|

시장보고서

상품코드

1636568

영국의 이차 전지 시장 전망 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)United Kingdom Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

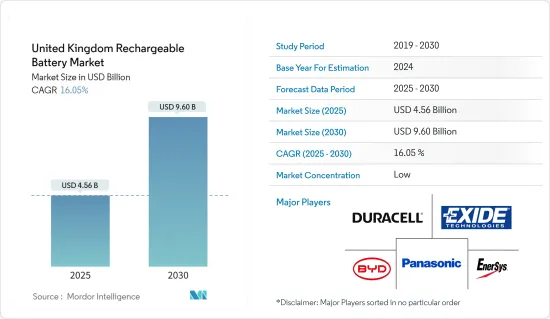

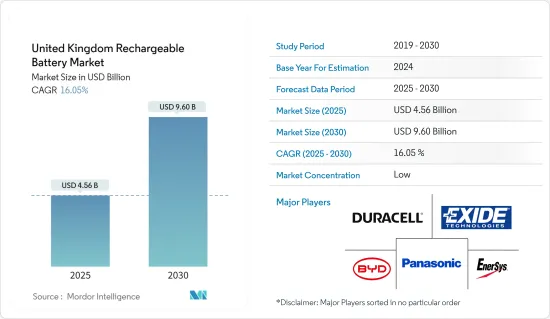

영국의 이차 전지 시장 규모는 2025년에 45억 6,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장률(CAGR)은 16.05%로, 2030년에는 96억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 전기차(EV) 보급률 상승과 리튬이온 배터리 가격 하락이 예측 기간 동안 이차 전지 수요를 주도할 것으로 예상됩니다.

- 한편, 원료의 매장량 부족은 영국의 이차 전지 시장의 성장을 크게 억제할 가능성이 있습니다.

- 그럼에도 불구하고 스마트 워치, 무선 이어폰, 스마트 밴드 등과 같은 웨어러블 디바이스의 채택이 확대되고 있기 때문에 이차 전지 시장의 진출기업에 있어서 기회가 생길 것으로 기대되고 있습니다.

영국의 이차 전지 시장 동향

리튬 이온 배터리 유형이 시장을 독점

- 리튬 이온 배터리는 뛰어난 용량 대비 중량비율로 다른 기술을 능가하는 인기를 자랑합니다. 게다가 긴 수명, 낮은 유지보수 비용 , 보존 기간의 연장, 현저한 가격 하락 등의 이점은 영국에서 리튬 이온 배터리 수요를 더욱 촉진하고 있습니다.

- 리튬 이온 배터리는 전통적으로 다른 배터리에 비해 비싸지만 이 산업의 주요 업계들은 투자를 강화하고 있습니다. 규모의 경제 실현과 연구개발 노력의 강화에 주력함으로써 경쟁이 심화되고, 리튬 이온 배터리의 가격이 현저하게 하락하고 있습니다.

- 2023년에는 리튬 이온 배터리 가격이 139달러/kWh까지 하락하여 13% 이상의 하락을 기록했습니다. 지속적인 혁신과 제조의 발전으로 인해 가격은 2025년까지 113달러/kWh로 더 낮아졌고, 2030년에는 80달러/kWh에 이를 것으로 예상됩니다.

- 리튬 이온 배터리의 수요가 급증하고 있는 이유는 재생 가능 에너지와 전기자동차로의 전환에 있어서 리튬 이온 배터리가 매우 중요한 역할을 하고 있기 때문입니다. 태양광이나 풍력과 같은 신재생에너지원의 간헐적인 특징을 생각하면, 신뢰성이 높은 에너지 저장 장치가 절실히 필요합니다. 리튬 이온 배터리는 에너지 저장 시스템에서 중요한 역할을 하고, 수요 및 공급의 균형을 맞추고, 그리드의 안정성을 확보하는 데 도움이 됩니다.

- 정부는 국가의 배터리 에너지 저장 능력 강화에 크게 진전을 보이고 있습니다. 주요 기업은 저장 시스템의 용량을 증대시키는 것을 목표로 하는 프로젝트를 전개하고 있습니다. 그 예로 2024년 3월 클린 에너지 주력 기업인 NatPower Group의 자회사인 NatPower UK는 100억 파운드(120억 달러) 이상을 전국 배터리 에너지 저장 시스템에 투자할 계획을 발표했습니다. 이 야심찬 프로젝트는 영국 전력망의 새로운 변전소에 대한 6억 GBP(7억 6,600만 달러)의 투자로 배터리용량을 60GWh 증가시키는 것을 목표로 합니다. 이러한 사업은 예측기간 동안 축전시설에서 리튬 이온 배터리 수요가 높아질 것으로 예상됩니다.

- 리튬 이온 배터리 시장을 강화하기 위해 각국 정부는 많은 투자를 실시하고 충전 가능한 리튬 이온 배터리의 생산을 적극적으로 추진하고 있습니다. 예를 들어, 영국 정부는 2023년 11월 야심찬 EV 생산 목표에 맞추어 리튬 이온 배터리를 중심으로 한 탄력적인 배터리 공급망을 강화하기 위해 5,000만 파운드(6,300만 달러)의 투자를 약속했습니다. 2030년까지의 배터리 전략은 향후 5년간의 새로운 자본과 R&D 자금을 포함하여 무공해 차량, 배터리, 공급망에 대한 적극적인 지원을 약속하고 있습니다. 이러한 전략적 투자와 인센티브는 영국에서 배터리 생산을 가속화하고 리튬 이온 배터리 수요를 확대시킬 것으로 기대됩니다.

- 이러한 개발 상황을 감안하면 리튬 이온 이차 전지의 전망은 예측 기간 동안에도 여전히 낙관적입니다.

전기차의 보급이 시장을 주도

- 오랫동안 내연 기관차(ICE)가 시장을 독점해 왔습니다. 그러나 환경에 대한 관심이 높아짐에 따라 전기차(EV)로의 이동이 두드러지고 있습니다. EV의 주류는 리튬 이온 이차 전지를 이용한 것으로, 에너지 밀도가 높고, 경량이며, 자기 방전이 적고, 유지 보수의 필요성이 낮기 때문에 선호되고 있습니다.

- 리튬 이온 이차 전지 시스템은 플러그인 하이브리드 자동차 및 전기자동차의 원동력이되었습니다. 타의 추종을 불허하는 에너지 밀도, 빠른 충전 능력 및 강력한 방전력으로 인해 리튬 이온 배터리는 주행 거리와 충전 시간에 대한 OEM 기준을 충족하는 유일한 기술이되었습니다. 대조적으로, 납 배터리는 무게가 무겁고 에너지 효율이 낮기 때문에 완전한 하이브리드 자동차 및 전기자동차에는 적합하지 않습니다.

- 최근 영국에서는 전기자동차의 도입이 급증하고 있습니다. 국제에너지기구(IEA)의 보고에 따르면 2023년 배터리 전기차 판매량은 31만대에 달했으며 2022년부터 14.8% 증가했습니다. 향후 몇 년동안 이 지역 전체에서 EV 판매량이 크게 증가될것으로 보입니다.

- 영국 정부는 전기자동차(EV)를 지지하고 저탄소 교통으로의 전환을 촉진하기 위한 여러 가지 정책을 시행하고 있습니다. 이러한 노력이 리튬 이온 배터리 수요를 높이고 있습니다. 2023년 정부는 EV 생산을 촉진하고 탄소 중립을 촉진하는 야심찬 계획을 발표했습니다.

- 영국은 2030년까지 신차의 80%, 신차 밴의 70%를 무공해 차량으로 하고, 2035년까지 완전 전환하는 것을 목표로 무공해차량(ZEV) 의무화를 설정했습니다. 게다가 2030년까지 가솔린차와 디젤차, 밴의 신차 판매를 금지하고, 2035년까지 모든 신차의 배기관을 무공해화 해야 합니다. 이러한 조치는 EV의 생산과 판매를 뒷받침할 뿐만 아니라 향후 수년간 이차 전지 수요도 급증할 것입니다.

- 이 지역의 주요 기업들은 전기자동차 생산을 확대하기 위해 많은 투자를 하고 프로젝트를 시작하고 있습니다. 예를 들어 Nissan은 2023년 11월 파트너사와 함께 전기자동차 캐쉬카이와 쥬크를 포함한 전기자동차 3모델을 자사 공장에서 생산하는 20억 파운드(25억 달러)의 구상을 발표했습니다. 또한 Nissan은 이러한 새로운 모델에 대응하는 영국 시설과 공급망 준비에 11억 2,000만 파운드(14억 달러)를 할당했습니다. 이러한 노력은 리튬 이온 배터리 수요 급증이 예상된다는 것을 뒷받침하고 있습니다.

- 이러한 노력이 쌓여서 EV 판매, 충전 인프라, 이차 전지 수요가 예측 기간 동안 크게 증가할 것이 분명합니다.

영국의 이차 전지 산업 개요

영국의 이차 전지 시장은 절반으로 단절되었습니다. 주요 기업(무순서)으로는 BYD Company Ltd., Duracell Inc., Exide Technologies, EnerSys, Panasonic Holdings Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 성장 촉진요인

- 전기자동차(EV)의 보급 확대

- 리튬 이온 배터리 가격 저하

- 억제요인

- 원료의 매장량 부족

- 성장 촉진요인

- 공급망 분석

- PESTLE 분석

- 투자 분석

제5장 시장 세분화

- 기술

- 리튬 이온

- 납 배터리

- 기타 기술(NiMh, Nicd 등)

- 용도

- 자동차용 전지

- 산업용 전지(동력용, 거치형(텔레콤, UPS, 에너지 저장 시스템(ESS) 등))

- 휴대용 전지(가전 제품 등)

- 기타

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- BYD Company Ltd

- Duracell Inc.

- EnerSys

- Panasonic Holdings Corporation

- Energizer

- Exide Technologies

- Saft Groupe SA

- AMTE Power

- Brill Power

- Eelpower

- 기타 저명한 기업 일람

- 시장 랭킹, 점유율 분석

제7장 시장 기회와 앞으로의 동향

- 웨어러블 디바이스의 채택 확대

The United Kingdom Rechargeable Battery Market size is estimated at USD 4.56 billion in 2025, and is expected to reach USD 9.60 billion by 2030, at a CAGR of 16.05% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, rising electric vehicle (EV) adoption and declining lithium-ion battery prices are expected to drive the demand for rechargeable batteries during the forecast period.

- On the other hand, the lack of raw material reserves can significantly restrain the growth of the United Kingdom's rechargeable battery market.

- Nevertheless, the growing adoption of wearable devices like smartwatches, wireless earphones, smart bands, and more are expected to create significant opportunities for rechargeable battery market players in the near future.

United Kingdom Rechargeable Battery Market Trends

Lithium-Ion Battery Type Dominate the Market

- Lithium-ion batteries are outpacing other technologies in popularity due to their superior capacity-to-weight ratio. Further, advantages like longevity, low maintenance, an extended shelf life, and a notable drop in prices are further fueling the demand for lithium-ion batteries in the United Kingdom.

- While lithium-ion batteries traditionally commanded a premium over their counterparts, key industry players have been ramping up investments. Their focus on achieving economies of scale and bolstering R&D efforts has intensified competition, leading to a notable dip in lithium-ion battery prices.

- In 2023, lithium-ion battery prices fell to USD 139/kWh, marking a decline of over 13%. With ongoing technological innovations and manufacturing advancements, projections suggest prices will further drop to USD 113/kWh by 2025 and reach USD 80/kWh by 2030.

- The surging demand for lithium-ion batteries is largely attributed to their pivotal role in the shift towards renewable energy and electric mobility. Given the intermittent nature of renewable sources like solar and wind, there's a pressing need for dependable energy storage. Lithium-ion batteries play a crucial role in energy storage systems, helping to balance supply and demand and ensuring grid stability.

- The government is making significant strides in bolstering the country's battery energy storage capacity. Major corporations are rolling out projects aimed at amplifying storage system capacities. A case in point: In March 2024, NatPower UK, a subsidiary of the clean energy giant NatPower Group, unveiled plans to invest over GBP 10 billion (USD 12 billion) in battery energy storage systems nationwide. The ambitious project aims to boost battery capacity by 60 GWh, complemented by an investment of GBP 600 million (USD 766 million) for new substations in the United Kingdom's electricity grid. Such undertakings are poised to elevate the demand for lithium-ion batteries in storage facilities during the forecast period.

- In a bid to bolster the lithium-ion battery market, governments are rolling out substantial investments and actively promoting the production of rechargeable lithium-ion batteries. For instance, in November 2023, the UK government pledged an investment of GBP 50 million (USD 63 million) to fortify a resilient battery supply chain, emphasizing lithium-ion batteries, in alignment with the nation's ambitious EV production goals. The Battery Strategy, set to run until 2030, promises targeted support for zero-emission vehicles, batteries, and their supply chains, including fresh capital and R&D funding over the next five years. Such strategic investments and incentives are poised to supercharge battery production in the United Kingdom, subsequently amplifying the demand for lithium-ion batteries.

- Given these developments, the outlook for lithium-ion rechargeable batteries remains bullish during the forecast period.

Increasing Adoption of Electric Vehicle to Drive the Market

- For a long time, vehicles with internal combustion engines (ICE) dominated the market. However, as environmental concerns grow, there's a notable shift towards electric vehicles (EVs). Predominantly, EVs utilize lithium-ion rechargeable batteries, favored for their high energy density, lightweight nature, minimal self-discharge, and low maintenance needs.

- Lithium-ion battery systems are the driving force behind plug-in hybrids and electric vehicles. Their unmatched energy density, rapid recharge capability, and robust discharge power make lithium-ion batteries the sole technology meeting OEM standards for driving range and charging time. In contrast, lead-based traction batteries fall short for full hybrids or EVs due to their heftier weight and lower energy efficiency.

- In recent years, the United Kingdom has seen a surge in electric vehicle adoption. The International Energy Agency (IEA) reported that in 2023, battery electric vehicle sales reached 0.31 million, marking a 14.8% increase from 2022. Projections indicate a significant uptick in EV sales across the region in the years ahead.

- The United Kingdom government has rolled out multiple policies to champion electric vehicles (EVs) and facilitate a shift towards a low-carbon transportation landscape. These initiatives have bolstered the demand for lithium-ion batteries. In 2023, the government unveiled ambitious plans to boost EV production and expedite the journey towards zero carbon emissions.

- The United Kingdom has set a Zero Emission Vehicle (ZEV) mandate, targeting 80% of new cars and 70% of new vans to be zero-emission by 2030, with a complete transition by 2035. Additionally, a ban on new petrol and diesel cars and vans is slated for 2030, and by 2035, all new vehicles must be zero-emission at the tailpipe. Such measures are poised to not only boost EV production and sales but also escalate the demand for rechargeable batteries in the coming years.

- Leading companies in the region are heavily investing and launching projects to amplify electric vehicle production. For instance, in November 2023, Nissan, alongside its partners, unveiled a GBP 2 billion (USD 2.5 billion) initiative to manufacture three electric car models, including the electric Qashqai and Juke, at their plant. Additionally, Nissan allocated GBP 1.12 billion (USD 1.4 billion) to ready its United Kingdom facilities and supply chain for these new models. Such endeavors underscore the anticipated surge in lithium-ion battery demand.

- Given these concerted efforts, it's evident that EV sales, charging infrastructure, and the demand for rechargeable batteries are set to rise significantly in the forecast period.

United Kingdom Rechargeable Battery Industry Overview

The United Kingdom rechargeable battery market is semi-fragmented. Some of the key players (not in particular order) are BYD Company Ltd, Duracell Inc., Exide Technologies, EnerSys, and Panasonic Holdings Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Electric Vehicle (EV) Adoption

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 Lack of Raw Material Reserves

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 Duracell Inc.

- 6.3.3 EnerSys

- 6.3.4 Panasonic Holdings Corporation

- 6.3.5 Energizer

- 6.3.6 Exide Technologies

- 6.3.7 Saft Groupe SA

- 6.3.8 AMTE Power

- 6.3.9 Brill Power

- 6.3.10 Eelpower

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption of Wearable Devices

샘플 요청 목록