|

시장보고서

상품코드

1850326

데이터 사이언스 플랫폼 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Data Science Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

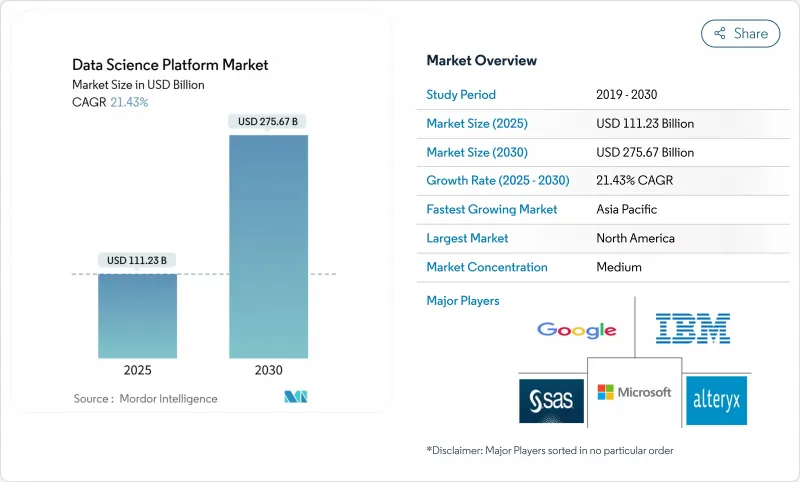

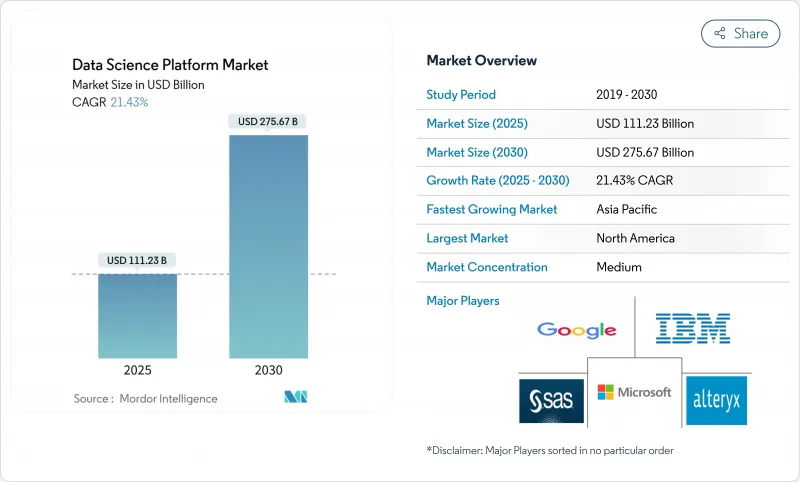

데이터 사이언스 플랫폼 시장 규모는 2025년에 1,112억 3,000만 달러로 평가되고, 2030년에는 2,756억 7,000만 달러로 상승하며, CAGR 21.43%를 나타낼 것으로 예측됩니다.

기업은 머신러닝 운영, 데이터 엔지니어링 및 비즈니스 인텔리전스 워크플로우를 단일 스택에 통합하고 EU의 AI 방법과 유사한 프레임워크 하에서 보다 엄격한 거버넌스 규칙을 충족함에 따라 수요가 확대되고 있습니다. 또한 비구조화된 IoT 및 비디오 스트림을 지원하는 에지 투 클라우드 패브릭의 확장, 확장 가능한 피처 스토어의 필요성, 클라우드 제공업체의 고밀도 GPU 인스턴스 배포도 기세로 이어지고 있습니다. 북미의 리더십은 성숙한 클라우드 인프라에 지지를 받고 있지만 아시아태평양은 제네레티브 AI와 데이터센터용량에 대한 투자를 가속화하고 있으며 급성장 지역의 지위를 지원하고 있습니다. 하이퍼스케일러는 네이티브 AI 툴을 내장하고, 전문 벤더는 오픈 포맷의 데이터 공유, 하이브리드 배포, 도메인 고유의 가속기에 의해 차별화를 도모하기 때문에 경쟁의 격렬함이 증가하고 있습니다.

세계의 데이터 사이언스 플랫폼 시장 동향 및 인사이트

오픈소스 ML 프레임 워크의 보급이 플랫폼 수렴을 촉진

TensorFlow와 PyTorch는 모델 프로토타이핑 시간을 단축하고 분산 트레이닝을 간소화하는 풀 스택 에코시스템으로 진화하여 기업에게 맞춤형 스택에서 프레임워크에 얽매이지 않는 벤더 관리 플랫폼으로의 전환을 촉구하고 있습니다. 그 결과 중견기업은 엔지니어링 오버헤드를 늘리지 않고도 통합된 환경에 연결할 수 있어 Time-to-Value가 가속화됩니다. AI/ML 인프라에 대응하는 특허 패밀리는 전년 대비 45% 증가했으며, 플랫폼 제공업체가 벤더 록인을 회피하고 거버넌스를 강화하기 위해 활용하는 혁신이 지속되고 있음을 나타냅니다.

모델 거버넌스 규제 강화는 매니지드 플랫폼의 보급을 촉진

2024년 8월에 시행된 EU의 AI법은 리스크 관리와 감사 추적의 의무를 부과하며, 컴플라이언스 대시보드, 자동 문서화, 지속적인 모니터링을 내장한 턴키 플랫폼에 유리한 내용이 되었습니다. 역외 적용을 통해 EU 역외 기업도 유럽 고객에게 서비스를 제공하기 위해 유사한 기능을 채택하지 않을 수 없게 되는 한편, 세계 매출의 최대 7%에 이르는 벌칙이 컴플라이언스 위반의 비용을 날카롭게 합니다. 프랑스의 300억 유로(330억 달러) AI 펀드와 같은 정부 이니셔티브는 규정 준수 인프라에 대한 수요를 강화하고 있습니다.

EU 공공 부문의 다중 지역 개발을 방해하는 데이터 거주 장벽

GDPR(EU 개인정보보호규정)과 주권에 관한 규칙에 따라 공공기관은 국경 내에서의 처리를 강요하고 다국간의 전개를 복잡하게 하고 있습니다. EU의 ICT 투자 금액은 미국을 1조 3,600억 달러나 끌어내고 있으며, 국경을 넘는 중소기업의 43%는 지역 내 호스팅을 제공하는 공급자에게 벤더의 선택을 좁히는 입지 규제를 고민하고 있습니다.

부문 분석

플랫폼은 2024년 데이터 사이언스 플랫폼 시장의 72%를 차지했습니다. 이는 인제스트에서 모델 모니터링까지 다루는 통합 툴체인에 대한 기업의 의지를 반영합니다. 그러나 기업은 복잡한 워크로드를 운영하기 위해 권고, 사용자 정의 및 관리 기능을 구매하기 때문에 서비스는 CAGR 24.3%를 나타낼 전망입니다. 공급업체의 수익 모델은 고객의 탈퇴와 컴플라이언스 대응을 보장하기 위해 라이선스와 전문 계약을 융합하는 경향이 커지고 있습니다.

서비스의 기세는 MLOps의 스킬 갭을 배경으로 합니다. 즉, 도입에 대한 전문 지식이 부족한 기업은 설계, 자동화 및 모니터링을 아웃소싱합니다. 결과적으로, 데이터 사이언스 플랫폼 시장 규모에서의 서비스 슬라이스는 2030년까지 꾸준히 확대될 것으로 예측되며, 에코시스템이 순수한 소프트웨어 판매에서 성과 기반의 파트너십으로 이동하고 있음을 확인했습니다.

2024년 데이터 사이언스 플랫폼 시장 점유율은 클라우드 배포가 78%를 차지하며 탄력적인 GPU 클러스터와 AI에 최적화된 스토리지 요구에 힘입었습니다. 공급업체는 2023년 이후 인프라 수익 증가의 절반이 생성형 AI 워크로드에 직접 기인한다고 보고합니다.

향후 CAGR은 21.9%로 클라우드는 여전히 데이터 사이언스 플랫폼 시장의 주요 엔진입니다. 규제가 엄격한 업종에서는 On-Premise나 하이브리드의 도입이 계속되고 있지만, 그러한 유저도, 프로덕션 파이프라인을 소블린 존내에 유지하면서, 개발·테스트 단계를 클라우드에 오프로드하는 케이스가 늘고 있습니다. 에지 노드는 현재 보조 레이어를 형성하고 대기 시간이 중요한 추론을 허용하면서도 중앙 콘솔에서 오케스트레이션을 유지합니다.

데이터 사이언스 플랫폼 시장은 제공 제품별(플랫폼, 서비스), 배치별(On-Premise, 클라우드), 기업 규모별(중소기업, 대기업), 최종 사용자 산업별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 소매 및 E-Commerce, 제조, 기타), 지역별(북미, 유럽, 기타)로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 2025년 1분기 하이퍼스케일러 톱 3사의 클라우드 서비스 매출 684억 달러에 의해 강화되어 2024년 데이터 사이언스 플랫폼 시장 점유율의 40%를 유지했습니다. 벤처기업의 자금 조달, 특허 주도권, 충실한 파트너 에코시스템이 선진적인 도입을 뒷받침하고 있지만, 인프라 비용의 상승으로 공급자는 추가 용량을 위해 1,000억 달러를 넘는 기록적인 자본 예산을 투입하게 됩니다.

아시아태평양은 가장 빠르게 확대되고 있으며 중국의 AI 투자와 인도 데이터센터 설치 면적의 배가를 배경으로 CAGR 25.7%로 성장하고 있습니다. 지역 데이터센터의 가동량은 12GW를 넘어 지속적인 확대의 백본이 되고 있습니다. 호주 '디지털 경제 전략'과 중국 '데이터 팩터 3개년 행동 계획' 등 정부 프로그램은 플랫폼 도입을 뒷받침하는 정책적인 견인력을 창출하고 있습니다.

유럽은 규제 기로에 서 있습니다. EU의 AI법은 플랫폼 수요를 부추기는 하지만, 1조 3,600억 달러의 ICT 투자 갭에 더해, 주권의 필요성으로부터, 프로바이더는 로컬로 호스팅과 암호화를 구축할 수밖에 없습니다. 단편화된 시장은 비용을 상승시키지만 독일 인더스트리 4.0과 프랑스의 AI 자극책(300억 유로/330억 달러) 등의 이니셔티브는 준거한 주권 클라우드 솔루션에 인센티브를 부여합니다. 세계 소훈 클라우드에 대한 투자는 2027년까지 2,500억 달러 이상에 달할 것으로 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 오픈소스 ML 프레임워크의 보급이 플랫폼의 융합을 촉진

- 보다 엄격한 모델 거버넌스 규제(EU AI법 등)가 매니지드 플랫폼의 보급을 촉진

- 엣지 투 클라우드 데이터 패브릭의 채용에 의해 제조업에 있어서 하이브리드 DS 플랫폼을 실현

- 확장 가능한 기능 스토어를 필요로 하는 비구조화 IoT 및 비디오 데이터의 폭발적인 증가가 시장을 견인

- 시장 성장 억제요인

- 데이터 소재지의 장벽이 공공 부문에 있어서 복수 지역에의 전개를 막는 EU

- ML-Ops 엔지니어의 부족이 복잡한 도입을 억제

- 클라우드 요금 상승으로 실시간 트레이닝 워크로드에 대한 예산 되돌림이 발생

- 에너지·유틸리티에 있어서 레거시 데이터 사일로가 플랫폼의 ROI를 지연

- 밸류체인 분석

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시 경제 동향 평가

- 주요 이용 사례

- 생태계 분석

- 가격 설정과 가격 모델

- 데이터 사이언스 플랫폼의 주요 기능(AI/ML, 분석, 시각화, 탐색, 모델링)

제5장 시장 규모와 성장 예측(가치관)

- 제공별

- 플랫폼

- 서비스

- 배포별

- On-Premise

- 클라우드

- 기업 규모별

- 중소기업

- 대기업

- 최종 사용자 업계별

- IT 및 통신

- BFSI

- 소매업 및 전자상거래

- 제조업

- 에너지 및 유틸리티

- 헬스케어 및 생명과학

- 정부 및 방위

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- GCC

- 아랍에미리트(UAE)

- 사우디아라비아

- 카타르

- 기타 GCC 국가

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 지역별 공급업체 순위

- 기업 프로파일

- IBM Corporation

- Google LLC(Alphabet Inc.)

- Microsoft Corporation

- Alteryx Inc.

- SAS Institute Inc.

- Databricks Inc.

- Snowflake Inc.

- Amazon Web Services Inc.

- The MathWorks Inc.

- RapidMiner Inc.

- DataRobot Inc.

- H2O.ai

- TIBCO Software Inc.

- KNIME GmbH

- Domino Data Lab Inc.

- Oracle Corporation

- SAP SE

- Cloudera Inc.

- Qlik Tech International

- Altair Engineering Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.10The data science platform market size is valued at USD 111.23 billion in 2025 and is forecast to climb to USD 275.67 billion in 2030, advancing at a 21.43% CAGR.

Demand escalates as enterprises consolidate machine-learning operations, data engineering, and business-intelligence workflows on a single stack that satisfies tighter governance rules under the EU AI Act and similar frameworks. Momentum also stems from growing edge-to-cloud fabrics that accommodate unstructured IoT and video streams, the need for scalable feature stores, and cloud providers' rollout of high-density GPU instances. North American leadership remains anchored in mature cloud infrastructure, while Asia-Pacific's accelerating investment in generative AI and data-center capacity underpins its status as the fastest-growing region. Competitive intensity is rising as hyperscalers embed native AI tooling and specialist vendors differentiate through open-format data sharing, hybrid deployment, and domain-specific accelerators.

Global Data Science Platform Market Trends and Insights

Proliferation of Open-Source ML Frameworks Catalyzing Platform Convergence

TensorFlow and PyTorch have evolved into full-stack ecosystems that cut model-prototyping time and simplify distributed training, encouraging enterprises to shift from bespoke stacks to vendor-managed platforms that remain framework agnostic. The resulting convergence allows mid-market firms to plug into unified environments without heavy engineering overhead, accelerating time-to-value. Patent families addressing AI/ML infrastructure climbed 45% year-over-year, signaling continued innovation that platform providers harness to avoid vendor lock-in and bolster governance.

Stricter Model-Governance Regulations Triggering Managed-Platform Uptake

The EU AI Act, effective August 2024, imposes risk-management and audit-trail duties that favor turnkey platforms offering built-in compliance dashboards, automated documentation, and continuous monitoring. Extraterritorial reach compels non-EU firms to adopt similar capabilities to serve European customers, while penalties up to 7% of global turnover sharpen the cost of non-compliance. Government initiatives such as France's EUR 30 billion (USD 33 billion) AI fund strengthen demand for compliant infrastructure.

Data-Residency Barriers Hampering Multi-Region Roll-outs in EU Public Sector

GDPR and sovereignty rules force public entities to confine processing within national borders, complicating multinational deployments. The EU trails the US by USD 1.36 trillion in ICT investment, and 43% of cross-border SMEs struggle with location mandates that narrow vendor options to providers offering in-region hosting.

Other drivers and restraints analyzed in the detailed report include:

- Edge-to-Cloud Data-Fabric Adoption Enabling Hybrid Platforms in Manufacturing

- Explosion of Unstructured IoT and Video Data Requiring Scalable Feature Stores

- Shortage of MLOps Engineers Undermining Complex Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platforms contributed 72% of the data science platform market in 2024, reflecting enterprise appetite for integrated toolchains that cover ingestion to model monitoring. Yet services are expanding at a 24.3% CAGR as firms purchase advisory, customization, and managed capabilities to operationalize complex workloads. Vendor revenue models increasingly blend licenses with professional engagements to curb customer churn and assure compliance readiness.

Service momentum traces back to the MLOps skills gap: enterprises lacking deployment expertise outsource design, automation, and monitoring. As a result, the services slice of the data science platform market size is projected to widen steadily through 2030, reinforcing the ecosystem's shift from pure software sales to outcome-based partnerships.

Cloud deployments accounted for 78% of the data science platform market share in 2024, underpinned by the need for elastic GPU clusters and AI-optimized storage. Providers report that half of incremental infrastructure revenue since 2023 stems directly from generative AI workloads.

With a 21.9% CAGR ahead, cloud remains the primary engine of the data science platform market. On-premise and hybrid implementations persist in heavily regulated verticals, but even those users increasingly offload dev-test stages to the cloud while keeping production pipelines within sovereign zones. Edge nodes now form an adjunct layer, enabling latency-critical inference yet remaining orchestrated from centralized consoles.

Data Science Platform Market is Segmented by Offering (Platform, Services), Deployment (On-Premise, Cloud), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (IT and Telecom, BFSI, Retail and E-Commerce, Manufacturing, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 40% of the data science platform market share in 2024, bolstered by USD 68.4 billion in Q1 2025 cloud-service revenue from the top three hyperscalers. Venture funding, patent leadership, and a dense partner ecosystem nurture advanced deployments, though rising infrastructure costs push providers to bankroll record capital budgets exceeding USD 100 billion for additional capacity.

Asia-Pacific is the fastest expanding arena, growing at 25.7% CAGR on the back of China's generative-AI outlays and India's doubling data-center footprint. Regional data-center power surpassed 12 GW operational, providing the backbone for sustained expansion. Government programs such as Australia's Digital Economy Strategy and China's Three-Year Data Factor Action Plan create policy pull that underwrites platform adoption.

Europe sits at a regulatory crossroads: the EU AI Act fuels platform demand, yet a USD 1.36 trillion ICT investment gap plus sovereignty imperatives compel providers to build local hosting and encryption. Fragmented markets raise costs, but initiatives such as Germany's Industry 4.0 and France's AI stimulus (EUR 30 billion / USD 33 billion) incentivize compliant, sovereign-cloud solutions. Global sovereign-cloud spending is forecast to cross USD 250 billion by 2027.

- IBM Corporation

- Google LLC (Alphabet Inc.)

- Microsoft Corporation

- Alteryx Inc.

- SAS Institute Inc.

- Databricks Inc.

- Snowflake Inc.

- Amazon Web Services Inc.

- The MathWorks Inc.

- RapidMiner Inc.

- DataRobot Inc.

- H2O.ai

- TIBCO Software Inc.

- KNIME GmbH

- Domino Data Lab Inc.

- Oracle Corporation

- SAP SE

- Cloudera Inc.

- Qlik Tech International

- Altair Engineering Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Open-Source ML Frameworks Catalyzing Platform Convergence

- 4.2.2 Stricter Model-Governance Regulations (EU AI Act et al.) Triggering Managed-Platform Uptake

- 4.2.3 Edge-to-Cloud Data-Fabric Adoption Enabling Hybrid DS Platforms in Manufacturing)

- 4.2.4 Explosion of Unstructured IoT and Video Data Requiring Scalable Feature Stores Drives the Market

- 4.3 Market Restraints

- 4.3.1 Data-Residency Barriers Hampering Multi-Region Roll-outs in Public Sector EU

- 4.3.2 Shortage of ML-Ops Engineers Undermining Complex Deployments

- 4.3.3 Escalating Cloud Bills Creating Budget Pushback for Real-Time Training Workloads

- 4.3.4 Legacy Data Silos in Energy and Utilities Delaying Platform ROI

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

- 4.8 Key Use Cases

- 4.9 Ecosystem Analysis

- 4.10 Pricing and Pricing Models

- 4.11 Key Capabilities of Data Science Platforms (AI/ML, Analytics, Visualization, Exploration, Modelling)

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Offering

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Manufacturing

- 5.4.5 Energy and Utilities

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Government and Defense

- 5.4.8 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.1.1 United Arab Emirates

- 5.5.5.1.1.2 Saudi Arabia

- 5.5.5.1.1.3 Qatar

- 5.5.5.1.1.4 Rest of GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Vendor Ranking by Region

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Google LLC (Alphabet Inc.)

- 6.4.3 Microsoft Corporation

- 6.4.4 Alteryx Inc.

- 6.4.5 SAS Institute Inc.

- 6.4.6 Databricks Inc.

- 6.4.7 Snowflake Inc.

- 6.4.8 Amazon Web Services Inc.

- 6.4.9 The MathWorks Inc.

- 6.4.10 RapidMiner Inc.

- 6.4.11 DataRobot Inc.

- 6.4.12 H2O.ai

- 6.4.13 TIBCO Software Inc.

- 6.4.14 KNIME GmbH

- 6.4.15 Domino Data Lab Inc.

- 6.4.16 Oracle Corporation

- 6.4.17 SAP SE

- 6.4.18 Cloudera Inc.

- 6.4.19 Qlik Tech International

- 6.4.20 Altair Engineering Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment