|

시장보고서

상품코드

1850167

MEA 위치 분석 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)MEA Location Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

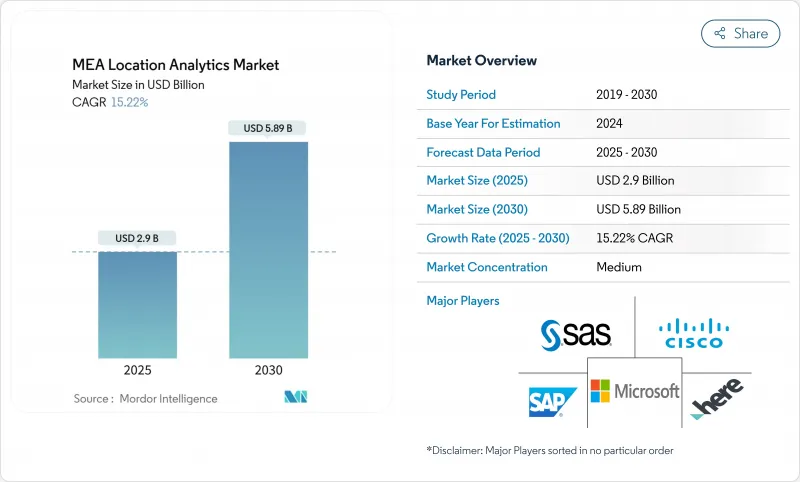

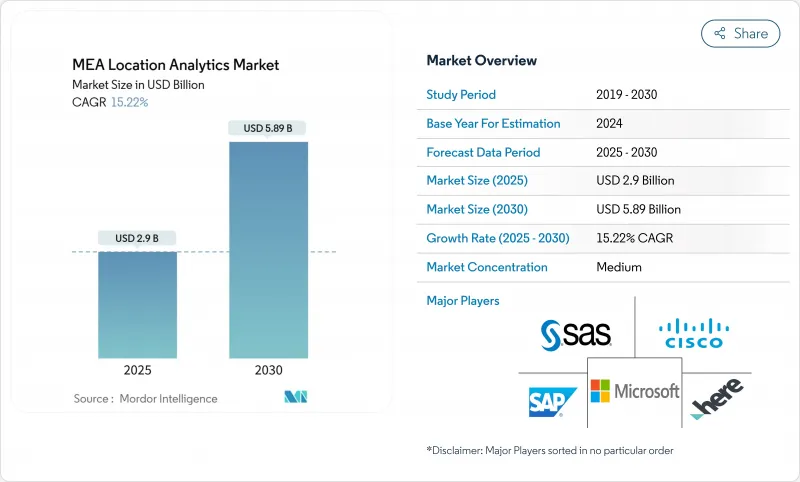

MEA 위치 분석 시장 규모는 2025년에 29억 달러, CAGR 15.22%로 성장하여 2030년에는 58억 9,000만 달러에 이를 것으로 예측됩니다.

걸프 협력 회의(GCC)로 스마트 시티에 대한 투자가 급증하고 공간 인텔리전스에 대한 수요가 확대되는 반면, 5G 도입과 주권 클라우드 배포로 데이터 수집 및 처리 속도와 보안이 향상되었습니다. 대규모 이동성 및 인프라 프로젝트에서는 교통, 안전 및 도시 서비스 최적화를 위해 지속적인 지오데이터 피드가 필요하기 때문에 실외 분석이 여전히 주류가 되고 있습니다. 동시에 실내 및 실외 추적의 융합이 전자상거래 물류를 재구성하고 있으며 NEOM과 같은 메가 프로젝트를 위한 디지털 트윈 이니셔티브가 보다 높은 빈도의 데이터와 실시간 시각화를 제공하기 위해 공급업체를 뒷받침하고 있습니다. 데이터의 주권에 관한 규제의 초점은 아키텍처 선택을 로컬 클라우드와 소블린 클라우드로 이끌어내고, 지리공간 분석의 기술 부족의 심각화는 전문 서비스 제공업체의 역할을 높이고 있습니다.

MEA 위치 분석 시장 동향 및 통찰

GCC 스마트 시티 프로그램에서 IoT 센서의 보급

리야드, 두바이, 도하의 유비쿼터스 센서 네트워크는 실시간 캡처 및 시각화가 가능한 강력한 분석 플랫폼을 필요로 하는 지오태그가 있는 스트림을 지속적으로 생성합니다. 두바이는 200개가 넘는 스마트 서비스를 도입했으며, McCa는 해지 시즌에 산간 연결을 유지하기 위해 LoRa 지원 장치를 통합합니다. 지자체 기관은 교통 밀도 예측, 폐기물 수집 최적화 및 보안 사고 모니터링에 이러한 데이터 흐름을 활용합니다. 그 결과 얻어지는 데이터량은 시 당국에 에지 처리와 AI 알고리즘의 채택을 촉구하고, 소스로 정보를 필터링해 분석했으며, 의사 결정을 가속시킵니다. 시험 도입이 본격적인 생산으로 전환됨에 따라, 지자체 입찰은 개방형 API와 멀티 프로토콜 호환성을 점점 더 많이 지정하고 있으며, 보다 광범위한 공급업체 생태계를 홍보하고 있습니다.

가속하는 5G 스몰셀 전개로 실시간 분석 가능

GCC 수도의 광범위한 5G 커버리지는 10ms 미만의 대기 시간을 제공하여 자율 주행 셔틀, 무인 항공기 기반 검사, 증강현실 도로 안내 등의 고급 용도를 가능하게 합니다. 사업자는 지자체의 플래너와 협력하여 거리 가구에 스몰셀을 내장하여 고해상도 추적 및 비디오 분석을 위한 신호 밀도를 향상시키고 있습니다. 새로운 대역폭을 통해 고해상도 3D 맵을 제어실로 실시간 스트리밍할 수 있어 긴급 대응 조정이 향상됩니다. 석유, 공공 및 물류 산업의 기업들은 모바일 자산으로부터 중단 없는 데이터 흐름이 필요하기 때문에 네트워크 업그레이드를 애널리틱스 로드맵에 맞추고 있습니다. 조기 도입 기업은 에지 AI가 센서의 경고를 로컬로 처리하면 예지 보전에 의한 운영 비용을 절감할 수 있다고 보고하고 있습니다.

데이터 주권 및 개인정보 보호 규정

사우디아라비아의 개인 데이터 보호법과 아랍에미리트(UAE)의 데이터 보호에 관한 연방정령은 국경 내에서 기밀성이 높은 위치 정보를 저장할 것을 프로세서에 의무화하고 있습니다. 의료, 금융 및 방어 프로젝트는 엄격한 동의와 감사 추적에 직면하여 On-Premise 또는 소블린 클라우드를 도입해야 합니다. 다국적 공급업체는 로컬 클라우드 리전을 시작하고 개인을 식별할 수 있는 정보를 분리하는 데이터 현지화 계층을 제공함으로써 대응합니다. 종종 법적 검토, 암호화 키 관리, 로컬 인시던트 지원 프로토콜이 필요합니다.

부문 분석

2024년 교통부와 공공사업부가 고속도로, 항만, 지하철 시스템을 디지털화하면서 실외 솔루션은 MEA 위치 분석 시장의 72%를 차지했습니다. 지오펜싱 알고리즘과 결합된 카메라 피드는 동적 요금 징수 및 교통 신호 최적화를 지원하여 주요 통로 혼잡을 완화합니다. 옥외에서 MEA 위치 분석 시장 규모는 도시 전반의 이동성 애즈 서비스 플랫폼의 혜택을 받아 2030년까지 꾸준히 확대될 것으로 예측됩니다. 실내에서는 쇼핑몰, 공항, 병원이 비콘과 LiDAR을 도입하여 고객의 이동 경로와 자산의 이용 상황을 파악하고 있습니다. 도입이 가장 진행되고 있는 것은 티아원 몰이며, 운영상의 이익이 하드웨어나 캘리브레이션의 비용을 상쇄하고 있습니다. 니어필드 추적은 상점 앱과 로열티 프로그램 간의 격차를 메우고 캠페인 전환을 강화합니다.

새로운 이용 사례는 실내 및 실외 데이터 세트를 융합하여 신호가 중단되지 않고 공급망 노드를 통해 자산을 추적합니다. 물류 운영자는 크로스 독 창고와 최종 마일 루트를 단일 플랫폼에서 매핑하여 전달 정확도를 높이고 잊어 버린 사고를 줄입니다. 시설 관리자는 빌딩 정보 모델링과 GIS 대시보드를 통합하여 공간 컨텍스트로 유지보수 티켓을 시각화합니다. 이 수렴은 플로어 플랜 디지털화, Wi-Fi 히트 맵핑, 전 지구 항법 위성 시스템(GNSS) 보정 서비스를 통합한 서비스를 제공하는 새로운 벤더가 등장해, 보다 광범위한 MEA 위치 분석 업계에서 2자리 성장이 전망되고 있습니다.

클라우드 플랫폼은 2024년 MEA 위치 분석 시장의 66%를 차지하고 CAGR 19.50%로 계속 On-Premise 시스템을 상회합니다. 전기통신사업자, 소매업체, 공공기관은 하이퍼스케일러가 운용하는 지역 데이터센터에 의존하여 테라바이트 단위의 지리공간 기록을 탄력적으로 보존·처리하고 있습니다. 클라우드 호스팅 워크로드의 MEA 위치 분석 시장 규모는 데이터 주권을 준수하는 지역이 증가함에 따라 2027년까지 On-Premise 지출을 초과할 것으로 예측됩니다. 지역별 보안 인증 및 저지연 에지 영역은 자율 주행 셔틀 제어 및 실시간 군중 모니터링과 같은 지연에 민감한 용도의 마이그레이션을 촉진합니다.

기밀 프로젝트와 공공 네트워크에서 분리된 시설에서는 On-Premise 솔루션이 필수적인 것은 아닙니다. 방어 및 중요 인프라 사업자는 엄격한 성능과 기밀성 목표를 달성하기 위해 강력한 서버와 프라이빗 클라우드를 도입했습니다. 하이브리드 아키텍처는 스트리밍 데이터를 로컬로 처리하는 에지 어플라이언스를 통합한 다음 집계된 통찰력을 소블린 클라우드로 오프로드하고 장기적인 분석을 통해 지원을 수집합니다. 공급업체는 구축된 커넥터, 제로 트러스트 프레임워크, 예산 제약을 완화하는 종량 과금 가격 설정을 통해 차별화를 도모하고 있으며, 배포의 유연성이 MEA 위치 분석 업계 전반의 구매 의사 결정을 지원한다는 것을 이야기하고 있습니다.

중동 및 아프리카의 위치 정보 분석 시장은 장소별(옥외, 실내), 전개 모델별(On-Premise, 온디맨드(클라우드)), 용도별(원격 감시, 자산 관리, 시설 관리), 컴포넌트별(소프트웨어, 서비스), 업종별(소매업, 제조업 등), 국가별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- GCC 스마트 시티 프로그램에서의 IoT 센서의 보급

- 실시간 분석을 가능하게 하는 5G 소형 셀 출시 가속화

- 소매업과 정부 기관에 있어서의 클라우드 퍼스트의 GIS/BI 도입

- 대규모 에너지 프로젝트에서 ESG 지역 보고서의 의무화

- 시장 성장 억제요인

- 데이터 주권과 프라이버시 규제

- 실내 위치 추적에 있어서의 고액의 설비 투자와 스킬 격차

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업간 경쟁 관계

- 대체품의 위협

- 투자분석

제5장 시장 규모와 성장 예측

- 장소별

- 옥외

- 실내

- 전개 모델별

- On-Premise

- On-demand (Cloud)

- 용도별

- 원격 모니터링

- 자산운용관리

- 시설 관리

- 업계별

- 소매

- 제조업

- 헬스케어

- 정부

- 에너지 및 전력

- 기타 업종

- 컴포넌트별

- 소프트웨어

- 서비스

- 국가별

- 아랍에미리트(UAE)

- 사우디아라비아

- 이스라엘

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Cisco Systems

- Microsoft Corporation

- HERE Technologies

- SAS Institute Inc.

- Oracle Corporation

- SAP SE

- Esri

- Tibco Software Inc.

- Pitney Bowes

- Galigeo

- Hexagon AB

- TomTom

- Trimble Inc.

- Mapbox

- Alteryx

- CARTO

- Foursquare

- Splunk Inc.

- Ubisense

제7장 시장 기회와 장래의 전망

SHW 25.11.07The MEA location analytics market size is valued at USD 2.9 billion in 2025 and is forecast to advance at a 15.22% CAGR, reaching USD 5.89 billion by 2030.

Surging smart-city investments across the Gulf Cooperation Council (GCC) are expanding demand for spatial intelligence, while 5G deployments and sovereign cloud rollouts improve the speed and security of data gathering and processing. Outdoor analytics remains dominant because large-scale mobility and infrastructure projects require continuous geodata feeds for traffic, safety, and urban-services optimization. At the same time, the fusion of indoor and outdoor tracking is reshaping e-commerce logistics, and digital twin initiatives for mega-projects such as NEOM are pushing vendors to deliver higher-frequency data and real-time visualization. Regulatory focus on data sovereignty is guiding architecture choices toward local or sovereign clouds, and mounting skills shortages in geospatial analytics are elevating the role of specialized service providers.

MEA Location Analytics Market Trends and Insights

Proliferation of IoT Sensors in GCC Smart-City Programmes

Ubiquitous sensor networks in Riyadh, Dubai, and Doha generate continuous geotagged streams that demand powerful analytics platforms capable of real-time ingestion and visualization. Dubai has implemented more than 200 smart services, while Makkah is integrating LoRa-enabled devices to maintain connectivity in mountainous terrain during the Hajj season. Municipal agencies use these data flows to predict traffic density, optimize waste collection, and monitor public safety incidents. The resulting data volume pushes city authorities to adopt edge processing and AI algorithms that filter and analyze information at the source, accelerating decision-making. As pilot deployments shift to full production, municipal tenders increasingly specify open APIs and multi-protocol compatibility, encouraging a broader supplier ecosystem.

Accelerated 5G Small-Cell Rollout Enabling Real-Time Analytics

Widespread 5G coverage in GCC capitals delivers sub-10-millisecond latency, allowing advanced applications such as autonomous shuttles, drone-based inspection, and augmented-reality wayfinding. Operators collaborate with municipal planners to embed small cells in street furniture, which improves signal density for high-resolution tracking and video analytics. The new bandwidth permits live streaming of high-definition 3D maps to control rooms, enhancing emergency response coordination. Enterprises across oil, utilities, and logistics verticals are aligning network upgrades with analytics roadmaps, citing the need for uninterrupted data flows from mobile assets. Early adopters report operational cost savings from predictive maintenance once edge AI processes sensor alerts locally.

Data-Sovereignty and Privacy Regulations

Saudi Arabia's Personal Data Protection Law and the UAE's Federal Decree-Law on Data Protection oblige processors to store sensitive location attributes within national borders. Healthcare, finance, and defense projects face strict consent and audit trails, prompting on-premises or sovereign cloud deployments. Multinational vendors respond by launching local cloud regions and offering data-localization tiers that segregate personally identifiable information. Compliance checks elevate project timelines and costs, often requiring legal reviews, encryption key management, and local incident-response protocols.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-First GIS/BI Adoption Across Retail and Government

- Mandatory ESG Geo-Reporting for Large Energy Projects

- High CAPEX and Skills Gap for Indoor Positioning

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Outdoor solutions represented 72% of the MEA location analytics market in 2024 as ministries of transport and public works digitized highways, ports, and metro systems. Camera feeds combined with geofencing algorithms support dynamic tolling and traffic-signal optimization, cutting congestion on flagship corridors. The MEA location analytics market size for outdoor deployments is forecast to climb steadily through 2030, benefiting from city-wide mobility-as-a-service platforms. Indoors, malls, airports, and hospitals deploy beacons and LiDAR to gain customer-journey and asset-utilization insights. Uptake is strongest in tier-one malls where operational gains offset hardware and calibration costs. Near-field tracking bridges the gap between store apps and loyalty programs, enhancing campaign conversion.

Emerging use cases blend indoor and outdoor datasets to track assets across supply-chain nodes without signal drop. Logistics operators map cross-dock warehouses and final-mile routes on a single platform, improving hand-off accuracy and reducing misplacement incidents. Facility managers integrate building information modeling with GIS dashboards to visualize maintenance tickets in spatial context. This convergence draws new vendors that bundle floor-plan digitization, Wi-Fi heat-mapping, and global navigation satellite system (GNSS) correction services into unified offerings, positioning them for double-digit gains within the broader MEA location analytics industry.

Cloud platforms owned 66% of the MEA location analytics market in 2024 and continue to outpace on-premises systems with a 19.50% CAGR. Telecom operators, retailers, and public agencies rely on regional data centers operated by hyperscalers to elastically store and process terabytes of geospatial records. The MEA location analytics market size for cloud-hosted workloads is projected to surpass on-premises spending before 2027 as data-sovereignty-compliant regions multiply. Region-specific security certifications and low-latency edge zones encourage migration of latency-sensitive applications such as autonomous shuttle control and real-time crowd monitoring.

On-premises solutions remain essential for classified projects and installations disconnected from public networks. Defense and critical-infrastructure operators deploy ruggedized servers and private clouds to meet stringent performance and confidentiality targets. Hybrid architectures gain traction, integrating edge appliances that process streaming data locally before offloading aggregated insights to sovereign clouds for long-term analytics. Vendors differentiate through pre-built connectors, zero-trust frameworks, and pay-as-you-go pricing to ease budget constraints, illustrating how deployment flexibility underpins purchasing decisions across the MEA location analytics industry.

Middle East and Africa Location Analytics Market Segmented by Location (Outdoor, Indoor), Deployment Model (On-Premise, On-Demand (Cloud)), Application (Remote Monitoring, Asset Management, and Facility Management), Component (Software and Services), Vertical (Retail, Manufacturing, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Cisco Systems

- Microsoft Corporation

- HERE Technologies

- SAS Institute Inc.

- Oracle Corporation

- SAP SE

- Esri

- Tibco Software Inc.

- Pitney Bowes

- Galigeo

- Hexagon AB

- TomTom

- Trimble Inc.

- Mapbox

- Alteryx

- CARTO

- Foursquare

- Splunk Inc.

- Ubisense

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of IoT sensors in GCC smart-city programmes

- 4.2.2 Accelerated 5G small-cell rollout enabling real-time analytics

- 4.2.3 Cloud-first GIS/BI adoption across retail and government

- 4.2.4 Mandatory ESG geo-reporting for large energy projects

- 4.3 Market Restraints

- 4.3.1 Data-sovereignty and privacy regulations

- 4.3.2 High CAPEX and skills gap for indoor positioning

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Location

- 5.1.1 Outdoor

- 5.1.2 Indoor

- 5.2 By Deployment Model

- 5.2.1 On-premise

- 5.2.2 On-demand (Cloud)

- 5.3 By Application

- 5.3.1 Remote Monitoring

- 5.3.2 Asset Management

- 5.3.3 Facility Management

- 5.4 By Vertical

- 5.4.1 Retail

- 5.4.2 Manufacturing

- 5.4.3 Healthcare

- 5.4.4 Government

- 5.4.5 Energy and Power

- 5.4.6 Other Verticals

- 5.5 By Component

- 5.5.1 Software

- 5.5.2 Services

- 5.6 By Country

- 5.6.1 United Arab Emirates

- 5.6.2 Saudi Arabia

- 5.6.3 Israel

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems

- 6.4.2 Microsoft Corporation

- 6.4.3 HERE Technologies

- 6.4.4 SAS Institute Inc.

- 6.4.5 Oracle Corporation

- 6.4.6 SAP SE

- 6.4.7 Esri

- 6.4.8 Tibco Software Inc.

- 6.4.9 Pitney Bowes

- 6.4.10 Galigeo

- 6.4.11 Hexagon AB

- 6.4.12 TomTom

- 6.4.13 Trimble Inc.

- 6.4.14 Mapbox

- 6.4.15 Alteryx

- 6.4.16 CARTO

- 6.4.17 Foursquare

- 6.4.18 Splunk Inc.

- 6.4.19 Ubisense

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment