|

시장보고서

상품코드

1910628

자동차 소프트웨어 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

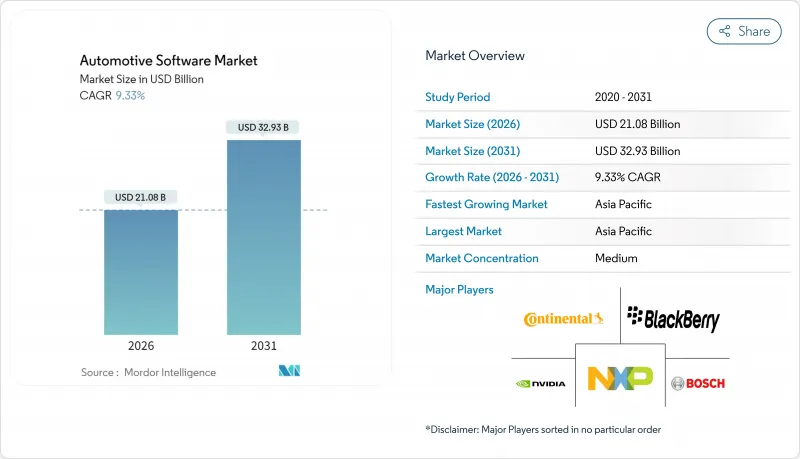

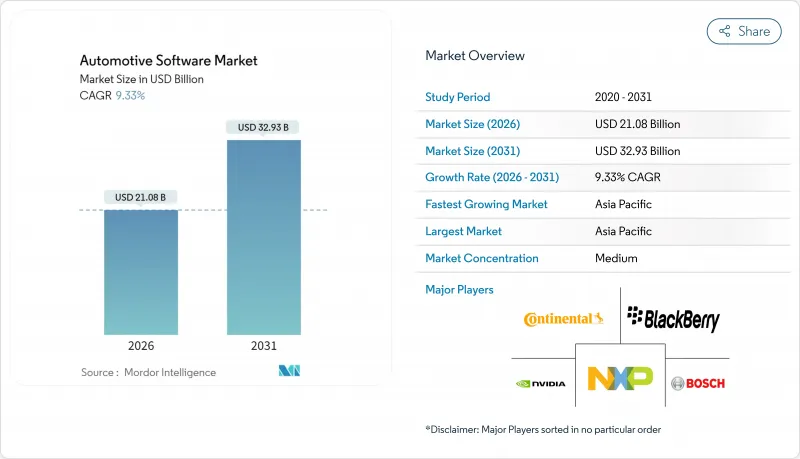

세계의 자동차 소프트웨어 시장은 2025년 192억 8,000만 달러로 평가되었으며, 2026년 210억 8,000만 달러에서 2031년까지 329억 3,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 9.33%로 예상됩니다.

이 성장은 하드웨어 중심 차량에서 소프트웨어 정의 플랫폼으로의 꾸준한 전환을 반영합니다. 배터리 최적화에서 자동 운전에 이르는 주요 기능은 기계 부품이 아닌 코드에 통합되는 형태입니다. 구역별 전자/전기 아키텍처의 채용 확대로 하네스의 중량을 최대 30% 삭감하고 새로운 기능을 위한 연산 능력을 해방하고 있습니다. 세계 자동차 제조업체들은 EU WP.29의 사이버 보안 및 소프트웨어 업데이트 규칙을 준수하기 위해 무선 업데이트(OTA) 기능의 도입을 급속히 진행하고 있습니다. 한편, 구독형 '온디맨드 기능' 서비스는 고수익 판매 후 수익원을 개척하기 시작하고 있습니다. 반도체 공급업체, 하이퍼스케일러, Tier 1 소프트웨어 기업의 관심이 높아짐에 따라 경쟁이 치열해지고 OS, 미들웨어, 안전 스택 자산을 확보하기 위한 인수가 급증하고 있습니다. 이러한 움직임과 전동화를 위한 정부의 인센티브는 배터리 관리 소프트웨어, 엣지 클라우드 연결, AI 구동형 코드 생성 툴로의 자본 유입을 계속하고 있습니다.

세계의 자동차 소프트웨어 시장 동향과 통찰

중국 자동차 제조업체에 의한 레벨 2 자동 운전 기능의 투입이 아시아의 ADAS 코드량을 증대

BYD, Xpeng, Zeekr등의 브랜드가 애자일 개발 프레임워크를 채용해, 기능 출시 사이클을 최대 60% 단축했습니다. 이로 인해 ADAS 코드 라인 수가 급증하고 서유럽 경쟁사의 경쟁력 추격이 가속되고 있습니다. 지각 처리, 센서 융합 및 경로 계획 알고리즘의 신속한 반복 개발은 중복 계산 처리에 대한 수요를 유발하고, 주요 칩 제조업체는 중국제 집중형 ECU 내에 통합된 도메인 특화형 가속기 설계를 진행하고 있습니다. 업계 관계자는 차량군을 최신 상태로 유지하기 위해서는 준거한 OTA 파이프라인이 필수이며, 지속적인 시장 리더십에는 보안 DevOps가 전제조건이라고 지적하고 있습니다.

OEM의 중앙 집중식 영역별 E/E 아키텍처 전환으로 세계 미들웨어 지출 증가

수십 개의 도메인 ECU를 4-6개의 구역 컨트롤러로 대체함으로써 Tesla Model 3 등의 모델에서 볼 수 있듯이 배선이 대폭 간소화되어 경량화와 전력 손실을 줄일 수 있습니다. 그러나 분산형 레이아웃은 이종 센서의 추상화, 결정론적 통신 관리, 기능 안전 파티션의 강제 등 복잡성을 소프트웨어 계층으로 이동시킵니다. 미들웨어 공급업체는 OEM 회사가 AUTOSAR Classic 및 Adaptive 스택, 실시간 POSIX 커널 및 클라우드 API의 통합을 급속히 진행하는 동안 통합 프로젝트 백로그가 발생했다고 보고합니다. NXP를 통한 TTTech Auto의 6억 2,500만 달러의 인수는 차종 제품군 전체에서 확장 가능한 인증된 미들웨어의 가치를 높이고 있습니다.

단편화된 미들웨어 표준이 OEM 간 재사용을 억제

통합 API의 부족으로 Tier 1 공급업체는 동일한 기능을 여러 개의 고유한 스택에 이식할 수 없으며 검증 비용 증가와 혁신 정체를 초래합니다. AUTOSAR 및 SOAFEE와 같은 컨소시엄은 조화로운 서비스 지향 프레임워크를 제안하고 있지만, 특히 독자적인 레이어를 고수하는 유럽 OEM간에 브랜드 전략의 차이가 수렴을 막고 있습니다. 따라서 미들웨어 벤더는 이식성을 우선으로 성능을 희생시키는 구성 가능한 어댑터를 개발하고 있으며, 이 타협은 런타임에 오버헤드 증가와 안전 인증의 복잡성을 초래합니다.

부문 분석

애플리케이션 소프트웨어는 2025년에도 자동차 소프트웨어 시장의 48.02%를 차지하며 여전히 가장 큰 수익원이 되었습니다. 이는 ADAS, 인포테인먼트 및 개인화된 무선 업데이트(OTA)에 대한 고객 수요를 반영한 것입니다. 운영 체제 플랫폼은 가장 급성장하는 분야이며 OEM 제조업체가 기능 안전을 위해 강화된 Linux 기반 배포판을 채택함에 따라 CAGR 9.62%로 확대되고 있습니다. 통합 컴퓨팅을 통한 기능 개발의 가속화에 따라 용도 계층 코드 시장 규모는 꾸준히 확대될 것으로 예측됩니다. POSIX 커널과 고레벨 용도 간의 안전 인증된 브리지 역할을 하는 미들웨어의 전략적 가치도 마찬가지로 증가하고 있으며, Aptiv는 이를 구역 간 트래픽의 '오케스트레이터'라고 부릅니다.

오픈소스 컴포넌트에 대한 의존도가 증가함에 따라 공급업체 간의 협상력이 재구성되고 있습니다. 반도체 공급업체는 고객 참여를 가속화하기 위해 참조 이미지를 번들로 제공하고 소프트웨어 통합업체는 장기 유지보수, 사이버 강화 및 변형 관리를 통해 수익을 창출합니다. 자동차 소프트웨어 시장이 공유 코드 기반으로 진화함에 따라 이해관계자는 컴플라이언스, 통합 툴, 실시간 결정성을 통해 차별화를 도모하고 있습니다. NXP에 의한 미들웨어 인수로 대표되는 업계 재편은 향후 전기차 및 자율주행차의 투입에 있어서 플랫폼의 범위가 계약 획득을 결정할 것을 시사하고 있습니다.

ADAS 및 안전 시스템은 EU 일반 안전 규정에 따른 지능형 속도 지원, 차선 유지 및 자동 긴급 브레이크의 의무화를 통해 2025년 자동차 소프트웨어 시장 수익의 33.25%를 차지했습니다. 이 분야는 높은 탑재율과 빈번한 기능 업그레이드의 혜택을 누리며 ADAS 소프트웨어는 5G 지원 데이터 파이프라인의 핵심이 되고 있습니다. 파워트레인 및 배터리 관리 용도는 OEM 각사가 BEV의 항속 거리 연장, 리튬 이온 배터리 보호, 양방향 충전 조정을 경쟁하면서 13.08%의 연평균 복합 성장률(CAGR)로 다른 분야를 능가할 것으로 예측되고 있습니다.

인포테인먼트 및 텔레매틱스 플랫폼은 5G 대역폭을 활용하고, 스트리밍 파트너를 통합하고, 예측 유지보수를 위한 차량 사용 데이터를 수집함으로써 지속적인 수익 확대의 야망을 뒷받침합니다. 차체 제어 모듈은 중앙 컴퓨팅 노드로 이동하고 공유 실리콘은 부품 비용을 줄이는 동시에 견고한 절연의 필요성을 증가시킵니다. 크로스 도메인 연계가 증가함에 따라 기존 경계는 모호해지지만 규제 압력은 안전 로직을 결정론적 코어에 고정시키고 비중요 소프트웨어는 컨테이너화 된 마이크로 서비스로 이동합니다.

지역별 분석

2025년 시점에서 아시아 지역은 자동차 소프트웨어 시장에서 38.62%의 최대 점유율을 차지했으며 11.48%의 연평균 복합 성장률(CAGR)로 확대될 것으로 전망됩니다. 이것은 중국에서 소프트웨어 정의 차량의 신속한 도입과 자율 항행 모듈에 대한 정부의 우대 조치가 견인하고 있습니다. 민첩한 출시 사이클을 통해 중국 자동차 제조업체는 기존 제조업체보다 60% 빠른 속도로 레벨 2 이상의 기능을 통합하여 국내 미들웨어 및 지각 스택 생태계를 활성화합니다. 한국은 5G-V2X의 조기 도입에 의해 엣지 클라우드 분석을 실현하고, 일본은 AI 모델 검증 랩을 통한 기능 안전 분야에서의 리더십에 주력하고 있습니다. 지역 배터리 공급망은 소프트웨어 강화 에너지 관리 시스템을 가속화하고 아시아가 자동차 소프트웨어 시장의 중심을 유지할 수 있도록 보장합니다.

북미는 2위에 위치해, 인플레이션 억제법(IRA)의 세액 공제를 활용해, 배터리 관리 소프트웨어나 가정용 충전 최적화 장치 수요를 확대하고 있습니다. 구독형 기능의 보급에 의해 자동차 제조업체는 판매 후에도 장기간에 걸쳐 운전 지원 기능의 업그레이드나 인포테인먼트 앱으로 수익화가 가능하게 되었습니다. 실리콘 밸리의 신흥 기업은 코드 릴리스 사이클을 단축하는 AI 툴을 제공하고, 디트로이트의 기존 기업은 소비자용 전자기기 수준의 개발 페이스를 실현하는 DevOps 파이프라인을 도입하고 있습니다. 이러한 요인이 결합되어 차량당 소프트웨어 탑재량은 높은 수준을 유지하고, 이 지역은 자동차 소프트웨어 시장에서 수익 창출 모델의 시험장으로서의 지위를 확고히 하고 있습니다.

유럽은 유엔 WP.29에 근거한 엄격한 사이버 보안 및 OTA(Over-The-Air) 규정을 기반으로 한 견고한 지위를 유지하고 인증된 소프트웨어 업데이트 관리 시스템의 도입을 추진하고 있습니다. 북유럽 국가(스웨덴이 주도)는 EV 보급과 디지털 서비스 대응력을 배경으로 10.85%의 연평균 복합 성장률(CAGR)이 전망되고 있습니다. 그러나 개발자 부족, 특히 AUTOSAR 공인 인력 부족은 임금 상승과 일정 지연의 위험을 초래합니다. 전문 교육 기관에 대한 투자는 자국 육성 능력으로의 전략적 전환을 보여주며, 소프트웨어 생산량을 확대하면서 품질을 보호한다는 유럽의 결의를 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중국 자동차 제조업체에 의한 레벨 2 자동 운전 기능 투입으로 아시아에서 ADAS 코드량 증대

- OEM 제조업체에 의한 집중형 구역별 전기 전자 아키텍처로의 이행이, 세계적으로 미들웨어 지출 증대

- EU WP.29 OTA 갱신 지침이 유럽의 안전한 소프트웨어 스택 가속화

- 구독형 '온 디맨드 기능' 모델이 북미에서 판매 후 소프트웨어 수익을 확대

- 미국 IRA 전기자동차 인센티브가 배터리 관리 소프트웨어 수요를 견인

- 한국에서 엣지 클라우드 자동차 소프트웨어 서비스를 실현하는 5G-V2X 네트워크의 전개

- 시장 성장 억제요인

- 단편화된 미들웨어 표준이 OEM 간 재사용을 억제

- 유럽에서의 AUTOSAR Classic 및 Adaptive 개발자 부족이 비용 견인

- R155/R156 사이버 인증 시험의 비용이 프로그램 스케줄을 지연 있습니다

- 신흥 시장의 레거시 CAN 아키텍처가 SDV 도입을 제한

- 가치/공급망 분석

- 규제 동향(UNECE R155/R156, 미국 OTA 규칙, EU 사이버 레지리언스법)

- 기술 전망(존 아키텍처, AI 툴 체인, 무선 갱신 파이프라인)

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액(달러))

- 소프트웨어 층별

- 애플리케이션 소프트웨어

- 미들웨어

- 운영체제

- 펌웨어/기본 입출력 소프트웨어

- 용도별

- ADAS 및 안전 시스템

- 인포테인먼트 및 텔레매틱스

- 파워트레인 및 배터리 관리

- 차체 컨트롤 및 쾌적성

- 커넥티드카 서비스

- 차량 유형별

- 승용차

- 소형 상용차

- 대형 상용차

- 추진력별

- 내연 기관차(ICE)

- 배터리식 전기자동차(BEV)

- 하이브리드 전기자동차(HEV/PHEV)

- 전개별

- 온보드(내장)

- 오프보드(클라우드/엣지 환경)

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Robert Bosch GmbH

- Continental AG

- Elektrobit

- BlackBerry Limited(QNX)

- Google LLC(Alphabet Inc.)

- Microsoft Corporation

- Wind River Systems

- NXP Semiconductors NV

- NVIDIA Corporation

- Aptiv PLC

- TTTech Auto AG

- Vector Informatik GmbH

- Infineon Technologies AG

- Intel Corporation

- LG Electronics Vehicle Solutions

- DENSO Corporation

- Panasonic Automotive Systems

- KPIT Technologies Ltd.

- Intellias Ltd.

- Tata Elxsi Ltd.

- Airbiquity Inc.

- MontaVista Software LLC

- Renesas Electronics Corporation

- HARMAN International

- GlobalLogic Inc.

제7장 시장 기회와 미래 전망

SHW 26.01.26The automotive software market was valued at USD 19.28 billion in 2025 and estimated to grow from USD 21.08 billion in 2026 to reach USD 32.93 billion by 2031, at a CAGR of 9.33% during the forecast period (2026-2031).

Growth reflects the steady shift from hardware-centric vehicles to software-defined platforms where key functions, ranging from battery optimisation to automated driving, reside in code rather than mechanical parts. The rising adoption of zonal electronic/electrical architectures is trimming harness weight by up to 30% and freeing computing power for new features. Global automakers are fast-tracking over-the-air (OTA) update capabilities to comply with EU WP.29 cybersecurity and software-update rules, while subscription-based "functions-on-demand" services are starting to unlock high-margin, post-sale revenue streams. Heightened interest from semiconductor suppliers, hyperscalers, and Tier-1 software firms is intensifying competition, prompting a surge of acquisitions to secure operating-system, middleware, and safety-stack assets. These moves and government incentives for electrification keep capital flowing into battery-management software, edge-cloud connectivity, and AI-driven code-generation tools.

Global Automotive Software Market Trends and Insights

Level-2+ Autonomous Launches by Chinese OEMs Boosting ADAS Code Volume in Asia

Agile development frameworks allow brands such as BYD, Xpeng, and Zeekr to trim feature-release cycles by up to 60%, driving an explosion in ADAS code lines and accelerating competitive catch-up by Western rivals. Rapid iteration on perception, sensor fusion, and path-planning algorithms fuels demand for redundant compute, leading chipmakers to design domain-specific accelerators packaged within Chinese-built centralized ECUs. Industry observers note that compliant OTA pipelines are mandatory to keep those fleets current, making secure DevOps a prerequisite for sustained market leadership.

OEM Shift to Centralized Zonal E/E Architectures Raising Middleware Spend Globally

Replacing dozens of domain ECUs with four to six zone controllers simplifies wiring significantly, as exemplified in models such as Tesla Model 3, cuts weight, and reduces power loss. Yet decentralised layout shifts complexity toward software layers that must abstract heterogeneous sensors, manage deterministic communication, and enforce functional-safety partitions. Middleware vendors report a backlog of integration projects as OEMs race to harmonise AUTOSAR Classic and Adaptive stacks, real-time POSIX kernels, and cloud APIs. NXP's USD 625 million purchase of TTTech Auto highlighted the premium on certified middleware that can scale across vehicle families.

Fragmented Middleware Standards Hindering Cross-OEM Re-use

Lack of unified APIs forces Tier-1s to port identical functions to multiple proprietary stacks, elevating validation expense and slowing innovation. Consortia such as AUTOSAR and SOAFEE have proposed harmonised service-oriented frameworks, yet diverging brand strategies stall convergence, particularly among European OEMs with entrenched bespoke layers. Middleware houses thus build configurable adapters that sacrifice performance for portability, a compromise that adds runtime overhead and complicates safety certification.

Other drivers and restraints analyzed in the detailed report include:

- EU WP.29 OTA-Update Mandate Accelerating Secure Software Stacks in Europe

- Subscription-Based 'Functions-on-Demand' Models Expanding Post-Sale Software Revenues in North America

- Shortage of AUTOSAR Classic and Adaptive Developers in Europe Inflating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Application software still delivers the highest revenue at 48.02% of the automotive software market in 2025, mirroring customer appetite for ADAS, infotainment, and personalised over-the-air upgrades. Operating-system platforms are the fastest-growing slice, advancing at 9.62% CAGR as OEMs embrace Linux-based distributions hardened for functional safety. The market size for application-layer code is projected to climb steadily as consolidated compute unlocks faster feature roll-outs. Middleware's strategic value climbs in step, acting as a safety-certified bridge between POSIX kernels and high-level apps; Aptiv calls it the "orchestrator" of zonal traffic.

Growing reliance on open-source components reshapes vendor bargaining power. Silicon suppliers bundle reference images to accelerate customer entry, while software integrators monetise long-term maintenance, cyber-hardening, and variant management. As the automotive software market evolves toward shared code bases, stakeholders differentiate via compliance, integration tooling, and real-time determinism. Consolidation, exemplified by NXP's middleware acquisition, signals that platform breadth will determine contract wins for forthcoming electric and autonomous vehicle launches.

ADAS and safety systems delivered 33.25% revenue of the automotive software market in 2025, thanks to mandatory intelligent-speed assist, lane-keeping, and AEB under the EU General Safety Regulation. The cluster benefits from high attach rates and frequent feature upgrades, keeping ADAS software at the heart of 5 G-enabled data pipelines. Powertrain and battery-management applications are forecasted to outpace all others at 13.08% CAGR as OEMs race to extend BEV range, safeguard lithium-ion cells, and orchestrate bidirectional charging.

Infotainment and telematics platforms absorb 5G bandwidth, integrate streaming partners, and harvest vehicle-usage data for predictive maintenance, fuelling recurring revenue ambitions. Body-control modules migrate to central compute nodes, where shared silicon slashes bill-of-materials cost yet magnifies the need for robust isolation. Increasing cross-domain orchestration blurs historical boundaries, but regulatory pressure keeps safety logic anchored in deterministic cores while non-critical software shifts toward containerised microservices.

The Automotive Software Market Report is Segmented by Software Layer (Application Software, Middleware, and More), Application (ADAS and Safety Systems and More), Vehicle Type (Passenger Cars and More), Propulsion (Internal Combustion Engine Vehicles (ICE) and More), Deployment (On-Board (Embedded) and Off-Board (Cloud / Edge)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia commanded the largest regional share at 38.62% of the automotive software market in 2025, and is projected to grow at an 11.48% CAGR, propelled by China's fast-track deployment of software-defined vehicles and government incentives for autonomous navigation modules. Agile release cycles let Chinese OEMs integrate Level-2+ functions at a pace 60% quicker than traditional counterparts, catalysing domestic middleware and perception-stack ecosystems. South Korea's early roll-out of 5 G-V2X enables edge-cloud analytics, while Japan focuses on functional-safety leadership through AI-model verification labs. Regional battery supply chains accelerate software-enhanced energy-management systems, ensuring that Asia remains the gravitational centre of the automotive software market.

North America sits second, leveraging the Inflation Reduction Act credits to swell demand for battery-management software and home-charging optimisers. Subscription-driven features have proliferated, allowing automakers to monetise driver-assistance upgrades and infotainment apps long after the point of sale. Silicon Valley start-ups inject AI tooling that shortens code-release cycles, and Detroit incumbents adopt DevOps pipelines mirroring consumer-electronics cadence. Together, these factors sustain high per-vehicle software content, cementing the region as a testbed for revenue-generation models in the automotive software market.

Europe maintains a formidable position anchored by stringent cybersecurity and OTA mandates under UN WP.29, driving uptake of certified software-update management systems. The Nordics, spearheaded by Sweden, are pegged for a 10.85% CAGR on the back of EV prevalence and digital-service readiness. Nonetheless, developer shortages, particularly AUTOSAR-certified talent, impose wage inflation and risk schedule slippage. Investment in dedicated training academies reflects a strategic pivot to home-grown capability, underscoring Europe's resolve to safeguard quality while scaling software output.

- Robert Bosch GmbH

- Continental AG

- Elektrobit

- BlackBerry Limited (QNX)

- Google LLC (Alphabet Inc.)

- Microsoft Corporation

- Wind River Systems

- NXP Semiconductors N.V.

- NVIDIA Corporation

- Aptiv PLC

- TTTech Auto AG

- Vector Informatik GmbH

- Infineon Technologies AG

- Intel Corporation

- LG Electronics Vehicle Solutions

- DENSO Corporation

- Panasonic Automotive Systems

- KPIT Technologies Ltd.

- Intellias Ltd.

- Tata Elxsi Ltd.

- Airbiquity Inc.

- MontaVista Software LLC

- Renesas Electronics Corporation

- HARMAN International

- GlobalLogic Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Level-2+ Autonomous Launches by Chinese OEMs Boosting ADAS Code Volume in Asia

- 4.2.2 OEM Shift to Centralized Zonal E/E Architectures Raising Middleware Spend Globally

- 4.2.3 EU WP.29 OTA-Update Mandate Accelerating Secure Software Stacks in Europe

- 4.2.4 Subscription-Based 'Functions-on-Demand' Models Expanding Post-Sale Software Revenues in North America

- 4.2.5 U.S. IRA EV Incentives Driving Battery-Management Software Demand

- 4.2.6 Roll-out of 5G-V2X Networks Enabling Edge-Cloud Automotive Software Services in South Korea

- 4.3 Market Restraints

- 4.3.1 Fragmented Middleware Standards Hindering Cross-OEM Re-use

- 4.3.2 Shortage of AUTOSAR Classic & Adaptive Developers in Europe Inflating Costs

- 4.3.3 R155/R156 Cyber-Homologation Testing Costs Delaying Program Timelines

- 4.3.4 Legacy CAN Architectures in Emerging Markets Limiting SDV Adoption

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook (UNECE R155/R156, U.S. OTA Rules, EU Cyber Resilience Act)

- 4.6 Technological Outlook (Zonal Architecture, AI Tool-chains, Over-the-Air Pipelines)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Software Layer

- 5.1.1 Application Software

- 5.1.2 Middleware

- 5.1.3 Operating System

- 5.1.4 Firmware / Basic Input-Output Software

- 5.2 By Application

- 5.2.1 ADAS and Safety Systems

- 5.2.2 Infotainment and Telematics

- 5.2.3 Powertrain and Battery-Management

- 5.2.4 Body Control and Comfort

- 5.2.5 Connected Vehicle Services

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.4 By Propulsion

- 5.4.1 Internal Combustion Engine Vehicles (ICE)

- 5.4.2 Battery Electric Vehicles (BEV)

- 5.4.3 Hybrid Electric Vehicles (HEV/PHEV)

- 5.5 By Deployment

- 5.5.1 On-Board (Embedded)

- 5.5.2 Off-Board (Cloud / Edge)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of the Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Elektrobit

- 6.4.4 BlackBerry Limited (QNX)

- 6.4.5 Google LLC (Alphabet Inc.)

- 6.4.6 Microsoft Corporation

- 6.4.7 Wind River Systems

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 NVIDIA Corporation

- 6.4.10 Aptiv PLC

- 6.4.11 TTTech Auto AG

- 6.4.12 Vector Informatik GmbH

- 6.4.13 Infineon Technologies AG

- 6.4.14 Intel Corporation

- 6.4.15 LG Electronics Vehicle Solutions

- 6.4.16 DENSO Corporation

- 6.4.17 Panasonic Automotive Systems

- 6.4.18 KPIT Technologies Ltd.

- 6.4.19 Intellias Ltd.

- 6.4.20 Tata Elxsi Ltd.

- 6.4.21 Airbiquity Inc.

- 6.4.22 MontaVista Software LLC

- 6.4.23 Renesas Electronics Corporation

- 6.4.24 HARMAN International

- 6.4.25 GlobalLogic Inc.