|

시장보고서

상품코드

1630442

남미의 벙커 연료 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)South America Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

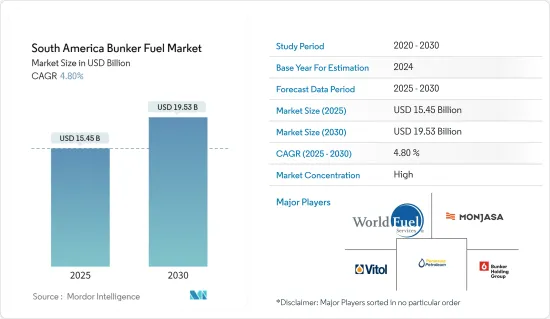

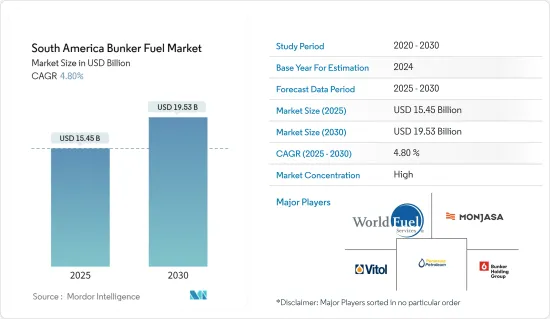

남미의 벙커 연료 시장 규모는 2025년 154억 5,000만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 4.8%를 나타낼 전망이며, 2030년에는 195억 3,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 중기적으로는 중요한 물자의 해상 수송 증가와 보다 깨끗한 벙커 연료 수요를 촉진하는 엄격한 환경 규제의 실시 등의 요인이 남미의 벙커 연료 시장의 성장을 견인합니다.

- 반면 석유시장의 변동은 벙커 연료 공급업체의 수익성에 영향을 미치고 계획과 투자를 어렵게 만들 수 있으므로 벙커 연료 시장에 큰 영향을 미칠 것으로 예상됩니다.

- 그럼에도 불구하고 깨끗한 벙커 연료 사용 증가는 남미 벙커 연료 시장에 큰 기회를 만들어냅니다.

- 브라질은 원유 생산량의 대폭적인 증가와 이 나라의 수출의 꾸준한 증가와 같은 요인으로 인해 이 지역의 벙커 연료 시장을 독점할 것으로 예상됩니다.

남미 벙커 연료 시장 동향

초저유황 연료유(VLSFO)가 크게 성장

- 국제해양기구(IMO)에 의한 선박으로부터의 유황 배출량 감축의 의무를 받고, 남아프리카의 벙커 연료 시장에서의 얕은 유황 연료유(VLSFO) 수요는 최근 대폭 증가하고 있습니다.

- 2023년 4월 현재 남아프리카의 벙커 연료 시장에서 사용되는 대부분의 VLSFO가 수입품이기 때문에 국내 벙커 연료 시장에서는 VLSFO의 입수가 특히 치박하고 있습니다. 저유황 연료유는 더반 항구, 포트 엘리자베스 항구, 케이프 타운 항구 및 아르고아 베이(포트 엘리자베스 해안 응쿠라 해안)의 해상 벙커링에서 구할 수 있습니다.

- 2022년 12월부터 2023년 4월까지의 가격 변동은 5% 정도입니다. 이와는 대조적으로 VLSFO의 가격은 크게 변동하고 있으며 이로 인해 이 연료에 대한 수요가 더욱 높아지고 있습니다.

- 2022년 10월, 선박 연료 업계 전문 상품 무역 회사인 FUEL & MARINE OIL CORP(FAMOIL)는 페루의 운영에 벙커 배송 선박을 추가했습니다. 이 회사는 탱커 Ecomar II를 선대에 추가했습니다. 이 배는 타라라, 파이타, 바요발, 샐러베리, 잠보테 항구 피스코, 산니콜라스, 마타라니, 로에서 초저유황 연료유(VLSFO)와 고황 연료유를 공급합니다.

- 또한 남미 시장에서 VLSFO 수요는 이 지역에서 운영하는 선박 수가 증가함에 따라 견인되고 있습니다. 이러한 연료가 해양생물에 미치는 환경에 미치는 영향에 대한 규제가 엄격해지고 있는 것도 결과적으로 VLSFO 수요를 밀어 올리고 있습니다.

- 전반적으로 IMO의 유황 상한 실시 후 수요 증가와 같은 요인으로 인해 예측 기간 동안 시장이 크게 성장할 것으로 예상됩니다.

시장을 독점하는 브라질

- 브라질은 이 지역에서 가장 큰 경제 강국이며 예측 기간 동안 가장 빠르게 성장하는 시장이 될 전망입니다. 이 나라는 인구 증가, 산업화, 도시화로 세계에서 가장 빠르게 성장하는 국가 중 하나입니다.

- 브라질의 석유 수출 증가는 남미 벙커 연료 시장을 견인하는 매우 중요한 역할을 할 것으로 예상됩니다. 브라질은 주요 산유국으로 석유 생산량을 확대하고 있으며, 수출 증가는 이 지역의 벙커 연료 시장에 큰 기회를 가져왔습니다.

- 국제항로가 남미 해역을 통과하기 때문에 선박이 사용하는 벙커 연료 수요는 급증할 것으로 예상됩니다. 브라질은 유력한 석유 수출국으로서 전략적으로 중요한 위치에 있기 때문에 남미에서 벙커 연료의 가용성과 가격 동향에 영향을 미치는 중요한 선수가 되고 있습니다.

- 예를 들어, 2022년 11월 노르웨이의 Kanfer Shipping AS는 Nimofast Brasil SA와 파트너십 계약을 체결하고 2025년 이후 브라질에서 중소규모 LNG선과 LNG 벙커링 솔루션을 확립합니다. LNG선과 LNG 벙커선은 파라나주에 있는 니모퍼스트 LNG 수입·배급터미널에 상설되는 FSU를 경유하여 선적됩니다.

- 게다가 브라질로부터의 석유 수출 증가는 이 지역에서 해상무역활동의 활성화라는 폭넓은 동향과 일치하고 있습니다. 선박의 왕래가 심해짐에 따라 선박의 주요 에너지원인 벙커 연료 수요도 상당히 증가할 것으로 예상됩니다.

- 이 벙커 연료 수요의 급증은 세계 무역에서 남미의 중요성 증가를 반영할 뿐만 아니라 브라질과 같은 석유 수출국이 선박 연료와 같은 관련 부문의 동향에 큰 영향을 미칠 가능성 있다는 에너지 시장의 상호 연관성을 부각하고 있습니다.

- 브라질은 회수 가능한 초심부 석유 매장량이 세계 최대이며, 브라질의 석유 생산량의 96.7%가 해양에서 생산되고 있습니다. 2022년 석유 생산량은 1억 6,310만 톤으로 2021년 1억 5,690만 톤에서 증가했습니다.

- 따라서 석유 및 가스 생산량 증가가 예상되는 가운데 브라질과 기타 지역 간의 무역활동은 더욱 증가할 것으로 예상됩니다. 주요 국제 거래는 해상 노선을 통해 이루어지기 때문에 브라질은 가까운 미래에 벙커 연료의 신흥 시장이 될 것으로 예상됩니다.

- 위의 모든 요인은 예측 기간 동안 이 나라가 벙커 연료 측면에서 이 지역을 지배하는 데 도움이 될 것으로 예상됩니다.

남미 벙커 연료 산업 개요

남미의 벙커 연료 시장은 절반으로 축소되었습니다. 주요 기업에는 Bunker Holding A/S, Monjasa Holding A/S, AP Moeller Maersk A/S, World Fuel Services Corp, Peninsula Petroleum Ltd. 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모 및 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 남미에서 증가하고 있는 필수 원자재의 해상 운송

- 보다 깨끗한 벙커 연료에 대한 지원 정책

- 억제요인

- 석유시장의 불안정성

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 세분화

- 연료 유형별

- 고유황 연료유(HSFO)

- 초저유황 연료유(VLSFO)

- 해양 가스유(MGO)

- 액화천연가스(LNG)

- 기타 연료(메탄올, LPG, 바이오디젤)

- 선박 유형별

- 컨테이너

- 유조선

- 일반화물

- 벌크 컨테이너

- 기타 선박 유형

- 지역별

- 브라질

- 칠레

- 아르헨티나

- 기타 남미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- 연료 공급업체

- Vitol Holding BV

- Monjasa Holding A/S

- Bunker Holding A/S

- World Fuel Services Corp

- Peninsula Petroleum Ltd

- TotalEnergies SA

- Chevron Corporation

- 선박 소유업체

- AP Moeller Maersk A/S

- Mediterranean Shipping Company SA

- China COSCO Holdings Company Limited

- CMA CGM Group

- Hapag-Lloyd AG

- Ocean Network Express

- 연료 공급업체

- 시장 순위/점유율 분석

제7장 시장 기회와 앞으로의 동향

- 클린 연료의 이용

The South America Bunker Fuel Market size is estimated at USD 15.45 billion in 2025, and is expected to reach USD 19.53 billion by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the ever-rising marine transportation of essential commodities and implementation of stricter environmental regulations driving the demand for cleaner bunker fuels drive the growth in the South American bunker fuel market.

- On the other hand, the oil market's volatility is significantly expected to affect the bunker fuel market as it can impact the profitability of bunker fuel suppliers and make planning and investing difficult.

- Nevertheless, the increase in the use of clean bunker fuels creates a significant opportunity for the South American bunker fuel market.

- Brazil is expected to dominate the bunker fuel market in the region owing to factors like substantial crude oil production and a steady rise in exports from the country.

South America Bunker Fuel Market Trends

Very Low Sulfur Fuel Oil (VLSFO) to Witness Significant Growth

- The demand for shallow sulfur fuel oil (VLSFO) in the South African Bunker fuel market has seen a significant rise in recent years, following the International Maritime Organization's (IMO) mandate on reducing sulfur emissions from ships.

- As of April 2023, VLSFO availability is particularly strained in the domestic bunker fuel market, as most of the VLSFO used in the South Africa bunker fuel market is imported. Low-sulfur fuel oil is available in the ports of Durban, Port Elizabeth, and Cape Town, as well as at offshore bunkering in AlgoaBay (off Port Elizabeth and Ngqura).

- Moreover, the price fluctuations for VLSFO in the region are lesser compared to their counterparts, as between December 2022 and April 2023, the changes in prices were recorded at around 5%. In contrast, the counterparts have registered more variance, which further adds to the demand for this fuel.

- In October 2022, FUEL & MARINE OIL CORP (FAMOIL), a commodity trading house specializing in the marine fuel industry, added a bunker delivery vessel to its operation in Peru. The company added the tanker Ecomar II to its fleet. The vessel supplies Very Low Sulfur Fuel Oil (VLSFO) and High Sulfur Fuel Oil at Talara, Paita, Bayovar, Salaverry, Chimbote ports Pisco, San Nicolas, Matarani, and Llo.

- Moreover, the demand for VLSFO in the South American market is also driven by the growing number of vessels operating in the region. The stricter regulations on the environmental impact of these fuels on marine life have consequently driven the demand for VLSFO.

- Overall, the market is expected to witness significant growth during the forecast period owing to factors like increasing demand, which spurred up after the implementation of the IMO sulfur cap.

Brazil to Dominate the Market

- Brazil is the largest economy in the region and is expected to be the fastest-growing economy in the forecast period. The country is one of the fastest-growing countries worldwide because of the increasing population, industrialization, and urbanization.

- The increasing exports of oil from Brazil are anticipated to play a pivotal role in driving the market for bunker fuel in South America. Brazil, as a major oil-producing nation, has been expanding its oil output, and the growing exports present a significant opportunity for the bunker fuel market in the region.

- As international shipping routes pass through South American waters, the demand for bunker fuel used by marine vessels is expected to surge. Brazil's strategic location as a prominent exporter of oil makes it a crucial player in influencing the availability and pricing dynamics of bunker fuel in South America.

- For instance, In November 2022, Norwegian company Kanfer Shipping AS signed a partnership deal with Nimofast Brasil S.A. to establish small and medium-scale LNG shipping and LNG bunkering solutions in Brazil from 2025 onwards. The LNG vessels and LNG bunker ships will be loaded via the permanently based FSU at the Nimofast LNG import- and distribution terminal in the state of Parana.

- Moreover, the rise in oil exports from Brazil aligns with the broader trend of increased maritime trade activities in the region. As shipping traffic intensifies, the demand for bunker fuel as the primary energy source for marine vessels is expected to witness a corresponding uptick.

- This surge in demand for bunker fuel not only reflects the growing importance of South America in global trade but also underscores the interconnected nature of energy markets, where oil-exporting countries like Brazil can significantly impact the dynamics of related sectors such as marine fuels.

- Brazil owns the largest recoverable ultra-deep oil reserves in the world, with 96.7% of Brazil's oil production produced offshore. In 2022, the oil production was 163.1 million tonnes, increased from 156.9 million tonnes in 2021.

- Hence, with the expected increase in oil and gas production, trading activities between Brazil and the rest of the world are expected to increase further. With major international trading activities carried out through the marine route, Brazil is expected to become the emerging market for bunker fuel in the near future.

- All of the above factors are expected to help the country dominate the region in terms of bunker fuel during the forecast period.

South America Bunker Fuel Industry Overview

The South American bunker fuel market is semi-fragmented. Some of the major companies (in no particular order) are Bunker Holding A/S, Monjasa Holding A/S, AP Moeller Maersk A/S, World Fuel Services Corp, and Peninsula Petroleum Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Marine Transportation of Essential Commodities in South America

- 4.5.1.2 Supportive Policies for Cleaner Bunker Fuel

- 4.5.2 Restraints

- 4.5.2.1 Volatile Nature of Oil Market

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 High Sulfur Fuel Oil (HSFO)

- 5.1.2 Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3 Marine Gas Oil (MGO)

- 5.1.4 Liquefied Natural Gas (LNG)

- 5.1.5 Other Fuel Types (Methanol, LPG, and Biodiesel)

- 5.2 Vessel Type

- 5.2.1 Containers

- 5.2.2 Tankers

- 5.2.3 General Cargo

- 5.2.4 Bulk Container

- 5.2.5 Other Vessel Types

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Chile

- 5.3.3 Argentina

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Fuel Suppliers

- 6.3.1.1 Vitol Holding BV

- 6.3.1.2 Monjasa Holding A/S

- 6.3.1.3 Bunker Holding A/S

- 6.3.1.4 World Fuel Services Corp

- 6.3.1.5 Peninsula Petroleum Ltd

- 6.3.1.6 TotalEnergies SA

- 6.3.1.7 Chevron Corporation

- 6.3.2 Ship Owners

- 6.3.2.1 AP Moeller Maersk A/S

- 6.3.2.2 Mediterranean Shipping Company SA

- 6.3.2.3 China COSCO Holdings Company Limited

- 6.3.2.4 CMA CGM Group

- 6.3.2.5 Hapag-Lloyd AG

- 6.3.2.6 Ocean Network Express

- 6.3.1 Fuel Suppliers

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Utilization of Clean Bunker Fuels

샘플 요청 목록