|

시장보고서

상품코드

1693710

유럽의 민간 항공기 객실용 조명 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Europe Commercial Aircraft Cabin Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

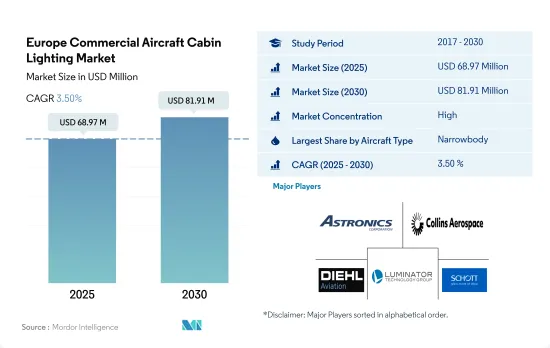

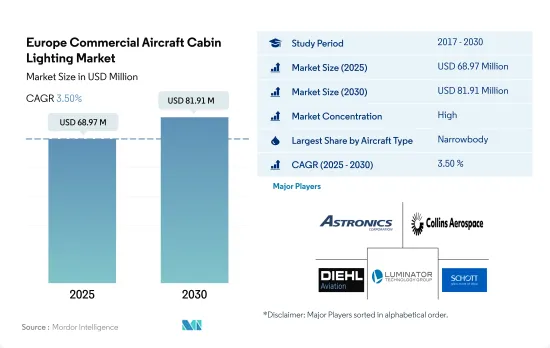

유럽의 민간 항공기 객실 조명 시장 규모는 2025년에 6,897만 달러, 2030년에는 8,191만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 3.50%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

이 지역에서는 협폭동체 항공기에 대한 수요 증가와 항공사의 부상으로 인해 경량화와 승객의 전반적인 경험을 개선하기 위해 정교한 LED 조명으로 전환하고 있습니다.

- 최신 세대의 항공기 좌석은 연료비를 절감하고 항공기의 지속가능성을 높이기 위해 가볍고 비금속 소재와 경량 설계로 만들어졌습니다. 와이드 바디 항공기에 비해 내로우 바디 항공기는 더 적극적인 성장률을 보일 수 있으며, 2017-2022년 내로우 바디 항공기는 전체 납품 대수의 대부분을 차지하며 전체의 82%를 차지했습니다.

- 또한, 이 지역의 항공사들은 성능, 신뢰성, 내구성, 내구성, 무게 측면에서 현재 기내 조명의 단점을 해소할 수 있는 고품질 LED 조명으로 전환하고 있습니다. 차세대 항공기에 LED 주변 조명(LED)이 널리 도입됨에 따라 일관된 서비스 품질을 유지하면서 객실 현대화 활동을 지속할 수 있게 되었습니다.

- 대부분의 항공사가 승객의 경험을 향상시키기 위해 혁신적인 객실 조명을 선택함에 따라 다양한 항공사가 주문하는 수많은 항공기가 시장을 주도할 것으로 예측됩니다. 로스텍항공, 라이언에어, 위드에어, 에어프랑스, 루프트한자, 튀르키예항공 등 주요 항공사들은 약 670대의 항공기를 주문했습니다. 이러한 대규모 항공기 발주는 예측 기간 동안 항공기 객실용 조명에 대한 수요를 증가시킬 것으로 예측됩니다.

- 기내 조명에 대한 수요를 견인하는 것은 편안함과 경험의 향상에 대한 관심이 증가하고 있기 때문입니다. 유지보수 비용을 절감하고 부피가 큰 기존 조명을 현대적이고 컴팩트한 LED 조명 솔루션으로 대체하기 위한 끊임없는 기술 혁신은 항공기 객실 조명 시장의 성장을 돕는 데 매우 중요합니다.

기내 조명 및 기타 첨단 기내 조명 제품의 첨단 기술 개발 및 도입은 유럽에서 항공기 조명 솔루션에 대한 수요를 크게 증가시키고 있습니다.

- LED 무드 조명, 인간 중심 조명, 기타 혁신적인 객실 조명 제품 등 새로운 기술의 혁신과 도입은 유럽에서 항공기 조명 시스템에 대한 수요를 크게 촉진하고 있습니다. 다양한 색상의 다양한 조명 옵션은 항공사와 항공기 제조업체가 항공 여행 중 고객의 기분과 경험을 향상시키고 시차적응을 완화하는 데 도움을 주고 있습니다.

- 이 지역에서는 LCC의 성공률이 높습니다. 에어프랑스, 영국항공, 루프트한자 등 이 지역의 주요 항공사들은 민간 항공기 시장의 전반적인 승객 경험을 개선하는 데 주력하고 있습니다. 이는 이 지역의 조명 시스템 등 민간 항공기 객실 인테리어에 대한 수요를 촉진하는 데 중요한 역할을 할 것으로 예측됩니다.

- 다양한 항공사가 발주하는 상당수의 항공기가 시장을 주도할 것으로 예측됩니다. 대부분의 유럽 항공사들은 이동 중 승객의 경험을 향상시키기 위해 최첨단 객실 조명을 활용하고 있습니다. 러시아 항공, 에어 라이언에어, 위즈 에어, 프랑스 에어프랑스, 독일 항공사, 튀르키예항공 등 유럽 주요 항공사들은 총 670대의 항공기를 주문했습니다. 브리티시 에어웨이즈, 에어로플로트 항공 등 다른 대형 항공사들도 항공기에 첨단 LED 무드 조명을 도입하고 있습니다. 협동체 및 와이드바디 항공기에 대한 막대한 항공기 주문과 더 나은 여행 경험을 위한 신기술 도입은 예측 기간 동안 항공기 객실 조명에 대한 수요를 창출할 것으로 예측됩니다.

유럽 민항기 객실 조명 시장 동향

항공 여행의 회복과 다양한 항공사의 항공기 대량 주문 등의 요인이 시장 성장을 가속하고 있습니다.

- 중국과 미국 간의 지속적인 정치적 긴장이 보잉에 영향을 미치고 있으며, 보잉은 현재 중국 고객을 위해 주문한 737 MAX 제트기의 일부를 재판매할 계획이며, 보잉은 중국 항공사가 더 이상 제트기를 주문하지 않아 어려운 상황에 직면해 있습니다. 중국 저우산에 위치한 보잉의 인도 센터는 준비가 완료되어 737 MAX의 인도를 재개할 예정입니다. 주산 공장은 연간 100대의 항공기를 수용할 수 있습니다.

- 에어버스는 2022년 상반기에 259대(442대)의 신규 순수주를 기록했고, 올해 누적 1,044대(1,080대)의 신규 순수주를 기록했으며, 2022년에는 820대(1,078대)의 신규 수주를 기록해 2021년 총 수주량보다 더 많은 수주를 기록했습니다. 2022년 에어버스는 보잉을 불과 46대 차이로 따돌리고 4년 연속 수주 왕좌를 차지했으며, 2021년 에어버스는 총 771대의 총 주문량을 기록했고, 264대의 취소로 총 507대의 순 신규 수주를 달성했습니다. 6월, Airbus는 12개의 고객사에 902대를 주문하고 2대의 A321neo를 취소했다고 보고했습니다.

- 누적 기준으로 보잉은 415대(총 527대)를 수주하여 작년 상반기 186대(총 286대)를 넘어섰으며, 2022년에는 774대(총 935대)를 수주하여 2021년 479대(총 909대)를 넘어섰으며, 2023년에는 774대(총 935대)를 수주할 것으로 예상하고 있습니다.년6월 현재 보잉은 9개 고객사로부터 총 304대의 제트기(총 주문량)를 예약했습니다. 그러나 보잉은 16대의 777X 취소를 보고했으며, 그 결과 288대의 순 신규 주문이 발생했습니다.

항공 여객 수송량 증가는 국내 및 국제 항공 여행 수요 증가에 의해 뒷받침될 것으로 예측됩니다.

- 2022년 유럽 각국의 여행 제한이 점차 완화됨에 따라 유럽 대륙 내 이동이 코로나19 사태 때보다 훨씬 쉬워졌습니다. 이로 인해 국제선 수요가 급증했고, 봉쇄 기간 동안 여행을 할 수 없었던 승객들은 국내에서 휴가를 보내는 대신 다시 해외로 떠나고 싶어했고, 2022년 유럽 전체 항공 승객 수는 13억 명에 달하고, 2021년 대비 8% 성장했습니다. 영국, 독일, 스페인은 유럽 전체 항공 여객 수송량의 36%를 차지하고 있어 향후 몇 년 동안 다른 유럽 국가에 비해 신형 항공기에 대한 더 많은 수요를 창출할 수 있습니다. 또한, 유럽 항공사는 전 세계 국제 항공 여객 수의 40%를 수송하고 있습니다.

- 2022년 1-6월 유럽 공항 이용객 수는 2021년 대비 247% 증가하여 유럽 대륙 전체에서 6억 6,000만 명의 승객이 증가하였습니다. 영국, 네덜란드, 튀르키예, 독일은 가장 이용객이 많은 공항을 보유하고 있으며 2022년 상반기 여객 수가 크게 증가했으며, 2022년 8월 유럽 상위 5개 공항의 여객 수송량은 68.1% 증가했지만, 주로 아시아 지역의 여행 제한이 지속되면서 전염병이 발생하기 전인 2019년 8월의 수준보다 17.5% 감소했습니다. 낮은 수준에 머물렀습니다. 다른 유럽 공항들도 2022년 8월에 비슷한 항공 여객 수송량 증가를 보였습니다. 우크라이나 공항의 상업용 항공 운송량은 감소했으며, 벨라루스와 러시아 공항에서도 러시아-우크라이나 전쟁이 시작된 이후 승객 수가 감소했으며, 2023-2030년 항공 여객 운송량은 국내 및 국제 항공 수요 증가로 인해 31% 급증할 것으로 예측됩니다.

유럽 민항기 객실 조명 산업 개요

유럽의 민간 항공기 객실 조명 시장은 상당히 통합되어 있으며, 상위 5개 기업이 90.56%를 점유하고 있습니다. 이 시장의 주요 기업은 Astronics Corporation, Collins Aerospace, Diehl Aerospace GmbH, Luminator Technology Group, SCHOTT Technical Glass Solutions GmbH 등입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 오퍼

제3장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 항공 여객 운송량

- 신규 항공기 납입수

- 1인당 GDP(현행 가격)

- 항공기 제조업체의 판매량

- 항공기 수주잔

- 수주 총액

- 공항 건설 지출(지속 중)

- 항공사 연료비

- 규제 프레임워크

- 밸류체인과 유통 채널 분석

제5장 시장 세분화

- 항공기 유형

- 네로우 보디

- 와이드 보디

- 국가별

- 프랑스

- 독일

- 스페인

- 튀르키예

- 영국

- 기타 유럽

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 개요

- Astronics Corporation

- Collins Aerospace

- Diehl Aerospace GmbH

- Luminator Technology Group

- Safran

- SCHOTT Technical Glass Solutions GmbH

- STG Aerospace

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고 문헌

- 도표

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Commercial Aircraft Cabin Lighting Market size is estimated at 68.97 million USD in 2025, and is expected to reach 81.91 million USD by 2030, growing at a CAGR of 3.50% during the forecast period (2025-2030).

The increasing demand for narrowbody aircraft and the emergence of airlines in the region are leading to a shift toward sophisticated LED lighting in order to reduce weight and improve the overall passenger experience

- Modern-generation aircraft seats are made from lightweight, non-metallic materials and lightweight designs to reduce fuel expenses and increase the aircraft's sustainability. Compared to widebody aircraft, narrowbody aircraft may witness a more aggressive growth rate. During 2017-2022, narrowbody aircraft recorded a majority of the deliveries, accounting for 82% of the total number of aircraft delivered.

- The region's airlines are also transitioning to high-quality LED lighting, as it eliminates many of the shortcomings of the current interior cabin lighting in terms of performance, dependability, durability, and weight. The widespread implementation of LED Ambient Lighting (LED) on next-generation aircraft has helped keep cabin modernization activities ongoing while maintaining consistent service quality.

- It is anticipated that the huge number of aircraft orders placed by various airlines will drive the market as most airlines are opting for innovative cabin lighting to enhance passengers' experience. Major airlines, such as Rostec, Ryanair, Wizz Air, Air France, Lufthansa, and Turkish Airlines, have ordered approximately 670 aircraft. Huge aircraft orders such as these are expected to boost the demand for aircraft cabin lighting during the forecast period.

- The rising emphasis on improving comfort and experience is driving the demand for aircraft cabin lighting. Constant innovations to reduce maintenance costs and replace traditionally bulky lighting with modern and compact LED lighting solutions are critical in aiding the growth of the aircraft cabin lighting market.

The development and implementation of cutting-edge technologies in cabin lighting and other advanced cabin lighting products are significantly increasing the need for aircraft lighting solutions in Europe

- The innovations and introduction of new technologies, such as LED mood lighting, human-centric lighting, and other innovative cabin lighting products, are significantly fueling the demand for aircraft lighting systems in Europe. A wide range of lighting options in several colors is aiding airlines and aircraft manufacturers in enhancing customers' moods and experiences during air travel and lessening jetlag.

- The success of LCCs is high in this region. Major airline companies in the region, such as Air France, British Airways, and Lufthansa, are focusing on improving the overall passenger experience in the commercial aircraft market. This is expected to play a vital role in aiding the demand for commercial aircraft cabin interior products such as lighting systems in the region.

- A considerable number of aircraft orders placed by various airlines is expected to drive the market. The majority of airlines in Europe are utilizing cutting-edge cabin lighting to improve the passenger experience while on the move. Major European carriers, such as Russian Airlines, Air Ryanair, and Wizz Air, as well as French Air France, German Airlines, and Turkey Airlines, have placed orders for a total of 670 aircraft. Some of the other major airlines, such as British Airways and Aeroflot, also implemented advanced LED mood lighting in their aircraft. Such huge aircraft orders for narrowbody and widebody aircraft and the implementation of new technologies for better travel experience are expected to create demand for aircraft cabin lighting during the forecast period.

Europe Commercial Aircraft Cabin Lighting Market Trends

Factors such as recovery in air travel and substantial aircraft orders being placed by various airlines are driving the growth of the market

- Ongoing political tensions between China and the United States have impacted Boeing, and it now plans to remarket some 737 MAX jets earmarked for Chinese customers. Boeing is facing a difficult situation as Chinese airlines are no longer ordering its jets. The Boeing delivery center in Zhoushan, China, is ready and is expected to resume delivery of 737 MAX aircraft. The Zhoushan plant can accommodate 100 aircraft annually.

- Year-to-date, Airbus accumulated 1,044 net new orders (1,080 gross orders), compared to 259 net new orders (442 gross orders) in the first half of 2022. In 2022, Airbus booked 820 net new orders (1,078 gross orders), surpassing both 2021 gross orders and net new orders. In 2022, Airbus won the orders crown for the fourth consecutive year by a fairly slim margin of just 46 aircraft compared to Boeing. In 2021, Airbus booked a total of 771 gross orders and received 264 cancellations, for a total of 507 net new orders. In June 2023, Airbus booked orders for a whopping 902 aircraft for 12 different customers and reported two A321neo cancellations, for a total of 900 net new orders.

- Year-to-date, Boeing accumulated 415 net new orders (527 gross orders), compared to 186 net new orders (286 gross orders) in the first six months of last year. In 2022, Boeing booked 774 net new orders (935 gross orders), up from 479 net new orders (909 gross orders) in 2021. As of June 2023, Boeing booked orders from nine customers for a total of 304 jets (gross orders). However, the company also reported 16 777X cancellations, resulting in 288 net new orders.

The growth in air passenger traffic is expected to be supported by the increasing demand for domestic and international air travel

- The gradual relaxation of travel restrictions in various European countries in 2022 made travel within the continent much easier than during the COVID-19 pandemic. Due to this trend, international demand soared, with passengers unable to travel during the lockdowns eager to fly abroad once again instead of taking domestic vacations. In 2022, air passenger traffic in the whole of Europe reached 1.3 billion, a growth of 8% compared to 2021. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in Europe and, hence, may generate more demand for new aircraft compared to other European countries over the coming years. European airlines have also been responsible for carrying almost 40% of global international air passengers.

- European airport traffic grew by 247% in the first six months of 2022 compared to 2021, resulting in an additional 660 million passengers handled across the continent. The United Kingdom, the Netherlands, Turkey, and Germany, which have some of the countries with the busiest airports, recorded a significant rise in passenger traffic in H1 2022. In August 2022, passenger traffic in the top five European airports increased by 68.1% but remained -17.5% below pre-pandemic August 2019 levels, mainly due to continued travel restrictions in Asia. A similar increase in air passenger traffic was observed at airports in the Rest of Europe in August 2022. Commercial air traffic declined from Ukrainian airports, and airports in Belarus and Russia recorded declining passenger volumes as well since the beginning of the Russia-Ukraine War. The air passenger traffic is expected to surge by 31% during 2023-2030, with increased demand in domestic and international aviation.

Europe Commercial Aircraft Cabin Lighting Industry Overview

The Europe Commercial Aircraft Cabin Lighting Market is fairly consolidated, with the top five companies occupying 90.56%. The major players in this market are Astronics Corporation, Collins Aerospace, Diehl Aerospace GmbH, Luminator Technology Group and SCHOTT Technical Glass Solutions GmbH (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Spain

- 5.2.4 Turkey

- 5.2.5 United Kingdom

- 5.2.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Astronics Corporation

- 6.4.2 Collins Aerospace

- 6.4.3 Diehl Aerospace GmbH

- 6.4.4 Luminator Technology Group

- 6.4.5 Safran

- 6.4.6 SCHOTT Technical Glass Solutions GmbH

- 6.4.7 STG Aerospace

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms