|

시장보고서

상품코드

1687424

벙커연료 시장(2025-2030년) : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

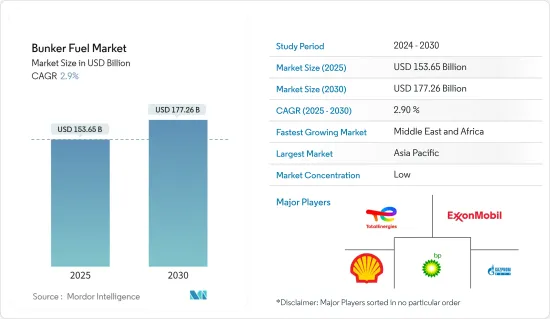

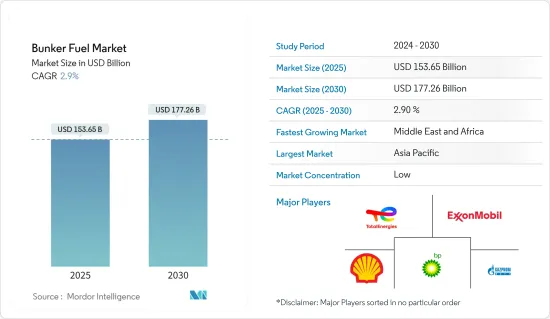

벙커연료 시장 규모는 2025년 1,536억 5,000만 달러에서 예측 기간(2025-2030년) 동안 CAGR 2.9%로 성장하여 2030년에는 1,772억 6,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 LNG 거래 증가가 벙커연료 수요를 높일 것으로 예상됩니다. LNG는 주로 산업, 상업 및 주택 분야의 전력 분야를 위해 거래됩니다. 중국과 인도와 같은 석탄 의존도가 높은 국가들은 중동, 러시아, 호주, 나이지리아와 같은 소수의 국가로부터 천연 가스 수입량을 늘려 점차 깨끗한 에너지로 전환하고 있습니다.

- 한편, 환경문제에 대한 우려와 해운업의 배출가스에 대한 엄격한 규제에 의해 예측 기간 중에는 중유, 특히 고유황 연료유의 사용이 제한될 것으로 예상됩니다.

- 그럼에도 불구하고 아시아태평양, 중동, 아프리카 등 지역에 걸친 신흥 국가의 경제 성과가 개선됨에 따라 해상 수송 수요와 운항 선박 수가 증가할 것으로 예상되며 향후 몇 년 동안 벙커연료 시장의 선도기업에게 큰 성장 기회를 제공합니다.

- 예측 기간 동안 아시아태평양이 시장을 독점하고 수요의 대부분은 중국과 인도와 같은 국가에서 발생할 것으로 예상됩니다.

벙커연료 시장 동향

LNG는 벙커연료 시장의 대폭적인 성장 부문으로 예상됩니다.

- 세계의 LNG 벙커링 시장은 온실가스 배출을 줄일 수 있는 장점으로 청정에너지에 대한 수요가 높아지는 가운데 세계의 LNG 사용량 증가에 견인되어 지난 10년간 발전해 왔습니다.

- 현재 운항중인 선박을 LNG 기반 선박으로 개조하는 것은 높은 비용을 초래하며 따라서 경제적으로 실행 불가능합니다. 그러나 새로운 배출 규제가 적용되면 LNG 기반 선박의 운항 비용은 모든 대체 연료 중 가장 낮을 것으로 예상됩니다. 또한, LNG 추진으로의 점진적인 전환은 중유, 선박용 가스유, 선박용 디젤유 등으로 선박에 연료를 공급하는 기존 방법보다 유리합니다. LNG 기반의 추진력은 이산화탄소 배출량을 대폭 줄여 선박의 운항 효율을 높입니다.

- LNG 연료 수요는 2030년까지 3,000만 톤으로 증가할 것으로 예상되고 있으며, 유럽, 아시아, 북미에서는 증가하는 가스 엔진 선대에 대응하기 위해 LNG 벙커선을 증설하고 있습니다. 조선소에 발주한 이 대용량 LNG 벙커선(LNGBV)은 주요 LNG 터미널에서 적재하고 가스 엔진이 장착된 외항선에 연료를 공급하도록 설계되었습니다.

- 2024년 2월 LNG 액티브 벙커선은 48척이었으며 2022년보다 11척이 많습니다. 전선대 중 절반 가까이는 유럽에서 운항하고 있으며 나머지는 아시아와 북미에서 조업하고 있습니다. 2024년 말 LNG 벙커링 선대의 수는 55척에 달했으며 2024년에만 총 67,900cm의 용량이 추가되었습니다.

- 특히 유럽 해역과 미국 해역에서 운영하는 선주는 현재 기존 선박보다 LNG 기반 선박을 선호합니다. 게다가 LNG 연료선은 벌크선 시장에서 가능성을 가지고 있습니다. 벌크선은 무거운 수하물을 운반하도록 설계되었으며 따라서 LNG 기술이 이러한 유형의 선박에 적용되는 것은 비교적 참신한 발상입니다. 벌크선은 가동중인 선박 중 가장 큰 점유율을 차지합니다.

- 또한 연료로 LNG를 사용하는 것은 입증된 상업적 솔루션입니다. LNG는 특히 배출가스 규제가 점점 강화되는 선박들에게 매우 큰 이점을 제공합니다. 중기적으로는 기존의 석유 기반 연료가 대부분의 선박의 주요 연료 선택사항이 될 것으로 예상되지만, 장기 시나리오에서는 LNG가 일반적인 선택이 될 것으로 보입니다.

- 2024년 4월, 기술 그룹인 Wartsila 산하의 Wartsila Gas Solutions는 스페인의 가스망을 소유 및 운영하는 Enagas의 자회사이자 스페인 선주인 Scale Gas용으로 건조 중인 1만 2500m3의 신규 LNG 벙커링 선박에 하역 시스템을 공급한다고 발표했습니다. 이 선박은 스페인 교통, 모빌리티 및 도시 계획부에 의한 부흥, 변혁, 및 강화 계획의 일환인 '지속 가능한 디지털 교통 지원 프로그램'의 공동 출자에 의한 것입니다.

- LNG는 기존 연료보다 비교적 저렴하며 석유 기반 선박 연료에 비해 온실가스 배출량을 23% 줄일 수 있어 세계 탈탄소 목표 달성에 기여합니다. 이러한 요인들로 인해 LNG는 향후 가장 인기 있는 선박용 연료가 될 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

- 아시아태평양은 인도, 중국, 싱가포르, 일본과 같은 국가의 거대한 해상 무역의 잠재력으로 인해 벙커연료 시장을 독점할 것으로 예상됩니다.

- 2023년 기준 중국은 수출액으로 1위, 수입액으로 2위 국가였습니다. 2023년 중국은 약 2조 5,000억 달러의 상품을 수입하고 3조 3,000억 달러를 수출했습니다. 중국의 주요 수출품은 기계 및 전기 장비, 자동차 부품, 화학 및 플라스틱, 철강 제품, 가구 등입니다.

- 호주는 세계에서 가장 큰 LNG 수출국 중 하나입니다. LNG 수출 증가는 호주 국제 무역의 성장을 지원합니다. LNG 수요는 세계적으로 크게 증가하고 있기 때문에 수출량은 향후 수년간 증가할 가능성이 높습니다.

- 국제무역과 국내무역의 해양부문 점유율을 높이기 위해 인도 정부는 2035년까지 220억 달러를 투자해 기존 항구의 현대화와 새로운 항구 건설을 진행할 것이라고 발표했습니다. 항만 인프라 개발은 예측 기간 동안 아시아태평양 해양 산업과 선박용 연료 공급업체에 대한 수요 증가로 이어질 것으로 예상됩니다.

- 2024년 2월, LNG 벙커 선박 용선주인 Pavilion Energy는 LNG 벙커 선박 Brassavola가 첫 STS(Ship to Ship) LNG 벙커 작업을 완료했다고 발표했습니다. Brassavola는 Rio Tinto가 용선주인 이중 연료 벌크선 Mount Api에 LNG를 공급했습니다.

- 따라서 앞서 언급한 요인들로 인해 예측 기간 동안 아시아태평양이 벙커연료 시장을 독점할 것으로 예상됩니다.

벙커연료 산업 개요

세계 벙커연료 시장은 단편화되었습니다. 시장의 주요 기업(순서부동)에는 Gazpromneft Marine Bunker LLC, ExxonMobil Corporation, Shell PLC, TotalEnergies SE, BP PLC 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 시장 규모 및 수요 예측(-2029년, 단위 : 달러)

- 최근 동향 및 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 세계의 LNG 무역 증가

- 발전용 천연 가스에의 높은 의존도

- 억제요인

- 환경 문제에 대한 우려와 해운업의 배출에 관한 엄격한 규제

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 투자분석

제5장 시장 세분화

- 연료 유형

- 고유황 연료유(HSFO)

- 초저황 연료유(VLSFO)

- 해양가스유(MGO)

- 액화천연가스(LNG)

- 기타 연료

- 선박 유형

- 컨테이너선

- 유조선

- 일반 화물선

- 벌크선

- 기타 선종

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 노르딕

- 터키

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 나이지리아

- 카타르

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- 연료 공급업체

- ExxonMobil Corporation

- Shell PLC

- Gazpromneft Marine Bunker LLC

- BP PLC

- PJSC Lukoil Oil Company

- TotalEnergies SE

- Chevron Corporation

- Clipper Oil

- Gulf Agency Company Ltd

- Bomin Bunker Holding GmbH & Co. KG

- 선박 소유자

- AP Moeller Maersk AS

- Mediterranean Shipping Company SA

- China COSCO Shipping Corporation Limited

- CMA CGM Group

- Hapag-Lloyd AG

- Ocean Network Express

- Evergreen Marine Corp Taiwan Ltd

- Yang Ming Marine Transport Corporation

- HMM Co. Ltd

- Pacific International Lines Pte Ltd

- 다른 주요 기업 목록

- 시장 랭킹 분석

- 연료 공급업체

제7장 시장 기회와 앞으로의 동향

- 해상 수송 수요 증가와 운항 선박 수 증가

The Bunker Fuel Market size is estimated at USD 153.65 billion in 2025, and is expected to reach USD 177.26 billion by 2030, at a CAGR of 2.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, increasing LNG trade is expected to boost the demand for bunker fuel. LNG is majorly traded for the power sector in industrial, commercial, and residential segments. Countries with high coal dependencies, such as China and India, are gradually moving toward cleaner energy by increasing the import volume of natural gas from the Middle East and a few other nations, like Russia, Australia, and Nigeria.

- On the other hand, environmental concerns and the strict regulations related to emissions from the maritime industry are anticipated to limit the usage of heavy bunker fuels, especially high sulfur fuel oil, during the forecast period.

- Nevertheless, with the improved economic performance of developing countries across regions such as Asia-Pacific and Middle East and Africa, the demand for marine transportation and the number of ships in operation are expected to increase, offering significant growth opportunities for players in the bunker fuels market over the coming years.

- Asia-Pacific is expected to dominate the market during the forecast period, with the majority of the demand being generated from countries like China and India.

Bunker Fuel Market Trends

LNG Likely to Witness Significant Market Growth as a Bunker Fuel

- The global LNG bunkering market has evolved over the past decade, driven by the increase in global LNG usage amid growing demand for clean energy due to its ability to reduce greenhouse gas emissions.

- The conversion of the current operating vessels into LNG-based vessels is highly expensive. Hence, it is not economically viable. However, the operational cost of LNG-based vessels is expected to be the lowest among all the fuel alternatives once the new emission regulations become applicable. Further, a gradual shift to LNG for propulsion is more advantageous than the traditional methods of fueling ships with heavy fuel oil, marine gas oil, marine diesel oil, etc. LNG-based propulsion reduces the carbon footprint significantly and increases a ship's operational efficiency.

- With demand for LNG as a fuel expected to rise to 30 million tonnes by 2030, Europe, Asia, and North America are adding LNG bunkering vessels to keep pace with the swelling gas-powered fleet. These larger capacity LNG bunker vessels (LNGBVs) on order at shipyards are designed to load at major LNG terminals and refuel gas-powered ocean-going tonnage.

- As of February 2024, there were 48 LNG active bunkering vessels, 11 more than in 2022. Out of the total fleet, nearly half operate in Europe, while the rest operate in Asia and North America. By the end of 2024, the number of LNG bunkering vessel fleets is likely to reach 55 units, with a total added capacity of 67,900 cm in 2024 alone.

- Shipowners, particularly those operating in the European or American Sea, now prefer LNG-based vessels over conventional vessels. Furthermore, LNG-fueled ships have not penetrated the market for bulk carriers to a significant extent, as these ships are designed to carry heavy loads, and LNG technology is relatively new to apply for this type of vessel. The bulk carriers amount to the largest share of the in-operation ships.

- Moreover, the use of LNG as a fuel is both a proven and commercially available solution. LNG offers enormous advantages, especially for ships in the light of ever-tightening emission regulations. Conventional oil-based fuels are expected to remain the primary fuel option for most ships in the mid-term, while LNG is likely to become a popular choice in the long-term scenario.

- In April 2024, Wartsila Gas Solutions, part of the technology group Wartsila, announced that it would supply the cargo handling system for a new 12,500 m3 LNG bunkering vessel being built for Spanish shipowner Scale Gas, a subsidiary of Enagas, the owner and operator of Spain's gas grid. The vessel is co-financed by the Support for Sustainable and Digital Transport Programme, part of the Recovery, Transformation and Resilience Plan from the Spanish Ministry of Transport, Mobility and Urban Agenda.

- LNG demand is likely to increase significantly in the forecast period as the order book for LNG vessels continues to increase due to it being relatively cheaper than conventional fuels and offering a 23% reduction in greenhouse gas emissions over oil-based marine fuel, which will aid in meeting global decarbonization goals. These factors project LNG to be the most popular marine fuel in the future.

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific is expected to dominate the bunker fuels market due to the immense maritime trade potential of countries like India, China, Singapore, and Japan.

- As of 2023, China ranked first in terms of exported goods and second for imported goods by value. In 2023, China imported goods worth around USD 2.5 trillion and exported USD 3.3 trillion. China's major exports are mechanical and electric machinery and equipment and automotive products, including vehicle parts, chemicals and plastics, iron and steel articles, and furniture.

- Australia is among the biggest exporters of LNG globally. Rising LNG exports have supported the growth in international trade in Australia. The export volume is likely to rise in the coming years as the demand for LNG is increasing significantly worldwide.

- To increase the share of the marine sector in international and domestic trade, the Indian government announced an investment of USD 22 billion by 2035 to modernize its existing ports and build new ports. The port infrastructure development is expected to increase the demand from the maritime industry and marine fuel suppliers in Asia-Pacific during the forecast period.

- In February 2024, Pavilion Energy, charterer of LNG bunker vessels, announced that LNG bunker vessel Brassavola had completed its first ship-to-ship (STS) LNG bunkering operation. In its maiden STS LNG bunkering operation, Brassavola delivered LNG to Rio Tinto chartered dual-fueled bulk carrier Mount Api.

- Therefore, in line with the aforementioned factors, Asia-Pacific is expected to dominate the bunker fuels market during the forecast period.

Bunker Fuel Industry Overview

The global bunker fuels market is fragmented. Some of the major players in the market (in no particular order) include Gazpromneft Marine Bunker LLC, ExxonMobil Corporation, Shell PLC, TotalEnergies SE, and BP PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increased LNG Trade Worldwide

- 4.5.1.2 Increasing Dependencies over Natural Gas for Power Generation

- 4.5.2 Restraints

- 4.5.2.1 Environmental Concerns and the Strict Regulations Related to Emissions from the Maritime Industry

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 High Sulfur Fuel Oil (HSFO)

- 5.1.2 Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3 Marine Gas Oil (MGO)

- 5.1.4 Liquefied Natural Gas (LNG)

- 5.1.5 Other Fuel Types

- 5.2 Vessel Type

- 5.2.1 Containers

- 5.2.2 Tankers

- 5.2.3 General Cargo

- 5.2.4 Bulk Carriers

- 5.2.5 Other Vessel Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Fuel Suppliers

- 6.3.1.1 ExxonMobil Corporation

- 6.3.1.2 Shell PLC

- 6.3.1.3 Gazpromneft Marine Bunker LLC

- 6.3.1.4 BP PLC

- 6.3.1.5 PJSC Lukoil Oil Company

- 6.3.1.6 TotalEnergies SE

- 6.3.1.7 Chevron Corporation

- 6.3.1.8 Clipper Oil

- 6.3.1.9 Gulf Agency Company Ltd

- 6.3.1.10 Bomin Bunker Holding GmbH & Co. KG

- 6.3.2 Ship Owners

- 6.3.2.1 AP Moeller Maersk AS

- 6.3.2.2 Mediterranean Shipping Company SA

- 6.3.2.3 China COSCO Shipping Corporation Limited

- 6.3.2.4 CMA CGM Group

- 6.3.2.5 Hapag-Lloyd AG

- 6.3.2.6 Ocean Network Express

- 6.3.2.7 Evergreen Marine Corp Taiwan Ltd

- 6.3.2.8 Yang Ming Marine Transport Corporation

- 6.3.2.9 HMM Co. Ltd

- 6.3.2.10 Pacific International Lines Pte Ltd

- 6.3.3 List of Other Prominent Companies

- 6.3.4 Market Ranking Analysis

- 6.3.1 Fuel Suppliers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Risisng Demand for Marine Transportation and Increasing Number of Ships in Operation

샘플 요청 목록