|

시장보고서

상품코드

1842545

뉴로포토닉스 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Neurophotonics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

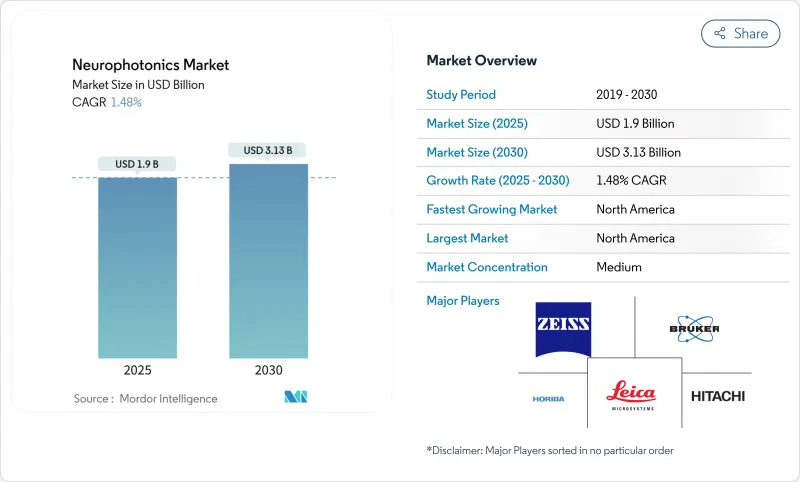

뉴로포토닉스 시장은 2025년에 19억 달러로 추정되고, 2030년에는 31억 3,000만 달러에 이를 전망이며, CAGR 10.48%로 성장할 것으로 예측됩니다.

심부 조직 광학 이미징, 인공지능 대응 데이터 분석, 저침습 뇌 인터페이스에서의 급속한 진보가 이 기술의 임상적 관련성을 넓혀가고 있습니다. 미국 BRAIN Initiative나 일본의 Moonshot Goal 1과 같은 프로그램을 통한 정부 자금으로 연구실에서의 발견이 상업 플랫폼으로 꾸준히 이행하고 있습니다. 벤처 투자자의 자본 유입과 선도적인 광학 장비 제조업체의 전략적 인수는 기술 혁신의 파이프라인을 강화하고 제품 개발주기를 단축합니다. 북미는 학술센터, 의료기기 규제 당국, 상환 관계자의 통합 에코시스템을 통해 주도적 지위를 유지하고, 아시아태평양은 일본의 세계 포토닉스 제조 거점과 중국과 인도의 연구개발비 증가를 배경으로 가속화하고 있습니다.

세계의 뉴로포토닉스 시장 동향 및 인사이트

신경 질환의 유병률 상승

신경 퇴행성 질환과 정신 질환은 세계적인 평균 수명의 성장과 함께 사회적, 경제적 부담을 증대시키고 있습니다. 5,500만 명 이상이 알츠하이머병을 앓고 있으며, 발병률은 고령화 사회에서 계속 상승하고 있습니다. 기능적 근적외선 분광법(fNIRS)과 광학 바이오 모듈레이션 기술은 기존의 자기 공명 영상법으로 비용이 불가능했던 실시간 뇌 산소 농도 데이터를 제공합니다. 캘리포니아 대학교 샌프란시스코에서 실시한 임상 연구는 근적외선 치료 후 Mini Mental State Exam의 점수가 현저하게 향상된 것으로 보고되어 빛에 의한 개입의 임상적 의의가 높아지고 있습니다. 병원은 인지 재활의 진행 상황을 모니터링하기 위해 이 기술을 채택하고 장비 제조업체는 외래 환자 환경에 적합한 사용하기 쉬운 시스템에 중점을 둡니다. 보급이 확대됨에 따라 뉴로포토닉스 시장은 진단과 치료 워크플로에서 지속적인 수요를 끌어내고 있습니다.

브레인 매핑 연구개발에 대한 정부 자금 확대

미국 BRAIN 이니셔티브는 특히 비변성 2광자 현미경과 같은 광신경 인터페이스 혁신을 목표로 한 다년간 보조금을 계상하고 있습니다. 유럽과 아시아태평양의 유사한 자금 지원 프레임 워크는 연구소, 장비 제조업체 및 임상 센터를 공유 컨소시엄에 참여시켜 기술 성숙을 가속화하고 있습니다. 일본 문샷 목표 1은 2025년 5억 2,000만 달러 상당의 국내 신경기술 부문을 예측하고 있으며, 장기적인 정책 헌신을 보여줍니다. 이러한 프로그램은 고위험 프로젝트를 맡고, 테스트 생산 라인을 조성하며, 재현성을 가속화하는 오픈 액세스 데이터 리포지토리를 만듭니다. 공공 부문의 지원은 이에 맞는 민간 투자를 불러들여 신흥 기업이 엄청난 희석을 받지 않고 프로토타입을 규제 등급 시스템으로 확장할 수 있게 합니다. 보조금이 기초 과학에서 트랜스레이셔널 이정표로 전환함에 따라, 업계 기업들은 더 빠른 상업적 이익을 얻고 뉴로포토닉스 시장의 상승 궤도를 강화합니다.

성인의 피질 이미징에서 제한된 투과 심도

성인의 뇌 조직에서는 빛이 산란하기 때문에 2광자 및 3광자 모달리티는 약 2-3mm의 깊이의 표층으로 한정됩니다. 파킨슨병이나 난치성 간질에 관여하는 피질하 타겟은 여전히 도달할 수 없기 때문에 임상의사는 심부뇌전극이나 고자장 MRI 등의 대체 모달리티를 채용할 수밖에 없습니다. 포토닉스의 보고에 따르면 400mW를 초과하는 누적 광 조사는 열 손상을 일으켜 촬영 시간을 제한합니다. 이 문제를 완화하기 위해 연구자들은 파면 성형 광학계와 테라 헤르츠 광 자극을 연구하고 있지만 상업적 준비는 아직 몇 년 앞에 있습니다. 한편, 깊이 제한은 하이엔드 이미징 벤더에게 당면 수익의 가능성을 좁히고 있습니다.

부문 분석

현미경 플랫폼은 2024년에 뉴로포토닉스 시장 점유율의 45.67%를 차지하였고, 회로 레벨 시각화의 주력 모달리티로서의 역할을 굳혔습니다. ZEISS FLUOVIEW FV4000MPE와 Bruker OptoVolt 모듈은 고속 공진 스캐너와 적응 광학계가 밀리 스케일 필드에서 서브 미크론 해상도를 제공한다는 것을 보여줍니다. 보다 미세한 구조적 인사이트에 대한 수요는 특히 신경과학의 최고 연구 기관의 핵심 이미징 시설에서 건전한 업그레이드 사이클을 지원합니다. 분광계는 휴대용 하드웨어로 기능적 혈행동태 매핑을 수행함으로써 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 11.25%를 기록할 전망입니다. 형광 수명 이미징과 라만 분광법을 융합시킨 멀티모달 구성은 화합물과 뇌의 상호작용 프로파일을 종합적으로 요구하는 제약기업의 고객을 끌어들인다. 공급업체는 GPU 가속 알고리즘을 통합하여 거의 즉시 부피 재구성을 수행하여 연구자가 획득 후 처리에 소비하는 시간을 절약합니다. 지속적인 혁신은 트랜스레이셔널 프로젝트 증가와 함께 현미경 하위 카테고리를 보다 광범위한 뉴로포토닉스 시장의 중심으로 삼고 있습니다.

spectroscopy solution의 뉴로포토닉스 시장 규모는 병원이 뇌졸중의 트리아지에 침대 옆에 fNIRS를 도입함에 따라 급증하고 있습니다. 취득 소프트웨어에 내장된 인공지능 분류기는 3초 이내에 허혈 동향에 플래그를 지정하여 즉시 개입을 안내합니다. 하마마츠 포토닉스의 NKT 포토닉스 인수에 의해 초고속 레이저 공급망이 확보되고, 라이카 마이크로시스템즈는 인스코픽스와 판매 계약을 맺으며, 세포 해상도의 미니스코프 키트를 공동 판매합니다. Microscopy Metadata Working Group과 같은 컨소시엄은 3D 이미지 메타데이터의 표준 표준을 확정하고 세계 코호트 연구의 데이터 풀을 촉진합니다. 이러한 움직임을 종합하면 신규 연구 그룹의 진입 장벽이 낮아지고 뉴로포토닉스 시장에서 현미경의 이점이 강화됩니다.

지역 분석

북미는 연방 정부의 풍부한 자금 풀과 퍼스트 인 휴먼 연구를 가속화하는 투명한 규제 패스웨이를 통해 2024년 세계 매출의 42.64%를 창출했습니다. 2024년에 Precision Neuroscience와 ClearPoint Neuro에 부여된 FDA의 획기적인 디바이스 지정은 혁신적인 플랫폼에 대한 신속한 검토를 보여줍니다. 수술 중 형광 지침에 대한 호의적인 상환 정책은이 지역 수요를 더욱 견고하게 만듭니다. 보스턴, 샌프란시스코, 토론토를 둘러싼 풍부한 벤처 캐피탈 생태계는 기업가의 재능을 끌어들여 초기 상업 출시 위험을 완화합니다. 그러나 장비 가격 상승과 가치 기반 관리의 의무화로 인해 공급자는 자본 예산을 보호하기 위해 견고한 의료 경제 자료를 개발할 필요가 있습니다.

아시아태평양의 CAGR은 가장 빠른 13.21%이며 공급망이 성숙함에 따라 북미 점유율이 떨어질 전망입니다. 일본은 180개 이상의 제조업체를 통해 세계 포토닉스 생산량의 약 30%를 유지하고 있으며, 국내 디바이스 어셈블러의 재료비를 삭감하는 스케일 메리트를 창출하고 있습니다. 중국의 지방 정부는 뉴로테크놀로지 파크에 자금을 제공하고, 클래스Ⅱ의 의료기기에 신속한 등록을 제공함으로써 시장 투입까지의 타임라인을 단축하고 있습니다. 인도의 의료용 전자기기에 대한 생산 연동 장려금 제도는 부품 제조업체를 유치하여 초기 수출 허브를 형성하고 있습니다. 호주 신경과학센터와의 국경을 넘어 학술 제휴는 트랜스레이셔널 프로토타입을 만들어 지역의 전문지식을 넓혀줍니다.

유럽에서는 확립된 연구 대학과 결속력 있는 데이터 프라이버시법이 다시설 공동시험을 촉진하고 균형 잡힌 경관을 유지하고 있습니다. 독일은 산학 공동 작업 그룹을 통해 옵토제네틱스의 표준화를 추진하고 영국은 뇌졸중 후속 케어에서 fNIRS 인지 기능 평가의 상환 경로를 시험적으로 도입하고 있습니다. 아시아 비용 경쟁에 직면한 현지 제조업체는 워크플로우 통합 및 수명 주기 지원을 중시한 프리미엄 서비스 모델로 축족을 옮깁니다. EU 의료기기 규제 하에서 규제 조정은 문서화 오버헤드를 증가시키지만 제품 품질에 대한 기대를 조화시켜 뉴로포토닉스 공급업체에게 유럽 내 유통을 원활하게 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신경질환의 유병률 상승

- 브레인 매핑의 연구개발에 대한 정부 자금 확대

- 광 뉴로 이미징 디바이스의 소형화 및 휴대성

- 옵토제네틱스 및 Fnirs의 아카데믹 랩에 대한 급속한 도입

- 몰입형 Xr 및 Bci 플랫폼과의 통합

- 신생아 및 주술기 모니터링의 이용 사례 증가

- 시장 성장 억제요인

- 성인의 피질 이미징에서 한정된 보급 심도

- 다광자 플랫폼의 높은 설비 투자 및 옥스

- 벤더 간 데이터 포맷의 상호 운용성의 부족

- 장기간의 연구에서 광독성 및 조직 가열의 위험

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 시스템 유형별

- 현미경

- 분광법

- 멀티모달 플랫폼

- 기타 시스템 유형

- 용도별

- 연구

- 진단

- 치료

- 최종 사용자별

- 학술기관 및 연구기관

- 병원 및 클리닉

- 제약 및 바이오테크놀러지 기업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Carl Zeiss AG

- Leica Microsystems

- Hamamatsu Photonics

- Bruker Corporation

- Artinis Medical Systems

- Horiba Ltd.

- Hitachi Ltd.

- Femtonics Ltd.

- Inscopix Inc.

- Cairn Research

- fNIR Devices LLC

- HemoPhotonics

- Thorlabs Inc.

- PicoQuant GmbH

- NKT Photonics

- Intelligent Imaging Innovations

- NeuroLight Technologies

- Luxmux Technologies

- Photometrics

- Neuronix Imaging

제7장 시장 기회 및 전망

AJY 25.10.29The neurophotonics market stands at USD 1.90 billion in 2025 and is forecast to reach USD 3.13 billion by 2030, advancing at a 10.48% CAGR.

Rapid progress in deep-tissue optical imaging, artificial-intelligence-enabled data analytics, and minimally invasive brain interfaces is widening the technology's clinical relevance. Government funding through programs such as the United States BRAIN Initiative and Japan's Moonshot Goal 1 fuels a steady flow of laboratory discoveries that migrate into commercial platforms. Capital inflows from venture investors and strategic acquisitions by large optical equipment makers strengthen the innovation pipeline and shorten product-development cycles. North America keeps its leadership position through an integrated ecosystem of academic centers, medical-device regulators, and reimbursement stakeholders, while Asia-Pacific accelerates on the back of Japan's global photonics manufacturing footprint and rising R&D outlays in China and India.

Global Neurophotonics Market Trends and Insights

Rising Prevalence of Neurological Disorders

Neurodegenerative and psychiatric conditions impose growing social and economic burdens as global life expectancy rises. More than 55 million individuals live with Alzheimer's disease, and incidence continues to rise in aging populations. Functional near-infrared spectroscopy (fNIRS) and photobiomodulation techniques provide real-time cerebral oxygenation data that conventional magnetic resonance imaging cannot deliver cost-effectively . Clinical studies at the University of California San Francisco reported notable gains in Mini Mental State Exam scores following near-infrared light therapy, strengthening the clinical case for optical interventions. Hospitals adopt the technology to monitor cognitive rehabilitation progress, while device makers focus on user-friendly systems suited for outpatient environments. As prevalence expands, the neurophotonics market draws sustained demand from both diagnostic and therapeutic workflows.

Expanding Government Funding for Brain-Mapping R&D

The United States BRAIN Initiative earmarks multiyear grants specifically targeting optical neural-interface innovations such as non-degenerate two-photon microscopy. Similar funding frameworks in Europe and Asia-Pacific bring research labs, device makers, and clinical centers into shared consortia, accelerating technology maturation. Japan's Moonshot Goal 1 forecasts a domestic neurotechnology sector worth USD 520 million in 2025, signaling long-term policy commitment. These programs underwrite high-risk projects, subsidize pilot manufacturing lines, and create open-access data repositories that speed reproducibility. Public-sector support draws matching private investment, allowing startups to scale prototypes into regulatory grade systems without prohibitive dilution. As grants transition from basic science to translational milestones, industry players capture earlier commercial payoffs, reinforcing the upward trajectory of the neurophotonics market.

Limited Penetration Depth in Adult Cortical Imaging

Light scatters in adult brain tissue, restricting two-photon and three-photon modalities to superficial layers roughly 2-3 mm deep. Subcortical targets involved in Parkinson's disease or refractory epilepsy remain out of reach, compelling clinicians to adopt alternative modalities such as deep-brain electrodes or high-field MRI. Extended illumination elevates tissue temperature; PhotoniX reports that cumulative light exposure above 400 mW causes thermal damage, capping imaging duration. To mitigate the issue, researchers explore wavefront-shaping optics and terahertz-photon stimulation, yet commercial readiness sits several years away. Meanwhile, the depth limitation curtails immediate revenue potential for high-end imaging vendors.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization and Portability of Optical Neuro-Imaging Devices

- Rapid Adoption of Optogenetics and fNIRS in Academic Labs

- Integration with Immersive XR and BCI Platforms

- Growth of Neonatal and Peri-Operative Monitoring Use Cases

- High CAPEX and OPEX of Multiphoton Platforms

- Lack of Data-Format Interoperability Across Vendors

- Phototoxicity and Tissue-Heating Risks in Long-Duration Studies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Microscopy platforms accounted for 45.67% of neurophotonics market share in 2024, consolidating their role as the workhorse modality for circuit-level visualization. The ZEISS FLUOVIEW FV4000MPE and Bruker OptoVolt modules exemplify how fast resonant scanners and adaptive optics yield sub-micron resolution over millimeter-scale fields. Demand for ever finer structural insight sustains a healthy upgrade cycle, especially within core imaging facilities at top neuroscience institutes. Spectroscopy systems record the fastest 11.25% CAGR to 2030 by tackling functional hemodynamic mapping with portable hardware. Multimodal configurations that fuse fluorescence lifetime imaging with Raman spectroscopy attract pharmaceutical customers seeking comprehensive compound-brain interaction profiles. Vendors integrate GPU-accelerated algorithms to deliver near-instantaneous volumetric reconstructions, saving researchers hours of post-acquisition processing. Sustained innovation coupled with rising translational projects keeps the microscopy sub-category at the spine of the broader neurophotonics market.

The neurophotonics market size for spectroscopy solutions is set to rise sharply as hospitals deploy bedside fNIRS for stroke triage. Artificial-intelligence classifiers embedded in acquisition software flag ischemic trends in under three seconds, guiding immediate intervention. Corporate activity intensifies; Hamamatsu's acquisition of NKT Photonics secures an ultrafast-laser supply chain, while Leica Microsystems formalizes a distribution pact with Inscopix to co-market cellular-resolution miniscope kits. Consortia such as the Microscopy Metadata Working Group finalize 3D-imaging metadata standards, promoting data pooling across global cohort studies. Collectively, these moves lower barriers to entry for new research groups, reinforcing microscopy's pre-eminent place in the neurophotonics market.

The Global Neurophotonics Market is Segmented by System Type (Microscopy, Spectroscopy, and More) Application (Research, Diagnostics, and Therapeutics), End User (Academic & Research Institutes, Hospitals & Clinics, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.64% of global revenue in 2024 thanks to deep federal funding pools and a transparent regulatory pathway that accelerates first-in-human studies. The FDA's breakthrough-device designation awarded to Precision Neuroscience and ClearPoint Neuro in 2024 exemplifies swift review for transformative platforms. Favorable reimbursement policies for intraoperative fluorescence guidance further solidify regional demand. Rich venture-capital ecosystems surrounding Boston, San Francisco, and Toronto attract entrepreneurial talent and de-risk early commercial launches. However, high equipment prices and value-based-care mandates compel suppliers to develop robust health-economic dossiers to defend capital budgets.

Asia-Pacific posted the fastest 13.21% CAGR and is poised to erode North American share as local supply chains mature. Japan maintains roughly 30% of global photonics output through more than 180 manufacturers, creating economies of scale that cut bill-of-materials cost for domestic device assemblers. Chinese provincial governments fund neurotechnology parks and offer expedited registrations for Class II medical devices, shortening go-to-market timelines. India's Production-Linked Incentive scheme for medical electronics lures component fabricators, shaping a nascent export hub. Cross-border academic partnerships with Australian neuroscience centers generate translational prototypes, broadening regional expertise.

Europe holds a balanced landscape where established research universities and cohesive data-privacy laws foster collaborative multi-site trials. Germany champions optogenetics standardization through joint industry-academia working groups, while the United Kingdom pilots reimbursement pathways for fNIRS cognitive assessments in stroke follow-up care. Local manufacturers, facing Asian cost competition, pivot to premium service models that emphasize workflow integration and lifecycle support. Regulatory alignment under the EU Medical Device Regulation introduces additional documentation overhead, but also harmonizes product quality expectations, smoothing intra-European distribution for neurophotonics suppliers.

- Carl Zeiss

- Danaher

- Hamamatsu Photonics

- Bruker

- Artinis Medical Systems

- HORIBA

- Hitachi

- Femtonics Ltd.

- Inscopix Inc.

- Cairn Research

- fNIR Devices

- HemoPhotonics

- Thorlabs

- PicoQuant GmbH

- NKT Photonics

- Intelligent Imaging Innovations

- NeuroLight Technologies

- Luxmux Technologies

- Photometrics

- Neuronix Imaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Neurological Disorders

- 4.2.2 Expanding Government Funding For Brain-Mapping R&D

- 4.2.3 Miniaturization & Portability Of Optical Neuro-Imaging Devices

- 4.2.4 Rapid Adoption Of Optogenetics & Fnirs In Academic Labs

- 4.2.5 Integration With Immersive Xr & Bci Platforms

- 4.2.6 Growth Of Neonatal/Peri-Operative Monitoring Use-Cases

- 4.3 Market Restraints

- 4.3.1 Limited Penetration Depth In Adult Cortical Imaging

- 4.3.2 High Capex & Opex Of Multiphoton Platforms

- 4.3.3 Lack Of Data-Format Interoperability Across Vendors

- 4.3.4 Phototoxicity & Tissue-Heating Risks In Long-Duration Studies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By System Type

- 5.1.1 Microscopy

- 5.1.2 Spectroscopy

- 5.1.3 Multimodal Platforms

- 5.1.4 Other System Types

- 5.2 By Application

- 5.2.1 Research

- 5.2.2 Diagnostics

- 5.2.3 Therapeutics

- 5.3 By End-user

- 5.3.1 Academic & Research Institutes

- 5.3.2 Hospitals & Clinics

- 5.3.3 Pharma & Biotech Companies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Carl Zeiss AG

- 6.3.2 Leica Microsystems

- 6.3.3 Hamamatsu Photonics

- 6.3.4 Bruker Corporation

- 6.3.5 Artinis Medical Systems

- 6.3.6 Horiba Ltd.

- 6.3.7 Hitachi Ltd.

- 6.3.8 Femtonics Ltd.

- 6.3.9 Inscopix Inc.

- 6.3.10 Cairn Research

- 6.3.11 fNIR Devices LLC

- 6.3.12 HemoPhotonics

- 6.3.13 Thorlabs Inc.

- 6.3.14 PicoQuant GmbH

- 6.3.15 NKT Photonics

- 6.3.16 Intelligent Imaging Innovations

- 6.3.17 NeuroLight Technologies

- 6.3.18 Luxmux Technologies

- 6.3.19 Photometrics

- 6.3.20 Neuronix Imaging

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment