|

시장보고서

상품코드

1850353

UV LED : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)UV LED - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

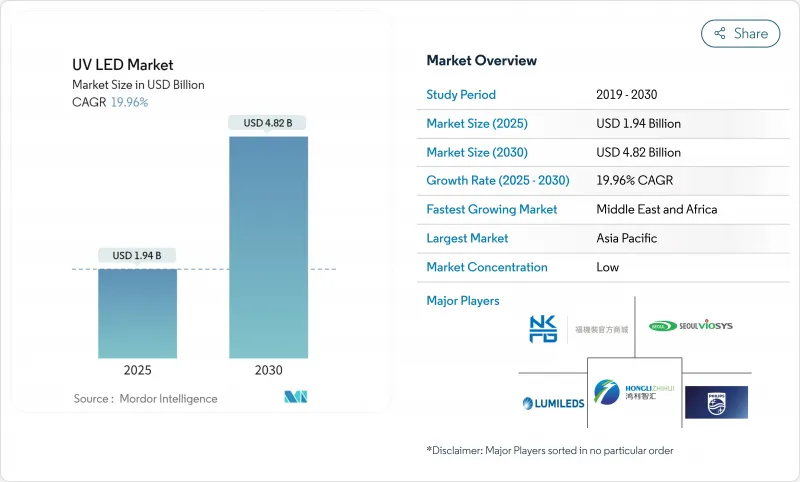

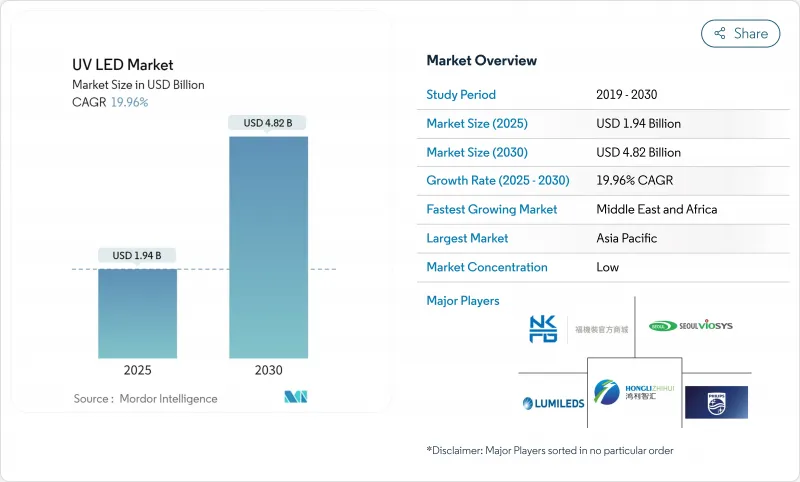

UV LED 시장의 2025년 시장 규모는 19억 4,000만 달러로 평가되었고 2030년에 48억 2,000만 달러에 이를 것으로 예측되며, CAGR은 19.96%를 나타낼 전망입니다.

성장은 전 세계 수은 램프 금지 조치, 에너지 효율적인 경화 솔루션에 대한 수요 급증, 그리고 칩 양자 효율의 급속한 향상으로 추진됩니다. 미나마타 협약, EU RoHS, 캐나다 수은 규정의 규제 일정이 2027-2025년에 집중되면서 최종 사용자들이 UV LED 채택을 추진하고 있습니다. AlGaN 에피택시, 플립칩 구조, 열 관리의 병행 발전으로 심자외선(deep-UV) 장치의 외부 양자 효율이 250mA에서 9.19%로 상승하여 기존 수은 램프와의 성능 격차를 좁혔습니다. 인쇄, 포장, 수처리 분야의 강력한 교체 수요가 2030년까지 공급업체 매출 가시성을 강화하고 있습니다.

세계의 UV LED 시장 동향 및 인사이트

UV LED 채택을 가속화하는 엄격한 수은 램프 단계적 폐지 정책

글로벌 규제로 조명 분야의 수은 사용이 사라지고 있습니다. 미나마타 협약은 147개 서명국이 2027년까지 형광등 사용을 중단하도록 합의했습니다. EU RoHS 지침은 이미 램프당 수은 함량을 5mg으로 제한했으며, 2027년 이후 전면 금지가 예상됩니다. 캐나다의 2025년 규정도 이와 동일한 방향입니다. 사용자가 전환함에 따라 인쇄 라인은 수은 램프를 고체 상태 배열로 교체한 후 에너지 사용량이 85% 감소했다고 보고합니다. 따라서 UV LED 장비를 사전 인증한 공급업체들은 장기적인 개조 계약을 확보하고 있습니다.

아시아 전역에서 급증하는 현장용 수질 소독 수요

급속한 도시화로 인해 인도, 인도네시아, 중국 연안 지역의 중앙 상수도망에 부담이 가중되고 있습니다. 노르웨이 현장 시험에서 LED 반응기를 사용해 하루 545m³의 유량에서 대장균군을 3-log 수준으로 제거하는 데 성공했으며, 이는 도시 상수도 유량에 대한 기술의 실용성을 입증했습니다. 소형 폼 팩터 덕분에 가정용 정수기, 소규모 공장, 농촌 진료소에 UV-C 방출기를 내장할 수 있습니다. 아시아 장비 제조사들은 태양광 마이크로 그리드에서 작동하는 통합 모듈을 확대하며, 오프그리드 수질 안전 시스템 보급을 가속화하고 있습니다.

양자 효율 한계가 고출력 응용을 제약

280nm 미만의 심자외선(Deep-UV) LED는 일반적으로 벽면 플러그 효율이 5% 미만으로, 저압 수은등(20-30%)보다 훨씬 낮습니다. 킬로와트급 출력이 필요한 상수도 업체는 대규모 LED 어레이를 설치해야 하여 자본 비용이 증가합니다. 현재 연구는 정공 주입 및 광 추출 개선을 위해 양자점, 초격자, 투명 기판에 집중되고 있습니다. AlGaN 초격자 설계는 35mW에서 양자 효율(EQE)을 8.6%까지 끌어올렸으나, 이러한 성능의 대량 생산은 아직 수년은 더 걸릴 전망입니다.

부문 분석

UV-A 시스템은 2024년 매출 점유율 72%를 차지하며 그래픽 아트 경화 및 위조품 감지 분야에서 우위를 유지했습니다. 그러나 의료 및 지방자치단체 사용자들이 수은이 없는 살균 솔루션을 도입함에 따라 UV-C는 22.5%의 연평균 성장률(CAGR)을 기록할 전망입니다. ams OSRAM의 OSLON™ UV 3535는 265nm에서 115mW를 출력하며 20,000시간의 수명을 제공하여 신뢰성 있는 수질 및 공기 반응기의 핵심 이정표가 되었습니다. UV-B 틈새 시장은 광치료 및 농업 광형성작용을 대상으로 하여 특수 수요 영역을 개척하고 있습니다.

지역별 도입 동향은 상이합니다. 유럽은 식품 가공 파이프라인에 255-275nm 방출기를 표준화하는 반면, 일본은 피부과용 308nm UV-B를 탐구하고 있습니다. 양자 효율이 지속적으로 향상됨에 따라, 의료용 공기 살균을 목표로 하는 UV-C 모듈의 UV LED 시장 규모는 2030년까지 업계 평균의 두 배로 성장할 것으로 전망됩니다. 원거리 UV-C 222nm 엑시머 방출기의 획기적인 발전은 사람이 있는 공간의 지속적인 안전 소독을 가능케 하여 사용 사례의 경계를 더욱 넓힐 것입니다.

모듈은 통합 용이성으로 인해 2024년 매출의 최대 비중인 42%를 유지했습니다. 그러나 칩은 소비자 기기와 실험실 장비용 맞춤형 광학 엔진 수요를 반영해 23.7%의 연평균 성장률을 기록할 전망입니다. GaN-on-SiC 기판은 열 저항을 줄여 2025년 시제품에서 칩 단위 100mW 출력을 가능케 합니다. 램프 하위 부문은 개조용 소켓을 공급하지만 어레이 방식이 확산되면서 점차 물량이 감소할 전망입니다.

초소형 칩은 신흥 바이오센서 및 랩온어칩(lab-on-a-chip) 장치의 기반이 됩니다. 연구진은 90nm 크기로 20%의 양자효율(EQE)을 달성한 나노 스케일 페로브스카이트 LED를 시연했습니다. 패키징이 세라믹에서 성형 복합재로 전환되면서 밀리와트당 평균 비용이 하락하여 휴대용 살균 기기 전반에 걸쳐 설계 적용이 촉진되고 있습니다. 결과적으로 칩 수준 판매에서 UV LED 시장 점유율은 2030년까지 35%로 상승할 것으로 전망됩니다.

지역 분석

아시아태평양 지역은 2024년 UV LED 시장 매출의 압도적인 55% 점유율을 차지했습니다. 중국의 자급자족 추진은 현지 에피택시 공급업체와 자체 장치 패키징 라인을 양산하고 있습니다. 일본과 한국은 고정밀 제조 노하우를 추가하는 반면, 대만은 심자외선 칩용 질화 갈륨 기판에 특화되어 있습니다. 증가하는 공공 보건 예산은 메가시티 전역에 걸쳐 UV 기반 물 및 공기 정화 수요를 유도하여 지역적 우위를 공고히 하고 있습니다.

북미가 2위를 차지합니다. 캘리포니아주의 수은등 단계적 폐지 가속화와 국내 칩 생산 능력에 대한 연방 자금 지원이 의료 및 첨단 제조업 분야의 채택을 촉진합니다. 그러나 복잡한 특허 얽힘과 높은 인건비가 확장 속도를 제한합니다. 유럽은 에너지 효율 규제로 인해 근접한 3위를 기록합니다. 에코디자인 규정에 따라 2030년까지 설치된 램프의 96%가 LED로 전환될 전망이며, 이는 UV 솔루션에 유리한 환경을 조성합니다.

중동 및 아프리카는 가장 빠르게 성장하는 지역으로, 담수화 시설과 신규 병원에 LED 반응기가 도입되며 연평균 20.4% 성장률을 기록 중입니다. 걸프 국가들은 수은 무함유 조명을 명시한 스마트시티 프로그램을 지원합니다. 남미는 음료 병입 및 양식업 분야에서 성장 동력을 얻고 있으나, 인증 주기로 인해 도시 상수도 프로젝트는 느리게 진행됩니다. 모든 지역에서 규제 강화와 기술 성숙이 동시에 진행되며 UV LED 시장은 수렴적 상승 궤도를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EU와 캘리포니아에서 엄격한 수은 램프 폐지 정책이 UV-LED 도입 가속

- 코로나19 이후 아시아 전역에서 급증하는 사용 지점 수질 소독 수요

- 식품 안전 규정 준수를 위한 유연 포장재에서 저이동성 UV LED 잉크로의 급속한 전환

- 유럽의 에너지 가격 상승이 저전력 UV-LED 경화 라인 선호

- 미니 LED 백라이트 로드맵이 반도체 팹 내 심자외선 검사 장비 채택 촉진

- 공항 및 병원 내 점유 공간 공기 살균을 위한 원거리 UVC(222 nm) 수용 확대

- 시장 성장 억제요인

- AlGaN 기반 UVC 칩의 양자 효율 한계로 인한 고출력 응용 분야 제약

- 북미 시장 신규 진입자의 비용 장벽을 높이는 로열티 부담이 큰 지식재산권 환경

- 산업용 경화 라인을 위한 고밀도 UV LED 어레이의 열 관리 과제

- 신흥 경제국에서의 도시 상수도 프로젝트 지연을 초래하는 느린 인증 주기(NSF/ANSI 55-2022)

- 업계 생태계 분석

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별(파장)

- UV-A

- UV-B

- UV-C

- 제품/형태별

- 램프

- 모듈

- 배열

- 칩

- 출력별

- 저출력(10mW 미만)

- 중출력(10-100mW)

- 고출력(100mW 초과)

- 용도별

- 경화(잉크, 코팅, 접착제)

- 소독 및 멸균

- 센싱 및 계측

- 의료 및 광선요법

- 위조 감지 및 보안

- 원예 및 실내 농업

- 기타 틈새 용도(3D 프린팅, 리소그래피)

- 최종 사용자 업계별

- 헬스케어 및 생명과학

- 인쇄 및 포장

- 전자 및 반도체

- 수도 및 하수도 사업

- 식품 및 음료 가공

- 자동차 및 항공우주

- 주택 및 상업용 빌딩

- 산업 제조

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ams OSRAM AG

- Signify NV

- Nichia Corporation

- Seoul Viosys Co., Ltd.

- Crystal IS Inc.(Asahi Kasei)

- Lumileds Holding BV

- Nikkiso Co., Ltd.(UV Business)

- LG Innotek Co., Ltd.

- LITE-ON Technology Corp.

- Honlitronics(Hongli Zhihui Group)

- Stanley Electric Co., Ltd.

- SemiLEDs Corporation

- Violumas Inc.

- DOWA Electronics Materials Co., Ltd.

- Nordson Corporation

- Luminus Devices, Inc.

- Heraeus Holding GmbH(Noblelight)

- Phoseon Technology(Excelitas)

- Sensor Electronic Technology Inc.(SETi)

- Bolb Inc.

제7장 시장 기회와 장래의 전망

HBR 25.11.19The UV LED market is valued at USD 1.94 billion in 2025 and is forecast to reach USD 4.82 billion by 2030, reflecting a 19.96% CAGR.

Growth is powered by global mercury-lamp bans, surging demand for energy-efficient curing solutions, and rapid gains in chip quantum efficiency. Regulatory timelines under the Minamata Convention, EU RoHS, and Canadian mercury rules converge in 2027-2025, pushing end users toward UV LED adoption, Parallel advances in AlGaN epitaxy, flip-chip structures, and thermal management have lifted external quantum efficiency for deep-UV devices to 9.19% at 250 mA, closing the performance gap with legacy mercury lamps. Strong replacement momentum in printing, packaging, and water treatment is reinforcing supplier revenue visibility through 2030.

Global UV LED Market Trends and Insights

Stringent Mercury-Lamp Phase-Out Policies Accelerating UV LED Adoption

Global regulation is eliminating mercury sources in lighting. The Minamata Convention aligned 147 signatories on a 2027 fluorescent exit. The EU RoHS Directive already caps mercury content at 5 mg per lamp, with full bans expected after 2027. Canada's 2025 rules mirror this direction. As users transition, printing lines report 85% lower energy use after swapping mercury lamps for solid-state arrays. Vendors that pre-qualified UV LED equipment are therefore securing long-term retrofit contracts.

Surge in Point-of-Use Water Disinfection Demand Across Asia

Rapid urbanisation stresses central water grids in India, Indonesia, and coastal China. Field trials in Norway demonstrated 3-log coliform removal at 545 m3/day using LED reactors, validating the technology's viability for municipal flows. Compact form factors allow embedding UV-C emitters in home dispensers, small factories, and rural clinics. Asian equipment makers are scaling integrated modules that operate on solar micro-grids, accelerating off-grid water-safety rollouts.

Quantum Efficiency Ceiling Limiting High-Power Applications

Deep-UV LEDs below 280 nm typically deliver <5% wall-plug efficiency, far below the 20-30% of low-pressure mercury lamps.Water utilities needing kilowatt-scale output must deploy large LED arrays, inflating capital costs. Research now focuses on quantum dots, super-lattices, and transparent substrates to improve hole injection and light extraction. AlGaN super-lattice designs boosted EQE to 8.6% at 35 mW, yet mass manufacturing at such performance remains years away.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift to Low-Migration UV LED Inks in Flexible Packaging

- Energy Price Inflation Favouring Low-Power UV LED Curing Lines

- Royalty-Heavy IP Landscape Raising Cost Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UV-A systems held 72% revenue share in 2024, retaining dominance in graphic-arts curing and counterfeit detection. UV-C, however, is set for a 22.5% CAGR as healthcare and municipal users deploy mercury-free germicidal solutions. ams OSRAM's OSLON(TM) UV 3535 delivers 115 mW at 265 nm with 20,000-hour life, a key milestone for reliable water and air reactors. The UV-B niche addresses phototherapy and agricultural photomorphogenesis, carving specialised demand pockets.

Adoption dynamics vary by region. Europe is standardising 255-275 nm emitters in food-processing pipelines, while Japan explores 308 nm UV-B for dermatology. As quantum-efficiency gains continue, the UV LED market size for UV-C modules targeting medical air sterilisation is projected to grow at double the sector average through 2030. Breakthroughs in far-UVC 222 nm excimer emitters promise human-safe continuous disinfection of occupied spaces, further widening the use-case frontier.

Modules retained the largest 42% slice of 2024 revenue due to integration ease. Chips, though, will post a 23.7% CAGR, reflecting demand for custom optical engines in consumer devices and lab instruments. GaN-on-SiC substrates cut thermal resistance, enabling chip-level powers of 100 mW in 2025 prototypes. The lamps sub-segment serves retrofit sockets but faces gradual volume decline as arrays gain traction.

Ultra-miniaturised chips underpin emerging biosensors and lab-on-a-chip devices. Researchers have demonstrated nano-scale perovskite LEDs with 20% EQE at 90 nm dimensions. As packaging shifts from ceramic to moulded composites, median cost per milliwatt is falling, stimulating design-in across portable sterilisation gadgets. Consequently, the UV LED market share of chip-level sales is forecast to rise to 35% by 2030.

The UV LED Market Report is Segmented by Technology (Wavelength) (UV-A, UV-B, and UV-C), Product/Form Factor (Lamps, Modules, and More), Power Output (Low Power, Medium Power, and More), Application (Curing, Disinfection and Sterilization, and More), End-User Industry (Healthcare and Life Sciences, Printing and Packaging, Automotive and Aerospace, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held a commanding 55% share of UV LED market revenue in 2024. China's self-reliance push is spawning local epitaxy suppliers and captive device packaging lines. Japan and South Korea add high-precision fabrication know-how, while Taiwan specialises in gallium-nitride substrates for deep-UV chips. Rising public-health budgets channel demand for UV-based water and air purification across megacities, cementing regional dominance.

North America ranks second. California's accelerated mercury-lamp phase-out, coupled with federal funding for domestic chip capacity, drives adoption in healthcare and advanced manufacturing. However, a dense patent thicket and higher labour costs temper the expansion pace. Europe follows closely, powered by energy-efficiency mandates. Ecodesign rules forecast that 96% of installed lamps will be LEDs by 2030, creating a receptive environment for UV solutions.

The Middle East & Africa is the fastest-growing area, showing a 20.4% CAGR as desalination plants and new hospitals incorporate LED reactors. Gulf states fund smart-city programmes that specify mercury-free lighting. South America sees momentum in beverage bottling and aquaculture, though municipal water projects move slowly due to certification cycles. Across all geographies, simultaneous regulation and technology maturation keep the UV LED market on a convergent uplift path.

- ams OSRAM AG

- Signify N.V.

- Nichia Corporation

- Seoul Viosys Co., Ltd.

- Crystal IS Inc. (Asahi Kasei)

- Lumileds Holding B.V.

- Nikkiso Co., Ltd. (UV Business)

- LG Innotek Co., Ltd.

- LITE-ON Technology Corp.

- Honlitronics (Hongli Zhihui Group)

- Stanley Electric Co., Ltd.

- SemiLEDs Corporation

- Violumas Inc.

- DOWA Electronics Materials Co., Ltd.

- Nordson Corporation

- Luminus Devices, Inc.

- Heraeus Holding GmbH (Noblelight)

- Phoseon Technology (Excelitas)

- Sensor Electronic Technology Inc. (SETi)

- Bolb Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Mercury Lamp Phase-Out Policies in EU and California Accelerating UV-LED Adoption

- 4.2.2 Surge in Point-of-Use Water Disinfection Demand Post-COVID-19 Across Asia

- 4.2.3 Rapid Shift to Low-Migration UV LED Inks in Flexible Packaging for Food Safety Compliance

- 4.2.4 Energy Price Inflation in Europe Favouring Low-Power UV-LED Curing Lines

- 4.2.5 Mini-LED Backlighting Roadmaps Driving Deep-UV Inspection Tools Adoption in Semiconductor Fabs

- 4.2.6 Growing Acceptance of Far-UVC (222 nm) for Occupied-Space Air Sanitisation in Airports and Hospitals

- 4.3 Market Restraints

- 4.3.1 Quantum Efficiency Ceiling (<5 %) of AlGaN-Based UVC Chips Limits High-Power Applications

- 4.3.2 Royalty-Heavy IP Landscape Raising Cost Barriers for New Entrants in North America

- 4.3.3 Thermal Management Challenges in High-Density UV LED Arrays for Industrial Curing Lines

- 4.3.4 Slow Certification Cycles (NSF/ANSI 55-2022) Delaying Municipal Water Projects in Emerging Economies

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology (Wavelength)

- 5.1.1 UV-A

- 5.1.2 UV-B

- 5.1.3 UV-C

- 5.2 By Product/Form Factor

- 5.2.1 Lamps

- 5.2.2 Modules

- 5.2.3 Arrays

- 5.2.4 Chips

- 5.3 By Power Output

- 5.3.1 Low Power (<10 mW)

- 5.3.2 Medium Power (10-100 mW)

- 5.3.3 High Power (>100 mW)

- 5.4 By Application

- 5.4.1 Curing (Inks, Coatings and Adhesives)

- 5.4.2 Disinfection and Sterilization

- 5.4.3 Sensing and Instrumentation

- 5.4.4 Medical and Phototherapy

- 5.4.5 Counterfeit Detection and Security

- 5.4.6 Horticulture and Indoor Farming

- 5.4.7 Other Niche Applications (3-D Printing, Lithography)

- 5.5 By End-user Industry

- 5.5.1 Healthcare and Life Sciences

- 5.5.2 Printing and Packaging

- 5.5.3 Electronics and Semiconductors

- 5.5.4 Water and Wastewater Utilities

- 5.5.5 Food and Beverage Processing

- 5.5.6 Automotive and Aerospace

- 5.5.7 Residential and Commercial Buildings

- 5.5.8 Industrial Manufacturing

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 South East Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Signify N.V.

- 6.4.3 Nichia Corporation

- 6.4.4 Seoul Viosys Co., Ltd.

- 6.4.5 Crystal IS Inc. (Asahi Kasei)

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Nikkiso Co., Ltd. (UV Business)

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 LITE-ON Technology Corp.

- 6.4.10 Honlitronics (Hongli Zhihui Group)

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 SemiLEDs Corporation

- 6.4.13 Violumas Inc.

- 6.4.14 DOWA Electronics Materials Co., Ltd.

- 6.4.15 Nordson Corporation

- 6.4.16 Luminus Devices, Inc.

- 6.4.17 Heraeus Holding GmbH (Noblelight)

- 6.4.18 Phoseon Technology (Excelitas)

- 6.4.19 Sensor Electronic Technology Inc. (SETi)

- 6.4.20 Bolb Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment