|

시장보고서

상품코드

1692494

비디오 인코더 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Video Encoder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

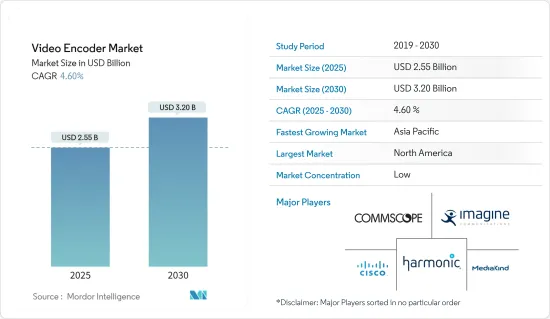

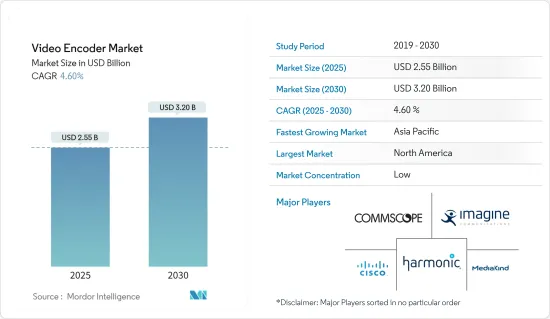

세계의 비디오 인코더 시장 규모는 2025년 25억 5,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 4.6%로 확대되어, 2030년에는 32억 달러에 달할 것으로 예측되고 있습니다.

주요 하이라이트

- 비디오 인코더 시장은 다양한 플랫폼에서의 고품질 비디오 스트리밍과 방송에 대한 수요가 높아짐에 따라 강력한 성장을 이루고 있습니다. 비디오 컨텐츠의 소비 증가, Over the Top(OTT) 서비스의 보급, 라이브 스트리밍 활동의 급증이 기여하고 있습니다.

- 기술의 진보는 비디오 엔코더 시장을 형성하는데 있어 매우 중요합니다.

- 게다가 인공지능(AI)과 머신러닝(ML)을 통합한 하드웨어 인코더의 개발은 중요한 동향을 나타내고 있습니다. 이 통합은 실시간 비디오 처리 능력을 향상시키고 네트워크 리소스를 최적화합니다.

- 게다가 Cisco Systems Inc., Harmonic Inc., Axis Communications AB (Canon Inc.) 등의 대기업이 비디오 인코더 시장을 선도하고 있습니다. 기업들은 시장에서의 지위를 강화하기 위해 합병, 인수, 제휴, 제품 발표 등의 전략을 적극적으로 추진하고 있습니다.

- 비디오 엔코더 시장은 큰 성장 기회와 함께 매우 유망한 전망을 보여줍니다. 연구개발을 우선하고 기술 변화에 신속하게 대응하는 기업은 새로운 동향을 활용하여 경쟁 우위를 유지하는데 유리한 입장에 있다고 생각됩니다.

- 비디오 엔코더 시장은 많은 성장 촉진요인이 풍부하지만, 하드웨어 비디오 엔코더와 관련된 고액의 초기 비용의 형태로 주목할만한 장애물이 떠오르고 있습니다. 원시 영상을 방송 및 스트리밍을 위한 디지털 형식으로 변환하는 데 중요한 이러한 장치는 종종 많은 양의 선행 투자가 필요합니다. 특히 중소기업이나 신흥기업에 있어서 이러한 금전적 지출은 큰 장애가 됩니다. 결과적인 고가의 비용은 잠재 고객이 새로운 기술을 도입하거나 기존 설정을 현대화하는 것을 생각해 버리고 시장 확대와 혁신을 방해할 수 있습니다. 또한 이러한 비용은 기업의 전반적인 투자 수익률에 직접 영향을 미칠 수 있으므로 제조업체가 비용 절감 방법을 검토하고 유연한 자금 조달 옵션을 제공함으로써 보다 광범위한 도입에 박차를 가하는 것이 중요합니다.

비디오 인코더 시장 동향

비디오 스트리밍 플랫폼의 보급이 시장 성장을 견인

- Netflix, Amazon Prime, YouTube 등의 동영상 스트리밍 서비스의 인기 상승으로 고품질의 저지연 스트리밍에 대한 욕구가 커지고 있습니다. 그 결과, 이러한 추세는 고급 비디오 인코더 수요를 견인하고 있습니다. 이 엔코더는 동영상을 효율적으로 압축하고 품질을 유지하며 특히 4K 및 8K와 같은 까다로운 해상도로 원활하게 시청할 수 있도록 지원합니다. Inplayer에 따르면 OTT 사용자 중 18.4%는 25-29세, 11.5%는 30-36세입니다. 주목해야 할 점은 OTT 사용자의 약 15%가 17세 이하라는 것입니다.

- 사용자가 제작한 컨텐츠와 전문 컨텐츠가 늘어나면서 스트리밍을 위한 비디오 제작이 붐비고 있습니다.

- 게다가 이벤트, 게임, 스포츠, 소셜 미디어에서의 라이브 스트리밍의 급증은 실시간 비디오 인코딩 솔루션의 필요성을 높이고, 비디오 엔코더 시장을 견인하고 있습니다.

- 또한 스마트폰, 태블릿, 스마트TV 동영상 스트리밍 이용의 급증은 적응형 비디오 인코딩의 필요성을 강조하고 있습니다.

아시아태평양이 최대 시장 점유율을 차지할 전망

- 중국의 지상파 디지털 TV 방송의 등장은 기존의 서비스를 개선하고 새로운 용도으로의 길을 열었습니다.

- 중국 정부도 사람들의 시청 체험을 향상시키고 있으며, 중국은 주요 도시에 지상파 HDTV 방송 컨텐츠의 무료 제공을 시작하도록 장려했습니다.

- Netflix, Amazon, Disney Hotstar와 같은 OTT 서비스가 오리지널 및 인수 컨텐츠에 투자함으로써 정액제 비디오 온 디맨드가 OTT 수입 전체의 93%를 차지하게 되어 2024년까지 30.7%로 증가, 인도에서는 27억 달러에 달할 전망입니다. 2024년 1월까지, YouTube는 4억 6,200만명의 유저를 매료해, 미국을 시청자수로 크게 이끌어, 인도의 주요한 동영상 플랫폼에 부상했습니다.

- 한국의 각 기업은 비디오 인코더 솔루션을 개발하여 방송과 스트리밍 시장을 견인하고 있습니다.

- 최근, 기술의 진보에 의해 하이비젼 텔레비전(HDTV)보다 고해상도의 4K영상을 녹화 및 표시할 수 있는 카메라, 디스플레이, 태블릿등의 기기가 급속하게 보급되고 있습니다. 하지만 방송이나 네트워크 전송으로 HD 영상을 전달하기 위한 차세대 영상 인코딩에 대한 기대가 높아지고 있습니다.

비디오 인코더 업계 개요

비디오 인코더 시장은 경쟁이 치열하고 Harmonic Inc., CommScope Holding Company Inc., MediaKind 등 대기업이 경쟁력을 유지하기 위해 지속적으로 능력을 강화하고 있습니다.

- 2024년 1월 볼류메트릭 비디오 기술의 주요 기업인 Arcturus사는 HoloSuite 툴셋 업데이트를 발표했습니다. Arcturus는 버추얼 프로덕션 팀뿐만 아니라 게임 개발자에게도 힘을 줍니다.

- 2023년 11월, 영상 및 음성 코덱 기술의 스페셜리스트인 MainConcept사는 OTT 및 TV 방송 워크플로우용의 리얼타임 인코딩 용도의 최신 버젼을 릴리스 하는 것을 발표했습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 비디오 코덱의 분석과 그 진화

- VVC 승인 기업 및 법인 기업 리스트

- VVC 규격에 공헌하고 있는 기업의 리스트

- COVID-19가 시장에 미치는 영향

- 업계의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 비디오 스트리밍 플랫폼의 인기 증가

- 하드웨어 엔코더와 비디오 카메라의 간편한 통합

- 클라우드 비디오 인코딩 기술이 수요를 견인

- 시장의 과제

- 하드웨어 비디오 인코더의 초기 비용 높이

제6장 시장 세분화

- 용도별

- 유료 TV

- 케이블 비디오 인코더

- 위성 비디오 인코더

- IPTV 비디오 인코더

- 방송 및 지상 디지털 TV(DTT)

- 공헌 비디오 및 엔코더

- 백홀 및 전송 비디오 엔코더

- DTT 비디오 인코더

- 보안 및 모니터링

- 유료 TV

- 지역별

- 아메리카

- 미국

- 캐나다

- 브라질

- 멕시코

- 기타 지역

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 폴란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 한국

- 일본

- 기타 아시아태평양

- 중동 및 아프리카

- 튀르키예

- 이스라엘

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아메리카

제7장 경쟁 구도

- 기업 프로파일

- Harmonic Inc.

- Commscope Holding Company Inc.

- MediaKind

- Cisco Systems Inc.

- Imagine Communications

- Z3 Technology

- ATEME

- Adtec Digital

- Telairity(VITEC)

- Axis Communications AB(Canon Inc.)

제8장 투자 분석

제9장 시장의 미래

JHS 25.05.15The Video Encoder Market size is estimated at USD 2.55 billion in 2025, and is expected to reach USD 3.20 billion by 2030, at a CAGR of 4.6% during the forecast period (2025-2030).

Key Highlights

- The video encoder market is witnessing strong growth, driven by the rising demand for high-quality video streaming and broadcasting across various platforms. Video encoders convert video signals into digital formats suitable for transmission over the Internet or other networks. This market's expansion is fueled by the increasing consumption of online video content, the proliferation of over-the-top (OTT) services, and the surge in live-streaming activities. The widespread adoption of social media platforms, where video content is a key engagement tool, further propels the demand for advanced video encoding solutions.

- Technological advancements are pivotal in shaping the video encoder market. Innovations in compression algorithms, such as H.265 (HEVC) and the emerging AV1 codec, enhance compression rates while maintaining video quality, facilitating efficient data transmission and storage. These advancements support the increasing demand for 4K and 8K video resolutions, which require significantly more bandwidth and storage capacity.

- Additionally, the development of hardware encoders that integrate artificial intelligence (AI) and machine learning (ML) represents a significant trend. These integrations improve real-time video processing capabilities and optimize network resources.

- Moreover, major players such as Cisco Systems Inc., Harmonic Inc., and Axis Communications AB (Canon Inc.) lead the pack in the video encoder market. Alongside these industry stalwarts, newer firms are making waves with innovative solutions. These players are actively pursuing strategies like mergers, acquisitions, partnerships, and product launches to bolster their market positions. Notably, many are forging strategic ties with OTT service providers and broadcasters, seeking to tap into synergies and broaden their customer reach.

- The video encoder market exhibits a highly promising outlook with significant growth opportunities. The ongoing evolution of video standards, the global deployment of 5G networks, and the increasing demand for immersive experiences, such as virtual reality (VR) and augmented reality (AR), are set to drive further innovations and applications. Companies prioritizing research and development and swiftly adapting to technological shifts will be well-positioned to capitalize on emerging trends and maintain their competitive advantage.

- While the video encoder market boasts numerous growth drivers, a notable hurdle emerges in the form of the steep initial costs associated with hardware video encoders. These devices, pivotal for transforming raw video into digital formats for broadcasting and streaming, often demand a significant upfront investment. This financial outlay can pose a formidable obstacle, especially for smaller enterprises and startups. The resulting high costs may dissuade potential customers from embracing new technologies or modernizing their existing setups, constraining market expansion and stifling innovation. Moreover, these expenses can directly impact a company's overall return on investment, underscoring the importance for manufacturers to explore cost-cutting measures or offer flexible financing options to spur wider adoption.

Video Encoder Market Trends

Increasing Popularity of Video Streaming Platforms is Expected to Drive the Market Growth

- The rising popularity of video streaming services such as Netflix, Amazon Prime, and YouTube has heightened the appetite for high-quality, low-latency streaming. Consequently, this trend drives the demand for advanced video encoders. These encoders are tasked with compressing videos efficiently, maintaining quality, and guaranteeing seamless viewing, especially at resolutions as demanding as 4K and 8K. According to Inplayer, among OTT users, 18.4% fall in the 25 - 29 age bracket, with 11.5% in the 30 - 36 range. Notably, approximately 15% of OTT users are under 17 years old.

- The rise of user-generated and professional content has led to a boom in video production for streaming. Consequently, there is a growing demand for efficient video encoding solutions. These solutions are crucial for increasing content volume, ensuring swift uploads, and seamless streaming experiences. This trend serves as a significant driver of the video encoder market.

- Moreover, the surge in live streaming across events, gaming, sports, and social media has heightened the need for real-time video encoding solutions, driving the video encoder market. Encoders that can process live content swiftly, ensuring minimal delays, are pivotal for delivering a smooth and engaging viewer experience.

- Also, the surge in smartphone, tablet, and smart TV usage for video streaming has underscored the necessity for adaptive video encoding. Encoders, pivotal for tailoring videos to diverse screen sizes and network speeds, are driving the video encoder market.

Asia-Pacific is Expected to Hold the Largest Market Share

- The advent of terrestrial digital television broadcasting in China has improved existing services and paved the way for new applications. The DTT broadcast standard enables wide-area fixed reception on HDTV and multiple SDTV programs. New services also include mobile, wearable, and high-speed applications.

- The Chinese government is also working to improve people's viewing experience, and China encouraged major cities to start offering free terrestrial HDTV broadcast content. This helps drive growth in the digital terrestrial market and the HDTV industry as a whole, including high-definition flat panels, chipsets, transmitters, software, and content creation.

- Investments by OTT services like Netflix, Amazon, and Disney+ Hotstar in original and acquired content will enable subscription video-on-demand to make up 93% of the total OTT revenue, increasing to 30.7% by 2024, amounting to USD 2.7 billion in India. By January 2024, YouTube emerged as the leading video platform in India, attracting 462 million users, significantly outpacing the United States in viewership.

- South Korean organizations are developing video encoder solutions to drive the broadcasting and streaming market. For example, KT Corp. is driving the pay TV services industry in South Korea regarding subscriptions and supervision, owing to its monopoly in the DTH segment and strong position in the IPTV segment, where it has the greatest share.

- In recent years, technological advances have led to the rapid spread of devices such as cameras, displays, and tablets that can record and display 4K video in higher resolution than high-definition televisions (HDTVs). With the proliferation of these devices, expectations are rising for next-generation video encoding for delivering HD video over broadcast and network delivery in Japan. 4K TVs are becoming increasingly popular in the home, and many models are available from major TV manufacturers.

Video Encoder Industry Overview

The video encoder market is highly competitive, with major players like Harmonic Inc., CommScope Holding Company Inc., and MediaKind continuously enhancing their capabilities to maintain a competitive edge. These companies strategically focus on product innovations, mergers, acquisitions, and partnerships to diversify their product portfolios and expand their global footprint.

- In January 2024, Arcturus, a key player in volumetric video technology, unveiled an update for its HoloSuite toolset. This update introduces a novel approach, enabling the seamless delivery of lightweight, scalable volumetric video to game engines. Arcturus empowers not just virtual production teams but also game developers. Users can now enrich their digital landscapes with more volumetric characters without compromising on data quality.

- In November 2023, MainConcept, a video and audio codec technology specialist, announced the release of the latest version of its real-time encoding application for OTT and TV broadcasting workflows. The new version, Live Encoder 3.4, supports VVC/H.266 and MPEG-5 LCEVC codecs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Analysis of Video Codecs and Their Evolution

- 4.3 List of VVC-approved and Incorporated Companies

- 4.4 List of Companies Contributing to the VVC Standard

- 4.5 Impact of COVID-19 on the Market

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Popularity of Video Streaming Platforms

- 5.1.2 Easy Integration of Hardware Encoders with Video Cameras

- 5.1.3 Cloud Video Encoding Technology to Drive the Demand

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Hardware Video Encoder

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Pay TV

- 6.1.1.1 Cable Video Encoder

- 6.1.1.2 Satellite Video Encoder

- 6.1.1.3 IPTV Video Encoder

- 6.1.2 Broadcast and Digital Terrestrial Television (DTT)

- 6.1.2.1 Contribution Video Encoder

- 6.1.2.2 Backhaul and Distribution Video Encoder

- 6.1.2.3 DTT Video Encoder

- 6.1.3 Security and Surveillance

- 6.1.1 Pay TV

- 6.2 By Geography

- 6.2.1 Americas

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.1.3 Brazil

- 6.2.1.4 Mexico

- 6.2.1.5 Rest of the Americas

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Russia

- 6.2.2.5 Poland

- 6.2.2.6 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 South Korea

- 6.2.3.4 Japan

- 6.2.3.5 Rest of Asia-Pacific

- 6.2.4 Middle East and Africa

- 6.2.4.1 Turkey

- 6.2.4.2 Israel

- 6.2.4.3 United Arab Emirates

- 6.2.4.4 Saudi Arabia

- 6.2.4.5 South Africa

- 6.2.4.6 Rest of Middle East and Africa

- 6.2.1 Americas

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Harmonic Inc.

- 7.1.2 Commscope Holding Company Inc.

- 7.1.3 MediaKind

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Imagine Communications

- 7.1.6 Z3 Technology

- 7.1.7 ATEME

- 7.1.8 Adtec Digital

- 7.1.9 Telairity (VITEC)

- 7.1.10 Axis Communications AB (Canon Inc.)