|

시장보고서

상품코드

1851504

맥주 포장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Beer Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

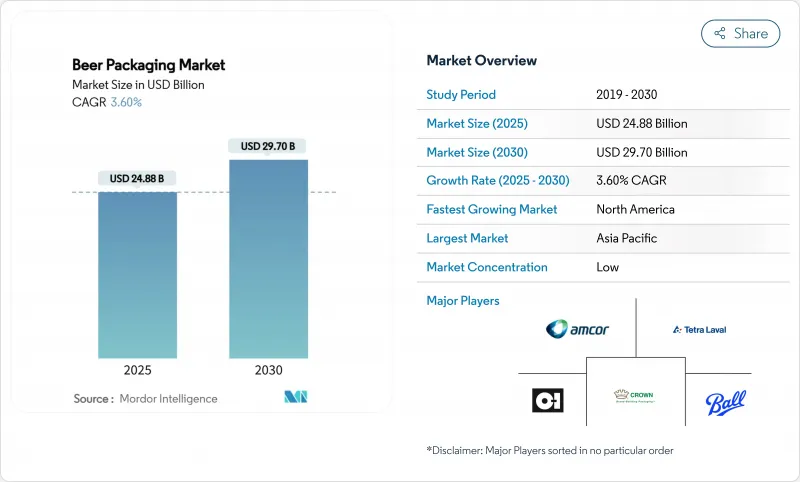

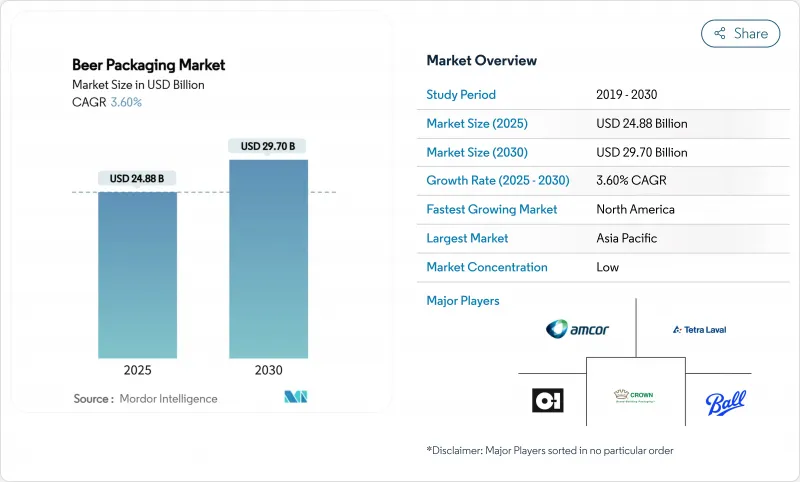

맥주 포장 시장 규모는 2025년에 248억 8,000만 달러, 2030년에는 297억 달러에 이를 것으로 예상되며, 예측 기간 중 CAGR은 3.60%를 나타낼 전망입니다.

이 성장은 지속 가능한 소재에 대한 수요 증가, 프리미엄 형식의 가속화, 소비 채널의 지속적인 변화를 반영합니다. 알루미늄의 점유율은 리사이클성과 물류의 효율성이 대기업·중소의 맥주 제조업체를 불문하고 매료하고 있는 것으로 확대를 계속하고 있어 PET는 콜드체인의 품질 보증이 개선되고 있는 점에서 지지를 모으고 있습니다. 유리는 수량에서 분명히 주도하고 있지만, 에너지 집약적인 생산과 무거운 화물 운송으로 인한 비용 압력에 직면하고 있습니다. 지역 비즈니스 기회는 도시화가 포장 맥주 매출을 높이는 아시아태평양과 크래프트 맥주 제조업체가 소매점 선반 동태와 일치하는 차별화된 환경 친화적인 형식을 요구하는 북미에 집중하고 있습니다. 주요 캔 제조 업체, 유리 제조 업체 및 유연한 팩 전문가공급 측면 투자는 재료 투입을 줄이고 브랜드 민첩성을 높이고 빠르고 폐기물이 적은 기술에 대한 업계의 축족을 보여줍니다.

세계의 맥주 포장 시장 동향과 인사이트

크래프트 맥주 양조장의 급증이 북미의 단납기 캔 디자인을 견인

Ball사의 Dynamark Advanced Pro와 같은 디지털 인쇄는 단일 팔레트에 여러 그래픽을 인쇄할 수 있기 때문에 기존의 최소 주문 수의 벽이 사라지고 크래프트 맥주 양조장의 성장이 포장의 경제성을 재구성하고 있습니다. 유연한 캔 라인은 양조업자가 과도한 유리병을 구입하지 않고 재고를 관리하고 새로운 SKU를 시험적으로 제조하며 계절별로 출시하는 데 도움이 됩니다. 디지털 인쇄 프리미엄은 오프셋 인쇄보다 300% 가까이 높지만, 지역 전체에서 9,000개가 넘는 맥주 양조장에서 보다 빠른 셀룰루율과 보다 강력한 선반 어필이 비용을 상쇄합니다.

EU의 예금 및 리턴 시스템에 의해 지원되는 경량 리터너블 유리 병 채택 증가

독일에서는 보증금 제도가 의무화되어 반송률이 98%에 달하고, Vetropack사의 Echovai 강화병과 같은 혁신을 촉진하고 있습니다. 프랑스에서는 연간 6,000만개의 병을 씻을 수 있는 집중 세척 허브를 추가하여 비용 구조를 일방적인 폐기에서 순환형 자산 관리로 이동시키고 있습니다.

유럽에서 PET를 줄이는 일회용 플라스틱 금지법

EU의 포장·용기 포장 폐기물 규제는 2030년까지 재활용률 30%를 강제하고 2025년부터 대상 포맷을 단계적으로 폐지합니다. 확대 생산자 책임 요금은 무한히 재활용 가능한 알루미늄에 비해 PET 비용을 늘리고 금속 및 경량 리터너블 유리로 포트폴리오를 이동하도록 촉구합니다.

부문 분석

유리는 감각적 중립성과 소비자의 정착한 연상으로 2024년에는 80.98%의 점유율을 유지했습니다. 그러나 2030년까지 100% 재활용 가능한 포장을 목표로 하는 정책 목표에 힘입어 알루미늄 재활용성의 우위성과 수송의 절약으로 수량이 감소합니다. PET는 CAGR 5.81%의 성장을 보였으며 이제 맥주 탄산 요구를 충족시키는 장벽 코팅 병에 끌려가지만 종이는 여전히 2차 팩으로 제한됩니다.

에너지 비용의 상승과 탄소세의 부과에 의해 알루미늄의 총 비용에서 우위성은 노 모래 유리보다도 확대됩니다. 한편, 사용후 식용유를 원료로 하는 바이오파라크실렌 PET와 같은 기술 혁신은 브랜드의 신뢰성을 향상시켜 폴리머의 폭넓은 채용을 예감시킵니다. 맥주 제조업체는 고급 제품을 위한 틈새 유리 SKU를 유지하고 있지만, 맥주 포장 시장에서는 새로운 생산 능력을 보다 가벼운 기재로 향하는 경향이 강해지고 있습니다.

2024년 세계 판매량의 75.32%는 병이 차지했습니다. 그래도 캔은 크래프트 맥주, 편의점 쇼핑, 옥외 소비에 있어서 다이나미즘이 포맷을 금속으로 기울이기 때문에 CAGR 6.75%로 가속하고 있습니다. 타루는 신흥 지역에서 세정 시스템의 설비 투자에 의해 성장이 둔화되고, 파우치도 약간의 성장에 그칩니다.

디지털 인쇄를 통해 소규모 맥주 제조업체는 다국적 기업의 포장 품질과 어깨를 정렬할 수 있어 낭비적인 오버런 없이 SKU의 회전 속도를 높일 수 있습니다. 브라질에서 볼 수 있는 지역 캔 라인에 대한 투자는 단위당 비용을 줄이고 공급력을 높이는 경제성을 더욱 확대합니다. 유리 제조업체는 엠보싱 가공이나 테이퍼 가공을 실시한 프로파일로 대항해, 매장에서 인지 가치를 높이고 있습니다.

지역 분석

2024년 점유율은 38.43%로 아시아태평양이 선도하고 인구 규모, 소득 상승, 급속한 도시화에 힘입어 포장된 업태를 선호했습니다. 베트남과 인도네시아에서는 콜드체인의 확대가 PET의 침투를 지원하고, 중국에서는 공예품 분야가 2024년에 331억 위안까지 성장하여 부티크 디자인의 캔이나 선물 지향의 유리병이 성장했습니다.

2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 것은 북미에서 6.43%를 나타낼 전망입니다. 9,000개가 넘는 크래프트 맥주 양조장이 소량 캔의 안정적인 수요를 창출하고 있지만, 관세와 슬래브 부족이 비용을 밀어 올리고 있습니다. 볼의 플로리다 인수와 같은 투자는 공급망을 간소화하고 지속 가능한 생산 능력을 추가하고이 지역의 성장 엔진으로서 알루미늄의 역할을 강화합니다.

유럽은 여전히 프리미엄의 아성이지만, 1인당 맥주 섭취량의 평평함에 직면하고 있습니다. EU의 재활용 의무화는 강화유리, 리터너블유리, 고재활용 컨텐트 캔으로의 자본이동의 방아쇠가 됩니다. 독일의 맥주 회사는 서큘러 이코노미의 KPI를 충족하면서 산업적인 속도를 달성하는 엠보싱 라인을 도입하여 프리미엄 포장을 선보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 크래프트 맥주 양조장의 급증이 북미의 단납기 캔 디자인을 견인

- EU의 예금·리턴 제도에 지지된 경량 리터너블 유리병의 채용 증가

- 콜드체인의 급속한 확대가 아시아 맥주에 PET 침투 가능

- 브랜드 프리미엄화가 독일 맥주 회사의 엠보싱 가공 특수 병을 뒷받침

- 알루미늄 관세 인하가 남미에서 캔 전환을 유발

- E-Commerce 멀티팩이 영국의 골판지 2차 포장 수요를 가속

- 시장 성장 억제요인

- 유럽에서 PET를 억제하는 일회용 플라스틱 금지법

- 미국의 알루미늄 슬래브 공급의 핍박이 크래프트 맥주 제조업체의 캔 비용을 상승

- 소비자의 경질 탄산음료로의 변화가 호주 유리 판매량을 감소

- 신흥 시장에서 리터너빌리티를 제한하는 통의 개수에 걸리는 높은 캡엑스

- 공급망 분석

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 포장 재료별

- 유리

- 금속

- PET

- 종이

- 포장 유형별

- 병

- 캔

- 케그

- 파우치

- 팩 사이즈별

- 330ml 미만

- 331-650ml

- 650ml 이상

- 유통 채널별

- 직접 판매

- 간접 판매

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주, 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor Ltd.

- Ardagh Group SA

- Crown Holdings Inc.

- Ball Corporation

- Tetra Laval International SA

- OI Glass Inc.

- Canpack Group

- Silgan Holdings Inc.

- Vidrala SA

- Allied Glass Containers Ltd.

- Plastipak Holdings Inc.

- Nampak Ltd.

- Orora Limited

- Graphic Packaging International

- Toyo Seikan Group Holdings Ltd.

- Envases Universales

- Berlin Packaging LLC

- Sidel(Sidel Group)

- Krones AG

제7장 시장 기회와 향후 전망

KTH 25.11.13The Beer packaging market size stands at USD 24.88 billion in 2025 and is expected to reach USD 29.70 billion in 2030, advancing at a 3.60% CAGR over the forecast period.

This growth reflects rising demand for sustainable materials, the acceleration of premium formats, and ongoing shifts in consumption channels. Aluminum's share continues to expand as recyclability and logistics efficiency attract large and small brewers alike, while PET gains traction where cold-chain quality assurance is improving. Glass holds a clear lead in volume but now contends with cost pressures from energy-intensive production and heavier freight loads. Regional opportunities cluster in Asia-Pacific, where urbanization lifts packaged beer sales, and in North America, where craft breweries seek differentiated, eco-friendly formats that match retail shelf dynamics. Supply-side investments by leading can makers, glass producers, and flexible-pack specialists underline an industry pivot toward high-speed, low-waste technologies that cut material inputs and boost brand agility.

Global Beer Packaging Market Trends and Insights

Surge in Craft Breweries Driving Short-Run Can Designs in North America

Craft brewery growth reshapes packaging economics as digital printing such as Ball's Dynamark Advanced Pro lets multiple graphics run on one pallet, eliminating historic minimum-order barriers. Flexible can lines help brewers manage inventory, pilot new SKUs, and execute seasonal launches without excess glass bottle purchases. Though digital print premiums approach 300% over offset, the cost is offset by faster sell-through rates and stronger shelf appeal at more than 9,000 breweries across the region.

Rising Adoption of Lightweight Returnable Glass Bottles Backed by EU Deposit-Return Schemes

Mandated deposit systems achieve 98% return rates in Germany, prompting innovations like Vetropack's Echovai tempered bottle that is 30% lighter yet rugged across multiple cycles. France's rollout adds centralized washing hubs capable of 60 million bottles per year, shifting cost structures from one-way disposal toward circular asset management.

Legislative Bans on Single-Use Plastics Curtailing PET in Europe

The EU Packaging and Packaging Waste Regulation enforces 30% recycled content by 2030 and phases out targeted formats from 2025. Extended Producer Responsibility fees raise PET costs relative to infinitely recyclable aluminum, prompting portfolio shifts toward metal and lightweight returnable glass.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Cold-Chain Expansion Enabling PET Penetration in Asian Beer

- Brand Premiumization Fueling Embossed Specialty Bottles Among German Breweries

- Tight U.S. Aluminum Slab Supply Elevating Can Costs for Craft Brewers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glass preserved an 80.98% share in 2024 due to sensory neutrality and entrenched consumer associations. Yet aluminum's recyclability edge and transportation savings peel away volume, aided by policy targets for 100% recyclable packaging by 2030. PET, advancing at 5.81% CAGR, draws on barrier-coated bottles that now satisfy beer's carbonation needs, while paper remains confined to secondary packs.

Rising energy costs and carbon levies widen aluminum's total-cost edge over furnace-fired glass. Meanwhile, innovations like bio-paraxylene PET from used cooking oil improve brand credentials and foreshadow broader polymer adoption. Brewers keep niche glass SKUs for premium variants, but the Beer packaging market increasingly redirects new capacity toward lighter substrates.

Bottles supplied 75.32% of global volume in 2024. Still, cans are accelerating at a 6.75% CAGR as dynamism in craft beer, convenience shopping, and outdoor consumption tips formats in favor of metal. Keg growth remains muted by cleaning-system cap-ex in emerging regions, and pouches stay marginal.

Digital printing lets small brewers match multinational packaging quality, increasing SKU churn without wasteful overruns. Investment in regional can lines, as seen in Brazil, further scales economies that shrink per-unit costs and enhance availability. Glass manufacturers counter with embossing and tapered profiles that lift perceived value on-premise.

The Beer Packaging Market Report is Segmented by Packaging Material (Glass, Metal, PET, Paper), Packaging Type (Bottle, Can, Keg, Pouches), Pack Size (Less Than Equal To 330 Ml, 331-650 Ml, More Than 650 Ml), Distribution Channel (Direct Sales, Indirect Sales), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 38.43% share in 2024, underpinned by population scale, climbing incomes, and rapid urbanization that favor packaged formats. Cold-chain expansion in Vietnam and Indonesia supports PET penetration, while China's craft segment grew to CNY 33.1 billion in 2024, fostering boutique can designs and gift-oriented glass bottles alike.

North America posts the fastest 6.43% CAGR through 2030. More than 9,000 craft breweries generate steady demand for short-run cans, though tariff and slab shortages inflate costs. Investments such as Ball's Florida acquisition streamline supply networks and add sustainable capacity, reinforcing aluminum's role as the region's growth engine.

Europe remains a premium stronghold but confronts flat per-capita beer intake. The EU's recyclability mandate triggers capital shifts into tempered, returnable glass and high-recycled-content cans. German breweries showcase premium packaging by installing embossed lines that hit industrial speeds while meeting circular-economy KPIs.

- Amcor Ltd.

- Ardagh Group SA

- Crown Holdings Inc.

- Ball Corporation

- Tetra Laval International SA

- O-I Glass Inc.

- Canpack Group

- Silgan Holdings Inc.

- Vidrala SA

- Allied Glass Containers Ltd.

- Plastipak Holdings Inc.

- Nampak Ltd.

- Orora Limited

- Graphic Packaging International

- Toyo Seikan Group Holdings Ltd.

- Envases Universales

- Berlin Packaging LLC

- Sidel (Sidel Group)

- Krones AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Craft Breweries Driving Short-Run Can Designs in North America

- 4.2.2 Rising Adoption of Lightweight Returnable Glass Bottles Backed by EU Deposit-Return Schemes

- 4.2.3 Rapid Cold-Chain Expansion Enabling PET Penetration in Asian Beer

- 4.2.4 Brand Premiumization Fueling Embossed Specialty Bottles Among German Breweries

- 4.2.5 Aluminum Tariff Cuts Triggering Can Conversions in South America

- 4.2.6 E-commerce Multipacks Accelerating Corrugated Secondary Packaging Demand in the UK

- 4.3 Market Restraints

- 4.3.1 Legislative Bans on Single-Use Plastics Curtailing PET in Europe

- 4.3.2 Tight U.S. Aluminum Slab Supply Elevating Can Costs for Craft Brewers

- 4.3.3 Consumer Shift to Hard Seltzers Reducing Glass Volumes in Australia

- 4.3.4 High Cap-Ex for Keg Refurbishment Limiting Returnability in Emerging Markets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Material

- 5.1.1 Glass

- 5.1.2 Metal

- 5.1.3 PET

- 5.1.4 Paper

- 5.2 By Packaging Type

- 5.2.1 Bottle

- 5.2.2 Can

- 5.2.3 Keg

- 5.2.4 Pouches

- 5.3 By Pack Size

- 5.3.1 Less than 330 ml

- 5.3.2 331-650 ml

- 5.3.3 More than 650 ml

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Indirect Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor Ltd.

- 6.4.2 Ardagh Group SA

- 6.4.3 Crown Holdings Inc.

- 6.4.4 Ball Corporation

- 6.4.5 Tetra Laval International SA

- 6.4.6 O-I Glass Inc.

- 6.4.7 Canpack Group

- 6.4.8 Silgan Holdings Inc.

- 6.4.9 Vidrala SA

- 6.4.10 Allied Glass Containers Ltd.

- 6.4.11 Plastipak Holdings Inc.

- 6.4.12 Nampak Ltd.

- 6.4.13 Orora Limited

- 6.4.14 Graphic Packaging International

- 6.4.15 Toyo Seikan Group Holdings Ltd.

- 6.4.16 Envases Universales

- 6.4.17 Berlin Packaging LLC

- 6.4.18 Sidel (Sidel Group)

- 6.4.19 Krones AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment