|

시장보고서

상품코드

1850250

GaN RF 반도체 장비 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)GaN RF Semiconductor Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

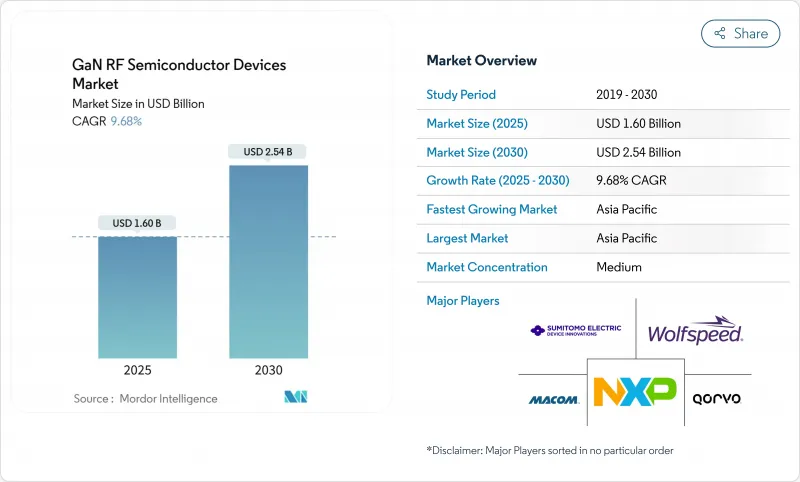

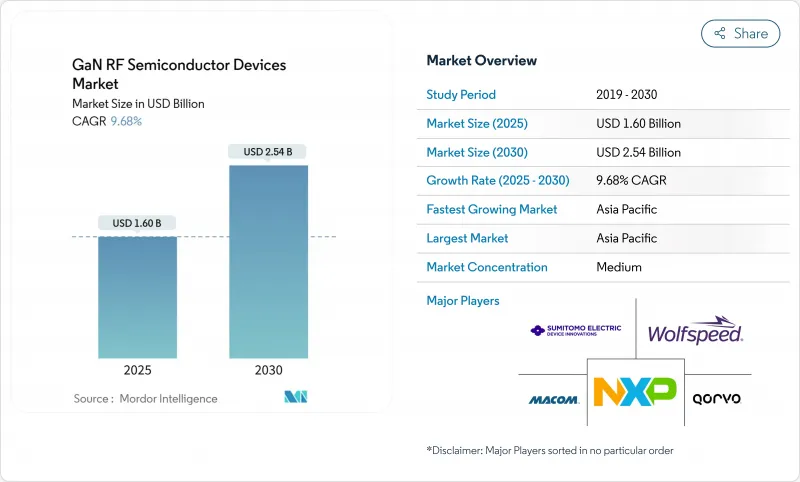

GaN RF 반도체 장비 시장 규모는 2025년에 16억 달러로 평가되었고, 2030년에는 25억 4,000만 달러로 확대될 것으로 예측되며, CAGR은 9.68%를 나타낼 전망입니다.

5G 인프라, 능동 전자 스캔 어레이(AESA) 레이더, 위성 페이로드, 79GHz 자동차 이미징 레이더 분야에서 고주파 및 고출력 솔루션에 대한 수요 증가로 갈륨 나이트라이드(GaN)는 통신, 방위, 모빌리티 생태계 전반에 걸쳐 주류 기술로 자리매김했습니다. GaN-on-SiC는 열적 견고성 측면에서 성능 벤치마크로 남아 있는 한편, 200mm GaN-on-Si 웨이퍼로의 전환은 기존 LDMOS 대비 비용 격차를 좁혀 가격에 민감한 6GHz 미만 무선 장비에서의 채택을 확대했습니다. 지역적으로, GaN RF 반도체 소자 시장은 아시아태평양 지역의 정책 지원 반도체 자립 추진과 광대역 갭 전자 장비를 우선시하는 미국-EU 국방 현대화 예산의 동시 추진으로 혜택을 받았습니다. 수직 통합 제조업체 간 경쟁 심화로 150mm 및 200mm 에피웨이퍼 병목 현상 완화와 신흥 밀리미터파(mmWave) 및 6G 연구 프로그램의 기판 안정성 확보를 위한 특허 출원, 전략적 인수, 생산 능력 확장이 급증했습니다.

세계의 GaN RF 반도체 장비 시장 동향 및 인사이트

5G 매크로셀 및 스몰셀 구축 가속화로 GaN 채택 확대

중국, 한국, 일본 전역에 설치된 대규모 MIMO 기지국 아키텍처는 최대 64개의 전력 증폭기 채널을 필요로 했으며, 여기서 갈륨 나이트라이드는 LDMOS 대비 15-20%의 에너지 효율 향상을 제공하여 사이트 수준의 운영 비용을 절감했습니다. 오픈 RAN 표준화는 무선 하드웨어를 시스템 공급업체로부터 더욱 분리시켜, 전문 GaN 공급업체들이 원격 무선 헤드 업그레이드용 소켓을 확보할 수 있게 했습니다. 중국 모바일의 기록적 도입은 현장 신뢰성을 입증했으며, Qorvo의 0.013% 고장률은 통신사의 신뢰를 강화했습니다. 200mm 웨이퍼 전환을 통한 USD/W 출력 비용의 점진적 감소는 GaN RF 반도체 장비가 농촌 및 심층 실내 소형 셀 계층으로의 광범위한 침투를 가능케 했습니다. 통신사의 에너지 절감 목표는 GaN의 낮은 발열 특성과 부합하여, 부품 가격보다 효율성 지표를 중시하는 조달 체계 구축을 촉진했습니다.

미국/EU AESA 레이더 현대화가 고출력 수요 주도

미국 국방부는 GaN을 제조 준비도 수준 10(MRL 10)으로 격상시키고 2024-2025년 차세대 레이더 프로그램에 30억 달러 이상을 배정하여 고출력 단일 집적 마이크로파 회로(MMIC)의 다년간 생산 증가를 촉발했습니다. 유럽 각국 국방부도 장거리 감시 및 전자전 장비 교체 주기를 통해 이러한 추세를 반영했으며, GaN의 우수한 전력 밀도는 탐지 범위와 전파 방해 효과를 높였습니다. 해군 저대역 송신기에 GaN을 적용하는 허니웰의 2,990만 달러 규모 계약은 노후화 완화 및 스펙트럼 유연성 확보라는 우선순위를 보여주는 사례다. 200W/mm 열유량을 견디는 패키징 기술 혁신은 상용 통신 라디오로 확산되며 GaN RF 반도체 장비 시장을 방위 산업 영역을 넘어 확장시켰습니다.

비용 프리미엄이 가격 중시의 전개 보급 억제

2024년 기준, 6GHz 미만 라디오용 GaN 전력 증폭기는 LDMOS 대비 40% 가격 차이를 보였으며, 이는 에너지 절감 효과가 가동 18개월 이내에 격차를 상쇄함에도 신흥 시장에서의 전환을 지연시켰습니다. 텍사스 인스트루먼트의 8인치 GaN-on-Si 공정 전환으로 다이 비용이 10% 이상 감소했으나, 거시경제적 압박으로 인해 특히 인도 및 동남아시아 일부 지역의 통신사 설비 투자(capex)는 여전히 제약받았습니다. 이에 통신 장비 제조사들은 이중 공급 전략을 유지하며 LDMOS 생산량을 지속하고, GaN RF 반도체 장비 시장의 단기 성장 가능성을 제한했습니다.

부문 분석

통신 인프라 부문은 2024년 매출의 43.2%를 차지하며 GaN RF 반도체 장비 시장의 핵심을 이루었습니다. 기지국 공급업체들은 GaN을 채택하여 소형화 및 매크로 무선 장비에서 55.2%의 배수 효율 기준을 달성했습니다. 이는 냉각 부하 감소와 타워 상단 중량 경감으로 이어져 고밀도 5G 구축에 핵심적입니다. 오픈-RAN 분산화 추세는 독립형 전력 증폭기 전문업체들의 설계 수주 기회를 확대했으며, 소이텍(Soitec)의 공학 기판은 삽입 손실을 줄여 사이트당 커버리지를 향상시켰습니다. 통신사들이 GaN 프론트엔드를 전제로 한 6G 서브-THz 파일럿 시험을 진행함에 따라 GaN RF 반도체 소자 시장은 2025년까지 성장 모멘텀을 유지했습니다.

2024년 자동차 레이더 시장은 여전히 소규모였으나 2030년까지 연평균 18.5% 성장할 것으로 전망됩니다. 중국의 첨단 운전자 보조 시스템 의무화 정책과 한국의 커넥티드 카 생태계는 79GHz 이미징 레이더 수요를 촉진했으며, GaN은 신뢰성을 저하시키지 않으면서 밀리미터파 전력 밀도를 처리했습니다. GaN PA-LNA 모듈을 적용한 V2X 통신 파일럿은 양산 가능성을 높입니다. 200mm GaN-on-Si 웨이퍼 기반의 비용 절감 로드맵은 주류 차량 전자장비와의 호환성을 약속하며, 더 넓은 GaN RF 반도체 장비 시장의 규모를 창출할 전망입니다.

방위 및 항공우주 분야에서는 레이더, 전자전, 위성통신 페이로드가 GaN의 방사선 내성과 출력 전력을 활용했습니다. 소비자 가전에서는 Wi-Fi 7 라우터와 핸드셋 프런트 엔드에 GaN PA를 채택하며 소신호 시장 가능성을 입증했습니다. 산업용 로봇은 GaN HEMT로 구동되는 6.78MHz 무선 충전 송신기를 도입해 수익원을 다각화하는 산업 간 확장성을 강조했습니다.

2024년 개별 전력 트랜지스터는 46.4% 점유율을 기록했으며, 이는 레이더, 방송, 매크로셀 라디오 전반에 걸쳐 확고한 설계 도입 주기를 반영한 것입니다. MACOM의 포트폴리오는 2W부터 7kW까지 아우르며, GaN RF 반도체 소자 시장의 기반이 된 확장성을 입증했습니다.[2] 열 성능이 강화된 볼트다운 패키지는 80% 이상의 드레인 효율을 지원하여 가혹한 작동 주기에서도 소자 수명을 연장했습니다.

단일 집적 마이크로파 회로(MMIC) 전력 증폭기는 2030년까지 연평균 19.2% 성장률로 가장 빠른 성장세를 보일 전망입니다. 위상 배열 모듈, 공간 제약이 있는 위성 통신 단말기, 밀리미터파 백홀 라디오는 이득 단계와 바이어스 네트워크를 소형 다이로 통합한 MMIC를 선호했습니다. Qorvo의 광대역 QPA2210D는 이 추세를 대표하며, 개별 부품 대비 6dB 높은 전력 추가 효율을 제공합니다. RF 스위치 및 프런트엔드 모듈은 핫 스위칭 스트레스를 처리하기 위해 증강 모드 GaN 트랜지스터를 채택했으며, 저잡음 증폭기는 C-밴드 위성 링크에서 GaAs를 대체하기 시작하여 GaN RF 반도체 장비 산업 지형을 확대하고 있습니다.

GaN RF 반도체 장비 시장은 용도별(방위 및 항공우주, 통신 인프라, 기타), 장비 유형별(분리형 RF 전력 트랜지스터, MMIC/모놀리식 전력 앰프, 기타), 기판 기술별(G aN-On-SiC, GaN-On-Si, 기타), 주파수 대역별(VHF/UHF(1GHz 미만), L/S 밴드(1-4GHz), 기타), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류됩니다.

지역별 분석

아시아태평양 지역은 2024년 매출의 34.1%를 차지하며 선두를 달렸으며, 2030년까지 연평균 18.4%의 성장률을 보일 것으로 예상됩니다. 중국의 5G 기지국 급증, 현지 GaN 파운드리 확충, ‘제3의 반도체 붐’ 정책 지원이 지역 자립을 촉진했습니다. 한국은 AI 센터와 자동차 레이더에 집중한 반면, 일본은 가전 산업의 유산과 SiC 기판 공급을 활용했습니다. 대만의 첨단 백엔드 서비스는 GaN-on-Si 비용 최적화를 가속화하여 GaN RF 반도체 소자 시장 성장 고리를 강화했습니다

북미는 미국 국방 예산과 위성인터넷 초대형 군집에 힘입어 2위를 차지했습니다. 폴라 반도체의 미네소타 GaN-on-Si 프로젝트 등 국내 팹에 대한 정부 지원이 공급망 회복탄력성을 뒷받침했습니다. 캐나다의 통신망 개편과 멕시코의 자동차 전자 클러스터는 대륙적 수요 다각화를 창출해 단일 산업 변동성으로부터 지역 GaN RF 반도체 소자 시장을 보호했습니다.

유럽은 자동차 레이더 분야 선도적 위상과 에너지 효율적인 산업용 드라이브를 결합했습니다. 독일은 79GHz 차량 센서 보급을 주도했고, 프랑스는 항공우주 페이로드를 중점적으로 추진했으며, 영국은 스펙트럼 중심 전자전 업그레이드를 최우선 과제로 삼았습니다. EU 전략적 자율성 패키지는 IQE-X-FAB의 650V GaN 플랫폼과 같은 합작 투자에 보조금을 지원하여 지역화 가치 사슬을 육성했으며, 이는 블록 내 GaN RF 반도체 소자 시장 규모 확장의 기반이 되었습니다. 브라질 전역의 신흥 도입, 걸프협력회의(GCC)의 스마트시티 구축, 호주의 저궤도 백홀 시험은 이 기술의 글로벌 확산 궤적을 보여주었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아태평양 지역 5G 매크로셀 및 소형 셀 구축

- 미국/EU AESA 레이더 현대화 자금 지원

- 저궤도/중궤도 위성통신 콘스텔레이션에서의 페이로드 수요

- 중국 및 한국의 mmWave 자동차용 이미징 레이더 채택

- 인더스트리 4.0 로봇용 고출력 무선 충전

- 오픈-RAN 원격 무선 헤드(RRH)의 급속한 확산

- 시장 성장 억제요인

- 서브-6GHz 기지국에서 LDMOS 대비 비용 프리미엄

- 3kW 초과 전술 레이더 블록에서의 SiC 침투

- 에피웨이퍼와 서브스트레이트공급 병목(150mm와 200mm)

- 200W/mm 초과 시 열 관리 및 신뢰성

- 밸류체인 분석

- 기술의 전망

- GaN-on-Si 양산화와 200mm 웨이퍼로 전환

- 규제 전망

- 5G/6G와 레이더에 관한 ITU와 FCC의 스펙트럼 릴리스

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- GaN RF의 특허 상황

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 용도별

- 방위 및 항공우주

- 통신 인프라

- 소비자 가전

- 자동차(ADAS, V2X)

- 산업 및 에너지

- 데이터센터 및 고효율 전력 링크

- 장비 유형별

- 분리형 RF 전력 트랜지스터

- MMIC/모놀리식 전력 앰프

- RF 스위치 및 프론트엔드 모듈

- 로우 노이즈 드라이버 앰프

- 기판 기술별

- GaN-on-SiC

- GaN-on-Si

- GaN-on-Diamond 및 첨단 복합재료

- 주파수 대역별

- VHF/UHF(1GHz 미만)

- L/S 밴드(1-4GHz)

- C/X 밴드(4-12GHz)

- Ku/Ka 밴드(12-40GHz)

- 밀리미터파(40GHz 초과, 5G FR2 포함)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 대만

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Wolfspeed, Inc.

- Qorvo, Inc.

- Sumitomo Electric Device Innovations

- NXP Semiconductors NV

- MACOM Technology Solutions-GaN-on-SiC

- Broadcom Inc.

- Infineon Technologies AG

- RFHIC Corp.

- Ampleon Netherlands BV

- Mitsubishi Electric Corporation

- Fujitsu Ltd.(GaN RF)

- Northrop Grumman Microelectronics

- Integra Technologies, Inc.

- Analog Devices Inc.

- WIN Semiconductors Corp.

- Finwave Semiconductor Inc.

- Tagore Technology Inc.

- Guerrilla RF

- SEDI-Silent-Solutions Engineering(EU)

- Teledyne e2v HiRel

제7장 시장 기회와 장래의 전망

HBR 25.11.19The GaN RF semiconductor devices market size reached USD 1.60 billion in 2025 and is projected to advance to USD 2.54 billion by 2030, delivering a CAGR of 9.68%.

Rising demand for high-frequency, high-power solutions in 5G infrastructure, active electronically scanned array (AESA) radar, satellite payloads, and 79 GHz automotive imaging radar positioned gallium nitride as a mainstream technology across telecom, defense, and mobility ecosystems. GaN-on-SiC remained the performance benchmark for thermal robustness, while the transition to 200 mm GaN-on-Si wafers compressed cost gaps versus legacy LDMOS, amplifying adoption in price-sensitive sub-6 GHz radio units. Regionally, the GaN RF semiconductor devices market benefited from Asia-Pacific's policy-backed semiconductor self-reliance drive and concurrent U.S.-EU defense modernization budgets that prioritized wide-bandgap electronics. Intensifying competition among vertically integrated manufacturers triggered rapid patent filings, strategic acquisitions, and capacity expansions designed to ease 150 mm and 200 mm epi-wafer bottlenecks and secure substrate resilience for emerging mmWave and 6 G research programs.

Global GaN RF Semiconductor Devices Market Trends and Insights

5G macro- and small-cell roll-outs accelerate GaN adoption

Massive-MIMO base-station architectures installed across China, Korea, and Japan relied on up to 64 power-amplifier channels, where gallium nitride delivered a 15-20% energy-efficiency uplift versus LDMOS, cutting site-level operating costs. Open-RAN standardization further decoupled radio hardware from system vendors, enabling specialist GaN suppliers to win sockets for remote-radio-head upgrades. Record deployments by China Mobile validated field reliability, while Qorvo's 0.013% failure rate reinforced operator confidence. Progressive reductions in USD/W output through 200 mm wafer migration positioned the GaN RF semiconductor devices market for broader penetration of rural and deep-indoor small-cell layers. Telecom carriers' energy-saving targets aligned with GaN's lower heat dissipation, catalyzing procurement frameworks that rewarded efficiency metrics over component price.

U.S./EU AESA radar modernization drives high-power demand

The U.S. Department of Defense elevated GaN to Manufacturing Readiness Level 10 and allocated more than USD 3 billion for next-generation radar programs between 2024-2025, triggering multi-year production ramps for high-power monolithic microwave integrated circuits (MMICs). European ministries mirrored this trajectory through long-range surveillance and electronic-warfare refresh cycles, where GaN's superior power density increased detection range and jamming effectiveness. Honeywell's USD 29.9 million contract to retrofit Navy low-band transmitters with GaN exemplified obsolescence mitigation and spectrum agility priorities. Packaging breakthroughs that survived 200 W/mm heat flux migrated downstream to commercial telecom radios, expanding the GaN RF semiconductor devices market beyond defense silos.

Cost premium tempers penetration in price-sensitive deployments

In 2024, GaN power amplifiers carried a 40% price delta over LDMOS for sub-6 GHz radios, delaying transitions in emerging markets, even though energy savings absorbed the gap within 18 months of operation. Texas Instruments' move to 8-inch GaN-on-Si fabrication lowered die cost by more than 10%, but macroeconomic pressures still constrained carrier capex, especially in India and parts of Southeast Asia. Telecom OEMs, therefore, maintained dual-sourcing strategies, sustaining LDMOS volume and limiting near-term upside for the GaN RF semiconductor devices market.

Other drivers and restraints analyzed in the detailed report include:

- LEO/MEO sat-com constellation payload demand

- mmWave automotive imaging radar adoption in China and South Korea

- Epi-wafer and substrate shortages create production chokepoints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telecom infrastructure accounted for 43.2% of 2024 revenue, anchoring the GaN RF semiconductor devices market. Base-station vendors adopted GaN to unlock smaller footprints and a 55.2% drain efficiency benchmark in macro radio units. This translates to reduced cooling loads and lower tower-top weight, critical for dense 5G rollouts. Open-RAN disaggregation encouraged independent power-amplifier specialists to capture design wins, while Soitec's engineered substrates reduced insertion losses, boosting coverage per site. The GaN RF semiconductor devices market retained momentum through 2025 as operators trialed 6 G sub-THz pilots that presupposed GaN front ends.

Automotive radar remained a modest slice in 2024 but is forecast to expand at an 18.5% CAGR to 2030. China's mandatory advanced-driver-assistance mandates and South Korea's connected-car ecosystem spurred demand for 79 GHz imaging radar, where GaN handled millimeter-wave power density without compromising reliability. V2X communication pilots incorporating GaN PA-LNA modules amplify volume prospects. Cost-down roadmaps tied to 200 mm GaN-on-Si wafers promised alignment with mainstream vehicle electronics, creating scale for the wider GaN RF semiconductor devices market.

Across defense and aerospace, radar, electronic warfare, and sat-com payloads drew on GaN's radiation tolerance and output power. Consumer electronics adopted GaN PAs for Wi-Fi 7 routers and handset front ends, validating smaller-signal opportunities. Industrial robotics embraced 6.78 MHz wireless-charging transmitters powered by GaN HEMTs, underscoring cross-sector breadth that diversified revenue streams.

Discrete power transistors captured 46.4% share in 2024, reflecting entrenched design-in cycles across radar, broadcast, and macro-cell radios. MACOM's portfolio spanned 2 W to 7 kW, illustrating scalability that underpinned the GaN RF semiconductor devices market.[2] Thermal-enhanced bolt-down packages supported >80% drain efficiency, extending device lifetimes in harsh duty cycles.

Monolithic microwave integrated-circuit power amplifiers delivered the fastest growth, projected at 19.2% CAGR through 2030. Phased-array modules, space-constrained sat-com terminals, and mmWave backhaul radios favored MMICs that collapsed gain stages and bias networks into compact dies. Qorvo's wideband QPA2210D exemplified this trend, offering 6 dB higher power-added efficiency versus discrete alternatives. RF switches and front-end modules employed enhancement-mode GaN transistors to handle hot-switching stresses, while low-noise amplifiers began displacing GaAs in C-Band satellite links, broadening the GaN RF semiconductor devices industry landscape.

Gan RF Semiconductor Device Market is Segmented by Application (Defense and Aerospace, Telecom Infrastructure, and More), Device Type (Discrete RF Power Transistors, MMIC / Monolithic Power Amplifiers, and More), Substrate Technology (GaN-On-SiC, GaN-On-Si, and More), Frequency Band (VHF / UHF (<1 GHz), L / S-Band (1-4 GHz), and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific led with 34.1% of 2024 revenue and is projected to advance at an 18.4% CAGR through 2030. China's 5 G base-station surge, local GaN foundry build-outs, and policy support under the "third semiconductor wave" catalyzed regional self-reliance. Korea focused on AI-centers and automotive radar, while Japan leveraged consumer-electronics legacy and SiC substrate supply. Taiwan's advanced backend services accelerated GaN-on-Si cost optimization, reinforcing the GaN RF semiconductor devices market growth loop.

North America ranked second, buoyed by the U.S. defense budget and satellite-internet mega constellations. Government funding for domestic fabs, such as Polar Semiconductor's Minnesota GaN-on-Si project, supported supply-chain resiliency. Canada's telecom revamps and Mexico's automotive-electronics clusters created continental demand diversity that insulated the regional GaN RF semiconductor devices market from single-sector volatility.

Europe combined automotive radar leadership with energy-efficient industrial drives. Germany spearheaded 79 GHz vehicle sensor roll-outs, France emphasized aerospace payloads, and the United Kingdom prioritized spectrum-dominated electronic-warfare upgrades. EU strategic autonomy packages channelled grants to joint ventures such as IQE-X-FAB's 650 V GaN platform, nurturing a localized value chain that underpinned the GaN RF semiconductor devices market size expansion in the bloc. Emerging adoption across Brazil, Gulf Cooperation Council smart-city rollouts, and Australia's low-Earth-orbit backhaul trials showcased the technology's global diffusion trajectory.

- Wolfspeed, Inc.

- Qorvo, Inc.

- Sumitomo Electric Device Innovations

- NXP Semiconductors N.V.

- MACOM Technology Solutions - GaN-on-SiC

- Broadcom Inc.

- Infineon Technologies AG

- RFHIC Corp.

- Ampleon Netherlands B.V.

- Mitsubishi Electric Corporation

- Fujitsu Ltd. (GaN RF)

- Northrop Grumman Microelectronics

- Integra Technologies, Inc.

- Analog Devices Inc.

- WIN Semiconductors Corp.

- Finwave Semiconductor Inc.

- Tagore Technology Inc.

- Guerrilla RF

- SEDI - Silent-Solutions Engineering (EU)

- Teledyne e2v HiRel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G Macro- and Small-Cell Roll-outs across Asia-Pacific

- 4.2.2 U.S./EU AESA Radar Modernization Funding

- 4.2.3 LEO / MEO Sat-Com Constellation Payload Demand

- 4.2.4 mmWave Automotive Imaging Radar Adoption in China and South Korea

- 4.2.5 High-Power Wireless Charging for Industrie 4.0 Robotics

- 4.2.6 Rapid Proliferation of Open-RAN Remote Radio Heads

- 4.3 Market Restraints

- 4.3.1 Cost Premium vs. LDMOS in Sub-6 GHz Base-Stations

- 4.3.2 SiC Encroachment in >3 kW Tactical Radar Blocks

- 4.3.3 Epi-wafer and Sub-strate Supply Bottlenecks (150 and 200 mm)

- 4.3.4 Thermal Management and Reliability at >200 W/mm

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.5.1 GaN-on-Si Mass-Production and 200 mm Transition

- 4.6 Regulatory Outlook

- 4.6.1 ITU and FCC Spectrum Releases for 5G/6G and Radar

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 RF-GaN Patent Landscape

- 4.9 Imapct of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Defense and Aerospace

- 5.1.2 Telecom Infrastructure

- 5.1.3 Consumer Electronics

- 5.1.4 Automotive (ADAS, V2X)

- 5.1.5 Industrial and Energy

- 5.1.6 Data Centers and High-Efficiency Power Links

- 5.2 By Device Type

- 5.2.1 Discrete RF Power Transistors

- 5.2.2 MMIC / Monolithic Power Amplifiers

- 5.2.3 RF Switches and Front-End Modules

- 5.2.4 Low-Noise and Driver Amplifiers

- 5.3 By Substrate Technology

- 5.3.1 GaN-on-SiC

- 5.3.2 GaN-on-Si

- 5.3.3 GaN-on-Diamond and Advanced Composites

- 5.4 By Frequency Band

- 5.4.1 VHF / UHF (<1 GHz)

- 5.4.2 L / S-Band (1-4 GHz)

- 5.4.3 C / X-Band (4-12 GHz)

- 5.4.4 Ku / Ka-Band (12-40 GHz)

- 5.4.5 mmWave (>40 GHz, incl. 5G FR2)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Taiwan

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Wolfspeed, Inc.

- 6.4.2 Qorvo, Inc.

- 6.4.3 Sumitomo Electric Device Innovations

- 6.4.4 NXP Semiconductors N.V.

- 6.4.5 MACOM Technology Solutions - GaN-on-SiC

- 6.4.6 Broadcom Inc.

- 6.4.7 Infineon Technologies AG

- 6.4.8 RFHIC Corp.

- 6.4.9 Ampleon Netherlands B.V.

- 6.4.10 Mitsubishi Electric Corporation

- 6.4.11 Fujitsu Ltd. (GaN RF)

- 6.4.12 Northrop Grumman Microelectronics

- 6.4.13 Integra Technologies, Inc.

- 6.4.14 Analog Devices Inc.

- 6.4.15 WIN Semiconductors Corp.

- 6.4.16 Finwave Semiconductor Inc.

- 6.4.17 Tagore Technology Inc.

- 6.4.18 Guerrilla RF

- 6.4.19 SEDI - Silent-Solutions Engineering (EU)

- 6.4.20 Teledyne e2v HiRel

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment