|

시장보고서

상품코드

2027003

철강 시장 예측(-2031년) : 유형(철, 강), 제철 기술, 제강 기술, 최종사용자 산업(건설 및 건축, 자동차 및 운송, 소비재, 중공업), 지역별Iron & Steel Market by Type (Iron and Steel), Iron Production Technology, Steel Production Technology, End-use Industry (Construction & Building, Automotive & Transportation, Consumer Goods, Heavy Industries), and Region - Global Forecast to 2031 |

||||||

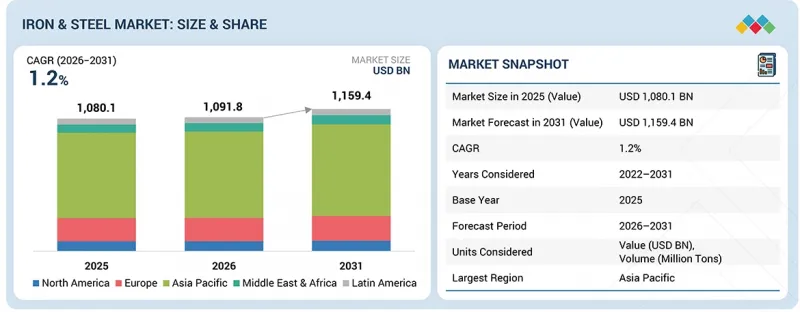

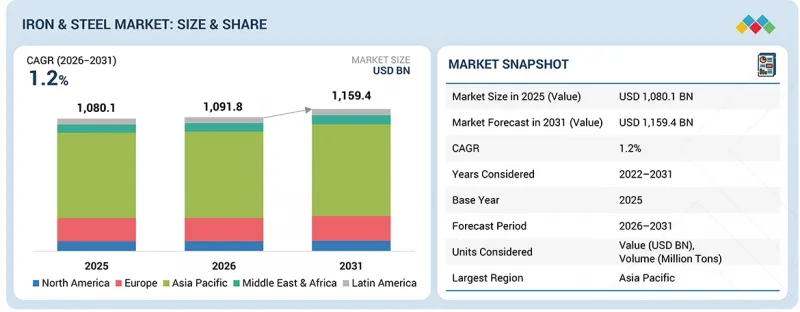

철강 시장 규모는 2026년 1조 918억 달러에서 2031년까지 1조 1,594억 달러로 성장하며, 예측 기간 중 CAGR은 1.2%에 달할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(달러)·톤 |

| 부문 | 유형, 제철 기술, 제강 기술, 최종사용자 산업, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

세계의 급속한 도시화, 인프라 개발, 산업 및 제조 활동의 확대로 철강에 대한 수요가 증가하고 있습니다.

"철강 부문은 예측 기간 중 가장 큰 부문이 될 것으로 예상됩니다. "

철강 부문은 건설, 인프라, 자동차, 운송, 에너지, 제조 등 다양한 분야의 활용에 힘입어 예측 기간 중 가장 큰 부문이 될 것으로 예상됩니다. 철강은 높은 강도, 내구성, 다용도성, 다양한 용도 요건을 충족시키기 위해 다양한 등급과 모양으로 가공할 수 있는 특성으로 인해 여전히 기초적인 소재로 남아 있습니다. 세계의 급속한 도시화와 대규모 인프라 개발 프로젝트로 인해 철강 소비량이 크게 증가하고 있습니다. 또한 산업화의 진전과 자동차 부문의 확대로 인해 고성능, 경량 철강 제품에 대한 수요가 더욱 증가하고 있습니다. 철강 생산의 기술 발전과 더불어 지속가능한 철강 및 재활용 철강의 채택 확대도 시장 성장을 지원하고 있습니다. 스마트 시티, 교통망, 재생에너지 인프라에 대한 투자 증가도 철강 부문의 우위를 더욱 공고히 하고 있습니다. 전반적으로 이러한 요인들로 인해 철강은 세계 철강 시장에서 가장 크고 가장 중요한 부문으로 자리매김하고 있습니다.

"고로법 부문은 예측 기간 중 두 번째로 큰 시장 규모가 될 것으로 예상됩니다. "

고로법은 대량의 쇳물을 효율적이고 안정적으로 생산할 수 있으므로 대규모 산업 수요에 적합하며, 여전히 지배적인 위치를 유지하고 있습니다. 이 공정은 잘 구축된 인프라, 성숙한 기술, 높은 운영 신뢰성을 바탕으로 세계 철 생산에서의 입지를 더욱 확고히 하고 있습니다. 또한 기존 제강 시스템과의 호환성 및 고품질 철광석 처리 능력은 주요 철강 생산 지역에서의 지속적인 활용을 지원하고 있습니다. 직접 환원법(DRI)과 같은 저탄소 대체 기술에 대한 관심이 높아지고 있음에도 불구하고 고로 제철 공정은 비용 효율성과 대규모 생산 능력으로 인해 여전히 선도적인 위치를 유지하고 있습니다. 건설, 자동차, 인프라 부문의 수요 증가는 세계 철강 시장에서 철강 생산 기술 부문에서의 우위를 더욱 공고히 하고 있습니다.

"기본산소로(BOF) 제강 기술 부문은 예측 기간 중 두 번째로 큰 규모를 차지할 것으로 예상됩니다. "

이 공정은 고로에서 나온 쇳물을 탄소 함량이 조절된 고품질의 철강으로 효율적으로 전환하는 세계 철강 생산의 근간이 되고 있습니다. BOF 기술은 대규모 연속 생산이 가능하므로 건설, 자동차, 인프라, 중장비 엔지니어링 분야의 활발한 산업 수요를 충족시키기에 매우 적합합니다. 잘 구축된 인프라, 운영의 신뢰성, 비용 효율성은 세계 철강 산업에서 그 우위를 더욱 확고히 하고 있습니다. 또한 BOF 공정은 기존 고로 운영과 광범위하게 통합되어 원활한 생산 흐름과 높은 생산 효율을 보장합니다. 전기 아크로(EAF)를 기반으로 한 지속가능한 방식으로의 전환이 진행되고 있음에도 불구하고 BOF는 우수한 생산 능력, 안정적인 품질, 그리고 전 세계 전통적 철강 제조 생태계에서 확고한 입지를 바탕으로 선도적인 위치를 유지하고 있습니다.

"금액 기준으로는 예측 기간 중 유럽이 두 번째로 큰 시장으로 성장할 것으로 예상됩니다. "

금액 기준으로 유럽은 탄탄한 산업 기반과 주요 최종사용자 부문의 안정적인 수요에 힘입어 예측 기간 중도 2위 지역으로 남을 것으로 예상됩니다. 이 지역에서는 건설, 자동차, 인프라 개조, 에너지 프로젝트에서 철강 소비가 여전히 높은 수준을 유지하고 있습니다. 노후화된 인프라의 개보수 및 현대적이고 에너지 효율적인 건물 확장을 위한 지속적인 투자도 수요 유지에 기여하고 있습니다. 동시에 유럽의 지속가능성에 대한 관심은 재활용 철강재와 청정 생산 방식을 확대하여 업계 전반의 구매 및 생산 의사결정에 영향을 미치고 있습니다. 엄격한 규제 기준과 확립된 제조 생태계도 시장 가치의 안정성을 더욱 지원하고 있습니다. 전반적으로 안정적인 산업 활동과 환경 친화적인 철강 솔루션으로의 전환이 결합되어 예측 기간 중 유럽은 제2의 지역 시장으로서의 입지를 확고히 할 것으로 보입니다.

세계의 철강 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 철강 시장 : 유형별

제10장 철 시장 : 제조 기술별

제11장 강철 시장 : 제조 기술별

제12장 철강 시장 : 최종사용자 산업별

제13장 철강 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.05.20The iron & steel market is projected to grow from USD 1,091.8 billion in 2026 to USD 1,159.4 billion by 2031, at a 1.2% CAGR over the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) Volume (Million Tons) |

| Segments | Type; Iron Production Technology; Steel Production Technology; End-use Industry; and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

Demand for iron & steel is rising due to rapid urbanization, infrastructure development, and expanding industrial and manufacturing activities worldwide.

"Steel segment projected to be the largest segment during the forecast period."

The steel segment is projected to be the largest during the forecast period, driven by its extensive use across the construction, infrastructure, automotive, transportation, energy, and manufacturing industries. Steel remains a fundamental material because of its high strength, durability, versatility, and ability to be engineered into various grades and forms to meet diverse application requirements. Rapid urbanization and large-scale infrastructure development projects worldwide are significantly increasing steel consumption. Additionally, growing industrialization and the expansion of the automotive sector are further strengthening demand for high-performance, lightweight steel products. Technological advancements in steel production, along with rising adoption of sustainable and recycled steel, are also supporting market growth. Increasing investments in smart cities, transportation networks, and renewable energy infrastructure are further reinforcing the dominance of the steel segment. Overall, these factors position steel as the largest and most critical segment in the global iron and steel market.

"Blast furnace process iron production technology segment projected to be the second-largest segment during the forecast period."

The blast furnace process iron production technology segment is projected to be the largest during the forecast period, driven by its widespread adoption in integrated steel manufacturing facilities worldwide. This conventional method remains dominant because it efficiently and consistently produces large volumes of hot metal, making it well suited to large-scale industrial demand. The process benefits from well-established infrastructure, mature technology, and high operational reliability, further strengthening its position in global iron production. Additionally, its compatibility with existing steelmaking systems and ability to process high-quality iron ore support its continued use across major steel-producing regions. Despite growing interest in low-carbon alternatives such as the Direct Reduced Iron process, the Blast Furnace Process continues to lead because of its cost efficiency and large-scale output capability. Increasing demand from the construction, automotive, and infrastructure sectors further reinforces its dominance in the iron production technology segment of the global iron and steel market.

"Basic oxygen furnace steel production technology segment projected to be the second-largest segment during the forecast period."

The basic oxygen furnace (BOF) steel production technology segment is projected to be the largest during the forecast period, owing to its widespread adoption in integrated steelmaking facilities across major steel-producing regions. This process remains a cornerstone of global steel production because it efficiently converts hot metal from blast furnaces into high-quality steel with controlled carbon content. BOF technology supports large-scale, continuous production, making it highly suitable for meeting strong industrial demand from the construction, automotive, infrastructure, and heavy engineering sectors. Its well-established infrastructure, operational reliability, and cost-effectiveness further strengthen its dominance in the global steel industry. Additionally, BOF processes are widely integrated with existing blast furnace operations, ensuring seamless production flow and high output efficiency. Despite the increasing shift toward electric arc furnace-based sustainable methods, BOF continues to lead because of its superior production capacity, consistent quality, and strong presence in traditional steel manufacturing ecosystems worldwide.

"Building & construction end-use industry segment projected to be the second-largest segment during the forecast period."

The building & construction segment is projected to be the largest during the forecast period, driven by rapid urbanization, infrastructure expansion, and rising investments in residential, commercial, and public infrastructure projects worldwide. This segment remains the dominant consumer of iron & steel because of the essential need for structural strength, durability, and load-bearing capacity in construction. Growing population levels and rising demand for modern housing, smart cities, and high-rise buildings are further accelerating steel consumption in this sector. Large-scale government initiatives focused on transportation networks, bridges, industrial corridors, and urban redevelopment are also significantly boosting demand. The versatility of steel across construction applications, along with its recyclability and cost-effectiveness, further strengthens its position. Advancements in construction technologies and the increasing use of high-performance steel grades are also supporting market growth. Overall, these factors ensure the continued dominance of the building & construction segment in the global iron and steel market.

"In terms of value, Europe is projected to be the second-largest segment during the forecast period."

In terms of value, Europe is expected to remain the second-largest region during the forecast period, supported by its strong industrial base and steady demand from key end-use sectors. The region continues to see significant iron & steel consumption across construction, automotive, infrastructure upgrades, and energy projects. Ongoing investments in renovating older infrastructure and expanding modern, energy-efficient buildings are also helping sustain demand. At the same time, Europe's focus on sustainability is driving greater use of recycled steel and cleaner production methods, shaping purchasing and production decisions across the industry. Strong regulatory standards and a well-established manufacturing ecosystem further support a consistent market value. Overall, stable industrial activity, combined with the shift toward greener steel solutions, keeps Europe firmly positioned as the second-largest regional market during the forecast period.

Companies Covered: ArcelorMittal (Luxembourg), China Baowu Steel Group (China), Tata Steel (India), Nucor Corporation (US), JSW (India), Nippon Steel Corporation (Japan), Ansteel Group Corporation Limited (China), POSCO (South Korea), HBIS Group Co., Ltd. (China), Steel Authority of India Ltd. (SAIL) (India), CSN (National Steel Company) (Brazil), and SSAB AB (Sweden), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the iron & steel market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The report's scope covers detailed information on the drivers, restraints, challenges, and opportunities influencing the growth of the iron & steel market. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products offered, and key strategies, such as partnerships, collaborations, product launches, expansions, and acquisitions, associated with the iron & steel market. This report also includes a competitive analysis of upcoming startups in the iron & steel market ecosystem.

Reasons to Buy the Report

The report will provide market leaders and new entrants with the closest approximations of revenue figures for the overall iron & steel market and its subsegments. It will help stakeholders understand the competitive landscape, gain deeper insights into positioning their businesses more effectively, and plan suitable go-to-market strategies. The report will also help stakeholders gauge the pulse of the market and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (abundance of iron ore and other minerals for steel production, expansion of urban infrastructure networks beyond core cities, rising steel consumption in the energy and power and automotive industries), restraints (carbon transition pressure and the cost of decarbonization technologies, volatility in raw material quality and supply security), opportunities (green steel premiumization and carbon-neutral supply contracts, expansion of scrap-based steel production), and challenges (navigating trade barriers and market access uncertainty, excess global steel overcapacity distorting pricing and profitability dynamics).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the iron & steel market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the iron & steel market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the iron & steel market.

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players such as ArcelorMittal (Luxembourg), China Baowu Steel Group (China), Tata Steel (India), Nucor Corporation (US), JSW (India), Nippon Steel Corporation (Japan), Ansteel Group Corporation Limited (China), POSCO (South Korea), HBIS Group Co., Ltd. (China), Steel Authority of India Ltd. (SAIL) (India), CSN (National Steel Company) (Brazil), and SSAB AB (Sweden).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.3.6 STAKEHOLDERS

- 1.4 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN IRON & STEEL MARKET

- 3.2 IRON & STEEL MARKET, BY TYPE AND END-USE INDUSTRY

- 3.3 IRON & STEEL MARKET, BY STEEL PRODUCTION TECHNOLOGY

- 3.4 IRON & STEEL MARKET, BY IRON PRODUCTION TECHNOLOGY

- 3.5 IRON & STEEL MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Abundance of iron ore & other minerals for steel production

- 4.2.1.2 Expansion of urban infrastructure networks beyond core cities

- 4.2.1.3 Rising steel consumption in energy & power and automotive industries

- 4.2.2 RESTRAINTS

- 4.2.2.1 Carbon transition pressure and cost of decarbonization technologies

- 4.2.2.2 Volatility in raw material quality and supply security

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Green steel premiumization and carbon-neutral supply contracts

- 4.2.3.2 Scrap-based steel production expansion (circular economy integration)

- 4.2.4 CHALLENGES

- 4.2.4.1 Navigating trade barriers and market access uncertainty

- 4.2.4.2 Excess global steel overcapacity distorting pricing and profitability dynamics

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN IRON & STEEL MARKET

- 4.3.1.1 Cost-competitive low-carbon steel production without margin erosion

- 4.3.1.2 Securing high-quality raw material supply for consistent steel performance

- 4.3.1.3 Scalable scrap collection and processing infrastructure in emerging markets

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 Ultra-low impurity scrap utilization for high-grade flat steel production

- 4.3.2.2 Limited availability of DR-grade iron ore for hydrogen-based steelmaking

- 4.3.2.3 Inability to achieve ultra-low emission steel below 0.5 tonnes CO2 per ton

- 4.3.1 UNMET NEEDS IN IRON & STEEL MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE AMONG KEY PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA RELATED TO HS CODE 78, BY COUNTRY, 2021-2025 (USD THOUSAND)

- 5.6.2 EXPORT DATA RELATED TO HS CODE 78, BY COUNTRY, 2021-2025 (USD THOUSAND)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ARCELORMITTAL: ADVANCED HIGH-STRENGTH STEEL FOR AUTOMOTIVE LIGHTWEIGHTING

- 5.10.2 POSCO: INNOVEX HIGH-GRADE ELECTRICAL STEEL FOR EV MOTORS

- 5.10.3 TATA STEEL: COLORCOAT PRISMA COATED STEEL FOR SUSTAINABLE CONSTRUCTION

- 5.11 IMPACT OF 2025 US TARIFFS ON IRON & STEEL MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 KEY IMPACT ON VARIOUS REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 BLAST FURNACE-BASIC OXYGEN FURNACE (BF-BOF) STEELMAKING

- 6.1.2 ELECTRIC ARC FURNACE (EAF) STEELMAKING

- 6.1.3 DIRECT REDUCED IRON (DRI) TECHNOLOGY

- 6.1.4 COMPLEMENTARY TECHNOLOGIES

- 6.1.4.1 Coke oven & sintering technology

- 6.1.4.2 Scrap processing & pre-treatment systems

- 6.1.5 ADJACENT TECHNOLOGIES

- 6.1.5.1 Hydrogen-based Steelmaking (H-DRI)

- 6.1.5.2 Carbon Capture, Utilization, and Storage (CCUS)

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM (2025-2027) | PROCESS EFFICIENCY & DECARBONIZATION READINESS PHASE

- 6.2.2 MID-TERM (2027-2030) | PROCESS INTEGRATION & LOW-CARBON TRANSITION PHASE

- 6.2.3 LONG-TERM (2030-2035+): GREEN STEEL & FULL DECARBONIZATION PHASE

- 6.3 PATENT ANALYSIS

- 6.3.1 INTRODUCTION

- 6.3.2 APPROACH

- 6.3.3 TOP APPLICANTS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 FULLY HYDROGEN-PLASMA IRONMAKING (PLASMA SMELTING REDUCTION)

- 6.4.2 MOLTEN OXIDE ELECTROLYSIS (MOE) STEEL PRODUCTION

- 6.4.3 SELF-HEALING STEEL MATERIALS

- 6.5 IMPACT OF AI/GENERATIVE AI ON IRON & STEEL MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN IRON & STEEL

- 6.5.3 CASE STUDIES OF AI IMPLEMENTATION IN IRON & STEEL MARKET

- 6.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN IRON & STEEL MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF IRON & STEEL

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF IRON & STEEL

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 IRON & STEEL MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 IRON

- 9.2.1 DECARBONIZATION AND FEEDSTOCK QUALITY FUNDAMENTALLY TRANSFORMING GLOBAL IRON VALUE CHAINS

- 9.3 STEEL

- 9.3.1 SHIFTING DEMAND MIX AND LOW-CARBON TECHNOLOGIES REDEFINING GLOBAL STEEL COMPETITIVENESS

- 9.3.1.1 Carbon steel

- 9.3.1.2 Stainless steel

- 9.3.1.3 Alloy steel

- 9.3.1.4 Tool steel

- 9.3.1.5 Types by steel forming

- 9.3.1.5.1 Hot-rolled coil

- 9.3.1.5.2 Hot-rolled plate

- 9.3.1.5.3 Cold-rolled coil

- 9.3.1.5.4 Hot-dipped galvanized coil

- 9.3.1.5.5 Electro zinc-coated coil

- 9.3.1.5.6 Wire rod

- 9.3.1.5.7 Sections & beams

- 9.3.1 SHIFTING DEMAND MIX AND LOW-CARBON TECHNOLOGIES REDEFINING GLOBAL STEEL COMPETITIVENESS

10 STEEL MARKET, BY PRODUCTION TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 BASIC OXYGEN FURNACE

- 10.2.1 CARBON-INTENSIVE LEGACY INFRASTRUCTURE AND SCALE EFFICIENCIES CONTINUE TO DEFINE BOF STEELMAKING

- 10.3 ELECTRIC ARC FURNACE

- 10.3.1 SCRAP AVAILABILITY AND ENERGY ECONOMICS DRIVING EAF STEELMAKING COMPETITIVENESS

- 10.4 OTHER PRODUCTION TECHNOLOGIES

11 IRON MARKET, BY PRODUCTION TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 BLAST FURNACE PROCESS

- 11.2.1 HIGH CARBON INTENSITY AND RAW MATERIAL DEPENDENCE CONTINUE TO DEFINE BLAST FURNACE IRONMAKING

- 11.3 DIRECT REDUCED IRON (DRI) PROCESS

- 11.3.1 GAS-BASED REDUCTION AND HYDROGEN TRANSITION RESHAPING DRI COMPETITIVENESS GLOBALLY

12 IRON & STEEL MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 BUILDING & CONSTRUCTION

- 12.2.1 INFRASTRUCTURE INVESTMENT MOMENTUM AND SUSTAINABILITY SHIFTS RESHAPING CONSTRUCTION STEEL DEMAND

- 12.3 AUTOMOTIVE & TRANSPORTATION

- 12.3.1 ELECTRIFICATION AND LIGHTWEIGHTING TRENDS TRANSFORMING STEEL DEMAND IN MOBILITY

- 12.4 CONSUMER GOODS

- 12.4.1 APPLIANCE DEMAND AND URBAN CONSUMPTION TRENDS DRIVING STEEL USE IN CONSUMER GOODS

- 12.5 HEAVY INDUSTRIES

- 12.5.1 INDUSTRIAL EXPANSION AND ENERGY TRANSITION DRIVING STEEL DEMAND IN HEAVY INDUSTRIES

- 12.6 OTHER END-USE INDUSTRIES

13 IRON & STEEL MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Robust construction, automotive output, and reshoring trends

- 13.2.2 CANADA

- 13.2.2.1 Housing expansion, industrial exports, and logistics growth

- 13.2.3 MEXICO

- 13.2.3.1 Infrastructure expansion and automotive growth

- 13.2.4 REST OF NORTH AMERICA

- 13.2.1 US

- 13.3 ASIA PACIFIC

- 13.3.1 CHINA

- 13.3.1.1 Industrial upgrading and infrastructure expansion

- 13.3.2 INDIA

- 13.3.2.1 Infrastructure expansion and industrial growth

- 13.3.3 JAPAN

- 13.3.3.1 Infrastructure modernization and energy transition

- 13.3.4 SOUTH KOREA

- 13.3.4.1 Industrial upgrading and export-led manufacturing

- 13.3.5 REST OF ASIA PACIFIC

- 13.3.1 CHINA

- 13.4 EUROPE

- 13.4.1 GERMANY

- 13.4.1.1 Industrial recovery, automotive expansion, and green steel transition

- 13.4.2 UK

- 13.4.2.1 Infrastructure recovery, construction pipeline, and aerospace growth

- 13.4.3 FRANCE

- 13.4.3.1 Infrastructure modernization, automotive expansion, and housing revival

- 13.4.4 RUSSIA

- 13.4.4.1 Industrial production, infrastructure expansion, and energy stability

- 13.4.5 SPAIN

- 13.4.5.1 Rapid construction surge and stable steel output

- 13.4.6 ITALY

- 13.4.6.1 Industrial manufacturing expansion and structural demand shifts

- 13.4.7 REST OF EUROPE

- 13.4.1 GERMANY

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Industrial diversification and mega infrastructure expansion

- 13.5.1.2 UAE

- 13.5.1.2.1 Mega infrastructure investment and industrial expansion

- 13.5.1.3 Rest of GCC countries

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Infrastructure investment and industrial manufacturing

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Mining strength and industrial expansion

- 13.6.2 ARGENTINA

- 13.6.2.1 Investment revival and mining-led export growth

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 BRAND COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Type footprint

- 14.6.5.4 Production technology footprint (Iron)

- 14.6.5.5 Production technology footprint (Steel)

- 14.6.5.6 End-use industry footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.7.5.1 List of key startups/SMEs

- 14.7.6 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.8.1 COMPANY VALUATION

- 14.9 FINANCIAL METRICS

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 DEALS

- 14.10.2 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 ARCELORMITTAL

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weakness and competitive threats

- 15.1.2 CHINA BAOWU STEEL GROUP CORPORATION LIMITED

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 TATA STEEL

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 JSW

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 NUCOR CORPORATION

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 NIPPON STEEL CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.6.3.3 Expansions

- 15.1.6.4 MnM view

- 15.1.7 ANSTEEL GROUP CORPORATION LIMITED

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.7.4 MnM view

- 15.1.8 POSCO

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.4 MnM view

- 15.1.9 HBIS GROUP CO., LTD.

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Deals

- 15.1.9.3.3 Expansions

- 15.1.9.4 MnM view

- 15.1.10 STEEL AUTHORITY OF INDIA LTD. (SAIL)

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Expansions

- 15.1.10.4 MnM view

- 15.1.11 CSN (NATIONAL STEEL COMPANY)

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.11.3.2 Expansions

- 15.1.11.4 MnM view

- 15.1.12 SSAB AB

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches

- 15.1.12.3.2 Deals

- 15.1.12.3.3 Expansions

- 15.1.12.4 MnM view

- 15.1.1 ARCELORMITTAL

- 15.2 OTHER PLAYERS

- 15.2.1 SHAGANG GROUP

- 15.2.2 NLMK

- 15.2.3 SEVERSTAL

- 15.2.4 EREGLI DEMIR VE CELIK FAB. T.A.S.

- 15.2.5 SOHAR STEEL

- 15.2.6 C.D. WALZHOLZ GMBH & CO. KG

- 15.2.7 HENAN ANHUILONG STEEL CO., LTD.

- 15.2.8 HEBEI DONGHAI SPECIAL STEEL GROUP

- 15.2.9 FENG HSIN STEEL CO. LTD.

- 15.2.10 WORTHINGTON STEEL, INC.

- 15.2.11 LIBERTY STEEL GROUP

- 15.2.12 GERDAU

- 15.2.13 CORROS METALS PVT. LTD.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.1.2 List of secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key primary participants

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Breakdown of interviews with experts

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 TOP-DOWN APPROACH

- 16.2.2 BOTTOM-UP APPROACH

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 SUPPLY-SIDE APPROACH

- 16.4 GROWTH FORECAST

- 16.5 DATA TRIANGULATION

- 16.6 RESEARCH ASSUMPTIONS

- 16.7 RESEARCH LIMITATIONS & RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS