|

시장보고서

상품코드

1693714

중동의 민간 항공기 객실 조명 : 시장 점유율 분석, 산업 동향, 성장 동향 예측(2025-2030년)Middle East Commercial Aircraft Cabin Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

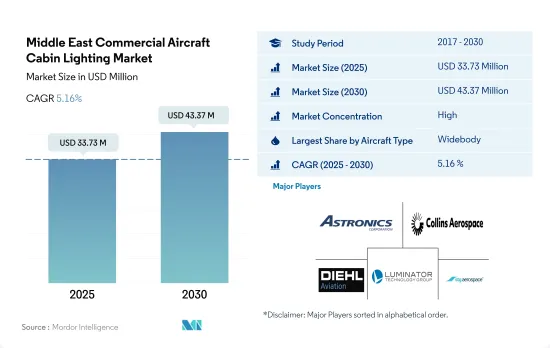

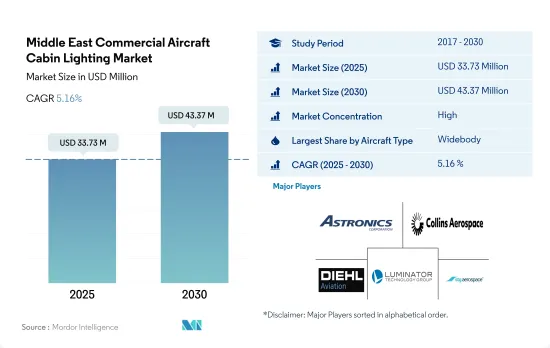

중동의 민간 항공기 객실 조명 시장 규모는 2025년에 3,373만 달러, 2030년에는 4,337만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 5.16%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

와이드바디 항공기 수요 증가와 승객의 여행 경험을 중시하는 항공사가 중동의 객실 조명 수요를 견인할 것으로 예측됩니다.

- 중동의 항공 산업은 관광객 증가, 경제 발전, 항공사의 항공기 확장 등의 요인으로 인해 수년 동안 꾸준히 성장하고 있습니다. 이 지역의 항공사들은 효율성, 신뢰성, 내구성, 내구성, 무게 측면에서 기존 기내 조명 시스템의 다양한 단점을 해결하는 데 도움이 되는 첨단 LED 조명 시스템으로 전환하고 있습니다. 다양한 OEM에 의한 LED 조명의 발전은 기존 기내 조명보다 더 빠릅니다. 또한, LED 기술은 탑승, 식사, 수면 및 기상 시 기내 분위기를 개선하고 승객의 기분을 개선하는 것으로 입증되었습니다. 중동 전체에서 와이드바디 부문의 납품이 압도적으로 많았으며, 2017-2022년 전체 납품의 52%를 차지했습니다.

- 항공기 객실 조명에 대한 수요는 주로 이 지역의 여러 항공사가 주문한 거대한 항공기 주문에 의해 주도되고 있으며, 2023년 9월 현재 이 지역의 여러 항공사가 약 777대의 항공기를 주문한 것으로 나타났습니다. 이 777기 중 협동체가 403대, 와이드바디가 374대입니다. 카타르항공, 에티하드항공, 에미레이트항공 등 이 지역의 주요 항공사들은 기내 조명 시스템 개선에 주력하고 있습니다.

- 또한, 사우디아라비아, 카타르, 아랍에미리트 등 주요 시장의 존재로 인해 2023-2030년에 약 944대의 항공기가 이 지역에 인도될 예정입니다. 이 지역의 다양한 항공기 증설 계획은 협동체 및 와이드바디 항공기 조달을 촉진할 것으로 예측됩니다. 이러한 요인들은 예측 기간 동안 민간 항공기 객실 조명 시장의 성장률을 8.30%까지 끌어올릴 것으로 예측됩니다.

아랍에미리트는 아랍에미리트 항공사의 대량 항공기 주문으로 인해 이 지역에서 더 큰 성장이 예상되고 있습니다.

- 항공사에게 고객 경험은 항상 최우선 순위입니다. 항공사는 승객에게 긍정적인 여행 경험을 제공하는 것이 중요합니다. 불만족스러운 고객이나 의욕이 없는 고객은 필연적으로 승객 수를 감소시키고 항공사의 이익을 감소시킵니다. 승객이 언제 여행하든 긍정적인 경험을 할 수 있도록 하는 것은 필수적입니다. 따라서 이 지역의 항공사들은 여행 중 완벽한 승객 경험을 정의하는 데 중요한 역할을 하는 새롭고 혁신적인 제품(예: 무드 조명)에 주목하고 있습니다.

- 또한, 이 지역의 항공기 객실 조명 시장 수요는 다양한 항공사가 항공기 교체 및 장거리 및 연비 효율이 높은 항공기의 필요성에 의해 주도되고 있습니다. 에어 아라비아, 에미레이트 항공, 에티하드 항공, 카타르 항공, 사우디아라비아, 리야드 항공, 플라이 두바이 등 주요 항공사들은 총 391대의 협동체 항공기와 413대의 와이드 바디 항공기를 주문했습니다. 이 중 에미레이트항공, 에티하드항공, 플라이두바이 등 아랍에미레이트의 주요 항공사들이 361대를 주문했습니다. 따라서 아랍에미리트는 대규모 항공기 수주에 힘입어 더 큰 성장을 이룰 것으로 예측됩니다. 이러한 주문 항공기는 예측 기간 동안 인도될 것으로 예상되며, 이러한 주문이 항공기 객실 조명 시장 수요를 견인할 것으로 예측됩니다.

- 또한 Boeing에 따르면, 중동은 향후 20년간 빠르게 성장하여 급증하는 여객 수송을 위해 약 3,400대의 제트기가 필요할 것으로 예측됩니다. 이러한 요인으로 인해 이 지역의 항공기 조명 시장 수요는 2023-2030년까지 9.08% 증가할 것으로 예측됩니다.

중동 민항기 객실 조명 시장 동향

항공 산업의 성장은 항공 여행 증가와 각 항공사의 대량 항공기 주문이 원동력이 되고 있습니다.

- Airbus와 Boeing은 세계 2대 상용기 제조업체입니다. 두 OEM은 2014년부터 2021년까지 총 주문량에서 비슷한 추세를 보이고 있으며, 2014년 Airbus는 1,796대, Boeing은 1,550대의 총 주문량을 기록하였습니다. 지난 기간 동안 2018년과 2021년을 제외한 대부분의 해에 Airbus의 총 주문량이 Boeing을 앞질렀습니다. 그러나 순수주에서는 2018년을 제외하고는 Airbus가 Boeing을 능가하는 결과를 보이고 있습니다.

- 2020년전염병으로 인해 여러 항공사가 주문을 취소했습니다. 2020 년에 Airbus는 115 건의 취소를 기록했지만 Boeing은 655 건의 주문을 취소 및 전환으로 잃었고 그 중 641 건은 737 MAX의 취소였습니다. 도 회계기준을 맞추기 위해 수주잔고에서 555대의 제트기를 삭제했습니다.

- 중국과 미국 간의 지속적인 정치적 긴장이 보잉에 영향을 미치고 있으며, 보잉은 현재 중국 고객을 위해 737MAX 제트기의 일부를 재판매할 예정입니다. 중국 항공사가 더 이상 제트기를 주문하지 않기 때문에 보잉은 어려운 상황에 직면해 있으며, 보잉은 정치적 상황이 개선될 때까지 필요하지 않은 주산 완성품 배송 센터에서 벗어나지 못하고 있습니다.

- 2022년, 전 세계 여행 규제 완화로 인해 항공사의 서비스 재개가 촉진되고, 기체 확장 계획이 재검토되었습니다. 보잉은 2022년 11월까지 총 685건의 주문을 받았으며, 114건의 취소와 571건의 신규 순주문으로 총 685건의 주문을 받았습니다. 마찬가지로 2022년 11월까지 에어버스는 1,062건의 총 주문과 237건의 취소, 825건의 순 신규 수주를 기록했습니다. 전 세계 항공사의 항공기 증설 계획으로 인해 양사의 수주는 더욱 증가할 것으로 보입니다.

지속적인 항공 여행의 성장은 중동의 항공 여객 수송량의 원동력입니다.

- 국제 여행객과 무역의 중계지로서 인기가 높은 중동은 비즈니스 및 레저 여행객의 출발지 및 목적지로서도 성장하고 있으며, 2020년 중동의 항공 여객 수송량은 코로나19 팬데믹으로 인한 여행 제한으로 64% 감소했습니다. 그러나 2022년에는 백신 접종률 상승과 휴가철 수요 증가로 인해 이 지역의 항공 여객 수송량은 3억 4,950만 명으로 2021년 대비 16%, 2019년 대비 45% 성장했습니다. 아랍에미리트와 사우디아라비아 등 주요 국가들이 전체 항공 여객 수송량의 42%를 차지하며 기타 중동 국가들에 비해 신형 항공기에 대한 높은 수요를 창출했습니다.

- 2022년 여객 수송능력은 2021년 대비 73.8% 증가했고, 여객 탑승률은 24.6% 증가한 75.8%를 기록했습니다. 이 지역의 항공 여행 회복세는 계속 탄력을 받고 있으며, 항공 여객 수송량은 향후 20년 내에 두 배로 늘어날 것으로 예측됩니다. 바레인, 쿠웨이트, 오만, 사우디아라비아, 아랍에미리트, 이라크, 이란, 요르단, 예멘, 카타르 등 중동의 주요 국제선 노선 중 상당수는 이미 코로나19 이전 수준을 넘어섰습니다. 이는 항공 여행이 회복세를 보이고 있으며, 계속해서 탄력을 받고 있음을 보여줍니다. 중동 내에서도 많은 주요 국제선 노선이 이미 코로나19 이전 수준을 넘어섰습니다. 높은 관광 및 여행 의욕은 중동 및 아프리카의 항공 산업 회복을 지속적으로 촉진하고 있으며, 2030년 항공 여객 수송량은 2022년 대비 34% 증가할 것으로 예측됩니다.

중동 민항기 객실 조명 산업 개요

중동의 민간 항공기 객실 조명 시장은 상당히 통합되어 있으며, 상위 5개 기업이 88.36%의 점유율을 차지하고 있습니다. 이 시장의 주요 기업은 Astronics Corporation, Collins Aerospace, Diehl Aerospace GmbH, Luminator Technology Group, STG Aerospace 등입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 오퍼

제3장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 항공 여객 운송량

- 신규 항공기 납입수

- 1인당 GDP(현행 가격)

- 항공기 제조업체의 판매량

- 항공기 수주잔고

- 수주 총액

- 공항 건설 지출(지속 중)

- 항공사 연료비

- 규제 프레임워크

- 밸류체인과 유통 채널 분석

제5장 시장 세분화

- 항공기 유형

- 내로우 바디

- 와이드 바디

- 국가별

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 개요

- Astronics Corporation

- Collins Aerospace

- Diehl Aerospace GmbH

- Luminator Technology Group

- SCHOTT Technical Glass Solutions GmbH

- STG Aerospace

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고 문헌

- 도표

- 주요 인사이트

- 데이터 팩

- 용어집

The Middle East Commercial Aircraft Cabin Lighting Market size is estimated at 33.73 million USD in 2025, and is expected to reach 43.37 million USD by 2030, growing at a CAGR of 5.16% during the forecast period (2025-2030).

Rising demand for widebody aircraft and airlines focusing on passenger travel experience is expected to drive the demand for cabin lighting in the Middle East

- The aviation industry in the Middle East has been steadily growing over the years, driven by factors such as increased tourism, economic development, and the expansion of airline fleets. Airlines in the region are moving toward advanced LED lighting systems as they help eliminate various drawbacks of the existing interior cabin lighting systems in terms of efficiency, reliability, durability, and weight. The advancements in LED lighting by various OEMs are more rapid than conventional aircraft cabin lighting. Additionally, LED technology has proved to improve passengers' moods by enhancing the cabin ambiance for boarding, eating, sleeping, and waking up. The widebody segment dominated the deliveries made across the Middle East, accounting for 52% of the total number of deliveries during 2017-2022.

- The demand for aircraft cabin lighting is driven primarily by huge aircraft orders that are being placed by various airlines in the region. As of September 2023, approximately 777 aircraft were placed by various airlines in the region. Of these 777 aircraft, narrowbody accounted for 403 aircraft, and widebody accounted for 374 aircraft. Major airlines in the region, such as Qatar Airways, Etihad, and Emirates, are focusing on improving their interior lighting systems.

- Furthermore, around 944 aircraft are scheduled to be delivered in the region due to the presence of major markets, such as Saudi Arabia, Qatar, and the United Arab Emirates, during 2023-2030. Various fleet expansion plans in the region are expected to boost the procurement of both narrowbody and widebody aircraft. These factors are expected to drive the growth of the commercial aircraft cabin lighting market during the forecast period by 8.30%.

UAE is expected to witness a larger growth in the region due to huge aircraft orders placed by the country's airlines

- Customer experience is always a top priority for airlines. It is important for airlines to offer passengers a positive travel experience. Dissatisfied or disengaged customers inevitably result in fewer passengers and reduced profits for airlines. It is vital for passengers to have a positive experience whenever they travel. Therefore, airlines in the region are focusing on new, innovative products (such as mood lighting) that play an important role in defining the complete passenger experience during their travel.

- Additionally, the demand for the aircraft cabin lighting market in the region is driven by aircraft orders that are being placed by various airlines as part of fleet renewal and the need for long-range, fuel-efficient aircraft. Some of the major airlines, such as Air Arabia, Emirates, Etihad, Qatar Airways, Saudia, Riyadh Air, and Flydubai, have ordered a total of 391 narrowbody and 413 widebody aircraft. Of these total aircraft ordered, UAE's top airlines, such as Emirates, Etihad, and Flydubai, have ordered 361 aircraft. Hence, the UAE is expected to witness larger growth driven by its huge aircraft orders. These ordered aircraft are expected to be delivered throughout the forecast period, and these orders are expected to drive the demand for aircraft cabin lighting market.

- Furthermore, according to Boeing, the Middle East is expected to expand enormously over the next 20 years, requiring a fleet of around 3,400 jets to serve fast-growing passenger traffic. Factors such as these are expected to drive the demand in the region's aircraft lighting market by 9.08% from 2023 to 2030.

Middle East Commercial Aircraft Cabin Lighting Market Trends

The aviation industry's growth is driven by the rising air travel and the high volume of aircraft orders placed by various airlines

- Airbus and Boeing are the two leading commercial aircraft manufacturers worldwide. Both OEMs have shown a similar trend in terms of gross orders between 2014 and 2021. In 2014, Airbus recorded a gross order of 1,796 aircraft, while Boeing recorded 1,550 aircraft. In the historical period, Airbus' gross orders have been higher than Boeing's in most years except in 2018 and 2021. However, in terms of net orders, Airbus has shown better results than Boeing, except in 2018.

- The pandemic in 2020 resulted in several airlines canceling their orders. In 2020, Airbus recorded 115 cancellations, while Boeing lost 655 orders to cancellations and conversions, of which 641 were 737MAX cancelations. Boeing also removed 555 jets from its backlog to align with accounting standards.

- Ongoing political tensions between China and the United States have impacted Boeing, and it now plans to remarket some 737 MAX jets earmarked for Chinese customers. Boeing is facing a difficult situation as Chinese airlines no longer order jets. Boeing is stuck with a completion and delivery center in Zhoushan that it does not need until the political situation improves.

- In 2022, the ease in the global travel restrictions aided airlines in resuming their services and reconsidering fleet expansion plans. The demand for new aircraft increased and was reflected in the net orders. From 2022 until November, Boeing booked 685 gross orders and received 114 cancellations for 571 net new orders. Similarly, until November 2022, Airbus booked 1,062 gross orders and received 237 cancellations for 825 net new orders. The fleet expansion plans of airlines globally will further improve the net orders of both manufacturers.

Consistent growth in air travel is the driving factor for air passenger traffic in the Middle East

- The Middle East, a popular connection point for international travelers and trade, is also growing as a starting point and destination for business and leisure passengers. In 2020, air passenger traffic in the Middle East dropped by 64% due to travel restrictions caused by the COVID-19 pandemic. However, in 2022, due to the rising vaccination rates and strong demand over the holiday season, air passenger traffic in the region reached 349.5 million, a growth of 16% compared to 2021, while the growth was at 45% compared to 2019. Major countries, such as the United Arab Emirates and Saudi Arabia, accounted for 42% of the total air passenger traffic, generating higher demand for new aircraft compared to other Middle Eastern countries.

- In 2022, passenger capacity increased by 73.8%, and passenger load factor grew by 24.6% to 75.8% compared to 2021. Air travel recovery in the region continues to gather momentum, and air passenger traffic is expected to double within the next 20 years. Many major Middle Eastern international route areas in Bahrain, Kuwait, Oman, Saudi Arabia, the United Arab Emirates, Iraq, Iran, Jordan, Yemen, and Qatar are already exceeding pre-COVID-19 levels. Such factors indicate that air travel has recovered and continues to gather momentum. Many major international routes, even within the Middle East, are already exceeding pre-COVID-19 levels. Tourism and the high willingness to travel continue to foster the industry's recovery in the Middle East & Africa. The air passenger traffic levels are expected to grow by 34% in 2030 compared to 2022.

Middle East Commercial Aircraft Cabin Lighting Industry Overview

The Middle East Commercial Aircraft Cabin Lighting Market is fairly consolidated, with the top five companies occupying 88.36%. The major players in this market are Astronics Corporation, Collins Aerospace, Diehl Aerospace GmbH, Luminator Technology Group and STG Aerospace (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Country

- 5.2.1 Saudi Arabia

- 5.2.2 United Arab Emirates

- 5.2.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Astronics Corporation

- 6.4.2 Collins Aerospace

- 6.4.3 Diehl Aerospace GmbH

- 6.4.4 Luminator Technology Group

- 6.4.5 SCHOTT Technical Glass Solutions GmbH

- 6.4.6 STG Aerospace

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms