|

시장보고서

상품코드

1842662

종합적 대사 패널 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Comprehensive Metabolic Panel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

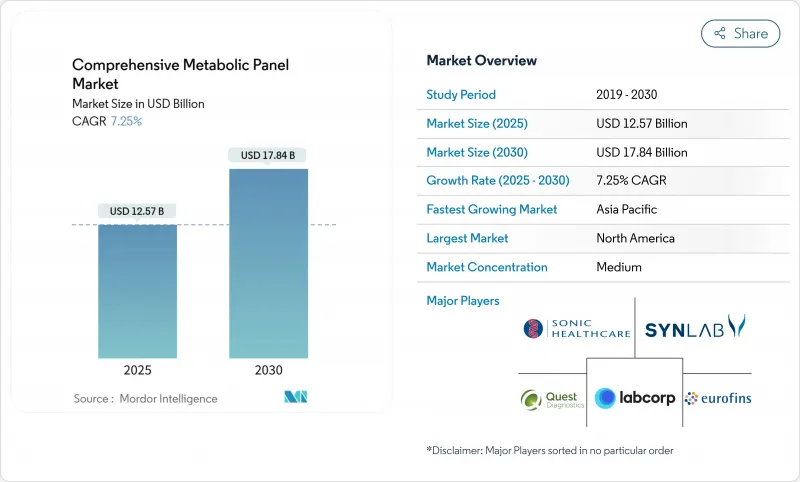

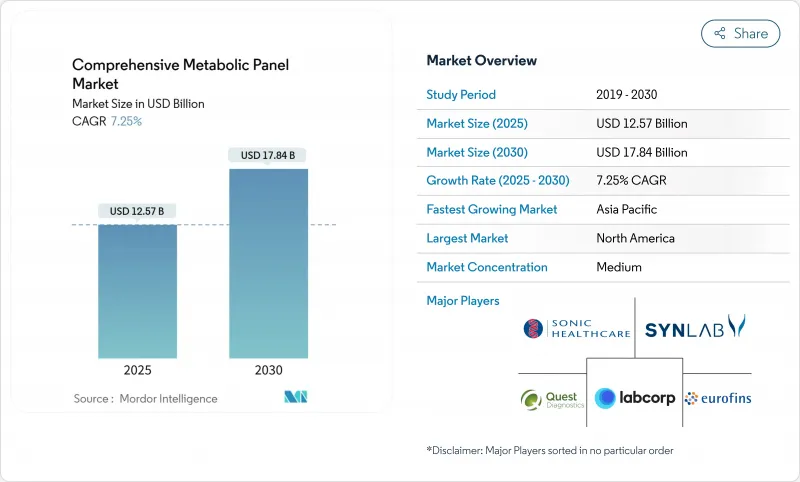

종합적 대사 패널 시장의 2025년 시장 규모는 125억 7,000만 달러로, 2030년에는 178억 4,000만 달러에 이르고, CAGR 7.25%를 나타낼 것으로 예측됩니다.

새로운 예방 의료 정책, 당뇨병, 신장, 간 질환 부담 확대, POC(Point of Care) 진단 네트워크의 확대가 지속적인 수요의 기반이 되고 있습니다. 병원은 FDA의 2024년 임상 검사(LDT) 규칙을 충족하기 위해 화학 워크플로우를 자동화하고, 독립적인 실험실은 새로운 품질 시스템 의무를 준수하기 위해 높은 처리량 시스템을 도입했습니다. AI를 활용한 분석은 표준 애드온이 되고 있어, 수작업에 의한 리뷰의 비율을 줄이고, 루틴 패널을 의사결정 지원 자산으로 바꾸고 있습니다. 실험실 등급 결과를 몇 분 안에 제공하는 POC 화학 분석 장치는 검사량을 추구하여 핵심 실험실과 직접 경쟁하게 되며 조달 패턴이 재구성되었습니다.

세계의 종합적 대사 패널 시장 동향과 인사이트

예방검진에 대한 의식의 고조

고용주가 후원하는 웰니스 이니셔티브 증가로 연간 1회의 대사 패널이 표준화되고 있습니다. 생체 인식 스크리닝 프로그램은 직원의 건강 관리 비용을 1인당 월 24.25달러로 줄여 참가자의 16%에서 숨겨진 위험을 발견했습니다. 정부도 예방진단에 보조금을 내고 있으며 메디케어는 2025년 만성질환 관리에 사용되는 대사 패널의 상환을 확대했습니다. 캐나다와 독일은 침묵 신장병을 강조하는 매스미디어 캠페인을 개발하여 위험한 성인을 정기적인 화학 검사로 안내합니다. 현재, 약국은 예방 접종에 대사 검사를 번들하여 소비자의 접근을 넓히고 있습니다. 이와 같은 노력은 패널이 단발적인 케어에서 정기적인 케어로 이행하여 검사량이 증가하고 종합적 대사 패널 시장 전체의 시약 수요가 안정됩니다.

만성 신장 질환, 간 질환, 당뇨병 환자의 세계 부담 증가

당뇨병 환자는 2050년까지 13억 1,000만 명에 달할 것으로 예측되며 장기적인 대사 모니터링 수요가 예상됩니다. 만성신장병(CKD)은 이미 세계 6억 7,300만 명이 앓고 있으며, 2형 당뇨병이 CKD 관련 사망의 주요 원인이 되고 있습니다. 중국에서는 성인 당뇨병 유병률이 2023년 13.7%에 달했으며 개입 없이는 두배가 될 수 있습니다. 이러한 통계를 통해 지불자는 조기 발견과 위험 계층화를 위한 일상적인 CMP를 상환해야 합니다. 대사기능 장애와 관련된 지방간이 임상적으로 인지됨에 따라 CMP에 통합된 간기능 마커는 더욱 중요해지고 있습니다. 따라서 장기적인 역학적 압력은 종합적 대사 패널 시장 예측 CAGR을 1.8포인트 상승시킵니다.

공인 임상 화학자 및 임상 검사 기사 부족

미국의 임상검사 포지션의 46% 가까이가 공석이며, 2만 6,000명 수요에 대해 매년 5,000명밖에 신졸자가 입사하고 있습니다. 2025년 1월부터 시행되는 CLIA의 새로운 인사규칙에서는 보다 높은 교육 자격과 감독 로테이션이 요구되어 응모자층이 좁아집니다. 캐나다와 서유럽의 일부도 비슷한 적자에 직면하고 있으며, 잔업대가 부피가 커지고 납기가 길어지고 있습니다. 인적 부족은 검사실이 변화를 늘릴 수 없기 때문에 기기의 도입을 늦추고 종합적 대사 패널 시장의 추정 CAGR을 1.4% 저하시킵니다.

부문 분석

신장 기능 검사는 2024년 종합적 대사 패널 시장의 31.52%를 차지했으며, 1차 케어에서 CKD 스크리닝 의무화에 지원되었습니다. 한편, 포도당 검사는 당뇨병 프로그램이 모든 CMP에 공복 글루코오스와 HbA1c를 포함하고 있기 때문에 CAGR 9.65%를 나타내 가장 급속히 확대하고 있습니다. 단백질 검사는 알부민의 상태가 수술의 위험 점수에서 중요성을 증가함에 따라 꾸준히 성장하며, 전해질 패널은 여전히 중요한 치료의 치료에 필수적입니다. 간 기능 검사는 신진 대사 기능 장애와 관련된 지방 간 질환의 유병률이 증가하는 동안 다시 주목 받고 있습니다.

지속 포도당 모니터링의 동향은 모세관 샘플링과 중앙 실험실의 정밀도를 융합시킨 새로운 시료 채취 제품에 박차를 가하고 있습니다. Labcorp사의 가정용 포도당 리스크 측정기는 정맥 채혈과의 일치율 97%를 달성하여 소비자에게 직접 판매를 확대했습니다. Roche의 Elecsys PRO-C3는 고급 바이오 마커를 활용하여 간 섬유증의 병기 분류를보다 정확하게 수행합니다. 포도당 패널에 통합된 AI 알고리즘은 조기 혈당 변동을 신고하여 개인화된 관리 계획을 가능하게 합니다. 이러한 진보를 총칭하면 새로운 수익 창출에서 포도당 검사의 리더십이 강화되어 디지털 건강 관련 분석의 종합적 대사 패널 시장 규모가 확대됩니다.

지역 분석

북미는 2024년 종합적 대사 패널 시장 수익의 36.82%를 차지했는데, 이는 루틴 검사를 조성하는 고급 보험 적용과 고용자의 웰니스 프로그램 때문입니다. 미국은 주요 병원 네트워크에서 AI의 시험적 도입으로 혜택을 받았으며 캐나다는 인플루엔자 예방 접종을 받을 때 대사 검사를 권장하는 공중 보건 캠페인을 활용했습니다. 멕시코의 연방 의료 개혁은 지역 클리닉에서 POC 채용을 가속화했습니다. 2024년 FDA의 LDT 규칙은 선행 컴플라이언스 비용을 증가시켰지만 투자자의 신뢰를 높이는 명확한 승인 경로를 형성했습니다.

유럽은 각국의 의료제도가 CMP를 만성질환관리 프로토콜에 통합하고 있기 때문에 여전히 2위의 공헌국입니다. 독일, 영국, 프랑스는 화학 플랫폼을 인공지능 대응으로 업그레이드했으며, 스페인과 이탈리아는 자가 채취 파트너십을 시험적으로 도입했습니다. EU IVDR은 문서화 요건을 끌어올려 소규모 실험실을 전략적 제휴와 아웃소싱으로 향하게 했습니다. NHS 영국의 장기 계획은 지역 의료 허브에서 POC 화학 검사를 추진하고 검사의 분산을 촉진합니다. 동유럽 국가는 EU의 통합 기금을 통해 실험실을 현대화하고 화학-면역측정 통합 플랫폼을 수입합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 9.62%를 나타낼 전망입니다. 중국에서는 당뇨병 유병률이 급상승하고 있으며 건강 중국 2030 전략에 따른 전국적인 CMP 스크리닝 캠페인이 추진됩니다. 일본과 한국은 기술자 부족에 대처하기 위해 AI 지원에 의한 자동화를 채용하고, 호주는 POC 기기를 마이 헬스 레코드에 링크시켜 실시간으로 데이터를 집계합니다. 인도의 진단 약부문은 민간 체인의 검사실 네트워크 확대에 의해 CAGR 8-9%를 나타낼 전망입니다. 동남아시아 국가들은 원격지용 컨테이너형 이동 실험실에 투자하여 CMP 검사에 대한 액세스를 확대합니다.

중동 및 아프리카은 걸프 협력 회의 국가의 중앙 집중식 메가 랩에 투자하고 1 차 케어 센터에서 POC 분석 장비를 개발합니다. 남아프리카에서는 국민건강보험 로드맵에 CMP가 필수진단제로 기재되어 조달이 활발해지고 있습니다. 남미에서는 민간 보험 회사가 만성 질환 번들에 포함된 대사 스크리닝에 매년 자금을 제공하는 브라질과 아르헨티나가 견인 역할을 하고 있습니다. 모든 신흥 지역에서 당뇨병과 신장 질환을 대상으로 한 기증자 자금 프로그램은 종합적 대사 패널 시장의 기본 볼륨을 구축하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 예방검진에 대한 의식의 고조

- 만성 신장병, 간병, 당뇨병 환자의 세계 증가

- 외래에서의 POC 화학 분석 장치의 급속한 보급

- CMP 워크플로우에 내장된 AI 주도의 의사결정 지원

- 고용주최의 웰니스 패널이 검사수를 증가

- 실험실과 제휴하는 재택 검체 채취의 신흥 기업

- 시장 성장 억제요인

- 인정 임상 화학자 및 임상 검사 기사의 부족

- 엄격한 CLIA-88 및 EU IVDR 규정 준수 비용

- LIS와 EHR 생태계 간의 데이터 교환 갭

- 고품위 효소 시약의 가격 변동 증가

- 공급망 분석

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 검사 유형별

- 단백질

- 신장 기능 검사

- 전해질 패널

- 간 기능 검사

- 포도당

- 기타 검사

- 질병별

- 신장 질환

- 당뇨병

- 간 질환

- 기타 질환

- 최종 사용자별

- POC(Point-of-Care) 센터

- 독립 및 병원 검사실

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Quest Diagnostics

- Laboratory Corporation of America Holdings

- Sonic Healthcare Ltd.

- SYNLAB Group

- Eurofins Scientific

- Mayo Clinic Laboratories

- Abbott Laboratories

- Roche Diagnostics

- Siemens Healthineers

- Danaher Corp.(Integrated Dx)

- ARUP Laboratories

- Charles River Laboratories

- NeoGenomics Laboratories

- Genoptix Inc.

- CENTOGENE AG

- Unipath Limited

- BioReference Laboratories

- Scion Lab Services

- TCG Corp.

- Medicover Diagnostics

제7장 시장 기회와 전망

KTH 25.10.30The comprehensive metabolic panel market is valued at USD 12.57 billion in 2025 and is forecast to reach USD 17.84 billion by 2030, advancing at a 7.25% CAGR.

Emerging preventive-care policies, the widening burden of diabetes, kidney, and liver disorders, and expanding point-of-care (POC) diagnostic networks form the bedrock of sustained demand. Hospitals are automating chemistry workflows to meet the FDA's 2024 Laboratory Developed Test (LDT) rule, while independent laboratories deploy high-throughput systems to comply with new quality-system mandates. AI-powered analytics are becoming standard add-ons, reducing manual review rates and turning routine panels into decision-support assets. POC chemistry analyzers that deliver lab-grade results in minutes now compete directly with core labs for test volumes, reshaping procurement patterns.

Global Comprehensive Metabolic Panel Market Trends and Insights

Growing Awareness of Preventive Health Check-Ups

Rising employer-sponsored wellness initiatives are normalizing annual metabolic panels, with biometric screening programs cutting employee healthcare costs by USD 24.25 per member per month and uncovering hidden risks in 16% of participants. Governments also subsidize preventive diagnostics; Medicare expanded reimbursement for metabolic panels used in chronic-care management in 2025. Mass-media campaigns in Canada and Germany highlight silent kidney disease, nudging at-risk adults toward routine chemistry testing. Pharmacies now bundle metabolic screens with vaccination drives, widening consumer access. Together, these actions move panels from episodic to scheduled care, elevating test volumes and stabilizing reagent demand across the comprehensive metabolic panel market.

Rising Global Burden of Chronic Kidney, Liver & Diabetes Cases

Diabetes cases are projected to hit 1.31 billion by 2050, anchoring long-term demand for metabolic monitoring. Chronic kidney disease (CKD) already affects 673 million people worldwide, with type 2 diabetes the primary driver of CKD-related deaths. In China, adult diabetes prevalence reached 13.7% in 2023 and could double without intervention. Such statistics compel payers to reimburse routine CMPs for early detection and risk stratification. As metabolic dysfunction-associated steatotic liver disease gains clinical recognition, liver function markers embedded in CMPs gain additional relevance. Long-term epidemiological pressure therefore injects a durable 1.8-percentage-point lift into forecast CAGR for the comprehensive metabolic panel market.

Shortage of Certified Clinical Chemists & Lab Technicians

Nearly 46% of US clinical laboratory positions are vacant, and only 5,000 graduates enter the workforce annually against demand for 26,000. New CLIA personnel rules effective January 2025 require higher educational credentials and supervised rotations, narrowing the applicant pool. Canada and parts of Western Europe face similar deficits, driving overtime costs and lengthening turnaround times. Staffing gaps slow instrument adoption because laboratories cannot run additional shifts, subtracting an estimated 1.4-percentage-point from forecast CAGR for the comprehensive metabolic panel market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of POC Chemistry Analyzers in Ambulatory Settings

- AI-Driven Decision-Support Embedded into CMP Workflows

- Stringent CLIA-88 & EU IVDR Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Kidney Function Tests accounted for 31.52% of the comprehensive metabolic panel market in 2024, supported by CKD screening mandates in primary care. Glucose testing, however, is expanding fastest at a 9.65% CAGR as diabetes programs embed fasting glucose and HbA1c within every CMP. Proteins testing grows steadily as albumin status gains importance in surgical risk scoring, while electrolytes panels remain indispensable in critical-care triage. Liver Function Tests draw renewed attention amid rising metabolic dysfunction-associated steatotic liver disease prevalence.

Continuous glucose monitoring trends spur novel specimen-collection products that blend capillary sampling with central-lab accuracy. Labcorp's at-home glucose risk device achieved 97% concordance with venous draws, broadening direct-to-consumer uptake. Roche's Elecsys PRO-C3 leverages advanced biomarkers to stage liver fibrosis more precisely. AI algorithms embedded in glucose panels flag early glycemic variability, enabling personalized management plans. Collectively, these advances cement glucose testing's leadership in new-revenue creation and enhance the comprehensive metabolic panel market size for digital-health-linked assays.

The Comprehensive Metabolic Panel Market Report is Segmented by Test Type (Proteins, Kidney Function Tests, Electrolytes Panel, and More), Disease (Kidney Diseases, Diabetes, Liver Diseases, and More), End User (Point-Of-Care Centers, and Independent & Hospital Laboratories), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 36.82% of comprehensive metabolic panel market revenue in 2024 owing to sophisticated insurance coverage and employer wellness programs that subsidize routine testing. The United States further benefitted from AI pilot deployments in major hospital networks, while Canada leveraged public-health campaigns encouraging metabolic screens during flu-shot visits. Mexico's federal health reform accelerated POC adoption across community clinics. The 2024 FDA LDT rule added upfront compliance costs but also formed a clear approval pathway that boosts investor confidence.

Europe remains the second-largest contributor as national health systems integrate CMPs into chronic-disease management protocols. Germany, the United Kingdom, and France upgraded chemistry platforms to AI-ready configurations, while Spain and Italy piloted home-collection partnerships. The EU IVDR raised documentation requirements, nudging small labs toward strategic alliances or outsourcing. NHS England's Long-Term Plan promotes POC chemistry in community health hubs, catalyzing decentralized testing. Eastern European countries modernize laboratories through EU cohesion funds, importing integrated chemistry-immunoassay platforms.

Asia-Pacific delivers the fastest 9.62% CAGR through 2030. China's soaring diabetes prevalence drives nationwide CMP screening campaigns aligned with its Healthy China 2030 strategy. Japan and South Korea adopt AI-assisted autoverification to address technician shortages, while Australia links POC devices to My Health Record for real-time data aggregation. India's diagnostics sector grows at 8-9% CAGR as private chains expand laboratory networks. Southeast Asian nations invest in containerized mobile labs for remote areas, widening access to CMP testing.

The Middle East and Africa region invests in centralized mega-labs within Gulf Cooperation Council states and rolls out POC analyzers in primary-care centers. South Africa's National Health Insurance roadmap lists CMPs among essential diagnostics, stimulating procurement. South America sees incremental growth led by Brazil and Argentina, where private insurers fund annual metabolic screens as part of chronic-disease bundles. Across all emerging regions, donor-funded programs targeting diabetes and kidney disease build foundational volume for the comprehensive metabolic panel market.

- Quest Diagnostics

- LabCorp

- Sonic Healthcare Ltd.

- SYNLAB Group

- Eurofins

- Mayo Clinic Laboratories

- Abbott Laboratories

- Roche

- Siemens Healthineers

- Danaher Corp. (Integrated Dx)

- ARUP Laboratories

- Charles River

- NeoGenomics Laboratories

- Genoptix

- Centogene

- Unipath Limited

- BioReference Laboratories

- Scion Lab Services

- TCG

- Medicover Diagnostics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Awareness Of Preventive Health Check-Ups

- 4.2.2 Rising Global Burden Of Chronic Kidney, Liver & Diabetes Cases

- 4.2.3 Rapid Adoption Of POC Chemistry Analyzers In Ambulatory Settings

- 4.2.4 AI-Driven Decision-Support Embedded Into CMP Workflows

- 4.2.5 Employer-Sponsored Wellness Panels Boosting Test Volumes

- 4.2.6 Home Sample-Collection Start-Ups Partnering With Labs

- 4.3 Market Restraints

- 4.3.1 Shortage Of Certified Clinical Chemists & Lab Technicians

- 4.3.2 Stringent CLIA-88 & EU IVDR Compliance Costs

- 4.3.3 Data-Exchange Gaps Between LIS And EHR Ecosystems

- 4.3.4 Rising Price Volatility Of High-Grade Enzyme Reagents

- 4.4 Supply-Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Proteins

- 5.1.2 Kidney Function Tests

- 5.1.3 Electrolytes Panel

- 5.1.4 Liver Function Tests

- 5.1.5 Glucose

- 5.1.6 Other Test Types

- 5.2 By Disease

- 5.2.1 Kidney Diseases

- 5.2.2 Diabetes

- 5.2.3 Liver Diseases

- 5.2.4 Other Diseases

- 5.3 By End User

- 5.3.1 Point-of-Care Centers

- 5.3.2 Independent & Hospital Laboratories

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Quest Diagnostics

- 6.3.2 Laboratory Corporation of America Holdings

- 6.3.3 Sonic Healthcare Ltd.

- 6.3.4 SYNLAB Group

- 6.3.5 Eurofins Scientific

- 6.3.6 Mayo Clinic Laboratories

- 6.3.7 Abbott Laboratories

- 6.3.8 Roche Diagnostics

- 6.3.9 Siemens Healthineers

- 6.3.10 Danaher Corp. (Integrated Dx)

- 6.3.11 ARUP Laboratories

- 6.3.12 Charles River Laboratories

- 6.3.13 NeoGenomics Laboratories

- 6.3.14 Genoptix Inc.

- 6.3.15 CENTOGENE AG

- 6.3.16 Unipath Limited

- 6.3.17 BioReference Laboratories

- 6.3.18 Scion Lab Services

- 6.3.19 TCG Corp.

- 6.3.20 Medicover Diagnostics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment