 강화되고 있습니다.

"냉각 방식별로는 액체 냉각 부문이 예측 기간 중 금액 기준으로 가장 큰 점유율을 차지할 것으로 예측됩니다. "

산업 규모의 채굴 사업자들이 이 기술을 점점 더 많이 채택하고 있으므로 예측 기간 중 액체 냉각 부문이 금액 기준으로 가장 큰 점유율을 차지할 것으로 추정됩니다. 마이닝 팜은 운영이 최대 부하에 도달하고 랙 밀도가 높아지는 환경에서 기존 공랭식 냉각 시스템보다 우수한 방열 성능을 제공하므로 액체 기반 냉각 시스템을 선호하고 있습니다. 액침냉각 및 직접 액체 냉각 시스템을 도입하려면 맞춤형 엔지니어링, 유체 관리 시스템 및 인프라 구성 요소가 필요하므로 표준 설치 방법에 비해 전체 시스템 비용이 증가합니다. 채굴 사업자들은 전력 사용 효율을 높이고 향후 운영 비용을 절감하기 위해 첨단 냉각 시스템에 더 많은 비용을 투자하고 있습니다. 시설에 더 많은 초기 투자가 필요한 반면, 이 기술을 채택하는 기지가 증가함에 따라 액체 냉각 부문은 전 세계 암호화폐 냉각 산업에서 지배적인 시장 점유율을 유지하고 있습니다.

"하드웨어 유형별로는 예측 기간 중 ASIC 마이닝 부문이 금액 기준으로 가장 큰 점유율을 차지할 것으로 예측됩니다. "

이는 상업용 및 산업용 암호화폐 채굴 사업에서 ASIC 기반 하드웨어가 사용되고 있기 때문입니다. ASIC 마이너는 성능 향상과 전력 효율을 모두 필요로 하는 데이터센터에 높은 연산 성능을 제공하는 전용 장비로 존재합니다. 이러한 시스템은 집중적이고 지속적인 열을 발생시키기 때문에 소형 장비에 사용되는 기본 냉각 시스템보다 비용이 많이 드는 고급 냉각 시스템이 필요합니다. ASIC 채굴 사업에 자금을 투자하는 사업자들은 장비의 성능을 유지하고, 자산을 보호하고, 안정적인 운영 성과를 달성하기 위해 고품질 열 제어 시스템에 더 많은 자원을 할당하고 있습니다. ASIC 기술의 높은 채택률과 이에 따른 전용 냉각 시스템에 대한 수요는 예측 기간 중 세계 암호화폐 채굴 냉각 시장에서 이 부문의 선도적인 점유율을 유지할 것으로 보입니다.

예측 기간 중 북미가 가장 큰 성장 시장이 될 것으로 예측됩니다.

북미는 대규모 산업용 암호화폐 채굴 시설과 디지털 자산 시스템의 지속적인 개발로 인해 예측 기간 중 가장 큰 시장이 될 것으로 예측됩니다. 이 지역에서는 고급 냉각 기술을 필요로 하는 첨단 ASIC 채굴 장비를 지원하기 위해 채굴 업체들이 새로운 시설을 건설하고 있으므로 용량이 지속적으로 확대되고 있습니다. 인프라 프로젝트 개발은 신뢰할 수 있는 전력 시스템에 대한 접근성, 재생에너지 채택 확대, 특정 분야의 명확한 규제 프레임워크 등 세 가지 요인으로 인해 더욱 탄력을 받고 있습니다. 현재 북미의 사업자들은 높은 냉각 능력을 발휘하여 운영 비용을 절감하는 동시에 장비가 최적의 효율로 작동하도록 보장하는 에너지 절약형 냉각 시스템에 초점을 맞추었습니다. 이러한 요인들이 복합적으로 작용하여 예측 기간 중 북미는 암호자산 냉각 솔루션 시장에서 가장 빠르게 성장하는 시장이 될 것입니다.

세계의 크립토 쿨링 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 주요 신규 기술

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 크립토 쿨링 시장 : 냉각 방식별

제10장 크립토 쿨링 시장 : 하드웨어 유형별

제11장 크립토 쿨링 시장 : 채굴 규모별

제12장 크립토 쿨링 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.04.10The crypto cooling market is projected to grow from USD 1.27 billion in 2025 to USD 3.69 billion by 2032, at a CAGR of 16.5% during the forecast period. The global cryptocurrency cooling market is growing as cryptocurrency mining companies build industrial facilities that require constant cooling to sustain their operations. The development of mining equipment that produces higher hash rates and smaller equipment sizes has increased heat output in mining operations, requiring advanced cooling systems.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Type of Cooling, Hardware Type, Crypto Mining Scale, and Region |

| Regions covered | Asia Pacific, Europe, North America, and Rest of World |

Operators need to maintain system performance because temperature changes directly impact their ability to process data and protect their equipment from damage. Mining companies must now optimize their total expenses because market competition requires them to reduce their secondary energy needs stemming from cooling operations. The global market demand for efficient cooling systems, driven by advanced cooling technology, is being strengthened by the rise of modular data center designs and mining operations that prioritize performance-based mining methods.

"By type of cooling, the liquid cooling segment is estimated to hold the largest share, in terms of value, during the forecast period."

The liquid cooling segment is estimated to hold the largest share in terms of value during the forecast period, as industrial mining operations increasingly adopt this technology. Mining farms prefer liquid-based systems because they provide better heat dissipation than traditional air-cooling systems when operations reach maximum load capacity and operate at higher rack densities. The implementation of immersion and direct liquid-cooling systems requires customized engineering, fluid management systems, and infrastructure components, thereby increasing the total system value compared to standard installation methods. Mining operators spend more on advanced cooling systems to improve power usage efficiency and reduce future operational expenses. The liquid cooling segment maintains its dominant market share in the global crypto cooling industry because facilities require higher initial investments, while more locations implement this technology.

"By hardware type, the ASIC mining segment is estimated to hold the largest share, in terms of value, during the forecast period."

The ASIC mining segment is expected to hold the largest share in terms of value during the forecast period, as commercial and industrial cryptocurrency mining operations use ASIC-based hardware. ASIC miners exist as specialized equipment that delivers high computational performance to data centers that require both performance enhancement and power efficiency. The systems produce concentrated, continuous thermal output, which requires sophisticated cooling systems that cost more than the basic cooling systems used in smaller equipment. Operators who fund their ASIC mining operations allocate more resources to high-quality thermal control systems to maintain equipment performance, protect their assets, and achieve consistent operational results. The high adoption rate of ASIC technology, together with the need for specialized cooling systems, will drive its leading value share in the global crypto cooling market over the forecast period.

North America is projected to be the largest growing market during the forecast period.

North America is projected to be the largest market during the forecast period because of its extensive industrial cryptocurrency mining facilities and ongoing development of digital asset systems. The region has experienced continuous capacity growth because mining companies build new facilities to support their advanced ASIC mining equipment, which requires sophisticated cooling technologies. The development of infrastructure projects receives additional support from three factors: access to reliable power systems, growing adoption of renewable energy, and clear regulatory frameworks in specific areas. North American operators are now focusing on energy-saving cooling systems, which deliver high cooling capacity to reduce operational expenses while ensuring their equipment operates at optimal efficiency. The combination of these factors will make North America the fastest-expanding market for crypto cooling solutions throughout the forecast period.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1 - 30%, Tier 2 - 35%, and Tier 3 - 35%

- By Designation: C-Level Executives- 30%, Directors- 60%, and Others - 10%

- By Region: North America - 40%, Europe - 30%, Asia Pacific - 25%, Rest of World - 5%

Green Revolution Cooling (US), Submer (Spain), LiquidStack Holding B.V. (US), DCX Liquid Cooling Systems (Poland), and Engineered Fluids (US), among others, are the key players in the crypto cooling market. These players have adopted various strategies, including product launch and partnership to increase their market share and business revenue.

Research Coverage:

The report defines segments and projects the size of the crypto cooling market by type of cooling, hardware type, crypto mining scale, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as product launches and partnerships undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help market leaders/new entrants by providing the closest approximations of revenue for the crypto cooling market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (Rising power density of latest mining hardware, energy efficiency and sustainability push, integration with data center technologies), restraints (Crypto market volatility, high initial capital expenditure), opportunities (Integration with AI, telecom, and high-performance electronics, growth in advanced immersion, cooling systems in cryptocurrency mining data centers) and challenges (Lack of standardization, regulatory uncertainty) influencing the growth of the crypto cooling market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the crypto cooling market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the crypto cooling market across varied regions

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the crypto cooling market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Green Revolution Cooling (US), Submer (Spain), LiquidStack Holding B.V. (US), DCX Liquid Cooling Systems (Poland), and Engineered Fluids (US), among others, are the key players in the crypto cooling market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CRYPTO COOLING MARKET

- 3.2 CRYPTO COOLING MARKET, BY HARDWARE TYPE

- 3.3 CRYPTO COOLING MARKET, BY COOLING TECHNOLOGY

- 3.4 CRYPTO COOLING MARKET, BY HARDWARE TYPE AND REGION

- 3.5 CRYPTO COOLING MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising power density of latest mining hardware

- 4.2.1.2 Energy efficiency and sustainability push

- 4.2.1.3 Integration with datacenter technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 Crypto market volatility

- 4.2.2.2 High initial capital expenditure (CapEx)

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration with AI, telecom, and high-performance electronics

- 4.2.3.2 Growth in advanced immersion cooling systems in cryptocurrency mining data centers

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of standardization

- 4.2.4.2 Regulatory uncertainty

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN CRYPTO COOLING MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 LARGE-SCALE BITCOIN MINING FARMS

- 5.2.4 COLOCATION MINING FACILITIES

- 5.2.5 ENERGY-INTEGRATED MINING PROJECTS (FLARE GAS & STRANDED ENERGY)

- 5.2.6 HIGH-DENSITY DIGITAL INFRASTRUCTURE DEPLOYMENTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 DMG BLOCKCHAIN SOLUTIONS - STRATEGIC DEPLOYMENT OF IMMERSION COOLING TO ENHANCE MINING EFFICIENCY

- 5.7.2 HUT 8 - DRIVING STANDARDIZATION IN BITCOIN MINING HARDWARE THROUGH HPC-COMPATIBLE FORM FACTORS

- 5.7.3 ENHANCING MINING EFFICIENCY WITH FOGHASHING'S IMMERSION COOLING SOLUTION

- 5.8 IMPACT OF 2025 US TARIFF ON CRYPTO COOLING MARKET

- 5.8.1 INTRODUCTION

- 5.8.2 KEY TARIFF RATES

- 5.8.3 PRICE IMPACT ANALYSIS

- 5.8.4 IMPACT ON MAJOR COUNTRY/REGION

- 5.8.4.1 US

- 5.8.4.2 Europe

- 5.8.4.3 Asia Pacific

6 KEY EMERGING TECHNOLOGIES

- 6.1 OVERVIEW

- 6.2 AIR COOLING TECHNOLOGY

- 6.2.1 IMMERSION COOLING TECHNOLOGY

- 6.2.2 DIRECT-TO-CHIP (D2C) LIQUID COOLING

- 6.3 COMPLEMENTARY TECHNOLOGIES

- 6.3.1 WASTE HEAT RECOVERY & DISTRICT HEATING INTEGRATION

- 6.3.2 THERMAL MONITORING & AI-BASED COOLING OPTIMIZATION SYSTEMS

- 6.4 ADJACENT TECHNOLOGIES

- 6.4.1 HIGH-DENSITY AI/HPC DATA CENTER COOLING TECHNOLOGIES

- 6.4.2 MODULAR PREFABRICATED LIQUID-COOLED CONTAINERIZED DATA CENTERS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 DOCUMENT TYPE

- 6.5.4 INSIGHTS

- 6.5.5 LEGAL STATUS OF PATENTS

- 6.5.6 JURISDICTION ANALYSIS

- 6.5.7 TOP APPLICANTS

- 6.5.8 LIST OF MAJOR PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 ULTRA-HIGH-DENSITY MINING FARMS

- 6.6.2 RENEWABLE-POWERED & OFF-GRID MINING FACILITIES

- 6.6.3 WASTE HEAT REUSE & DISTRICT HEATING INTEGRATION

- 6.6.4 ENERGY-EFFICIENT BUILDING MATERIALS: ADVANCED INSULATION SYSTEMS SUPPORTING GLOBAL ENERGY EFFICIENCY STANDARDS

- 6.6.5 MODULAR LIQUID-COOLED CONTAINERIZED DEPLOYMENTS

- 6.7 IMPACT OF AI/GEN AI ON CRYPTO COOLING MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES: COMPANIES/INSTITUTIONS USE CASES

- 6.7.3 CASE STUDIES OF CRYPTO COOLING MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN CRYPTO COOLING MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 BITMAIN: LARGE-SCALE IMMERSION-COOLED MINING DEPLOYMENTS

- 6.8.2 RIOT PLATFORMS: INDUSTRIAL-SCALE LIQUID-COOLED MINING EXPANSION

- 6.8.3 NORTHERN DATA GROUP: SUSTAINABLE & HIGH-EFFICIENCY DATA CENTER COOLING INTEGRATION

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO APPLICATIONS OF CRYPTO COOLING

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 CRYPTO COOLING MARKET, BY TYPE OF COOLING

- 9.1 INTRODUCTION

- 9.2 AIR COOLING

- 9.2.1 COST-SENSITIVE OPERATORS AND EXPANSION OF MINING IN COOLER CLIMATES TO DRIVE MARKET

- 9.3 LIQUID COOLING

- 9.3.1 DIRECT-TO-CHIP

- 9.3.1.1 Ability to provide balanced solution to drive market

- 9.3.2 IMMERSION COOLING

- 9.3.2.1 Steady rise in global network hashrate and mining difficulty to drive market

- 9.3.1 DIRECT-TO-CHIP

10 CRYPTO COOLING MARKET, BY HARDWARE TYPE

- 10.1 INTRODUCTION

- 10.2 CPU MINING

- 10.2.1 RISE OF HOME-BASED MINING EXPERIMENTATION AND BLOCKCHAIN LEARNING TO INCREASE DEMAND

- 10.3 GPU MINING

- 10.3.1 CONTINUED INTEREST IN MINEABLE ALTERNATIVE CRYPTOCURRENCIES TO INCREASE DEMAND

- 10.4 ASIC MINING

- 10.4.1 ONGOING IMPROVEMENTS IN CHIP DESIGN AND EXPANSION OF INDUSTRIAL MINING FACILITIES TO DRIVE MARKET

11 CRYPTO COOLING MARKET, BY CRYPTO MINING SCALE

- 11.1 INTRODUCTION

- 11.2 HOME MINERS

- 11.2.1 BULLISH CRYPTOCURRENCY CYCLES AND RISING RETAIL INTEREST IN MINEABLE ALTCOINS TO DRIVE MARKET

- 11.3 SMALL COMMERCIAL MINERS

- 11.3.1 INCREASING HARDWARE DENSITY TO INCREASE DEMAND

- 11.4 LARGE-SCALE MINERS

- 11.4.1 RISING INSTITUTIONAL PARTICIPATION AND EXPANSION OF RENEWABLE-POWERED MINING SITES TO DRIVE MARKET

12 CRYPTO COOLING MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Industrial-scale mining expansion, grid-integrated operations, and post-halving efficiency optimization to drive market

- 12.2.2 CANADA

- 12.2.2.1 Low carbon hydropower access, cold climate efficiency advantages, and ESG-aligned infrastructure optimization to drive market

- 12.2.3 MEXICO

- 12.2.3.1 High-temperature operating conditions, industrial energy integration, and nearshore infrastructure expansion to drive market

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 RUSSIA

- 12.3.1.1 Low-cost hydropower in Siberia, cold climate efficiency advantages, and formalization of industrial mining regulations to drive market

- 12.3.2 GERMANY

- 12.3.2.1 Stringent energy efficiency regulations, waste heat recovery mandates, and renewable-integrated high-performance infrastructure to drive market

- 12.3.3 NORWAY

- 12.3.3.1 100% renewable hydropower access, cold climate free-cooling advantages, and policy-driven heat reuse integration to drive market

- 12.3.4 SWEDEN

- 12.3.4.1 Renewable-nuclear power mix, cold climate free-cooling efficiency, and policy-driven energy optimization requirements to drive market

- 12.3.5 IRELAND

- 12.3.5.1 Growth in commercial construction sector to drive market

- 12.3.6 REST OF EUROPE

- 12.3.1 RUSSIA

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Export-oriented ASIC manufacturing leadership, advanced cooling component production, and national energy efficiency technology initiatives to drive market

- 12.4.2 KAZAKHSTAN

- 12.4.2.1 Post-ban hashrate migration, regulatory formalization, and energy-efficiency optimization under rising electricity tariffs to drive market

- 12.4.3 MALAYSIA

- 12.4.3.1 Tropical climate efficiency needs, grid enforcement formalization, and renewable-backed industrial infrastructure development to drive market

- 12.4.4 THAILAND

- 12.4.4.1 Tropical climate thermal challenges, structured digital asset regulation, and renewable-backed industrial infrastructure expansion to drive market

- 12.4.5 AUSTRALIA

- 12.4.5.1 Renewable energy integration, high electricity price volatility, and climate-driven demand for advanced liquid cooling systems to drive market

- 12.4.6 INDONESIA

- 12.4.6.1 Tropical climate thermal demands, expanding geothermal renewable capacity, and structured regulatory support for digital assets to drive market

- 12.4.7 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 REST OF WORLD

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 MARKET SHARE ANALYSIS, 2024

- 13.4 BRAND/PRODUCT COMPARISON

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Type of cooling footprint

- 13.5.5.4 Hardware type footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 COMPETITIVE SCENARIO

- 13.7.1 PRODUCT LAUNCHES

- 13.7.2 DEALS

14 COMPANY PROFILES

- 14.1 MAJOR PLAYERS

- 14.1.1 SUBMER

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 GREEN REVOLUTION COOLING

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 LIQUIDSTACK HOLDING B.V.

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 ENGINEERED FLUIDS

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 DCX LIQUID COOLING SYSTEMS

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 MIDAS IMMERSION COOLING

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.7 ECOCOOLING

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.8 DONGGUAN LIANLI ELECTRONIC TECHNOLOGY CO., LTD.

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.9 DRY COOLERS, INC.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.10 DOLPHIN RADIATORS & COOLING SYSTEMS LLC

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.11 ROSSEAU

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Deals

- 14.1.12 AXH AIR-COOLERS

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.12.3 Recent developments

- 14.1.13 CRYPTOTHERM MANUFACTURING INC.

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Solutions/Services offered

- 14.1.13.3 Recent developments

- 14.1.14 E3 NV, LLC.

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Solutions/Services offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Deals

- 14.1.15 TEIMMERS

- 14.1.15.1 Business overview

- 14.1.15.2 Products/Solutions/Services offered

- 14.1.15.3 Recent developments

- 14.1.16 BIXBIT

- 14.1.16.1 Business overview

- 14.1.16.2 Products/Solutions/Services offered

- 14.1.16.3 Recent developments

- 14.1.16.3.1 Deals

- 14.1.17 HAYDEN INDUSTRIAL

- 14.1.17.1 Business overview

- 14.1.17.2 Products/Solutions/Services offered

- 14.1.17.3 Recent developments

- 14.1.1 SUBMER

- 14.2 OTHER PLAYERS

- 14.2.1 BOXTECHY

- 14.2.1.1 Recent developments

- 14.2.1.1.1 Product launches

- 14.2.1.1 Recent developments

- 14.2.2 NXC

- 14.2.3 CHILLMINE

- 14.2.4 HARTZELL

- 14.2.5 FLUID COOLING SYSTEMS

- 14.2.1 BOXTECHY

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 List of participating companies for primary research

- 15.1.2.3 Key industry insights

- 15.1.2.4 Breakdown of primary interviews

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 DEMAND-SIDE APPROACH

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS