|

시장보고서

상품코드

1440176

해상 화물 운송 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Sea Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

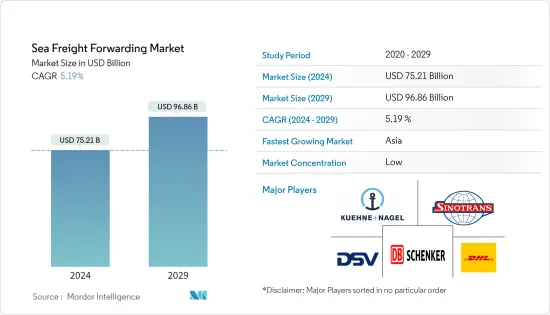

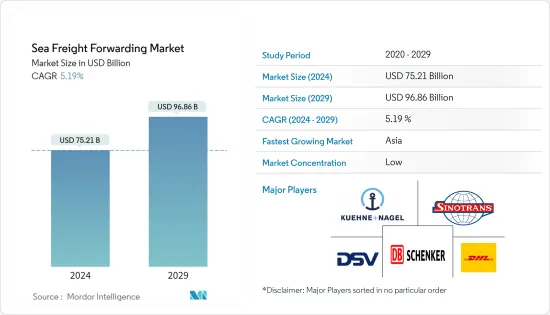

해상 화물 운송 시장 규모는 2024년 752억 1,000만 달러에 이를 것으로 추정됩니다. 2029년까지 968억 6,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 5.19%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

주요 하이라이트

- 인터넷 보급 확대, 구매력 평가 상승, 특히 전자상거래 산업을 위해 설계된 인프라 및 서비스 개발로 인해 세계 해상 화물 운송 시장은 호황을 누리고 있습니다. 신종 코로나 바이러스 감염증의 확산은 안전과 코로나19 확산 방지를 위해 해운업계 종사자들이 폐쇄되면서 해운업계에 악영향을 미쳤습니다.

- 해상 화물 운송은 여러 최종 사용자 산업에서 선호되는 모드로 부상하고 있으며, 일부 전략적 파트너십은 예측 기간 동안 해상 화물 운송의 성장을 가속할 수 있습니다. 성장하는 세계 국경 간 전자상거래 시장은 LCL의 양을 증가시켜 해상 화물 운송 시장의 성장에 긍정적인 영향을 미치고 있습니다.

- 해상 운송은 수천년동안 상품, 제품 및 사람을 운송하는 중요한 수단이었습니다. 오늘날 선박은 석탄, 석유 및 가스와 같은 중요한 상품을 운송하며 세계 경제를 지탱하고 있습니다. 2021년에만 약 150만 톤의 석탄과 110만 톤의 석유가 운송되었습니다.

- 더 중요한 것은 전체 물자의 약 85%가 주로 컨테이너선 등 해상운송을 통해 운송되고 있다는 점입니다. 다른 운송 수단에 비해 선박은 상대적으로 적은 배출량을 배출하지만 더 경제적이고 크고 무겁고 부피가 큰 품목을 운송하는 데 적합한 방대한 용량을 가지고 있습니다.

- 선주와 분석가들은 올해 남은 기간과 2023년까지 해운 운임이 더욱 하락할 것으로 예상하고 있습니다. 향후 2년 동안 많은 신조선이 취항할 예정이기 때문에 선대 규모의 순성장률은 2023년부터 2024년까지 9% 이상이 될 것으로 예상됩니다. 반면 브레머는 2024년 컨테이너 물동량 증가율은 소폭 마이너스를 기록할 것으로 예상했습니다.

해상 화물 운송 시장 동향

부상하는 크로스 브로커 이커머스 시장이 시장을 주도합니다.

2021년 전 세계 소매 전자상거래 매출은 약 5조 2,110억 달러에 달할 것으로 예상되며, 향후 몇 년동안 전자 소매 매출은 더 빠른 속도로 성장할 것으로 전망됩니다. 또한 온라인 쇼핑은 전 세계적으로 가장 인기 있는 온라인 활동 중 하나이기 때문에 국내 및 중국, 인도, 인도네시아와 같은 신흥 시장에서 국경 간 전자상거래를 촉진하고 있습니다. 여기에는 소비자 직접 판매뿐만 아니라 전자제품, 의약품, 소비자용 패키지 상품 배송도 포함됩니다.

신흥국들이 제조업 중심의 성장에서 중산층 확대로 인한 높은 소비 수준으로 점차 전환하는 가운데, 전자상거래의 성장은 이 지역의 소비 성장과 매우 밀접한 관련이 있습니다.

중국에서는 이미 국경 간 전자상거래가 전체 수출입 거래량의 최대 25%를 차지하고 있습니다. 중국과 비교하면 다른 지역의 전자상거래 관련 사업 규모는 훨씬 작지만 그 성장세도 빠르며, 전자상거래 화물 운송에서 가장 선호되는 수단 중 하나는 해상 운송이며, 2021년 해상 운송량이 200억 톤으로 증가할 것이라는 전망에서 알 수 있듯이 많은 기업들이 해상 운송을 선호하고 있습니다. 지지하고 있습니다.

해상무역 운송량 증가

해상 무역의 성장은 운송 비용 절감으로 전 세계 고객에게 이익을 가져다 줍니다. 운송 수단으로서의 해운 효율성이 향상되고 경제가 더욱 자유화됨에 따라 업계의 지속적인 성장 전망은 계속 긍정적입니다.

현재 상황에도 불구하고 업계의 장기적인 전망은 여전히 매우 긍정적입니다. 세계 인구는 여전히 증가하고 있으며, 개발도상국은 앞으로도 더 많은 상품과 원자재를 안전하고 효과적으로 운송할 수 있는 해운을 필요로할 것입니다. 최근 해상 국제 무역량이 다시 꾸준히 증가하기 시작했습니다. 해운이 가장 환경 친화적이고 비용 효율적인 상업 운송 수단이라는 사실은 결국 세계 무역에서 해상 운송이 차지하는 비율을 증가시킬 것입니다.

50,000척 이상의 상선이 해외에서 운항하며 모든 유형의 상품을 운송하고 있습니다. 거의 모든 국적의 선원 100만 명 이상이 전 세계 선단을 구성하고 있으며, 150여 개국에 등록되어 있습니다.

유엔무역개발회의(UNCTAD)에 따르면 상선 운항은 세계 경제에 약 3,800억 달러 상당의 운임을 창출하고 있으며, 이는 전체 무역의 약 5%에 해당합니다.

자유무역과 소비재 수요의 확대는 산업화의 발전과 국민경제의 자유화에 의해 촉진되었습니다. 기술의 발전은 운송 수단으로서의 운송의 효율성과 속도도 향상되었습니다.

1990년부터 2020년까지 해상 무역량은 2배 이상 증가하여 106억 5,000만 톤에 달했습니다. 2020년에는 18억 5,000만 톤의 국제 해상 무역이 컨테이너 선박으로 운송되었습니다. 2021년 1월 기준 파나마는 3억 4,360만 DWT의 선복량을 보유한 세계 최대 상선 선단을 보유하고 있습니다. 지난 30년동안 해상 무역 운송량은 약 3 배 증가하여 2021 년에는 1,500 억 톤에 도달하여 해상 화물 운송 업체의 업무량이 꾸준히 증가하고 있습니다.

해상 화물 운송 산업 개요

해상 화물 운송 시장은 경쟁이 치열하고 많은 기업이 존재하기 때문에 매우 세분화되어 있습니다. 해상 화물 운송 업체는 중개자 역할을하고 일반 해상 운송 업체를 통해화물을 발송하고 고객을 대신하여 모든 화물을 준비하는 개인 또는 회사입니다.

해상 화물 운송 업체는 필요한 모든 물류를 처리하고 배송과 관련된 활동을 수행합니다. 2012년부터 2022년까지 해상화물 물동량은 3배로 증가했으며, 최근 몇 년동안 많은 신규 시장 진출기업이 시장에 등장했습니다.

이 시장의 기존 주요 기업으로는 Kuehne Nagel, DHL Supply Chain &Global Forwarding, DB Schenker, DSV Panalpina, Sinotrans, Expeditors, Nippon Express, CEVA Logistics, CH. Robinson, Kerry Logistics 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 성과

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

- 분석 조사 방법

- 조사 단계

제3장 주요 요약

제4장 시장 인사이트

- 현재의 시장 시나리오

- 밸류체인/공급망 분석

- 기술 동향

- 투자 시나리오

- 정부 규제와 이니셔티브

- 스포트라이트 - 해상 운송 비용/운임

- E-Commerce 업계에 관한 통찰

- COVID-19에 의한 해상 화물 운송 시장에 대한 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 시장 기회

- 업계의 매력 - Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁도

제6장 시장 세분화

- 유형별

- FCL

- LCL

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 네덜란드

- 영국

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 호주

- 인도

- 싱가포르

- 말레이시아

- 인도네시아

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 남아프리카공화국

- 이집트

- GCC 국가

- 기타 중동 및 아프리카

- 남미

- 브라질

- 칠레

- 기타 남미

- 북미

제7장 경쟁 구도

- 시장 집중 개요

- 기업 개요

- Kuehne+Nagel

- Sinotrans

- DHL

- DB Schenker

- DSV Panalpina

- Expeditors

- CH Robinson

- Ceva Logistics

- Kerry Logistics

- Nippon Express

- Hellmann Worldwide Logistics

- Geodis

- Fr. Meyer's Sohn

- Yusen Logistics

- Bollore Logistics

제8장 시장의 미래

제9장 면책사항

LSH 24.03.14The Sea Freight Forwarding Market size is estimated at USD 75.21 billion in 2024, and is expected to reach USD 96.86 billion by 2029, growing at a CAGR of 5.19% during the forecast period (2024-2029).

Key Highlights

- The global sea freight forwarding market is booming, owing to the growing internet penetration, increasing Purchasing Power Parity, and developments in infrastructure and services designed particularly for the e-commerce industry. The epidemic negatively impacted the shipping industry as workforces in these sectors were shut down for safety and to prevent the spread of COVID-19.

- Sea freight forwarding has emerged as a preferred mode among several end-user industries and several strategic partnerships are also likely to promote the growth of sea freight forwarding during the forecast period. The growing global cross-border e-commerce market is driving the LCL volume and is positively impacting the sea freight forwarding market growth.

- Sea freight has been an important means of transporting goods, products, and people for thousands of years. Today, ships transport vital commodities such as coal, oil and gas, supporting the global economy. In 2021 alone, about 1.5 million tonnes of coal and about 1.10 million tonnes of oil were shipped.

- More importantly, about 85% of all goods are transported by sea, mainly by container ships. Compared to other means of transport, vessels have vast capacities suitable for transporting large, heavy, and bulky items that are more economical while producing relatively small amounts of emissions.

- Shipping rates are expected to drop further for the rest of the year and into 2023, according to shipowners and analysts. With a number of new vessels entering service over the next two years, net growth in the fleet size is expected to be over 9% through 2023 to 2024. By contrast, container volume growth in 2024 could be slightly negative according to Braemer.

Sea Freight Forwarding Market Trends

Rising Cross Broder E-Commerce is driving the Market

In 2021, retail e-commerce sales worldwide amounted to around USD 5,211 Billion and e-retail revenues are projected to grow even further at a quicker pace in the coming few years. Further, as online shopping is one of the most popular online activities worldwide is driving both the domestic and cross-border e-commerce in developing markets such as China, India, and Indonesia. This encompasses not just direct-to-consumer retail, but also shipments of electronics, pharmaceuticals, and consumer packaged goods.

Growth in e-commerce is tied very closely to the consumption growth in the region as developing economies make the gradual shift from growth by manufacturing for export to higher levels of consumption by expanding middle classes.

In China, cross-border e-commerce transactions already accounted for up to 25 percent of total import and export trading volumes. Compared to China, in other regions, the size of e-commerce related businessess is much smaller, but the growth is also rapid. One of the most preferred modese for e-commerce freight forwarding is through sea and many business are favoring that as evidenced by the growing of ocean freight volumes to 20 billion tons in 2021.

Rise In Seaborne Trade Transport Volume

The growth of seaborne trade benefits customers all around the world by lowering the cost of shipping. The prospects for the industry's continued growth remain favorable due to the increasing efficiency of shipping as a mode of transportation and further economic liberalization.

Despite the current circumstances, the industry's long-term prospects are still highly favorable. The world's population is still growing, and developing nations will keep needing more of the goods and raw materials that shipping transfers so securely and effectively. The volume of international trade conducted by sea has recently started to rise steadily once more. The fact that shipping is the most environmentally benign and cost-effective method of commercial transportation should eventually lead to an increase in the percentage of world trade that is transported by sea.

Over 50,000 merchant ships operate abroad and carry all different kinds of goods. More than a million seafarers of essentially every nationality make up the world fleet, which is registered in more than 150 countries.

According to the United Nations Conference on Trade and Development (UNCTAD), the operation of commercial ships generates freight rates worth roughly USD 380 billion for the global economy or about 5% of all trade.

The expansion of free trade and the demand for consumer goods has been fueled by rising industrialization and the liberalization of national economies. Technology advancements have also increased the effectiveness and speed of the shipping as a mode of transportation.

Between 1990 and 2020, seaborne trade volumes more than doubled to reach 10.65 billion tons. In 2020, 1.85 billion tons of international seaborne trade was carried by container ships. As of January 2021, Panama had the world's largest merchant fleet with 343.6 million DWT operator seats. The business volume of ocean freight forwarders has been steadily increasing because in the last three decades, the seaborne trade transport volume roughly tripled, reaching 150 billion metric tons in 2021.

Sea Freight Forwarding Industry Overview

The Sea Freight Forwarding Market is highly competitive and is highly fragmented with the presence of many players. A Sea Freight forwarder is an individual or company that acts as an intermediary and dispatches the shipments via common sea carriers and makes all arrangements for those shipments on behalf of its clients.

Sea Freight forwarders handle all the logistics needed and perform activities pertaining to shipments. With the Ocean freight volumes tripling from 2012 to 2022, the market has seen many new players entering in the last few years.

Some of the existing major players in the market include Kuehne + Nagel, DHL Supply Chain & Global Forwarding, DB Schenker, DSV Panalpina, Sinotrans, Expeditors, Nippon Express, CEVA Logistics, C.H. Robinson, and Kerry Logistics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Technological Trends

- 4.4 Investment Scenarios

- 4.5 Government Regulations and Initiatives

- 4.6 Spotlight - Sea Freight Transportation Costs/Freight Rates

- 4.7 Insights on the E-commerce Industry

- 4.8 Impact of COVID-19 on the Sea Freight Forwarding Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.2 Market Restraints

- 5.3 Market Opportunities

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Full Container Load (FCL)

- 6.1.2 Less-than Container Load (LCL)

- 6.1.3 Others

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.1.3 Mexico

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 France

- 6.2.2.3 Netherlands

- 6.2.2.4 United Kingdom

- 6.2.2.5 Italy

- 6.2.2.6 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 Australia

- 6.2.3.4 India

- 6.2.3.5 Singapore

- 6.2.3.6 Malaysia

- 6.2.3.7 Indonesia

- 6.2.3.8 South Korea

- 6.2.3.9 Rest of Asia-Pacific

- 6.2.4 Middle East & Africa

- 6.2.4.1 South Africa

- 6.2.4.2 Egypt

- 6.2.4.3 GCC Countries

- 6.2.4.4 Rest of Middle East & Africa

- 6.2.5 South America

- 6.2.5.1 Brazil

- 6.2.5.2 Chile

- 6.2.5.3 Rest of South America

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Kuehne + Nagel

- 7.2.2 Sinotrans

- 7.2.3 DHL

- 7.2.4 DB Schenker

- 7.2.5 DSV Panalpina

- 7.2.6 Expeditors

- 7.2.7 C.H Robinson

- 7.2.8 Ceva Logistics

- 7.2.9 Kerry Logistics

- 7.2.10 Nippon Express

- 7.2.11 Hellmann Worldwide Logistics

- 7.2.12 Geodis

- 7.2.13 Fr. Meyer's Sohn

- 7.2.14 Yusen Logistics

- 7.2.15 Bollore Logistics