|

시장보고서

상품코드

1842532

접착 붕대 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Adhesive Bandages - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

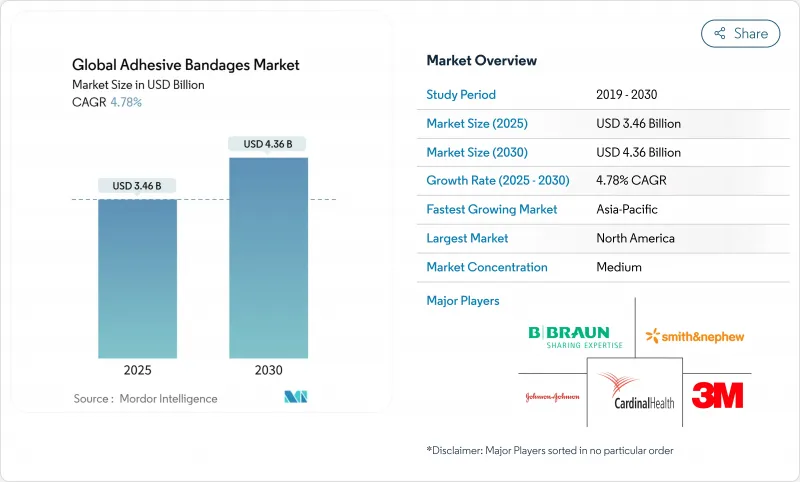

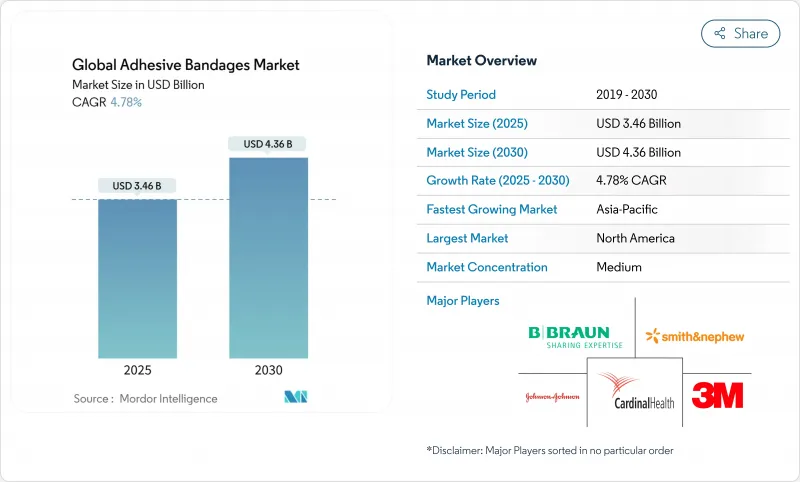

접착 붕대 시장 규모는 2025년에 34억 6,000만 달러로 평가되었고, 2030년에 43억 6,000만 달러에 이를것으로 예측되며, CAGR 4.78%로 성장할 전망입니다.

의료 시스템이 만성 상처 치료 비용 증가에 직면하면서 수요는 안정적으로 유지되고 있으며, 이로 인해 메디케어는 매년 281-317억 달러의 비용을 지출하고 있습니다. 약제 함유 제품이 현재 판매량 선두를 유지하는 한편, 디지털 헬스 통합으로 온도, pH, 수분을 기록하는 센서 장착 드레싱의 채택이 촉진되고 있습니다. 통기성, 방수성, 생분해성 소재의 병행 발전은 비의약성 제품군의 경쟁력을 유지시키며, 친환경 포장 및 휘발성 유기 화합물(VOC) 감소를 의무화하는 정책 움직임을 반영합니다. 전자상거래 플랫폼은 시장 진출 모델을 재편하며 가정 간호 중심의 소형 패키지 채택을 촉진하고, 북미는 강력한 보험 적용 및 스마트 붕대 승인을 가속화하는 명확한 규제 환경으로 선두를 유지합니다. 스마트 붕대 혁신 기업들이 표준 드레싱 대비 병원 치료 비용을 41% 절감하고 적용 시간을 61% 단축할 수 있습니다고 주장하면서 경쟁 압박이 심화되고 있습니다.

세계의 접착 붕대 시장 동향 및 인사이트

증가하는 수술 절차 및 외상 관련 부상

외래 및 통원 진료 센터가 무균 장벽을 유지하고 조기 퇴원을 가능하게 하는 장기간 착용 드레싱에 의존함에 따라 수술 건수 증가가 접착 붕대 시장을 견인하고 있습니다. 전미대학체육협회(NCAA) 조사에 따르면 대학 스포츠 부상의 50% 이상이 하지 외상으로, 정밀 운동용 스트립에 대한 지속적인 수요를 보여줍니다. 최소 침습적 수술 기법은 이차적 고정이 필요 없는 삼출물 관리용 얇고 유연성이 뛰어난 필름을 선호합니다. 기판층에 은 나노입자를 포함시키는 것은 수술 부위 감염 예방 목표를 지원하며, 이는 지불 기관에게 점점 더 중요한 품질 지표입니다.

만성 상처 및 당뇨성 궤양 발생률 증가

미국에서는 매년 670만 명이 만성 상처로 고통받으며, 직접 치료 비용만 500억 달러를 초과합니다. 당뇨병성 족부 궤양만으로도 연간 메디케어 지출이 62-69억 달러에 달합니다. 캘텍의 iCares 플랫폼과 같은 스마트 드레싱은 일산화질소 및 과산화수소 바이오마커를 실시간으로 분석하고 머신러닝 알고리즘을 통해 치유 경로를 예측합니다. 원자재 공급 부족에도 불구하고 하이드로콜로이드 매트릭스는 만성 상처 치료 분야에서 여전히 우위를 점하고 있으며, 자가 치유 클레이 나노시트를 적용한 하이드로겔 구조체는 4시간 이내 최대 90%의 구조적 회복을 약속합니다.

라텍스/PU에 대한 피부 자극 및 알레르기 반응

피부염 우려로 인해 정보에 민감한 소비자들의 제품 수용도가 낮아지고 있습니다. 2024년 제기된 집단 소송은 특정 반다이드 제품군에 퍼플루오로알킬 물질이 함유되어 있습니다고 주장하며, 유색인종 대상 제품의 건강 형평성 문제를 제기했습니다. 라텍스 알레르기는 일반 인구의 최대 6%에 영향을 미쳐 저알레르기성 실리콘 및 폴리우레탄 혼합재로 생산자를 유도하지만, 통기성과 비용 측면에서 상충점이 발생합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 증가하는 스포츠 부상 및 활동적인 라이프스타일 수요

- 가정용 응급처치 및 전자상거래 소형 패키지 급증

- 스마트 센서 탑재 붕대의 등장

- 고급 상처 봉합 솔루션의 경쟁

부문 분석

2024년 접착 붕대 시장 규모에서 의약용 제품이 54.35%를 차지했으며, 이는 병원 감염 예방 요구사항을 충족하는 내장형 항균제 덕분입니다. 은 나노입자 및 PHMB 매트릭스는 황색포도상구균에 대해 98.5%의 박테리아 제거율을 기록하여 임상적 신뢰도를 강화합니다. 저외상성 실리콘 코팅은 노인 및 소아 피부를 보호하며, 응집성 직물은 고강도 운동 부상에 적합합니다. 감염 예방 효과가 보상 트렌드에 부합함에 따라 제조사들은 가격 방어를 위한 증거 확보를 강화하고 있습니다.

비의약용 스트립은 현재 매출 규모는 작지만, 지속 가능한 PLA 및 무용제 접착제가 규제 탄소 목표와 부합하며 5.63% CAGR로 성장 중입니다. 탄성 천과 방수 PE 필름은 통기성과 수중 안전성을 중시하는 소비자 선호를 충족시킵니다. 소매업체들은 온라인 매장을 통해 대용량 패키지를 홍보하며, 선택적 의료 구매가 확산되는 신흥 경제권에서의 접근성을 확대하고 있습니다. 이러한 추세로 인해 접착 붕대 시장은 가격대별로 확고한 다각화를 유지하고 있습니다.

지역별 분석

북미는 2024년 글로벌 매출의 42.81%를 차지하며 1인당 지출 규모 확대, 엄격한 보험급여 제도, 스마트 센서 기술의 조기 도입을 통해 시장 주도권을 공고히 했습니다. 만성 상처 치료로 미국 의료 시스템은 연간 500억 달러 이상의 비용을 지출하며, 이로 인해 프리미엄 드레싱에 대한 지속적인 수요가 발생하고 있습니다. 캐나다는 만성 질환 관리에 무선 반창고를 통합하는 전국적 디지털 헬스 시범 사업을 지원하고 있으며, 멕시코는 지역 공급망을 단축하는 제조 허브를 확장하고 있습니다.

아시아태평양 지역은 2030년까지 7.42%의 가장 빠른 연평균 성장률(CAGR)을 기록할 전망입니다. 중국은 당뇨병 유병률 증가에 따라 대규모 수출 역량과 국내 소비 증가를 동시에 확보하고 있습니다. 일본의 초고령 인구 구조는 취약한 피부에 적합한 무손상 하이드로겔 제품의 수요를 촉진하며, 인도의 ‘아유슈만 바라트’ 정책 하 병원 확장은 농촌 지역 시장 침투를 가속화하고 있습니다. 지역 조달은 CE 인증 또는 미국 FDA 승인 제품을 점점 더 선호하여 다국적 기업들이 현지 조립에 투자하도록 유도하고 있습니다.

유럽은 의료기기 규정(EU 2017/745) 하에서 안정적인 확장을 보이며, 이는 임상 증거 및 추적성 의무를 강화합니다. 지속가능성 인센티브로 생분해성 기질이 장려되며, 바이어스도르프는 2024년 ‘로이코플라스트’ 라인에서 플라스틱 프리 패치를 출시해 6.5%의 유기적 성장을 기록했습니다. 독일, 영국, 프랑스가 수요를 주도하는 가운데 동유럽 시장은 EU 구조기금을 통해 접근성을 개선 중입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 증가하는 수술 절차 및 외상 관련 부상

- 만성 상처 및 당뇨병성 궤양 발생률 증가

- 증가하는 스포츠 부상 및 활동적인 라이프스타일 수요

- 통기성 및 방수 소재의 기술 발전

- 가정용 응급처치 및 전자상거래 소형 패키지 급증

- 스마트 센서 탑재 붕대의 등장

- 시장 성장 억제요인

- 라텍스/폴리우레탄에 대한 피부 자극 및 알레르기 반응

- 첨단 상처 봉합 솔루션의 경쟁

- 지속가능성 규제로 인한 고비용 생체재료 사용 증가

- 원자재 공급 변동성(면, 하이드로콜로이드)

- 가치 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 약용 붕대

- 접착성 직물 붕대

- 유연 고정 붕대

- 하이드로콜로이드 접착 붕대

- 항균(은/PHMB) 붕대

- 실리콘 기반 저외상 붕대

- 비약용 붕대

- 접착 붕대

- 유연 고정 붕대

- 방수 PE/PVC 스트립

- 탄성 천 스트립

- 생분해성 PLA 스트립

- 약용 붕대

- 용도별

- 상처 관리

- 급성(외과적 및 외상성)

- 만성(당뇨병성, 압박성, 정맥성 궤양)

- 정형외과 서포트

- 통증 관리(진통 패치)

- 스포츠 및 운동용 랩

- 응급 처치 및 재택 케어

- 수의학용

- 상처 관리

- 최종 사용자별

- 병원 및 진료소

- 외래수술센터(ASC)

- 재택 의료

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- 3M

- Johnson & Johnson

- Beiersdorf AG

- Cardinal Health

- Smith & Nephew plc

- B. Braun Melsungen AG

- Medline Industries LP

- ConvaTec Group plc

- Molnlycke Health Care

- Paul Hartmann AG

- BSN medical(Essity)

- Nitto Denko Corp.

- Dynarex Corporation

- Detectaplast NV

- Avery Dennison Medical

- DermaRite Industries

- Lohmann & Rauscher

- Winner Medical Group

- Nichiban Co., Ltd.

- Henkel AG(Loctite Medical)

제7장 시장 기회와 전망

HBR 25.10.29The adhesive bandages market size reached USD 3.46 billion in 2025 and is forecast to attain USD 4.36 billion by 2030, advancing at a 4.78% CAGR.

Demand holds steady as healthcare systems confront the rising costs of chronic wound care, which drain Medicare of USD 28.1 billion-USD 31.7 billion each year. Medicated formats sustain current volume leadership, while digital health convergence spurs adoption of sensor-enabled dressings that record temperature, pH, and moisture. Parallel advances in breathable, waterproof, and biodegradable materials keep non-medicated lines competitively relevant, reflecting policy moves that mandate greener packaging and reduced volatile organic compounds. E-commerce platforms reshuffle go-to-market models, driving rapid uptake of home-care-oriented micro-packs, and North America preserves its lead because of robust reimbursement and regulatory clarity that accelerates smart-bandage approvals. Competitive pressure intensifies as smart-bandage innovators claim they can trim hospital therapy costs by 41% and reduce application time 61% relative to standard dressings.

Global Adhesive Bandages Market Trends and Insights

Growing Surgical Procedures & Trauma-Related Injuries

Expanding surgical volumes boost the adhesive bandages market as outpatient and ambulatory centers rely on extended-wear dressings that preserve sterile barriers and enable early discharge. National Collegiate Athletic Association surveillance shows lower-extremity trauma represents more than 50% of collegiate injuries, underscoring sustained demand for precision athletic strips . Minimally invasive techniques favor thin, highly conformable films that manage exudate without secondary fixation. Incorporating silver nanoparticles within substrate layers supports surgical-site infection prevention goals, an increasingly critical quality metric for payers.

Rising Incidence of Chronic Wounds & Diabetic Ulcers

In the United States, 6.7 million individuals face chronic wounds each year, with direct treatment costs topping USD 50 billion. Diabetic foot ulcers alone trigger USD 6.2 billion-USD 6.9 billion in annual Medicare spending. Smart dressings such as Caltech's iCares platform analyze nitric oxide and hydrogen peroxide biomarkers in real time and predict healing trajectories via machine-learning algorithms. Hydrocolloid matrices retain dominance in chronic settings despite raw-material supply squeezes, while hydrogel constructs with self-healing clay nanosheets promise up to 90% structural recovery within 4 hours.

Skin Irritation & Allergic Reactions to Latex/PU

Dermatitis concerns narrow product acceptance among increasingly informed consumers. A class-action suit filed in 2024 claims certain Band-Aid lines contain per- and polyfluoroalkyl substances, raising health-equity issues for products marketed to people of color. Latex allergies affect up to 6% of the general population, pushing producers toward hypoallergenic silicone and polyurethane blends, but trade-offs emerge around breathability and cost.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Sports Injuries & Active Lifestyle Demand

- Surge in Home First-Aid & E-Commerce Micro-Packs

- Emergence of Smart Sensor-Enabled Bandages

- Competition From Advanced Wound-Closure Solutions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medicated variants controlled 54.35% of adhesive bandages market size in 2024 courtesy of embedded antimicrobials that answer hospital-acquired infection mandates. Silver nanoparticle and PHMB matrices log 98.5% bacterial elimination against Staphylococcus aureus, reinforcing clinical trust. Low-trauma silicone coatings protect geriatric and pediatric skin, while cohesive fabrics suit high-motion athletic injuries. As reimbursement trends reward infection-prevention proof points, producers escalate evidence generation to defend pricing.

Non-medicated strips, although smaller in revenue today, expand at a 5.63% CAGR as sustainable PLA and solvent-free adhesives dovetail with regulatory carbon targets. Elastic cloth and waterproof PE films satisfy consumer preference for breathable and aquatic-safe dressings. Retailers promote value packs through online storefronts, widening access across emerging economies where discretionary healthcare buys gain traction. Such momentum keeps the adhesive bandages market firmly diversified across price tiers.

Adhesive Bandages Market is Segmented by Product Type (Medicated Bandages and Non-Medicated Bandages), Application (Wound Management, Orthopedic Support, and More), End User (Hospitals/Clinics, Ambulatory Centers, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.81% of global revenue in 2024, cementing leadership through high per-capita spend, rigorous reimbursement, and early adoption of smart sensor technologies. Chronic wounds cost the United States healthcare system more than USD 50 billion annually, driving continuous demand for premium dressings. Canada funds nationwide digital-health pilots that integrate wireless bandages into chronic-disease management, while Mexico expands manufacturing corridors that shorten regional supply chains.

Asia-Pacific produces the fastest 7.42% CAGR through 2030. China combines large-scale export capacity with rising domestic consumption as diabetes prevalence climbs. Japan's super-aged demographic spurs uptake of atraumatic hydrogels suited for fragile skin, and India's hospital build-out under Ayushman Bharat pushes rural penetration. Regional procurement increasingly favors CE-marked or US-FDA-cleared products, prompting multinationals to invest in localized assembly.

Europe shows stable expansion under Medical Device Regulation (EU 2017/745), which tightens clinical-evidence and traceability obligations . Sustainability incentives encourage biodegradable substrates; Beiersdorf registered 6.5% organic growth in 2024 by launching plastic-free patches under its Leukoplast line. Germany, the United Kingdom, and France anchor demand, while Eastern European markets improve access via EU structural funds.

- 3M

- Johnson & Johnson

- Beiersdorf

- Cardinal Health

- Smiths Group

- B. Braun

- Medline Industries

- ConvaTec Group plc

- Molnlycke Health Care

- Hartmann Group

- BSN medical (Essity)

- Nitto Denko Corp.

- Dynarex

- Detectaplast NV

- Avery Dennison Medical

- DermaRite Industries

- Lohmann & Rauscher

- Winner Medical Group

- Nichiban Co., Ltd.

- Henkel AG (Loctite Medical)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Surgical Procedures & Trauma-Related Injuries

- 4.2.2 Rising Incidence Of Chronic Wounds & Diabetic Ulcers

- 4.2.3 Increasing Sports Injuries & Active Lifestyle Demand

- 4.2.4 Technological Advances In Breathable & Waterproof Materials

- 4.2.5 Surge In Home First-Aid & E-Commerce Micro-Packs

- 4.2.6 Emergence Of Smart Sensor-Enabled Bandages

- 4.3 Market Restraints

- 4.3.1 Skin Irritation & Allergic Reactions To Latex/Pu

- 4.3.2 Competition From Advanced Wound-Closure Solutions

- 4.3.3 Sustainability Regulations Pushing Costlier Bio-Materials

- 4.3.4 Raw-Material Supply Volatility (Cotton, Hydrocolloid)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Medicated Bandages

- 5.1.1.1 Cohesive Fabric Bandages

- 5.1.1.2 Flexible Fixation Bandages

- 5.1.1.3 Hydrocolloid Adhesive Bandages

- 5.1.1.4 Antimicrobial (Silver/PHMB) Bandages

- 5.1.1.5 Silicone-based Low-Trauma Bandages

- 5.1.2 Non-Medicated Bandages

- 5.1.2.1 Cohesive Fabric Bandages

- 5.1.2.2 Flexible Fixation Bandages

- 5.1.2.3 Waterproof PE/PVC Strips

- 5.1.2.4 Elastic Cloth Strips

- 5.1.2.5 Biodegradable PLA Strips

- 5.1.1 Medicated Bandages

- 5.2 By Application

- 5.2.1 Wound Management

- 5.2.1.1 Acute (Surgical & Traumatic)

- 5.2.1.2 Chronic (Diabetic, Pressure, Venous Ulcers)

- 5.2.2 Orthopedic Support

- 5.2.3 Pain Management (Analgesic patches)

- 5.2.4 Sports & Athletic Wraps

- 5.2.5 First-Aid & Home Care

- 5.2.6 Veterinary Use

- 5.2.1 Wound Management

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Home Healthcare

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 3M

- 6.3.2 Johnson & Johnson

- 6.3.3 Beiersdorf AG

- 6.3.4 Cardinal Health

- 6.3.5 Smith & Nephew plc

- 6.3.6 B. Braun Melsungen AG

- 6.3.7 Medline Industries LP

- 6.3.8 ConvaTec Group plc

- 6.3.9 Molnlycke Health Care

- 6.3.10 Paul Hartmann AG

- 6.3.11 BSN medical (Essity)

- 6.3.12 Nitto Denko Corp.

- 6.3.13 Dynarex Corporation

- 6.3.14 Detectaplast NV

- 6.3.15 Avery Dennison Medical

- 6.3.16 DermaRite Industries

- 6.3.17 Lohmann & Rauscher

- 6.3.18 Winner Medical Group

- 6.3.19 Nichiban Co., Ltd.

- 6.3.20 Henkel AG (Loctite Medical)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment