|

시장보고서

상품코드

1692465

자동차용 브레이크 패드 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Automotive Brake Pad - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

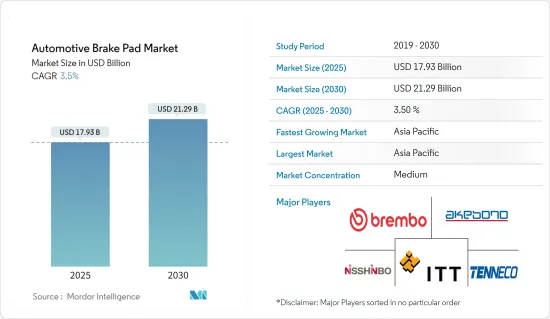

세계의 자동차용 브레이크 패드 시장 규모는 2025년에 179억 3,000만 달러로 추계되어 예측 기간(2025-2030년) CAGR 3.5%로 확대되고, 2030년에는 212억 9,000만 달러에 달할 것으로 예측됩니다.

소비자와 당국간에 안전에 대한 의식이 높아짐에 따라 자동차용 브레이크 시스템이 크게 개발되어, 그 결과, 안전성이 향상되고, 길거리에서의 사고가 감소하고 있습니다.

각 자동차 제조업체는 브레이크 효율을 향상시키기 위해 혁신적인 브레이크 패드를 차량에 통합하고 있습니다.

게다가 급속한 도시화, 교통 혼잡, 고성능 차에 대한 수요 증가가 승용차나 전기자동차(EV) 수요를 촉진하고 있습니다. 전기자동차의 보급은 브레이크 패드 제조업체가 EV의 회생 브레이크 특유의 요건에 맞춘 전용 솔루션을 개발하는 기회를 가져오고 있습니다.

자동차용 브레이크 패드 시장 동향

승용차가 시장을 선도하는 부문

승용차 부문은 자동차용 브레이크 패드 시장의 최대 부문이며, 승용차의 대수 증가, 자동차 업그레이드에 대한 소비자의 기호의 변화, 브레이크 시스템의 기술 진보 등의 요인에 의해 견인되고 있습니다.

도로를 달리는 승용차의 방대한 대수는 브레이크 패드 수요에 직접 공헌하고 있습니다. 승용차의 생산 대수와 판매 대수 증가, 그리고 세계에서 예상되는 전기자동차의 보급 확대에 의해 향후 수년간은 보다 높은 내구성과 방열 성능을 갖춘 선진적인 자동차용 브레이크 패드 제품에 대한 수요가 급증할 것으로 예상됩니다.

엄격한 안전 규제와 자동차의 안전성에 관한 소비자의 의식의 고조도, 조사된 시장을 견인하고 있습니다. 개인이나 가족의 이동 수단으로서 가장 널리 이용되고 있는 승용차는 사고를 일으키기 쉽기 때문에 엄격한 안전 규제의 대상이 되고 있습니다.

- 예를 들어 NHTSA는 2023년 7월 보행자용 AEB를 포함한 자동 긴급 브레이크 시스템을 경차에 의무화하는 새로운 연방 자동차 안전 기준을 제안했습니다.

선진국에서의 승용차 수요 증가와 더불어 프리미엄카와 고급차 제조업체가 첨단 기능을 탑재한 신제품 개발에 대한 투자를 늘리고 있기 때문에 시장의 주요 기업은 브레이크 패드의 내구성, 성능, 안전성을 높이는 첨단 재료와 설계를 도입하기 위한 연구개발에 투자할 수밖에 없습니다.

- 예를 들어, 일본을 거점으로 하는 Totachi Industrial Co. Ltd,은 2023년 8월, 브레이크 패드의 제조를 개시해, 종합적인 솔루션을 확대했습니다. 제품 라인 업에 추가된 브레이크 패드는 다양한 브랜드의 승용차용으로 설계되고 있습니다.

따라서 승용차 부문은 예측 기간 동안 큰 성장을 이룰 것으로 기대됩니다.

성장 가능성이 가장 높은 아시아태평양

세계적으로 보면 자동차용 브레이크 패드 시장에서는 아시아태평양이 가장 우위를 차지하고 있으며, 이어 유럽, 북미가 되고 있습니다.

중국은 세계 최대의 자동차 시장이기 때문에 주요 지역 중 하나로 떠오를 것으로 예상됩니다.

소음 저감, 패드 수명의 연장, 브레이크 성능의 향상은 매우 중요한 특징입니다.소음 공해가 우려되는 도시 환경에서는 저소음의 브레이크 패드가 강하게 요구되고 있습니다.

- 예를 들어, 미국 공급업체인 Tenneco는 2023년 6월 중국의 브레이크 패드 시장의 원동력이기도 한 전동화 차량의 현지 제조업체에 주력하는 것으로, 중국에서의 브레이크 부품 사업의 수익을 높이는 것을 목표로 내걸었습니다.

게다가 인도의 자동차 부문에서는 자동차의 생산과 판매가 늘어나고 있으며, 이 나라는 브레이크 패드의 잠재적인 시장이 되고 있습니다. 교통 안전 및 차량 유지 보수에 필수적이며 애프터마켓 매출을 촉진하고 있습니다.

- 예를 들어, 2023년 3월, 인도 및 세계 OEM의 Tier 1 공급업체인 Brakes India사는 전기자동차용으로 조정된 첨단 마찰 기술을 특징으로 하는 ZAP 브레이크 패드를 발표했습니다.

아시아태평양의 이러한 양호한 개발로 자동차 브레이크 패드 수요는 예측 기간 동안 적절한 속도로 성장할 가능성이 높습니다.

자동차용 브레이크 패드 산업 개요

자동차용 브레이크 패드 시장은 ITT Inc., Brembo SpA, ADVICS, Beijing Delphi Wanyuan Engine Management Systems, BorgWarner Shanghai Automotive Fuel Systems, Robert Bosch GmBH, Delphi Technologies, Tenneco Inc., Akebono Brake Company, EBC Brakes 등 주요 기업이 주로 점유하고 있습니다. 이 시장을 독점하고 있는 제조 기업은 소수이며, 첨단 기술을 제품에 통합하기 위해 연구 개발에 많은 투자를 하고 경쟁력을 유지하기 위해 항상 업그레이드한 제품을 투입하고 있습니다.

- 2023년 9월 Brembo SpA는 승용차 및 상용차에서 탄소 세라믹 브레이크 디스크 수요 증가에 대응하기 위한 전략적 이니셔티브를 발표했습니다. 이 계획의 일환으로 Brembo SGL Carbon Ceramic Brakes(BSCCB)는 2027년까지 1억 6,950만 달러를 투자해 독일 마이팅겐과 이탈리아 스테차노 시설에서 생산 능력을 70% 확대했습니다.

- 2023년 5월 Robert Bosch GmbH는 TVS 아파치 전용의 신형 엘리트 브레이크 패드를 발매했습니다. 이 패드는 독자적인 아브라 코트 기술에 의한 스트라이프 코팅을 한 첨단 패드입니다.

- 2023년 3월 Brakes India는 전기자동차 전용으로 설계된 뛰어난 마찰 기술을 활용한 ZAP 브레이크 패드를 발매했습니다. 이 패드는 내식성이 뛰어날뿐만 아니라 조용한 브레이킹을 실현하고 배터리 구동의 요구에 직접 대응합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 브레이크 패드 재료와 기술의 진보

- 시장 성장 억제요인

- 브레이크의 결함과 제품 리콜

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 소재 유형별

- 세미 메탈릭

- 비석면 유기

- 저금속

- 세라믹

- 포지션 유형별

- 프런트

- 리어

- 판매 채널별

- 상대방 브랜드 제조(OEM)

- 애프터마켓

- 차종별

- 승용차

- 상용차

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 한국

- 일본

- 기타 아시아태평양

- 세계 기타 지역

- 남미

- 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Brembo SpA

- ITT Inc.

- Robert Bosch GmBH

- Tenneco Inc.

- Akebono Brake Industry Co. Ltd

- ZF Friedrichshafen AG

- Continental AG

- Federal-Mogul Holdings LLC

- BorgWarner Inc.

- Nisshinbo Holdings Inc.

- Garrett Motion Inc.

제7장 시장 기회와 앞으로의 동향

제8장 주요 공급자 정보

JHS 25.05.07The Automotive Brake Pad Market size is estimated at USD 17.93 billion in 2025, and is expected to reach USD 21.29 billion by 2030, at a CAGR of 3.5% during the forecast period (2025-2030).

Increasing awareness about safety among consumers and authorities has led to significant developments in the automotive brake system, resulting in improved security and reduced accidents on the road. With further technological advancements, the market is expected to see even safer and more reliable brake systems.

Individual vehicle manufacturers are incorporating innovative brake pads in their vehicles to improve braking efficiency. Industry players offer a wide range of products that include environmentally friendly brake pad materials. Factors like these are expected to drive the market's growth during the forecast period.

Furthermore, rapid urbanization, traffic congestion, and the growing demand for high-performance vehicles are propelling the demand for passenger and electric vehicles (EVs). The proliferation of electric vehicles is presenting opportunities for brake pad manufacturers to develop specialized solutions tailored to the unique requirements of regenerative braking in EVs. This surge in demand for automobiles, in turn, augments the brake pad market.

Automotive Brake Pad Market Trends

Passenger Car is the Leading Segment in the Market

The passenger car segment is the largest segment in the automotive brake pad market, driven by factors like the increasing volume of passenger cars, changing consumer preferences toward vehicle upgradation, technological advancement in braking systems, etc.

The huge volume of passenger cars on the roads contributes directly to the demand for brake pads. In 2023, 57.01 million units of passenger cars were sold globally, as compared to 50.75 million units in 2022, registering a year-on-year growth of about 1.2%. The increase in passenger car production and sales and the anticipated greater adoption of electric vehicles across the globe are expected to create a surge in demand for advanced automotive brake pad products with higher durability and greater heat dissipation capability in the coming years.

Stringent safety regulations and increasing consumer awareness regarding vehicle safety also drive the market studied. Being the most widely used personal mode of transport for individuals and families, passenger cars are prone to accidents and thus are subject to strict safety norms. Governments in many regions have introduced mandatory regulations regarding braking systems in cars.

- For instance, in July 2023, the NHTSA proposed a new Federal Motor Vehicle Safety Standard to require automatic emergency braking systems, including pedestrian AEB, on light vehicles. The NHTSA projects that this proposed rule would save at least 360 lives a year and reduce injuries by at least 24,000 annually.

The rising investments from premium and luxury car manufacturers to develop new products with advanced features, coupled with the increasing demand for passenger cars in developed nations, are compelling key market players to invest in research and development to introduce advanced materials and designs that enhance the durability, performance, and safety of brake pads.

- For instance, in August 2023, Totachi Industrial Co. Ltd, based in Japan, expanded its comprehensive solution by initiating the manufacturing of brake pads. The latest addition to its product lineup encompasses brake pads designed for passenger cars across diverse brands. These brake pads are meticulously crafted to serve as OEM (original equipment manufacturer) products, guaranteeing exceptional quality.

Hence, the passenger car segment is expected to witness significant growth during the forecast period.

Asia-Pacific Witnessing Highest Potential for Growth

Globally, Asia-Pacific is the most dominant region in the automotive break pad market, followed by Europe and North America. Asia-Pacific is likely to possess the highest growth rate, with countries like China, India, Japan, and South Korea expected to contribute significantly in terms of revenue in the global anti-lock braking system due to safety norms and firm government regulations.

China is expected to emerge as one of the major regions, owing to its largest automotive market in the world. China was the world's largest regional market for automobiles in 2022, accounting for over 23.6 million unit sales alone. This growth directly influences the demand for brake pads, as each vehicle requires this essential component. The automotive industry in China is evolving, and so is the brake pad technology.

Noise reduction, extended pad life, and enhanced braking performance are crucial features. In urban environments where noise pollution is a concern, low-noise brake pads are highly sought after. The brake pad market in China is highly competitive, with both local and international players vying for market share. Multiple key market players are making substantial investments to establish new production facilities within the country.

- For instance, in June 2023, Tenneco, a US supplier, set its sights on boosting revenue from its brake parts business in China by focusing on local manufacturers of electrified vehicles, which also drive the brake pad market in the country.

Moreover, the growing vehicle production and sales in India's automotive sector make the country a potential market for brake pads. The aftermarket segment plays a substantial role in the Indian brake pad market. Regular brake pad replacement is essential for road safety and vehicle maintenance, which fuels aftermarket sales. Numerous players in the market are investing heavily in setting up new production units in the country to meet the rising demands for local and international markets and enhance their profitability and market share.

- For instance, in March 2023, Brakes India, a tier-1 supplier to both Indian and global OEMs, introduced ZAP brake pads featuring advanced friction technology tailored for electric vehicles. These specialized brake pads are designed to meet the unique needs of electric vehicle customers, providing improved corrosion protection and ensuring quieter braking.

Due to such favorable developments across Asia-Pacific, the demand for automotive brake pads is likely to grow at a decent rate during the forecast period.

Automotive Brake Pad Industry Overview

The automotive brake pad market is primarily dominated by key players such as ITT Inc., Brembo SpA, ADVICS, Beijing Delphi Wanyuan Engine Management Systems Co. Ltd, BorgWarner Shanghai Automotive Fuel Systems Co. Ltd, Robert Bosch GmBH, Delphi Technologies, Tenneco Inc., Akebono Brake Company, and EBC Brakes, among others. Few manufacturing companies dominate this market and invest heavily in research and development to integrate state-of-the-art technology into their products, consistently introducing upgraded offerings to maintain their competitive edge.

- September 2023: Brembo SpA announced a strategic initiative to meet the increasing demand for carbon ceramic brake discs in passenger cars and commercial vehicles. As part of the plan, Brembo SGL Carbon Ceramic Brakes (BSCCB) invested a whopping USD 169.5 million by 2027 to expand production capacities by 70% at its Meitingen, Germany, and Stezzano, Italy facilities.

- May 2023: Robert Bosch GmbH launched the new Elite brake pads specifically tailored for the TVS Apache. These cutting-edge pads boast a stripe-coating infused with the proprietary ABRACOAT technology.

- March 2023: Brakes India introduced ZAP brake pads, leveraging superior friction technology specifically designed for electric vehicles. These pads not only offer better corrosion protection but also ensure silent braking, catering directly to the needs of battery-powered.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Advancements in Brake Pad Materials and Technologies

- 4.2 Market Restraints

- 4.2.1 Brake Malfunctions and Product Recalls

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value (USD))

- 5.1 By Material Type

- 5.1.1 Semi-metallic

- 5.1.2 Non-asbestos Organic

- 5.1.3 Low-metallic

- 5.1.4 Ceramic

- 5.2 By Position Type

- 5.2.1 Front

- 5.2.2 Rear

- 5.3 By Sales Channel Type

- 5.3.1 Original Equipment Manufacturers (OEMs)

- 5.3.2 Aftermarket

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Commercial Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 South Korea

- 5.5.3.4 Japan

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the world

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Brembo SpA

- 6.2.2 ITT Inc.

- 6.2.3 Robert Bosch GmBH

- 6.2.4 Tenneco Inc.

- 6.2.5 Akebono Brake Industry Co. Ltd

- 6.2.6 ZF Friedrichshafen AG

- 6.2.7 Continental AG

- 6.2.8 Federal-Mogul Holdings LLC

- 6.2.9 BorgWarner Inc.

- 6.2.10 Nisshinbo Holdings Inc.

- 6.2.11 Garrett Motion Inc.