|

시장보고서

상품코드

1907292

산업용 포장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Industrial Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

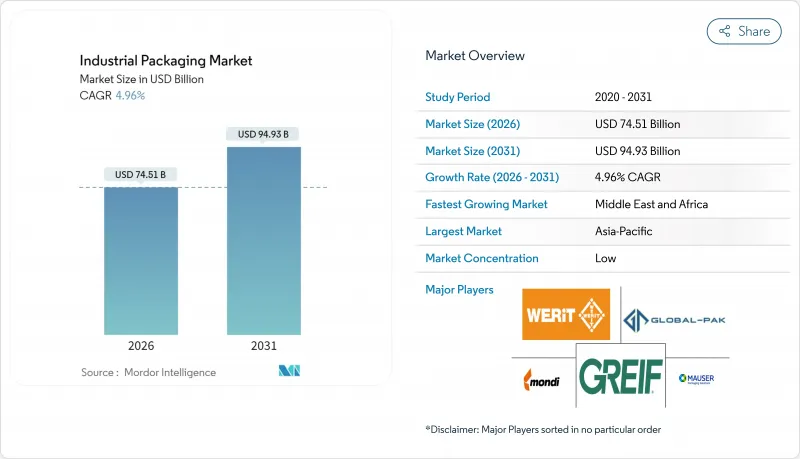

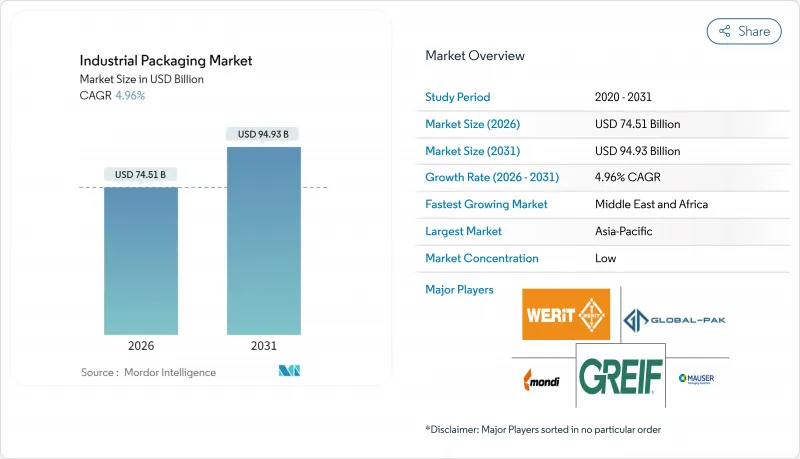

산업용 포장 시장 규모는 2026년 745억 1,000만 달러로 추정되며, 2025년 709억 9,000만 달러로 성장하여 2031년에는 949억 3,000만 달러에 이를 것으로 예상됩니다. 2026-2031년까지 연평균 4.96%의 성장률을 보일것으로 전망됩니다.

수요 회복력은 전자상거래 물류의 성장, 현장 포장 자동화의 가속화, 그리고 제조 부문 전반에 걸쳐 자재 선택과 운영 우선순위를 좌우하는 더욱 엄격한 규제 체계를 반영합니다. 전자상거래 물류에는 여러 거점을 거치는 배송 과정에서도 손상되지 않으면서 부피 중량을 최소화하는 보호 포장이 필요하며, 자동화 투자는 노동 시장 경색 속에서 생산자들이 노동 의존도를 줄이는 데 도움이 됩니다. 아시아태평양은 수출 지향형 제조업이 밀집되어 있는 것을 배경으로 2024년 수익의 40.45%를 차지했으며, 중동 및 아프리카는 에너지, 인프라, 식품 가공 분야에 대한 투자 계획을 배경으로 2030년까지 연평균 복합 성장률(CAGR) 6.34%로 가장 빠른 성장률을 보일 것으로 예상됩니다.산업 구매자들은 재활용 소재 함량 의무화와 기업의 지속가능성 목표를 핵심 조달 기준으로 삼고 있습니다.

세계의 산업용 포장 시장 동향과 인사이트

지속 가능하고 재생 가능한 소재의 상승

산업 구매자들은 재활용 소재 함량 의무화와 기업의 지속가능성 목표를 핵심 조달 기준으로 삼고 있습니다. 유럽연합(EU)은 2030년까지 플라스틱 제품의 재생재 함량 30%를 의무화하고 있으며, 컨버터 기업은 원료 조달의 재검토를 촉구하고 있습니다. 셀룰로오스계 복합재료는 식품·의약품 용도에 적합한 강도와 내습성을 갖추고 ISO 14855의 생분해성 기준을 충족합니다. 화이자는 자사 포장을 재활용 가능한 형태로 전환하여 포장 폐기물을 25% 삭감하면서 FDA 21 CFR 211의 무균성 규칙을 준수했습니다. 생산자는 새로운 금지 규정을 준수하면서 PFAS를 대체하는 바이오 코팅에 투자하여 수지 가격의 변동 위험을 헤지하고 있습니다. 연구개발이 확대되는 가운데, 조기 도입 기업은 비용면과 컴플라이언스면에서의 우위성을 획득해, 고객 유지율의 향상을 도모하고 있습니다.

전자상거래와 국경 간무역 흐름 확대

미국의 전자상거래 매출은 2024년에 1조 1400억 달러에 달할 것으로 예상되며, 이는 전체 소매 판매액의 16.4%에 해당합니다. 여러 사람이 취급하는 소포는 완충재와 부피 및 중량 효율이 뛰어난 포장이 필요합니다. 하루 2,000건 이상의 주문을 처리하는 시설에서는 99.5%의 정확도로 포장하고 인건비를 40% 절감할 수 있는 로봇을 점점 더 많이 도입하고 있습니다. 테슬라는 적응형 포장 시스템 도입 후 자재 사용량을 18% 삭감했습니다. 의약품의 규제 복잡화로 인해 시장을 가로지르는 ICH 표시 프로토콜을 충족하는 표준화된 세계 형식으로의 전환이 진행되고 있습니다.

수지·강재 가격의 변동

2024년 강재 가격은 650-850달러/톤으로 추이해 장기 계약을 맺는 드럼 제조업체를 압박했습니다. 폴리에틸렌과 폴리프로필렌은 15-20% 변동하여 원재료비가 비용의 60-70%를 차지하기 때문에 생산자가 타격을 흡수했습니다. 다우공급업체는 12%의 이익률 하락을 겪었습니다. 유연한 가격설정과 단기계약이 증가하는 반면 재협상은 2024년 이전 대비 25% 증가하여 관계에 부담이 되었습니다.

부문 분석

중형 벌크 컨테이너(IBC)는 350-700bar의 압력을 견딜 수 있는 복합 소재 용기가 필요한 수소 프로젝트에 힘입어 2031년까지 연평균 6.98%의 가장 빠른 성장률을 기록할 것으로 예상됩니다. 드럼통은 2025년 산업용 포장 시장의 35.02%를 점유했으며, 다목적 화학물질 운송의 핵심으로 자리매김하고 있습니다.

IBC(중형 벌크 컨테이너)는 수소 허브를 위한 70억 달러의 자금 조달을 통해 혜택을 받는 한편, 스틸 드럼 수요는 원재료 가격의 변동에 직면하면서도 확립된 유엔 인증 인지도를 누리고 있습니다. 플렉서블 IBC는 ATEX 준거의 정전기 방지 소재를 채용해 폭발성 분위기 분야에 대응하고 있습니다.

플라스틱은 2025년에 46.02%의 점유율로 우위를 유지했지만 규제 강화 압력이 높아지고 있습니다. PFAS 프리 배리어 코팅 기술의 성숙에 따라 종이 섬유 소재는 6.61%의 연평균 복합 성장률(CAGR)이 전망됩니다.

TAPPI의 측정에 따르면, 배리어성 판지의 생산량은 25% 증가했으며, 자동차 제조업체는 플라스틱 재활용 컨테이너에 30%의 재생재 함유를 의무화하고 있습니다. 고급 셀룰로오스 필름은 폴리에틸렌과 동등한 산소 장벽 성능을 발휘하여 종이 이용 사례를 확대하고 있습니다.

지역별 분석

아시아 태평양 지역은 수출 중심의 제조업과 국내 포장 기계 생산량의 8.1% 증가에 힘입어 2025년 매출의 40.12%를 차지할 것으로 예상됩니다. 중동 및 아프리카 지역은 200억 달러 규모의 석유화학 프로젝트에 힘입어 연평균 6.18%의 성장률을 기록하며 지역 내 최고 성장세를 보일 것입니다.

북미에서는 멕시코 수출이 15% 증가한 4,920억 달러에 달하고, 니어 쇼어링의 혜택을 받고 있습니다. 유럽에서는 순환형 경제 프로토콜이 강화되어 재활용 가능한 형태가 우월합니다.

사우디아라비아의 산업 정책에 따라 유엔 규격에 적합한 대형 드럼통과 복합 IBC 용기 수요가 확대. 인도에서는 3,400캐롤 루피(4억 800만 달러) 규모의 식품 가공 투자가 섬유계 2차 포장을 촉진. 일본의 화학물질 안전규제가 높은 배리어 다층 포장으로의 전환을 뒷받침. UAE의 산업전략은 제조업 GDP 비율 25%를 목표로 하여 지역 팔레트 컨테이너 풀 수요를 환기.

아프리카 대륙 자유 무역 협정(AfCFTA) 프레임 워크는 역내 무역을 촉진하고 표준화 된 산업용 포장 시장 솔루션의 국경을 넘어 진출의 길을 엽니다. 사하라 이남의 인프라 정비는 시멘트나 화학약품의 수송용 대형 봉투·드럼 수요를 확대합니다. 유럽 항만에서는 EDI 서류의 확대에 의해 통관이 가속되고, 벌크 컨테이너에의 국제 표준 라벨 채용이 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 지속 가능하고 재활용 가능한 소재의 상승

- 전자상거래 확대와 국경 간무역의 흐름

- 식품 등급 및 의약품 발크로디스틱스의 성장

- 현지 포장 자동화의 도입 상황

- 재사용 가능 포장 풀 비즈니스 모델

- 복합 IBC에 대한 수소 공급 체인 수요

- 시장 성장 억제요인

- 수지 및 강재 가격의 변동성

- 세계 환경 규제 강화

- 배리어 코팅에 있어서 PFAS/마이크로 플라스틱 금지

- 니어 쇼어링에 의한 장거리 수송 포장량의 감소

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 제품별

- 중간 벌크 용기(IBC)

- 드럼

- 자루

- 통

- 기타 제품

- 재료별

- 플라스틱

- 금속

- 종이 및 섬유 기반

- 기타 재료

- 최종 사용자 업계별

- 화학 및 제약

- 식품 및 음료

- 자동차

- 석유, 가스 및 석유화학

- 건축 및 건설

- 기타 최종 사용자 업계

- 포장 용량별

- 50L 이하

- 51-500L

- 501-1,000L

- 1,001-2,000L

- 2,000L 초과

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 케냐

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Greif, Inc.

- Mauser Packaging Solutions Holding Company

- Mondi plc

- Smurfit WestRock

- Amcor plc

- International Paper Company

- Packaging Corporation of America

- Schutz GmbH & Co. KGaA

- WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- Tank Holding Corp.

- Visy Industries Holdings Pty Ltd

- Pact Group Holdings Ltd

- Brambles Limited(CHEP)

- Global-Pak, Inc.

- Nefab AB

- Snyder Industries, LLC

- Myers Container, LLC

- Veritiv Corporation

- Snyder Industries, Inc.

- Pyramid Technoplast Ltd

제7장 시장 기회와 향후 전망

KTH 26.01.20Industrial packaging market size in 2026 is estimated at USD 74.51 billion, growing from 2025 value of USD 70.99 billion with 2031 projections showing USD 94.93 billion, growing at 4.96% CAGR over 2026-2031.

Demand resilience reflects the rise of e-commerce fulfillment, accelerating on-site packaging automation, and stricter regulatory frameworks that shape material choices and operational priorities across manufacturing sectors. E-commerce logistics require protective formats that survive multi-node shipping while keeping dimensional weight low, and automation investments help producers curb labor dependence amid tight labor markets. Asia-Pacific commanded 40.45% of 2024 revenue, supported by dense export-oriented manufacturing, while the Middle East and Africa are advancing the fastest at 6.34% CAGR to 2030 on the back of energy, infrastructure, and food processing investment pipelines.

Global Industrial Packaging Market Trends and Insights

Emergence of Sustainable and Recyclable Materials

Industrial buyers are making recycled-content mandates and corporate sustainability targets a central procurement criterion. The European Union requires 30% recycled content in plastic formats by 2030, compelling converters to overhaul feedstock sourcing. Cellulose-based composites deliver strength and moisture resistance suitable for food and pharma usage and meet ISO 14855 biodegradability thresholds. Pfizer's internal switch to recyclable formats cut packaging waste 25% yet complied with FDA 21 CFR 211 sterility rules. Producers hedge resin volatility by investing in bio-based coatings that replace PFAS while complying with emerging bans. As R&D scales, early adopters gain cost and compliance advantages that enhance customer retention.

Expansion of E-commerce and Cross-Border Trade Flows

E-commerce revenue in the United States hit USD 1.14 trillion in 2024, or 16.4% of retail sales. Multihandled parcels need cushioning and dimensional-weight efficient designs. Facilities shipping more than 2,000 orders per day are increasingly deploying robotics able to pack with 99.5% accuracy and cut labor costs by 40%. Tesla demonstrated an 18% materials drop after installing adaptive packaging systems. Regulatory complexity in pharmaceuticals pushes shippers toward standardized global formats that meet ICH labeling protocols across markets.

Volatile Resin and Steel Prices

Steel ranged from USD 650-850 / t in 2024, squeezing drum makers under long-term contracts. Polyethylene and polypropylene fluctuated 15-20%, with producers absorbing hits because raw inputs form 60-70% of cost. Dow's suppliers suffered 12% margin erosion. Flexible pricing and shorter contracts proliferate, yet renegotiations rose 25% over pre-2024 levels, straining relationships.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Food-Grade and Pharma Bulk Logistics

- On-Site Packaging Automation Adoption

- PFAS / Micro-Plastic Bans on Barrier Coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Intermediate bulk containers own the fastest 6.98% CAGR to 2031, propelled by hydrogen projects that require 350-700-bar composite vessels. Drums held 35.02% industrial packaging market share in 2025 and remain the backbone for multipurpose chemicals.

IBCs benefit from USD 7 billion in hydrogen hub funding, while steel drum demand faces raw-material swings yet enjoys entrenched UN certification familiarity. Flexible intermediate bulk containers adopt antistatic fabrics compliant with ATEX to serve explosive-atmosphere sectors.

Plastic dominated with 46.02% share in 2025 but faces mounting regulatory scrutiny. Paper and fiber options are set for a 6.61% CAGR as PFAS-free barrier coatings mature.

TAPPI measured 25% growth in barrier paperboard output, and automakers now mandate 30% recycled content in plastic returnable bins. Advanced cellulose films match oxygen barrier performance seen in polyethylene, enlarging paper's addressable use cases.

The Industrial Packaging Market Report is Segmented by Product (Intermediate Bulk Containers, Drums, Sacks, and More), Material (Plastics, Metal, Paper and Fiber-Based, and More), End-User Industry (Chemicals and Pharmaceuticals, Food and Beverage, Automotive, Oil Gas and Petrochemicals, and More), Packaging Capacity (<=50L, 51-500L, 501-1000L, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific supplied 40.12% of 2025 revenue thanks to export-heavy manufacturing and 8.1% growth in domestic packaging machinery output. Middle East and Africa will top regional growth charts at 6.18% CAGR, aided by USD 20 billion in petrochemical projects.

North America benefits from near-shoring as Mexico's exports rose 15% to USD 492 billion. Europe tightens circular-economy protocols that favor recyclable formats.

Saudi industrial policies drive demand for heavy-duty drums and composite IBCs meeting UN specs. India's food-processing investments worth INR 3,400 crore (USD 408 million) encourage fiber-based secondary packaging. Japanese chemical safety rules inspire high-barrier multilayer upgrades. The UAE's industrial strategy targets 25% manufacturing GDP share, stimulating regional pallet and container pools.

Africa's AfCFTA framework fosters intra-continental trade, opening gateways for standardized industrial packaging market solutions across borders. Sub-Saharan infrastructure work advances demand for large sacks and drums to move cement and chemicals. European ports expand EDI documentation to accelerate customs clearance, prompting adoption of globally harmonized labeling on bulk containers.

- Greif, Inc.

- Mauser Packaging Solutions Holding Company

- Mondi plc

- Smurfit WestRock

- Amcor plc

- International Paper Company

- Packaging Corporation of America

- Schutz GmbH & Co. KGaA

- WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- Tank Holding Corp.

- Visy Industries Holdings Pty Ltd

- Pact Group Holdings Ltd

- Brambles Limited (CHEP)

- Global-Pak, Inc.

- Nefab AB

- Snyder Industries, LLC

- Myers Container, LLC

- Veritiv Corporation

- Snyder Industries, Inc.

- Pyramid Technoplast Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Emergence of sustainable and recyclable materials

- 4.2.2 Expansion of e-commerce and cross-border trade flows

- 4.2.3 Growth in food-grade and pharma bulk logistics

- 4.2.4 On-site packaging automation adoption

- 4.2.5 Reusable packaging pool business models

- 4.2.6 Hydrogen-supply chain demand for composite IBCs

- 4.3 Market Restraints

- 4.3.1 Volatile resin and steel prices

- 4.3.2 Tightening global environmental regulations

- 4.3.3 PFAS / micro-plastic bans on barrier coatings

- 4.3.4 Near-shoring lowering long-haul packaging volumes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 The Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Intermediate Bulk Containers (IBCs)

- 5.1.2 Drums

- 5.1.3 Sacks

- 5.1.4 Pails

- 5.1.5 Other Products

- 5.2 By Material

- 5.2.1 Plastics

- 5.2.2 Metal

- 5.2.3 Paper and Fiber-based

- 5.2.4 Other Materials

- 5.3 By End-user Industry

- 5.3.1 Chemicals and Pharmaceuticals

- 5.3.2 Food and Beverage

- 5.3.3 Automotive

- 5.3.4 Oil, Gas and Petrochemicals

- 5.3.5 Building and Construction

- 5.3.6 Other End-user Industries

- 5.4 By Packaging Capacity

- 5.4.1 <= 50 L

- 5.4.2 51 - 500 L

- 5.4.3 501 - 1,000 L

- 5.4.4 1,001 - 2,000 L

- 5.4.5 > 2,000 L

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Greif, Inc.

- 6.4.2 Mauser Packaging Solutions Holding Company

- 6.4.3 Mondi plc

- 6.4.4 Smurfit WestRock

- 6.4.5 Amcor plc

- 6.4.6 International Paper Company

- 6.4.7 Packaging Corporation of America

- 6.4.8 Schutz GmbH & Co. KGaA

- 6.4.9 WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- 6.4.10 Tank Holding Corp.

- 6.4.11 Visy Industries Holdings Pty Ltd

- 6.4.12 Pact Group Holdings Ltd

- 6.4.13 Brambles Limited (CHEP)

- 6.4.14 Global-Pak, Inc.

- 6.4.15 Nefab AB

- 6.4.16 Snyder Industries, LLC

- 6.4.17 Myers Container, LLC

- 6.4.18 Veritiv Corporation

- 6.4.19 Snyder Industries, Inc.

- 6.4.20 Pyramid Technoplast Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment